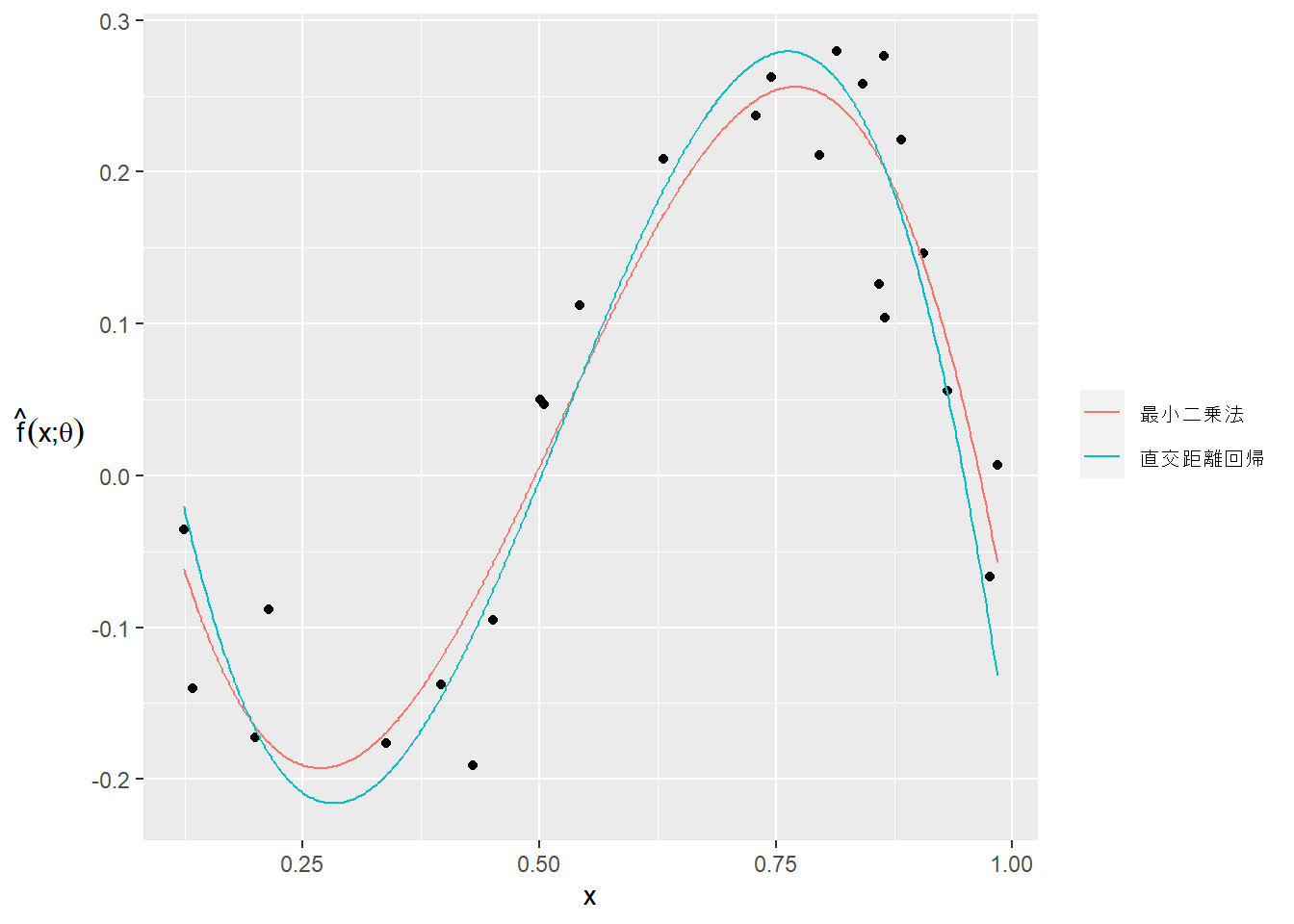

2 Linear functions > 2.1 Linear functions (p.29)

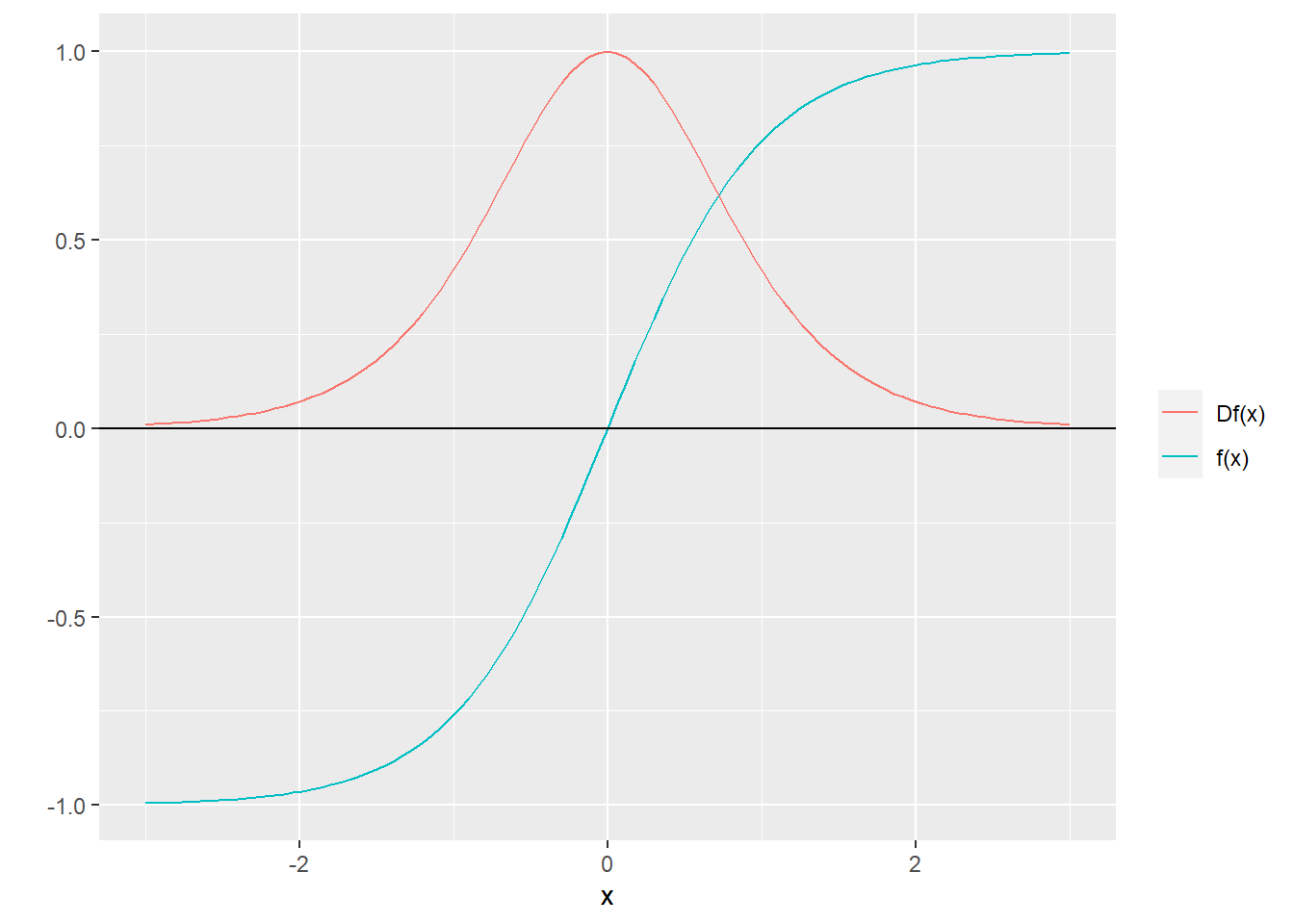

The inner product function. (p.30)

内積の定義は\(\textbf{a},\,\textbf{x}\) を共に\(n\) 次元ベクトルとしたときの \[f(\textbf{x})=\textbf{a}^T\textbf{x}=a_1x_1+a_2x_2+\cdots+a_nx_n\] - 関数\(f\) は\(\textbf{x}\) の重み付け和をとる関数と言える。

Superposition and linearity. (p.30)

\(\textbf{x},\textbf{y}\) を\(n\) 次元ベクトル、\(\alpha,\beta\) をスカラーとしたとき、内積は以下の性質(線形性、重ね合わせ原理)を満たす。

\[\begin{aligned}f(\alpha\textbf{x}+\beta\textbf{y})=\textbf{a}^T(\alpha\textbf{x}+\beta\textbf{y})=\textbf{a}^T(\alpha\textbf{x})+\textbf{a}^T(\beta\textbf{y})=\alpha(\textbf{a}^T\textbf{x})+\beta(\textbf{a}^T\textbf{y})\end{aligned}=\alpha f(\textbf{x})+\beta f(\textbf{y})\]

また、\(f\) が線形ならば、任意の次元に拡張できる。 \[f(\alpha_1\textbf{x}_1+\cdots+\alpha_k\textbf{x}_k)=\alpha_1f(\textbf{x}_1)+\cdots+\alpha_kf(\textbf{x}_k)\]

さらに、 \[\begin{aligned}

f(\alpha_1\textbf{x}_1+\cdots+\alpha_k\textbf{x}_k)

&=\alpha_1f(\textbf{x}_1)+f(\alpha_2\textbf{x}_2+ \cdots+\alpha_k\textbf{x}_k)\\

&=\alpha_1f(\textbf{x}_1)+\alpha_2f(\textbf{x}_2)+f(\alpha_3\textbf{x}_3+ \cdots+\alpha_k\textbf{x}_k)\\

&\,\,\,\vdots\\

&=\alpha_1f(\textbf{x}_1)+\cdots+\alpha_kf(\textbf{x}_k)

\end{aligned}\]

Inner product representation of a linear function. (p.31)

\(n\) 次元ベクトル\(\textbf{x}\) を単位ベクトルを用いて表した上で、

\[f(\textbf{x})=f(x_1e_1+\cdots+x_ne_n)=x_1f(e_1)+\cdots+x_nf(e_n)=\textbf{a}^T\textbf{x}\]

ここで\[\textbf{a}=(f(e_1),f(e_2),\cdots,f(e_n))\]

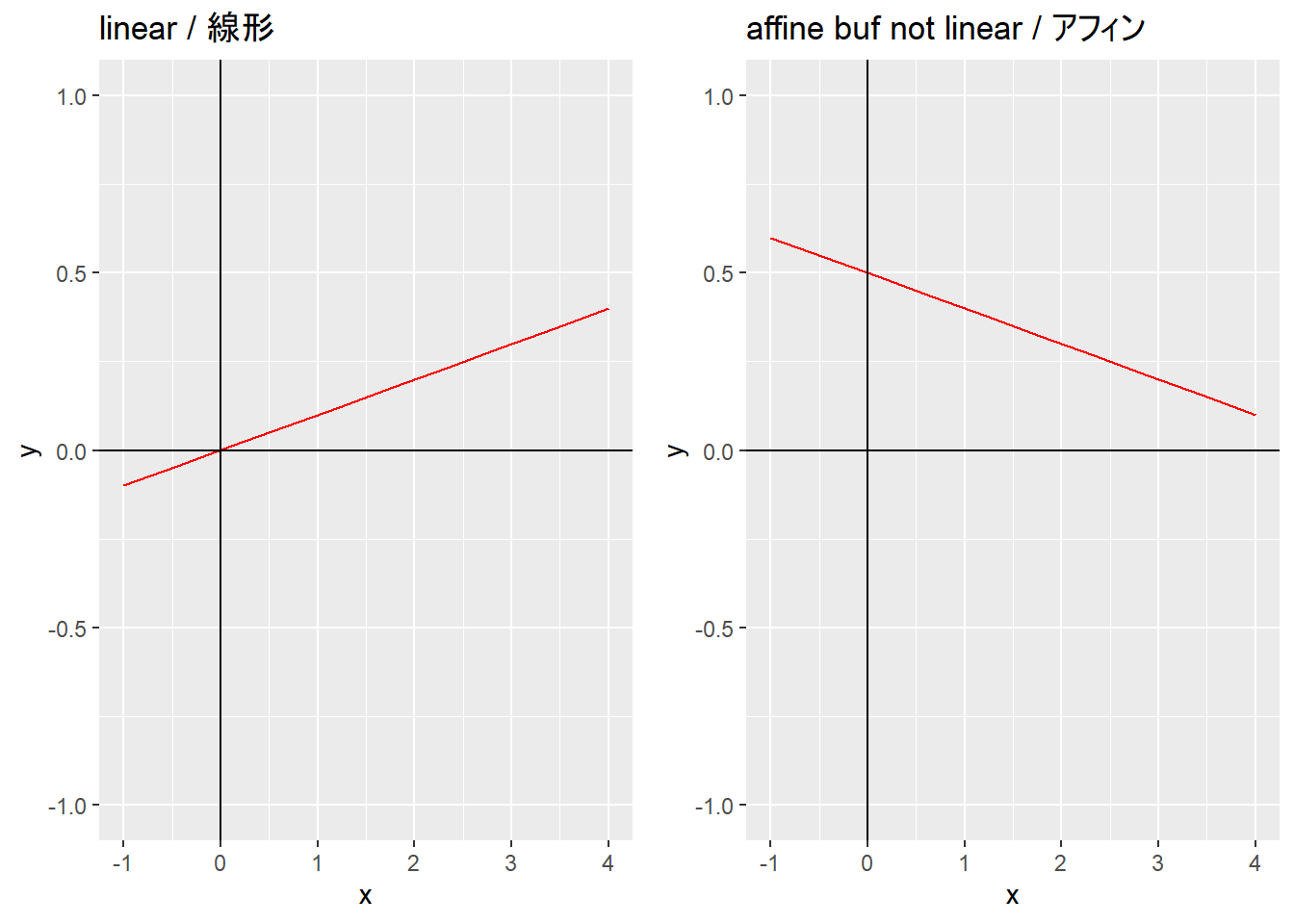

Affine functions. (p.32)

線形関数に定数項を加えた関数がアフィン関数(アフィン変換、アフィン写像)。

\(f(\textbf{x})=\textbf{a}^T\textbf{x}+b\) かつ\(\alpha+\beta=1\) とするとき、 \[\begin{aligned}

f(\alpha\textbf{x}+\beta\textbf{y})

&=\textbf{a}^T(\alpha\textbf{x}+\beta\textbf{y})+b\\

&=\alpha\textbf{a}^T\textbf{x}+\beta\textbf{a}^T\textbf{y}+1\cdot b\\

&=\alpha\textbf{a}^T\textbf{x}+\beta\textbf{a}^T\textbf{y}+(\alpha+\beta)b\\

&=\alpha(\textbf{a}^T\textbf{x}+b)+\beta(\textbf{a}^T\textbf{y}+b)\\

&=\alpha f(\textbf{x})+\beta f(\textbf{y})

\end{aligned}\]

つまり制限を加えた重ね合わせ原理はアフィン関数を意味する。

よって、\(\alpha+\beta=1\) かつ\(f(\alpha\textbf{x}+\beta\textbf{y}\neq\alpha f(\textbf{x})+\beta f(\textbf{y})\) の場合、\(f\) はアフィン関数ではない。

library (ggplot2)library (gridExtra)<- ggplot (data = data.frame (x = seq (- 1 , 4 , 1 )), mapping = aes (x = x)) + stat_function (fun = function (x) 0.1 * x, geom = "line" , n = 10 , color = "red" ) + geom_hline (yintercept = 0 ) + geom_vline (xintercept = 0 ) + ylim (c (- 1 , 1 )) + labs (title = "linear / 線形" )<- ggplot (data = data.frame (x = seq (- 1 , 4 , 1 )), mapping = aes (x = x)) + stat_function (fun = function (x) - 0.1 * x + 0.5 , geom = "line" , n = 10 , color = "red" ) + geom_hline (yintercept = 0 ) + geom_vline (xintercept = 0 ) + ylim (c (- 1 , 1 )) + labs (title = "affine buf not linear / アフィン" ):: as_ggplot (arrangeGrob (g1, g2, ncol = 2 ))

アフィン関数を単位ベクトルを用いて表すと、 \[f(\textbf{x})=f(0)+x_1\left(f(e_1)-f(0)\right)+\cdots+x_n\left(f(e_n)-f(0)\right)\]

ここで\(a_i=f(e_i)-f(0),\quad\,b=f(0)\)

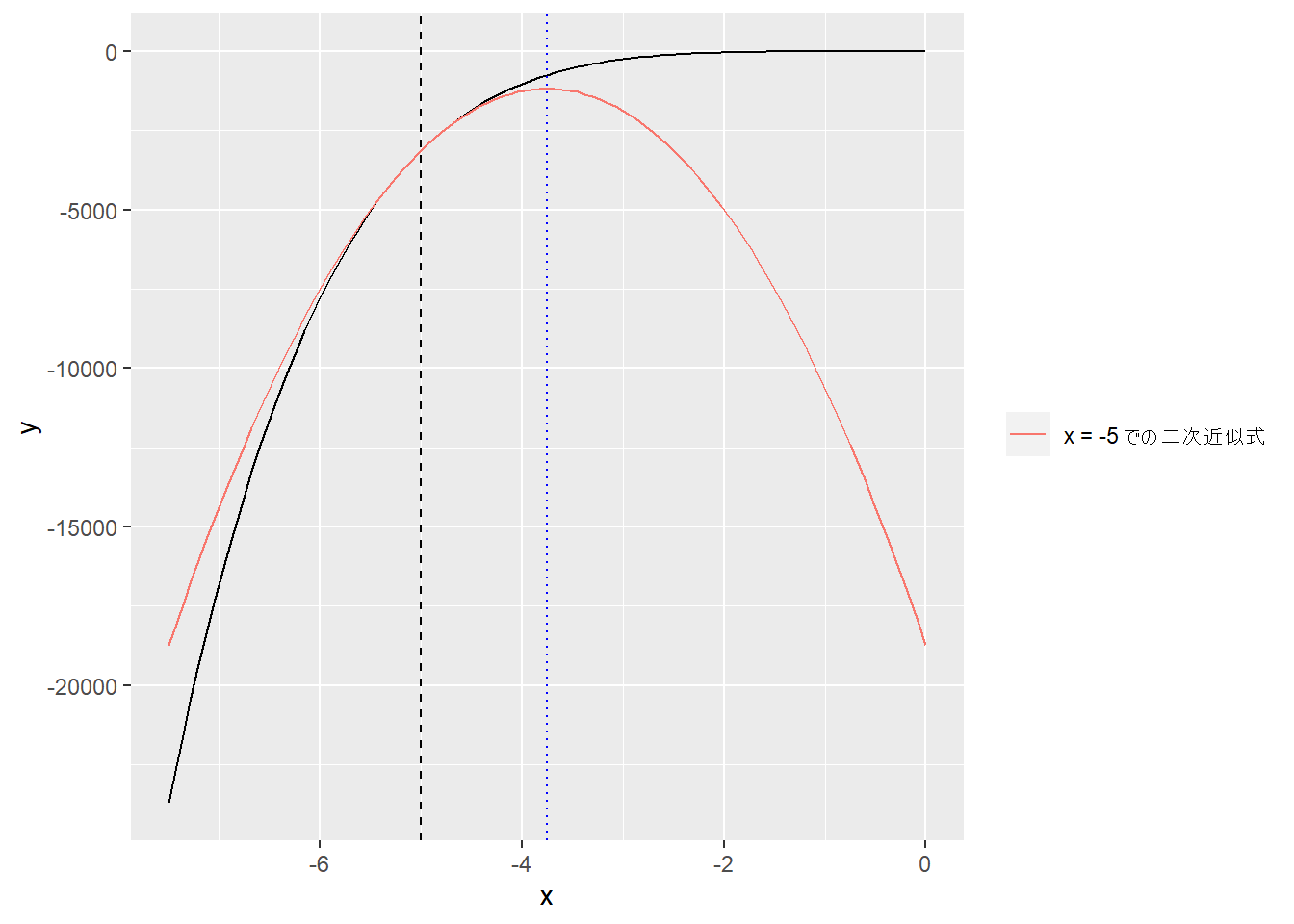

2 Linear functions > 2.2 Taylor approximation (p.35)

アフィンモデルを解くために微分法を利用する。

関数\(f:\textbf{R}^n\rightarrow\textbf{R}\) が微分可能とは、偏微分の存在を意味する。

\(\textbf{z}\) を\(n\) 次元ベクトルとしたとき、\(\textbf{z}\) またはその近傍での一次のテイラー展開は

\[\hat{f}(\textbf{x})=f(\textbf{z})+\dfrac{\partial f}{\partial x_1}(\textbf{z})(x_1-z_1)+\cdots+\dfrac{\partial f}{\partial x_n}(\textbf{z})(x_n-z_n)\]

\(\hat{f}\) は\(\textbf{x}\) のアフィン関数であり、\(z\) における\(f\) の勾配を\(n\) 次元ベクトル\[\nabla f(z)=\begin{bmatrix}\dfrac{\partial f}{\partial x_1}(z)\\\vdots\\\dfrac{\partial f}{\partial x_n}(z)\end{bmatrix}\] とすると、\[\hat{f}(x)=f(z)+\nabla f(z)^T(x-z)\] と表せられる。

第1項は\(x=z\) のときの定数\(f(z)\) であり、第2項は「\(z\) での\(f\) の勾配」と「\(x\) と\(z\) との偏差」の内積である。

一次のテイラー展開は線形関数と定数項との和で表すことができる。

\[\hat{f}(x)=\nabla f(z)^Tx+\left(f(z)-\nabla f(z)^Tz\right)\]

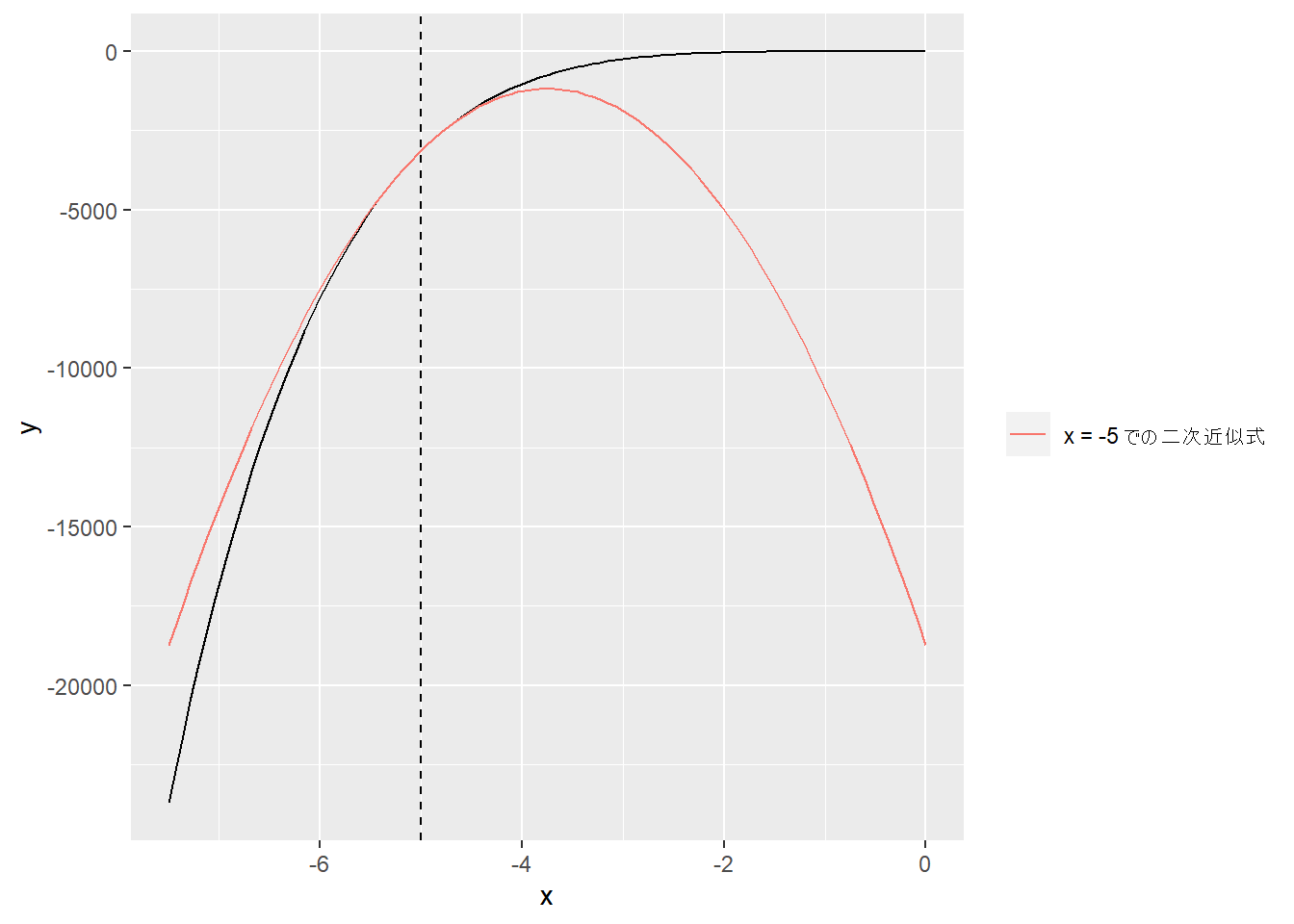

Example. (p.36)

線形でもアフィンでもない\[f(x)=x_1+\textrm{e}^{x_2-x_1}\] を例とする。

勾配は、 \[\nabla f(z)=\begin{bmatrix}1-\textrm{e}^{z_2-z_1}\\\textrm{e}^{z_2-z_1}\end{bmatrix}\]

library (dplyr)<- function (x, z = c (1 , 2 )) {<- function (x) {1 ] + exp (x[2 ] - x[1 ])%>% return ()<- function (z) {c (1 - exp (z[2 ] - z[1 ]), exp (z[2 ] - z[1 ])) %>% return ()<- function (x, z) {f (x = z) + (grad_f (z = z) %*% (x - z))%>% return ()list (x = paste0 ("(" , paste0 (format (x, nsmall = 2 ), collapse = "," ), ")" ),` f(x) ` = f (x) %>% round (4 ),` f_hat(x) ` = f_hat (x = x, z = z) %>% round (4 ),` |f(x)-f_hat(x)| ` = abs (f (x = x) - f_hat (x = x, z = z)) %>% round (4 )<- list ()1 ]] <- c (1.00 , 2.00 )2 ]] <- c (0.96 , 1.98 )3 ]] <- c (1.10 , 2.11 )4 ]] <- c (0.85 , 2.05 )5 ]] <- c (1.25 , 2.41 )lapply (seq (x), function (i) func_1st_taylor (x = x[[i]])) %>% Reduce (function (x, y) rbind (x, y), .)

x f(x) f_hat(x) |f(x)-f_hat(x)|

x "(1.00,2.00)" 3.7183 3.7183 0

y "(0.96,1.98)" 3.7332 3.7326 0.0005

y "(1.10,2.11)" 3.8456 3.8455 0.0001

y "(0.85,2.05)" 4.1701 4.1119 0.0582

y "(1.25,2.41)" 4.4399 4.4032 0.0367

2 Linear functions > 2.3 Regression model (p.38)

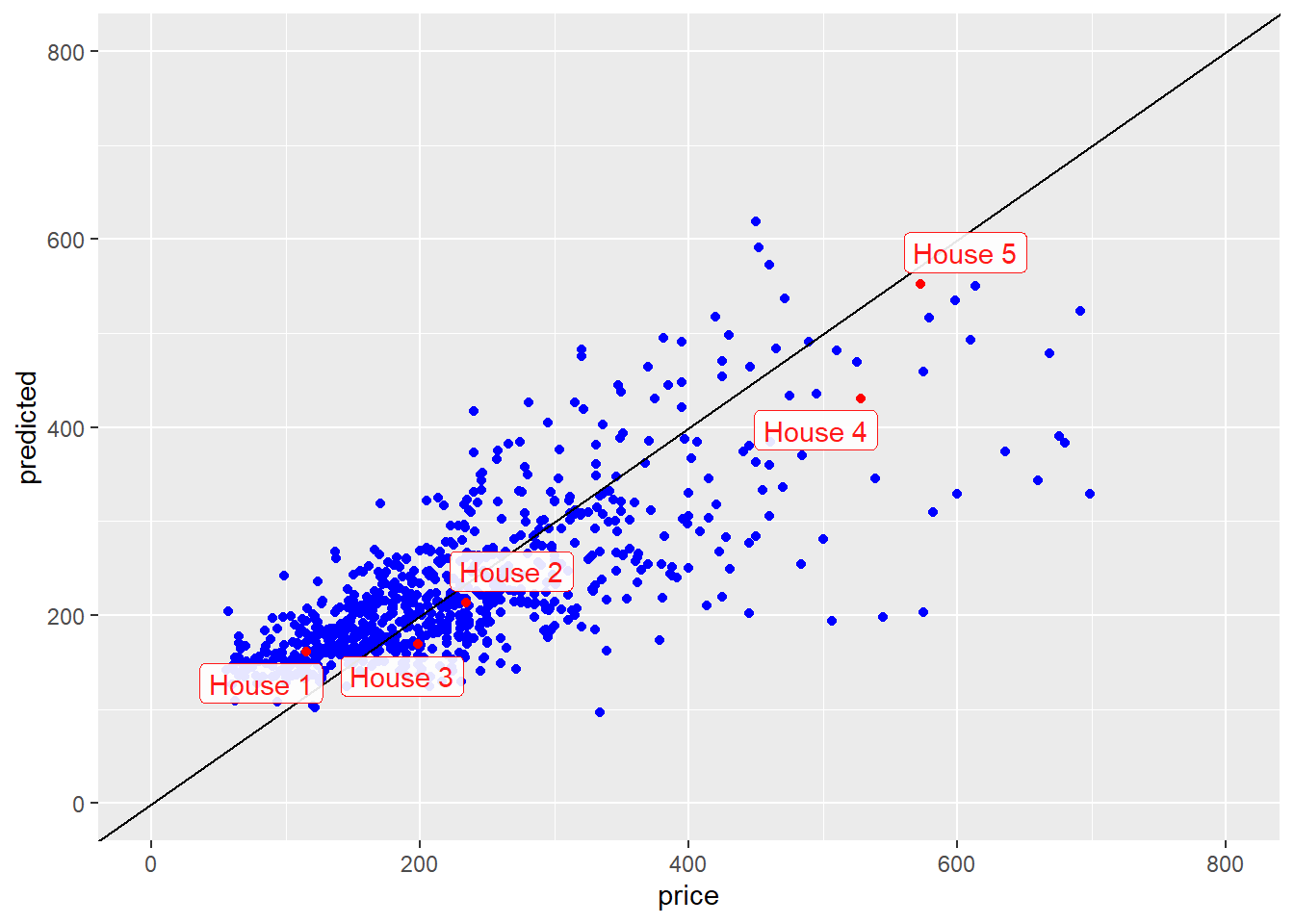

House price regression model. (p.39)

\(y\) :住宅販売価格、\(x_1\) :床面積、\(x_2\) :ベッドルーム数

\[\hat{y}=\textbf{x}^T\beta+v=\beta_1\textbf{x}_1+\beta_2\textbf{x}_2+v\]

# サンプルデータ list (baths = table (baths), location = table (location), price = summary (price),beds = table (beds), area = summary (area), condo = table (condo)

$baths

baths

1 2 3 4 5

166 493 106 8 1

$location

location

1 2 3 4

26 340 338 70

$price

Min. 1st Qu. Median Mean 3rd Qu. Max.

55.42 150.00 208.00 228.77 284.84 699.00

$beds

beds

1 2 3 4 5 6

8 116 380 223 46 1

$area

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.539 1.146 1.419 1.583 1.836 4.303

$condo

condo

0 1

735 39

<- lm (price ~ area + beds) %>% summary () %>% $ coefficients[, 1 ]

(Intercept) area beds

54.40167 148.72507 -18.85336

<- result[2 : 3 ] %>% round (2 )<- result[1 ] %>% round (2 )

<- c (0.846 , 1 ) # 床面積:0.846、ベッドルーム数:1 %*% beta + v # 予測値 which (area == x[1 ])which (area == x[1 ]) %>% beds[.]which (area == x[1 ])] # 実際の価格

[,1]

[1,] 161.3756

[1] 476

[1] 1

[1] 115

<- c (1.324 , 2 ) # 床面積:1.324、ベッドルーム数:2 %*% beta + v # 予測値 which (area == x[1 ])which (area == x[1 ]) %>% beds[.]which (area == x[1 ])] # 実際の価格

[,1]

[1,] 213.6185

[1] 381

[1] 2

[1] 234.5

<- cbind (area, beds) %*% beta + v<- cbind (area = c (0.846 , 1.324 , 1.150 , 3.037 , 3.984 ), beds = c (1 , 2 , 3 , 4 , 5 ),price = c (115.00 , 234.50 , 198.00 , 528.00 , 572.50 )<- cbind (df0, predicted = {1 : 2 ] %*% beta + v%>% as.vector (), obj = paste ("House" , seq (5 ))) %>% data.frame ()ggplot () + geom_point (mapping = aes (x = price, y = predicted), color = "blue" ) + geom_abline (intercept = 0 , slope = 1 ) + xlim (c (0 , 800 )) + ylim (c (0 , 800 )) + geom_point (mapping = aes (x = as.numeric (price), y = as.numeric (predicted)), color = "red" , data = df) + geom_label_repel (mapping = aes (x = as.numeric (price), y = as.numeric (predicted), label = obj),data = df, alpha = 0.9 , color = "red"

3 Norm and distance > 3.1 Norm (p.45)

\(n\) 次元ベクトル\(x\) のユークリッドノルムとは、 \[\|\textbf{x}\|=\displaystyle\sqrt{x_1^2+x_2^2+\cdots+x_n^2}=\displaystyle\sqrt{\textbf{x}^T\textbf{x}}\]

2乗に由来して、\(\|\textbf{x}\|_2\) とも表せられ、「マグニチュード」、「長さ」(ベクトルの次元も長さと呼ばれるため注意)とも呼ばれる。

library (dplyr)<- c (2 , - 1 , 2 ) %>% matrix (ncol = 1 )norm (x = x, type = "2" )^ 2 %>% sum () %>% sqrt ()

<- c (0 , - 1 ) %>% matrix (ncol = 1 )norm (x = x, type = "2" )^ 2 %>% sum () %>% sqrt ()

<- c (3 , - 1 , 2 , 4 ) %>% matrix (ncol = 1 )norm (x = x, type = "1" )%>% abs () %>% sum ()

<- c (3 , - 1 , 2 , 4 ) %>% matrix (ncol = 1 )norm (x = x, type = "i" )%>% abs () %>% max ()

Root-mean-square value. (p.46)

\[\textrm{rms}(\textbf{x})=\displaystyle\sqrt{\dfrac{x_1^2+\cdots+x_n^2}{n}}=\dfrac{\|\textbf{x}\|}{\sqrt{n}}\]

Norm of a sum. (p.46)

2つのベクトル\(x,y\) の合計のノルム

\[\|\textbf{x}+\textbf{y}\|^2=(\textbf{x}+\textbf{y})^T(\textbf{x}+\textbf{y})=\textbf{x}^T\textbf{x}+\textbf{x}^T\textbf{y}+\textbf{y}^T\textbf{x}+\textbf{y}^T\textbf{y}=\|\textbf{x}\|^2+2\textbf{x}^T\textbf{y}+\|\textbf{y}\|^2\]

よって \[\|\textbf{x}+\textbf{y}\|=\displaystyle\sqrt{\|\textbf{x}\|^2+2\textbf{x}^T\textbf{y}+\|\textbf{y}\|^2}\]

Norm of block vectors. (p.47)

\(\textbf{d}=(\textbf{a},\textbf{b},\textbf{c})\) のノルムは、 \[\|\textbf{d}\|^2=\textbf{d}^T\textbf{d}=\textbf{a}^T\textbf{a}+\textbf{b}^T\textbf{b}+\textbf{c}^T\textbf{c}=\|\textbf{a}\|^2+\|\textbf{b}\|^2+\|\textbf{c}\|^2\]

よって \[\|(\textbf{a},\textbf{b},\textbf{c})\|=\displaystyle\sqrt{\|\textbf{a}\|^2+\|\textbf{b}\|^2+\|\textbf{c}\|^2}=\|(\|\textbf{a}\|,\|\textbf{b}\|,\|\textbf{c}\|)\|\]

3 Norm and distance > 3.2 Distance (p.48)

Euclidean distance. (p.48)

ベクトル\(\textbf{a}\) とベクトル\(\textbf{b}\) のユークリッド距離とは、 \[\textbf{dist}(\textbf{a},\textbf{b})=\|\textbf{a}-\textbf{b}\|\]

library (dplyr)<- c (1.8 , 2.0 , - 3.7 , 4.7 )<- c (0.6 , 2.1 , 1.9 , - 1.4 )<- c (2.0 , 1.9 , - 4.0 , 4.6 )list (` u-v ` = norm (u - v, type = "2" ), ` u-w ` = norm (u - w, type = "2" ), ` v-w ` = norm (v - w, type = "2" ))

$`u-v`

[1] 8.367795

$`u-w`

[1] 0.3872983

$`v-w`

[1] 8.532878

\(u\) と\(v\) では\(u\) の方が\(w\) に近く、\(w\) と\(v\) では\(w\) の方が\(u\) に近い。

Units for heterogeneous vector entries. (p.51)

2つの\(次元n\) ベクトル\(\textbf{x}\) と\(\textbf{y}\) の距離の2乗は、 \[\|\textbf{x}-\textbf{y}\|^2=(x_1-y_1)^2+\cdots+(x_n-y_n)^2\]

# 第1成分は床面積(1000ft^2)、第2成分はベッドルーム数 <- c (1.6 , 2 )<- c (1.5 , 2 )<- c (1.6 , 4 )list (` x-y ` = norm (x - y, type = "2" ), ` x-z ` = norm (x - z, type = "2" ), ` y-z ` = norm (y - z, type = "2" ),` x ` = norm (x, type = "2" ), ` y ` = norm (y, type = "2" ), ` z ` = norm (z, type = "2" )

$`x-y`

[1] 0.1

$`x-z`

[1] 2

$`y-z`

[1] 2.002498

$x

[1] 2.56125

$y

[1] 2.5

$z

[1] 4.308132

\(\textbf{x}\) と\(\textbf{y}\) が最も近い。

# 第1成分は床面積(ft^2)、第2成分はベッドルーム数 <- c (1600 , 2 )<- c (1500 , 2 )<- c (1600 , 4 )list (` x-y ` = norm (x - y, type = "2" ), ` x-z ` = norm (x - z, type = "2" ), ` y-z ` = norm (y - z, type = "2" ),` x ` = norm (x, type = "2" ), ` y ` = norm (y, type = "2" ), ` z ` = norm (z, type = "2" )

$`x-y`

[1] 100

$`x-z`

[1] 2

$`y-z`

[1] 100.02

$x

[1] 1600.001

$y

[1] 1500.001

$z

[1] 1600.005

\(\textbf{x}\) と\(\textbf{z}\) が最も近い。つまり単位(unit)の取り方に依存する。

3 Norm and distance > 3.3 Standard deviation (p.52)

\(n\) 次元ベクトル\(\textbf{x}\) のStandard deviation(標準偏差)とは、平均除去後の\(\textbf{x}\) のRMSのこと。

\[\textbf{std}(\textbf{x})=\displaystyle\sqrt{\dfrac{(x_1-\textbf{avg}(\textbf{x}))^2+\cdots+(x_n-\textbf{avg}(\textbf{x}))^2}{n}}\]

library (dplyr)<- c (1 , - 2 , 3 , 2 )# 標本標準偏差 sum ((x - mean (x))^ 2 ) / length (x)%>% ^ 0.5

# 不偏標準偏差 sum ((x - mean (x))^ 2 ) / (length (x) - 1 )%>% ^ 0.5 sd (x)

[1] 2.160247

[1] 2.160247

Standardization. (p.56)

標準化したベクトル\(\textbf{x}\) とは

\[\textbf{z}=\dfrac{1}{\textbf{std}(\textbf{x})}(\textbf{x}-\textbf{avg}(\textbf{x})\textbf{1})\]

ここで\(\textbf{1}\) は、全ての要素が1のベクトル(VMLS p.5)。

5 Linear independence > 5.4. Gram-Schmidt algorithm (p.97)

Example. (p.100)

library (dplyr)<- function (a, tolerance = 1e-7 ) {# Reference https://ses.library.usyd.edu.au/handle/2123/21370 # a: matrix,linearly independent <- list ()for (i in seq (nrow (a))) {<- a[i, ]if (length (q) != 0 ) {for (j in seq (length (q))) {<- q_tilde - (q[[j]] %*% a[i, ]) * q[[j]]<- q_tilde^ 2 %>% sum () %>% sqrt ()if (root_sum_square < tolerance) {break else {<- q_tilde / root_sum_square<- q_tildereturn (list (a = a, q = q, root_sum_square = root_sum_square, i = i))

# 例1 <- func_Gram_Schmidt_orthonormalization (a = rbind (c (- 1 , 1 , - 1 , 1 ), c (- 1 , 3 , - 1 , 3 ), c (1 , 3 , 5 , 7 )))

$a

[,1] [,2] [,3] [,4]

[1,] -1 1 -1 1

[2,] -1 3 -1 3

[3,] 1 3 5 7

$q

$q[[1]]

[1] -0.5 0.5 -0.5 0.5

$q[[2]]

[1] 0.5 0.5 0.5 0.5

$q[[3]]

[1] -0.5 -0.5 0.5 0.5

$root_sum_square

[1] 4

$i

[1] 3

<- result$ qsapply (seq (q), function (x) q[[x]] %>% norm (type = "2" ))combn (seq (q), 2 ) %>% apply (MARGIN = 2 , function (x) q[[x[1 ]]] %*% q[[x[2 ]]])

# 例2 <- func_Gram_Schmidt_orthonormalization (a = sample (0 : 50 , 15 , replace = F) %>% matrix (nrow = 5 ))

$a

[,1] [,2] [,3]

[1,] 36 33 8

[2,] 38 26 39

[3,] 3 18 24

[4,] 14 9 1

[5,] 31 42 25

$q

$q[[1]]

[1] 0.7274583 0.6668368 0.1616574

$q[[2]]

[1] 0.02175702 -0.25789902 0.96592687

$q[[3]]

[1] -0.6858069 0.6991543 0.2021192

$root_sum_square

[1] 0.000000000000005941509

$i

[1] 4

<- result$ qsapply (seq (q), function (x) q[[x]] %>% norm (type = "2" ))combn (seq (q), 2 ) %>% apply (MARGIN = 2 , function (x) q[[x[1 ]]] %*% q[[x[2 ]]])

[1] 1 1 1

[1] 0.00000000000000011102230 -0.00000000000000027755576

[3] -0.00000000000000008326673

6 Matrices > 6.3 Transpose, addition, and norm > 6.3.4 Matrix norm (p.117)

\((m\times n)\) 行列\(A\) のノルム(フロベニウスノルム (Frobenius norm) )\(\|\textbf{A}\|\) は、 \[\|\textbf{A}\|=\displaystyle\sqrt{\displaystyle\sum_{i=1}^m\displaystyle\sum_{j=1}^n}A_{ij}^2\]

10 Matrix multiplication > 10.4 QR factorization (p.189)

<- function (A) {# Reference https://ses.library.usyd.edu.au/handle/2123/21370 <- func_Gram_Schmidt_orthonormalization (a = t (A))<- buf$ q %>% Reduce (function (x, y) rbind (x, y), .)<- Q_transpose %*% A<- Q_transpose %>% t ()<- Q %*% R<- Q %*% t (Q)return (list (A = A, QR = QR, R = round (R, 10 ), Q = round (Q, 10 ), QQt = round (QQt, 10 )))<- 5 <- rbind (rnorm (n = n) %>% round (2 ), rnorm (n = n) %>% round (2 ), rnorm (n = n) %>% round (2 ))func_QR_factorization (A = A)

$A

[,1] [,2] [,3] [,4] [,5]

[1,] 0.76 0.05 0.79 0.59 1.39

[2,] -1.33 0.12 0.86 -1.06 -0.78

[3,] 0.50 -1.30 0.20 -1.30 0.54

$QR

[,1] [,2] [,3] [,4] [,5]

[1,] 0.76 0.05 0.79 0.59 1.39

[2,] -1.33 0.12 0.86 -1.06 -0.78

[3,] 0.50 -1.30 0.20 -1.30 0.54

$R

[,1] [,2] [,3] [,4] [,5]

x 1.611366 -0.4788484 -0.2751703 0.7497987 1.46695423

y 0.000000 1.2155674 -0.2048960 1.6052914 -0.01945699

y 0.000000 0.0000000 1.1340189 -0.1501386 0.82447966

$Q

x y y

[1,] 0.4716496 0.2269299 0.8520854

[2,] -0.8253867 -0.2264252 0.5171735

[3,] 0.3102958 -0.9472246 0.0805116

$QQt

[,1] [,2] [,3]

[1,] 1 0 0

[2,] 0 1 0

[3,] 0 0 1

11 Matrix inverses > 11.3 Solving linear equations (p.207)

Back substitution. (p.207)

\(\textbf{R}\) を\((n\times n)\) の上三角行列(対角成分は全て非ゼロ。故に逆行列を持つ)として、\(\textbf{Rx}=\textbf{b}\) を解く。

対角成分より下は全てゼロであるため、 \[\begin{aligned}

R_{11}x_1+R_{12}x_2+\cdots+R_{1,n-1}x_{n-1}+R_{1n}x_n&=b_1\\

&\,\,\,\vdots\\

R_{n-2,n-2}x_{n-2}+R_{n-2,n-1}x_{n-1}+R_{n-2,n}x_{n}&=b_{n-2}\\

R_{n-1,n-1}x_{n-1}+R_{n-1,n}x_{n}&=b_{n-1}\\

R_{nn}x_{n}&=b_{n}\\

\end{aligned}\]

最後の行は\(x_{n}=b_{n}/R_{nn}\) となり、\(b_n\) も\(R_{nn}\) も与えられているため\(x_n\) が求められる。求めた\(x_n\) を下から2行目の式に代入すると、

\[x_{n-1}=(b_{n-1}-R_{n-1,n}x_n)/R_{n-1,b-1}\]

求めた\(x_{n-1}\) を下から3行目に代入して、と繰り返すと事によって、\(x_{n-2},x_{n-3},\cdots,x_1\) が求められる(後退代入(back substitution))。

後退代入により\(\textbf{Rx}=\textbf{b},\quad \textbf{x}=\textbf{R}^{-1}\textbf{b}\) が求められる。

library (dplyr)<- function (R, b) {<- nrow (R)<- rep (0 , n)for (i in rev (seq (n))) {<- b[i]<- iwhile (j < n) {<- x[i] - R[i, j + 1 ] * x[j + 1 ]<- j + 1 <- x[i] / R[i, i]return (x)<- runif (n = 16 ) %>% matrix (nrow = 4 ) %>% lower.tri (.)] <- 0 <- runif (n = 4 )list (R = R, b = b)

$R

[,1] [,2] [,3] [,4]

[1,] 0.6354191 0.377014 0.4446053 0.9687880

[2,] 0.0000000 0.686691 0.8987399 0.2545610

[3,] 0.0000000 0.000000 0.1691899 0.4926958

[4,] 0.0000000 0.000000 0.0000000 0.2151477

$b

[1] 0.5109851 0.5065029 0.6984124 0.2275627

<- func_back_substitution (R = R, b = b)<- %*% x%>% as.vector ()<- solve (R) %*% b%>% as.vector ()cbind (Rx, b, x, inv_Rb)

Rx b x inv_Rb

[1,] 0.5109851 0.5109851 -0.9329253 -0.9329253

[2,] 0.5065029 0.5065029 -1.0259244 -1.0259244

[3,] 0.6984124 0.6984124 1.0478511 1.0478511

[4,] 0.2275627 0.2275627 1.0577045 1.0577045

11 Matrix inverses > 11.4 Examples (p.210)

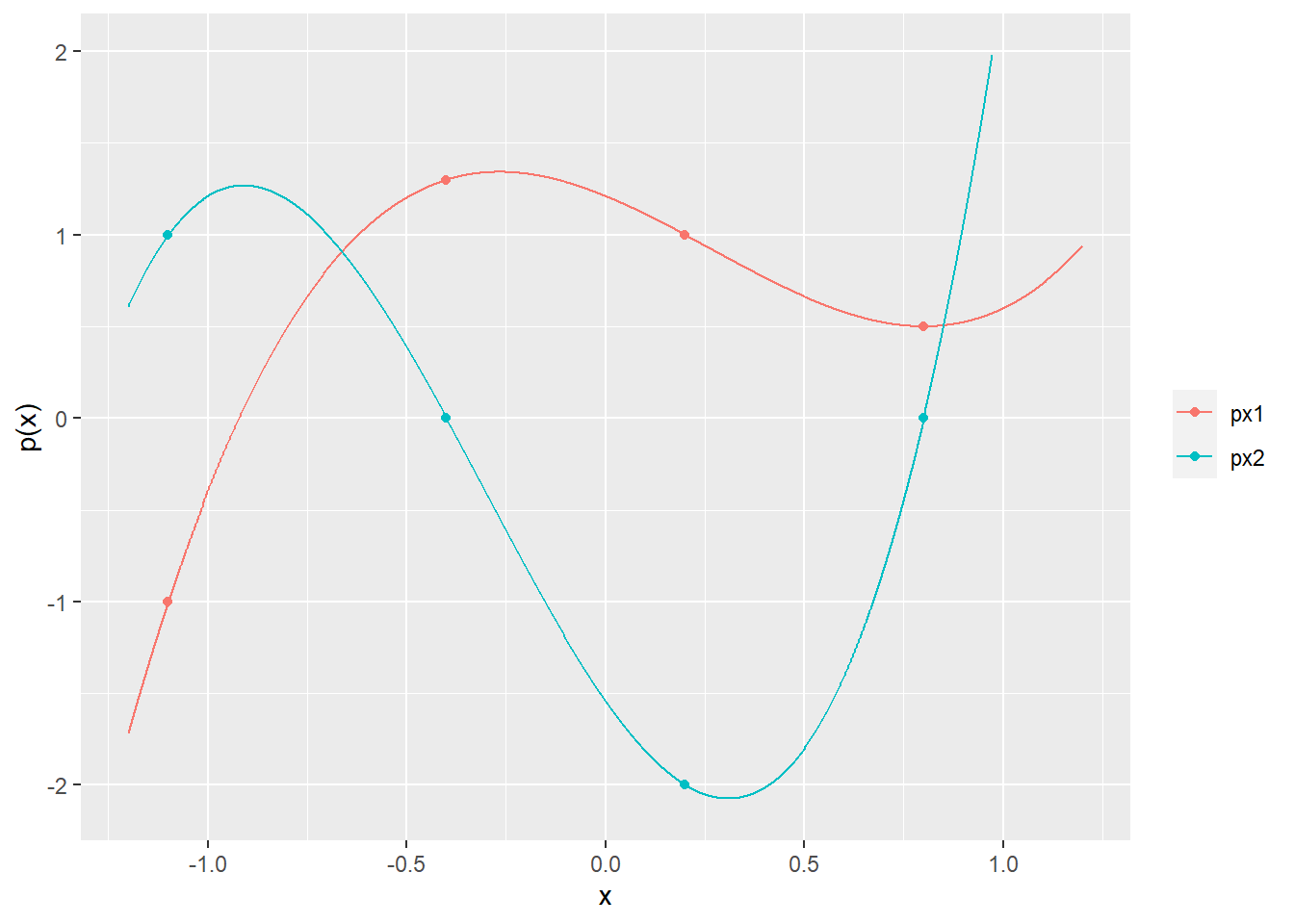

Polynomial interpolation. (p.210)

次の3次多項式について、 \[p(x)=c_1+c_2x+c_3x^2+c_4x^3\]

\[p(-1.1)=b_1,\quad p(-0.4)=b_2,\quad p(0.2)=b_3,\quad p(0.8)=b_4\] を満たす係数\(c\) を求める。

行列表現は\(\textbf{Ac}=\textbf{b}\) となり、\(\textbf{A}\) は \[\textbf{A}=\begin{bmatrix}

1&-1.1&(-1.1)^2&(-1.1)^3\\

1&-0.4&(-0.4)^2&(-0.4)^3\\

1&0.2&(0.2)^2&(0.2)^3\\

1&0.8&(0.8)^2&(0.8)^3

\end{bmatrix}\] となる、ヴァンデルモンド行列。

よって、\(\textbf{c}=\textbf{A}^{-1}\textbf{b}\) を解くと、

library (dplyr)library (tidyr)library (ggplot2)<- c (- 1.1 , - 0.4 , 0.2 , 0.8 )<- outer (X = x0, Y = seq (3 + 1 ) - 1 , FUN = "^" )# <- c (- 1.0 , 1.3 , 1.0 , 0.5 ) # x0のとき、左の点を通過するような c を求める。 <- solve (A) %*% b1# <- c (1.0 , 0.0 , - 2.0 , 0.0 ) # x0のとき、左の点を通過するような c を求める。 <- solve (A) %*% b2# <- seq (- 1.2 , 1.2 , length.out = 1000 )<- outer (X = x, Y = seq (3 + 1 ) - 1 , FUN = "^" )<- A %*% c1<- A %*% c2# <- data.frame (x, px1, px2) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ])<- data.frame (x = x0, px1 = b1, px2 = b2) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ])# ggplot () + geom_line (data = tidydf, mapping = aes (x = x, y = value, col = key)) + labs (x = "x" , y = "p(x)" ) + theme (legend.title = element_blank ()) + geom_point (mapping = aes (x = x, y = value, col = key), data = pointdf) + ylim (c (- 2.1 , 2 ))

Balancing chemical reactions. (p.211)

次の化学反応式と解く \[a_1\textrm{Cr}_2\textrm{O}_7^{2-}+a_2\textrm{Fe}^{2+}+a_2\textrm{H}^{+}\rightarrow b_1\textrm{Cr}^{3+}+b_2\textrm{Fe}^{3+}+b_3\textrm{H}_2\textrm{O}\]

library (dplyr)<- c ("Cr" , "O" , "Fe" , "H" , "イオン価" )# 反応物(Reactant) <- c (2 , 7 , 0 , 0 , - 2 , 0 , 0 , 1 , 0 , 2 , 0 , 0 , 0 , 1 , 1 ) %>% matrix (ncol = 3 )row.names (R) <- atoms# 生成物(product) <- c (1 , 0 , 0 , 0 , 3 , 0 , 0 , 1 , 0 , 3 , 0 , 1 , 0 , 2 , 0 ) %>% matrix (ncol = 3 )row.names (P) <- atomslist (R = R, P = P)

$R

[,1] [,2] [,3]

Cr 2 0 0

O 7 0 0

Fe 0 1 0

H 0 0 1

イオン価 -2 2 1

$P

[,1] [,2] [,3]

Cr 1 0 0

O 0 0 1

Fe 0 1 0

H 0 0 2

イオン価 3 3 0

\(a_1=1\) を条件とした場合、

# 係数行列 <- cbind (R, - 1 * P) %>% rbind (., c (1 , 0 , 0 , 0 , 0 , 0 ))# 目的変数 <- c (0 , 0 , 0 , 0 , 0 , 1 )# solve (A) %*% b %>% row.names (.) <- c ("a1" , "a2" , "a3" , "b1" , "b2" , "b3" )t (.)

a1 a2 a3 b1 b2 b3

[1,] 1 6 14 2 6 7

11 Matrix inverses > 11.5 Pseudo-inverse (p.214)

Numerical example. (p.216)

非正方行列\(\textbf{A}\) およびベクトル\(\textbf{b}\) を次のとおりとして\(\textbf{Ax}=\textbf{b}\) と解く。

library (dplyr)<- c (- 3 , 4 , 1 , - 4 , 6 , 1 ) %>% matrix (ncol = 2 )<- c (1 , - 2 , 0 )

列ベクトルが線形独立な行列\(\textbf{A}\) をQR分解

<- qr (A)<- qr.Q (QR)<- qr.R (QR)list (Q = Q, R = R)

$Q

[,1] [,2]

[1,] -0.5883484 -0.4576043

[2,] 0.7844645 -0.5229764

[3,] 0.1961161 0.7190925

$R

[,1] [,2]

[1,] 5.09902 7.2562970

[2,] 0.00000 -0.5883484

擬似逆行列\(\textbf{A}^+\) を求める。

\[\textbf{A}^+=\textbf{R}^{-1}\textbf{Q}^T\]

<- {solve (R) %*% t (Q)

[,1] [,2] [,3]

[1,] -1.2222222 -1.1111111 1.777778

[2,] 0.7777778 0.8888889 -1.222222

# 擬似逆行列を利用して x を求める。 <- pseudo_inverse_A %*% b

# 確認 cbind (Ax = A %*% x %>% round (10 ) %>% as.vector (), b = b)

Ax b

[1,] 1 1

[2,] -2 -2

[3,] 0 0

12 Least squares > 12.1 Least squares problem (p.225)

\[\textbf{A}=\textbf{xb}\]

library (dplyr)<- c (2 , 0 , - 1 , 1 , 0 , 2 ) %>% matrix (nrow = 3 , byrow = T)<- c (1 , 0 , - 1 ) %>% matrix (ncol = 1 )# 優決定系(over-determined)故に解無し。

\[\hat{\textbf{x}}=\left(\textbf{A}^{'}\textbf{A}\right)^{-1}\textbf{A}^{'}\textbf{b}=\textbf{A}^{+}\textbf{b}\] ここで、\(\textbf{A}^{+}\) は\(\textbf{A}\) の一般化逆行列

# xの推定量 <- solve (t (A) %*% A) %*% t (A) %*% b

[,1]

[1,] 0.3333333

[2,] -0.3333333

# 残差 <- A %*% x_hat - b

[,1]

[1,] -0.3333333

[2,] -0.6666667

[3,] 0.3333333

# 残差のノルムの自乗 norm (r_hat, type = "2" )^ 2

12 Least squares > 12.4 Examples (p.234)

Advertising purchases. (p.234)

\(\textbf{y}=\textbf{Ax}\)

library (dplyr)<- c (0.97 , 1.86 , 0.41 ,1.23 , 2.18 , 0.53 ,0.80 , 1.24 , 0.62 ,1.29 , 0.98 , 0.51 ,1.10 , 1.23 , 0.69 ,0.67 , 0.34 , 0.54 ,0.87 , 0.26 , 0.62 ,1.10 , 0.16 , 0.48 ,1.92 , 0.22 , 0.71 ,1.29 , 0.12 , 0.62 %>% matrix (ncol = 3 , byrow = T)<- max (A) / min (A)<- rep (10 ^ 3 , nrow (A)) %>% matrix (ncol = 1 )list (A = A, A_ramge = A_ramge, y = y)

$A

[,1] [,2] [,3]

[1,] 0.97 1.86 0.41

[2,] 1.23 2.18 0.53

[3,] 0.80 1.24 0.62

[4,] 1.29 0.98 0.51

[5,] 1.10 1.23 0.69

[6,] 0.67 0.34 0.54

[7,] 0.87 0.26 0.62

[8,] 1.10 0.16 0.48

[9,] 1.92 0.22 0.71

[10,] 1.29 0.12 0.62

$A_ramge

[1] 18.16667

$y

[,1]

[1,] 1000

[2,] 1000

[3,] 1000

[4,] 1000

[5,] 1000

[6,] 1000

[7,] 1000

[8,] 1000

[9,] 1000

[10,] 1000

\(\textbf{b}=\textbf{Q}^{'}\textbf{y}\)

<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% ylist (Q = Q, R = R, b = b)

$Q

[,1] [,2] [,3]

[1,] -0.2617400 -0.48336838 0.21255760

[2,] -0.3318971 -0.54118838 0.23326187

[3,] -0.2158680 -0.28051919 -0.44193172

[4,] -0.3480872 -0.04271022 0.23104990

[5,] -0.2968185 -0.19486267 -0.30605721

[6,] -0.1807895 0.04571691 -0.47254161

[7,] -0.2347565 0.13228601 -0.45820183

[8,] -0.2968185 0.23505481 0.04529853

[9,] -0.5180832 0.43409279 0.34276081

[10,] -0.3480872 0.30283093 -0.07258117

$R

[,1] [,2] [,3]

[1,] -3.705968 -2.510005 -1.7686876

[2,] 0.000000 -2.488850 -0.0996784

[3,] 0.000000 0.000000 -0.4757187

$b

[,1]

[1,] -3032.9456

[2,] -392.6674

[3,] -686.3848

\(\textbf{Rx}=\textbf{b}\)

<- solve (a = R) %*% b %>% round ()

[,1]

[1,] 62

[2,] 100

[3,] 1443

# RMS error %>% apply (MARGIN = 1 , function (x) x %*% x_hat) %>% - y%>% sqrt (sum (.^ 2 ) / nrow (A))

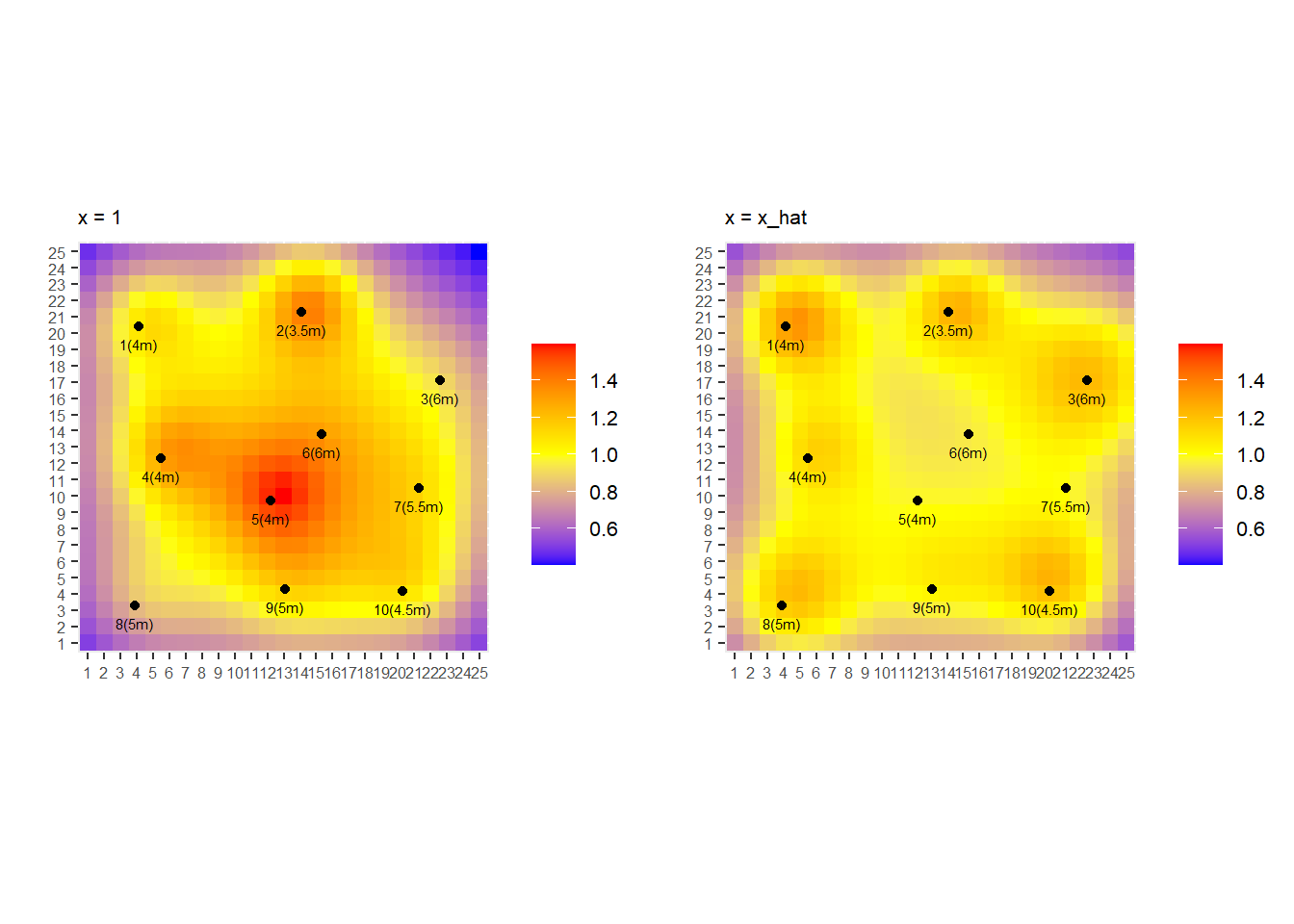

Illumination. (p.234)

# Extracted from 『https://ses.library.usyd.edu.au/handle/2123/21370』 library (ggplot2)library (reshape2)library (dplyr)library (gridExtra)<- 10 <- c (4.1 , 20.4 , 4.0 ,14.1 , 21.3 , 3.5 ,22.6 , 17.1 , 6.0 ,5.5 , 12.3 , 4.0 ,12.2 , 9.7 , 4.0 ,15.3 , 13.8 , 6.0 ,21.3 , 10.5 , 5.5 ,3.9 , 3.3 , 5.0 ,13.1 , 4.3 , 5.0 ,20.3 , 4.2 , 4.5 %>% matrix (nrow = n, byrow = T)

<- 25 <- N^ 2 <- seq (from = 0.5 , by = 1 , length.out = N)<- cbind (tmp %>% sapply (function (x) rep (x, length (tmp))) %>% as.vector (), rep (tmp, length (tmp)), 0 )head (pixels, 3 )tail (pixels, 3 )

[,1] [,2] [,3]

[1,] 0.5 0.5 0

[2,] 0.5 1.5 0

[3,] 0.5 2.5 0

[,1] [,2] [,3]

[623,] 24.5 22.5 0

[624,] 24.5 23.5 0

[625,] 24.5 24.5 0

<- matrix (data = 0 , nrow = m, ncol = n)for (i in seq (m)) {for (j in seq (n)) {<- - lamps[j, ]%>% matrix (nrow = 1 ) %>% norm (type = "2" ) %>% ^ 2 %>% 1 / .<- (m / sum (A)) * A<- rep (1 , m) %>% matrix (ncol = 1 )

<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y

<- solve (a = R) %*% b

[,1]

[1,] 1.46211018

[2,] 0.78797433

[3,] 2.96641047

[4,] 0.74358042

[5,] 0.08317333

[6,] 0.21263945

[7,] 0.21218408

[8,] 2.05114815

[9,] 0.90760315

[10,] 1.47222464

# RMS error %>% apply (MARGIN = 1 , function (x) x %*% x_hat) %>% - y%>% sqrt (sum (.^ 2 ) / nrow (A))

<- list ()<- A %*% matrix (data = 1 , nrow = 10 ) %>% matrix (nrow = N, byrow = T)<- melt (intensity)$ Var1 <- factor (df$ Var1, levels = df$ Var1 %>% unique ())$ Var2 <- factor (df$ Var2, levels = df$ Var2 %>% unique ())<- df$ value %>% range ()<- ggplot (df, mapping = aes (x = Var1, y = Var2, fill = value)) + geom_tile () + scale_fill_gradient2 (low = "blue" , high = "red" , mid = "yellow" ,midpoint = valuelimits %>% mean (), limits = valuelimits+ labs (title = "x = 1" , x = "" , y = "" ) + theme (legend.title = element_blank (),axis.text = element_text (size = 6 ),legend.text = element_text (size = 8 ),plot.title = element_text (size = 8 )+ coord_fixed ()<- lamps %>% data.frame () %>% colnames (.) <- c ("Var1" , "Var2" , "value" )1 ]] <- g + geom_point (data = pointdf, mapping = aes (x = Var1, y = Var2)) + geom_text (data = pointdf, mapping = aes (label = paste0 (seq (nrow (pointdf)), "(" , value, "m)" )),hjust = 0.5 , vjust = 2 , size = 2

<- A %*% x_hat %>% matrix (nrow = N, byrow = T)<- melt (intensity)$ Var1 <- factor (df$ Var1, levels = df$ Var1 %>% unique ())$ Var2 <- factor (df$ Var2, levels = df$ Var2 %>% unique ())<- ggplot (df, mapping = aes (x = Var1, y = Var2, fill = value)) + geom_tile () + scale_fill_gradient2 (low = "blue" , high = "red" , mid = "yellow" ,midpoint = valuelimits %>% mean (), limits = valuelimits+ labs (title = "x = x_hat" , x = "" , y = "" ) + theme (legend.title = element_blank (),axis.text = element_text (size = 6 ),legend.text = element_text (size = 8 ),plot.title = element_text (size = 8 )+ coord_fixed ()2 ]] <- g + geom_point (data = pointdf, mapping = aes (x = Var1, y = Var2)) + geom_text (data = pointdf, mapping = aes (label = paste0 (seq (nrow (pointdf)), "(" , value, "m)" )),hjust = 0.5 , vjust = 2 , size = 2

arrangeGrob (grobs = gg, ncol = 2 , nrow = 1 , widths = c (1 , 1 )) %>% ggpubr:: as_ggplot ()

13 Least squares data fitting > 13.1 Least squares data fitting > 13.1.1 Fitting univariate functions (p.249)

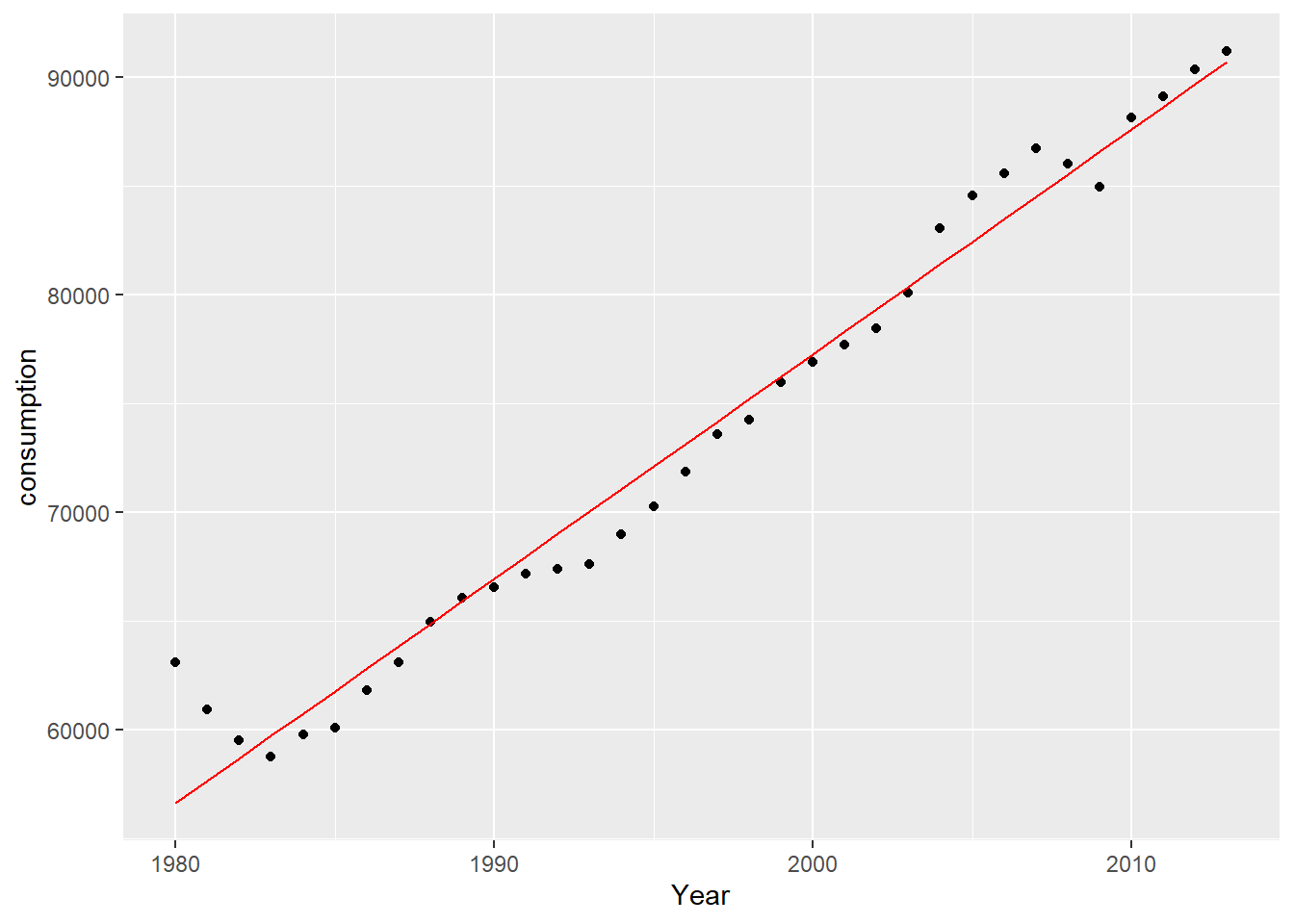

Straight-line fit. (p.249)

<- c (63122 , 60953 , 59551 , 58785 , 59795 , 60083 , 61819 , 63107 , 64978 , 66090 ,66541 , 67186 , 67396 , 67619 , 69006 , 70258 , 71880 , 73597 , 74274 , 75975 ,76928 , 77732 , 78457 , 80089 , 83063 , 84558 , 85566 , 86724 , 86046 , 84972 ,88157 , 89105 , 90340 , 91195 <- length (consumption)<- cbind (rep (1 , n), seq (0 , n - 1 , 1 ))<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% consumption<- solve (a = R) %*% b<- seq (1980 , 2013 , 1 )<- cbind (Year, A %*% x_hat)ggplot () + geom_point (mapping = aes (x = Year, y = consumption)) + geom_line (mapping = aes (x = fitting[, 1 ], y = fitting[, 2 ]), color = "red" )

[,1]

[1,] 56637.50

[2,] 1032.57

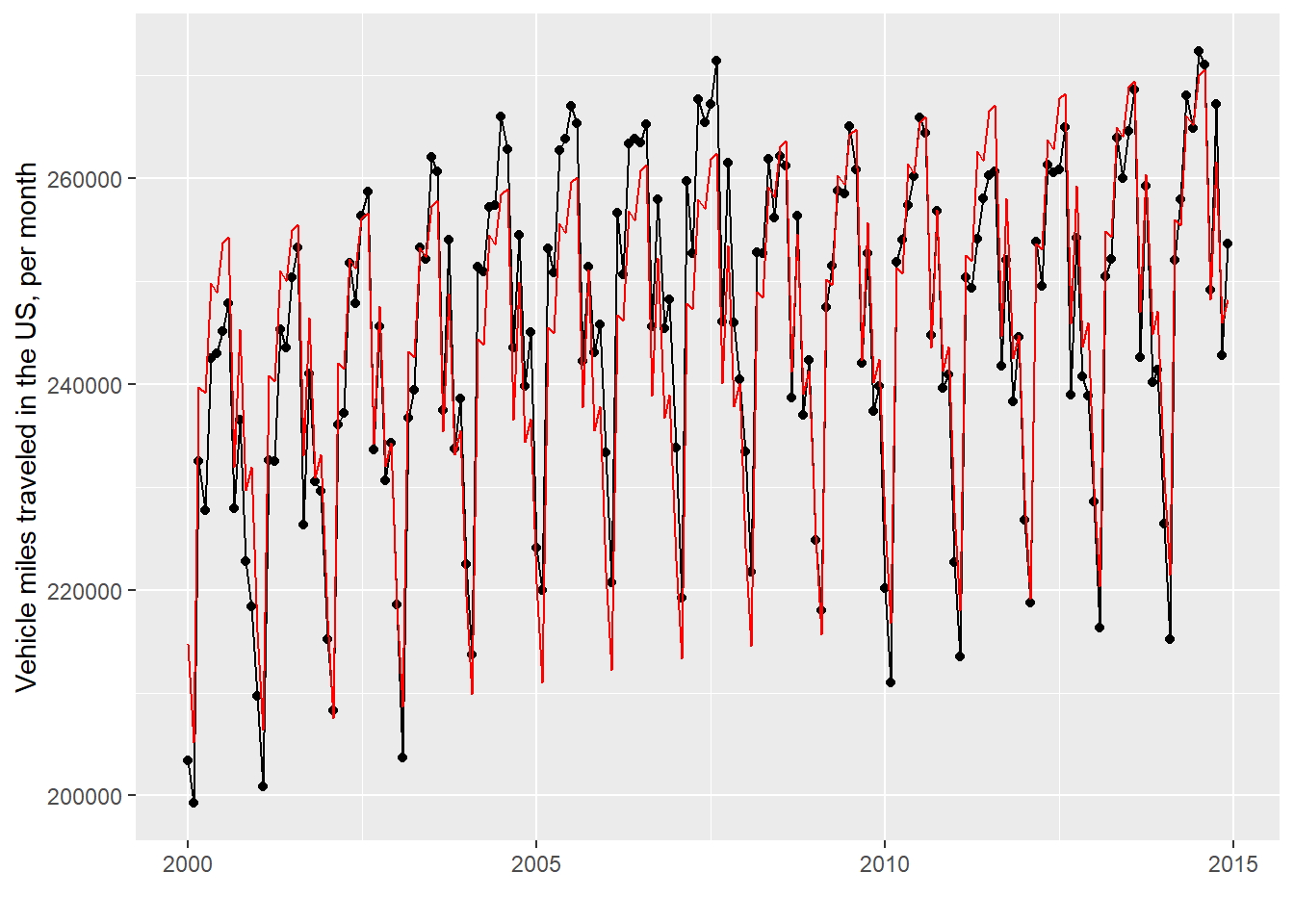

Estimation of trend and seasonal component. (p.252)

<- c (203442 , 199261 , 232490 , 227698 , 242501 , 242963 , 245140 , 247832 , 227899 , 236491 , 222819 , 218390 , # 2000 209685 , 200876 , 232587 , 232513 , 245357 , 243498 , 250363 , 253274 , 226312 , 241050 , 230511 , 229584 , # 2001 215215 , 208237 , 236070 , 237226 , 251746 , 247868 , 256392 , 258666 , 233625 , 245556 , 230648 , 234260 , # 2002 218534 , 203677 , 236679 , 239415 , 253244 , 252145 , 262105 , 260687 , 237451 , 254048 , 233698 , 238538 , # 2003 222450 , 213709 , 251403 , 250968 , 257235 , 257383 , 265969 , 262836 , 243515 , 254496 , 239796 , 245029 , # 2004 224072 , 219970 , 253182 , 250860 , 262678 , 263816 , 267025 , 265323 , 242240 , 251419 , 243056 , 245787 , # 2005 233302 , 220730 , 256645 , 250665 , 263393 , 263805 , 263442 , 265229 , 245624 , 257961 , 245367 , 248208 , # 2006 233799 , 219221 , 259740 , 252734 , 267646 , 265475 , 267179 , 271401 , 246050 , 261505 , 245928 , 240444 , # 2007 233469 , 221728 , 252773 , 252699 , 261890 , 256152 , 262152 , 261228 , 238701 , 256402 , 237009 , 242326 , # 2008 224840 , 218031 , 247433 , 251481 , 258793 , 258487 , 265026 , 260838 , 242034 , 252683 , 237342 , 239774 , # 2009 220177 , 210968 , 251858 , 254014 , 257401 , 260159 , 265861 , 264358 , 244712 , 256867 , 239656 , 240932 , # 2010 222724 , 213547 , 250410 , 249309 , 254145 , 258025 , 260317 , 260623 , 241764 , 252058 , 238278 , 244615 , # 2011 226834 , 218714 , 253785 , 249567 , 261355 , 260534 , 260880 , 264983 , 239001 , 254170 , 240734 , 238876 , # 2012 228607 , 216306 , 250496 , 252116 , 263923 , 260023 , 264570 , 268609 , 242582 , 259281 , 240146 , 241365 , # 2013 226444 , 215166 , 252089 , 257947 , 268075 , 264868 , 272335 , 271018 , 249125 , 267185 , 242816 , 253618 # 2014 %>% matrix (nrow = 15 , ncol = 12 , byrow = T)head (vmt)# 15年12ヶ月。計180ヶ月分

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10]

[1,] 203442 199261 232490 227698 242501 242963 245140 247832 227899 236491

[2,] 209685 200876 232587 232513 245357 243498 250363 253274 226312 241050

[3,] 215215 208237 236070 237226 251746 247868 256392 258666 233625 245556

[4,] 218534 203677 236679 239415 253244 252145 262105 260687 237451 254048

[5,] 222450 213709 251403 250968 257235 257383 265969 262836 243515 254496

[6,] 224072 219970 253182 250860 262678 263816 267025 265323 242240 251419

[,11] [,12]

[1,] 222819 218390

[2,] 230511 229584

[3,] 230648 234260

[4,] 233698 238538

[5,] 239796 245029

[6,] 243056 245787

<- 15 * 12 <- lapply (seq (15 ), function (x) diag (x = 1 , nrow = 12 )) %>% Reduce (function (x, y) rbind (x, y), .) %>% cbind (seq (m) - 1 , .)list (head_A = head (A), tail_A = tail (A), dim_A = dim (A))

$head_A

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

[1,] 0 1 0 0 0 0 0 0 0 0 0 0 0

[2,] 1 0 1 0 0 0 0 0 0 0 0 0 0

[3,] 2 0 0 1 0 0 0 0 0 0 0 0 0

[4,] 3 0 0 0 1 0 0 0 0 0 0 0 0

[5,] 4 0 0 0 0 1 0 0 0 0 0 0 0

[6,] 5 0 0 0 0 0 1 0 0 0 0 0 0

$tail_A

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

[175,] 174 0 0 0 0 0 0 1 0 0 0 0 0

[176,] 175 0 0 0 0 0 0 0 1 0 0 0 0

[177,] 176 0 0 0 0 0 0 0 0 1 0 0 0

[178,] 177 0 0 0 0 0 0 0 0 0 1 0 0

[179,] 178 0 0 0 0 0 0 0 0 0 0 1 0

[180,] 179 0 0 0 0 0 0 0 0 0 0 0 1

$dim_A

[1] 180 13

<- t (vmt) %>% as.vector () %>% matrix (ncol = 1 )list (head_y = head (y), tail_y = tail (y))

$head_y

[,1]

[1,] 203442

[2,] 199261

[3,] 232490

[4,] 227698

[5,] 242501

[6,] 242963

$tail_y

[,1]

[175,] 272335

[176,] 271018

[177,] 249125

[178,] 267185

[179,] 242816

[180,] 253618

<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% blist (Q = dim (Q), R = dim (R), b = dim (b), x_hat = dim (x_hat))

$Q

[1] 180 13

$R

[1] 13 13

$b

[1] 13 1

$x_hat

[1] 13 1

<- seq (as.Date ("2000-1-1" ), as.Date ("2014-12-1" ), by = "+1 month" )ggplot (mapping = aes (x = Date)) + geom_point (mapping = aes (y = y)) + geom_line (mapping = aes (y = y)) + geom_line (mapping = aes (y = A %*% x_hat), col = "red" ) + labs (x = "" , y = "Vehicle miles traveled in the US, per month" )

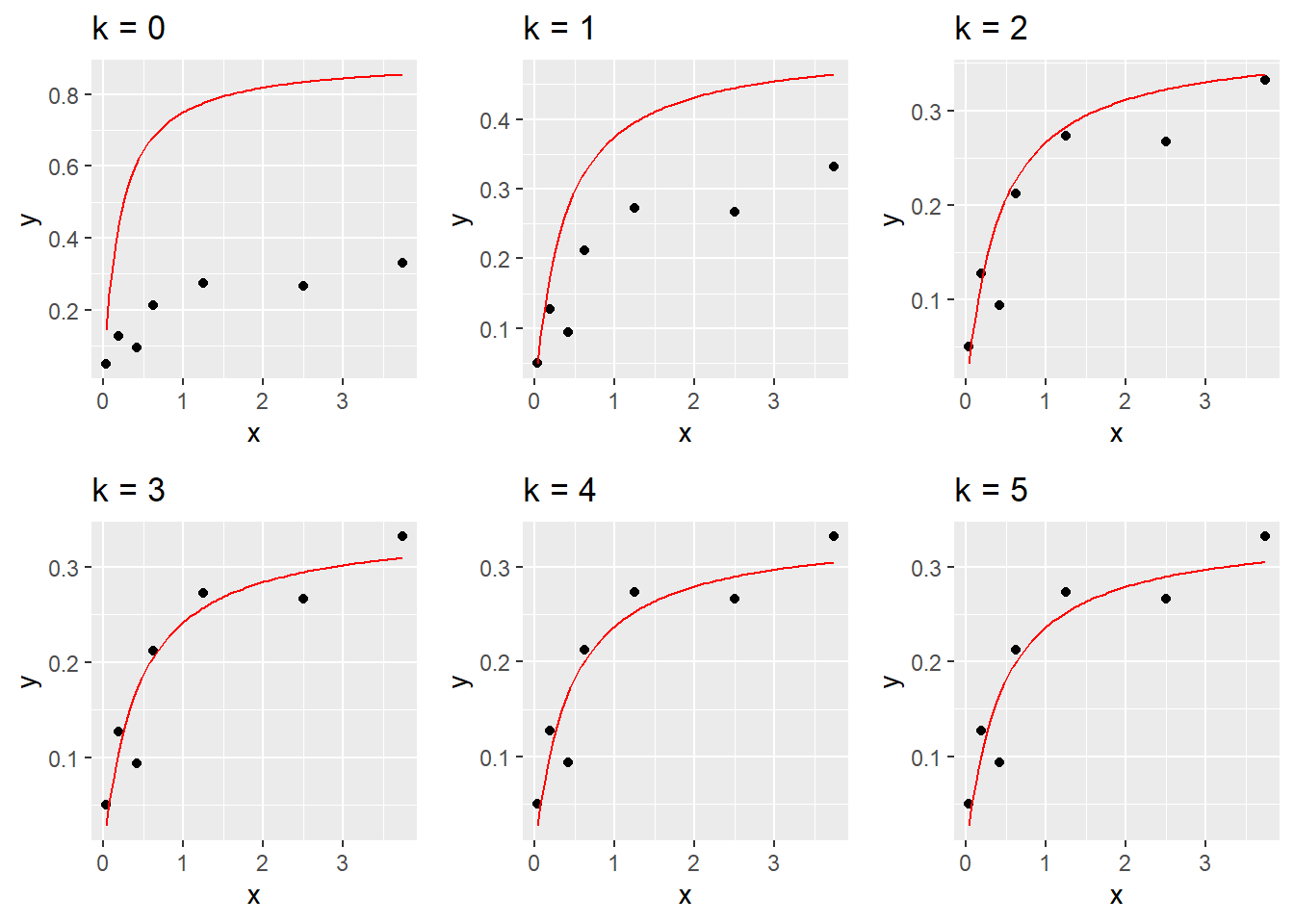

Polynomial fit. (p.255)

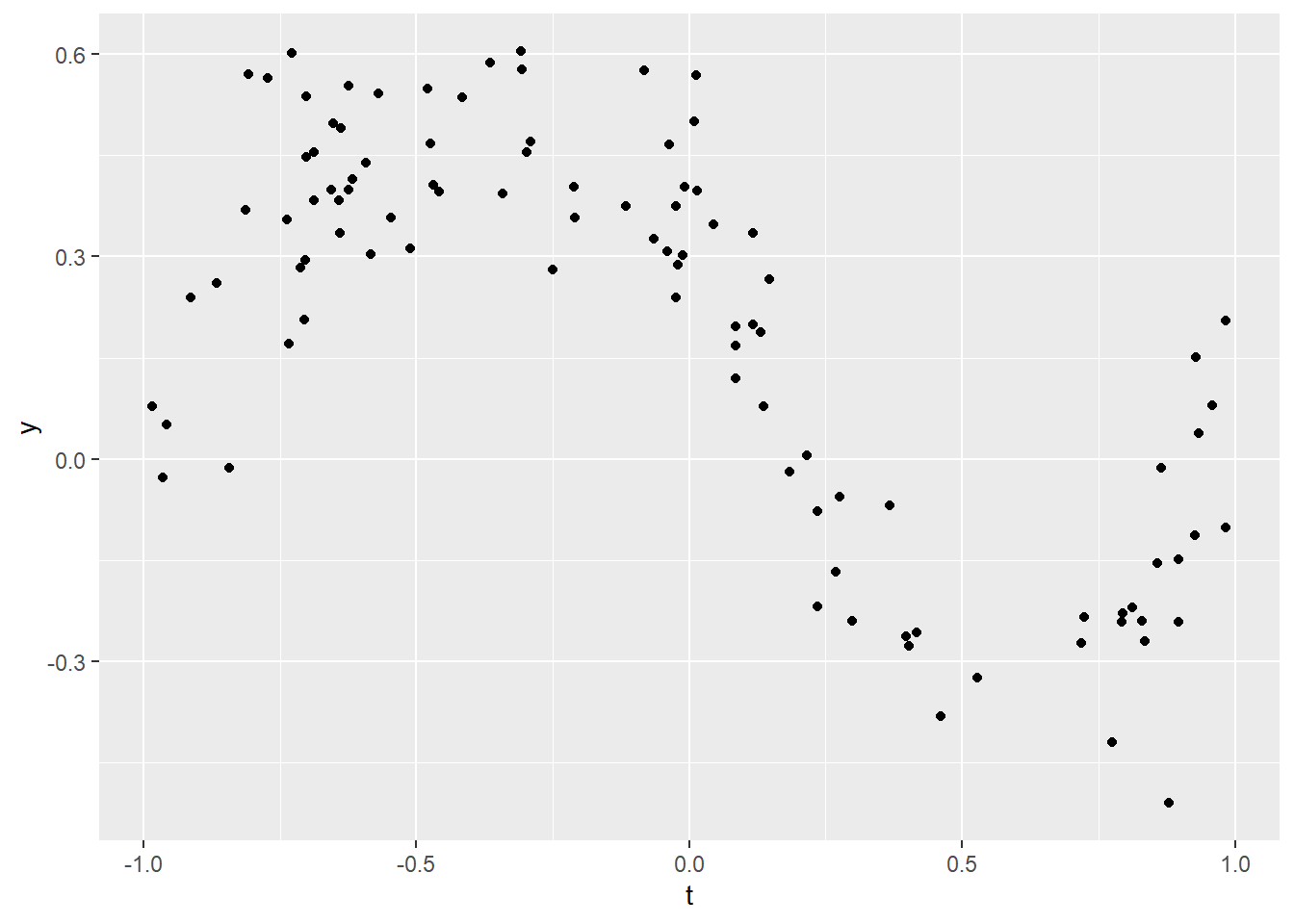

# サンプルデータ <- 100 <- - 1 + 2 * runif (n = m)<- t^ 3 - t + 0.4 / (1 + 25 * t^ 2 ) + 0.10 * rnorm (n = m)ggplot (mapping = aes (x = t, y = y)) + geom_point ()

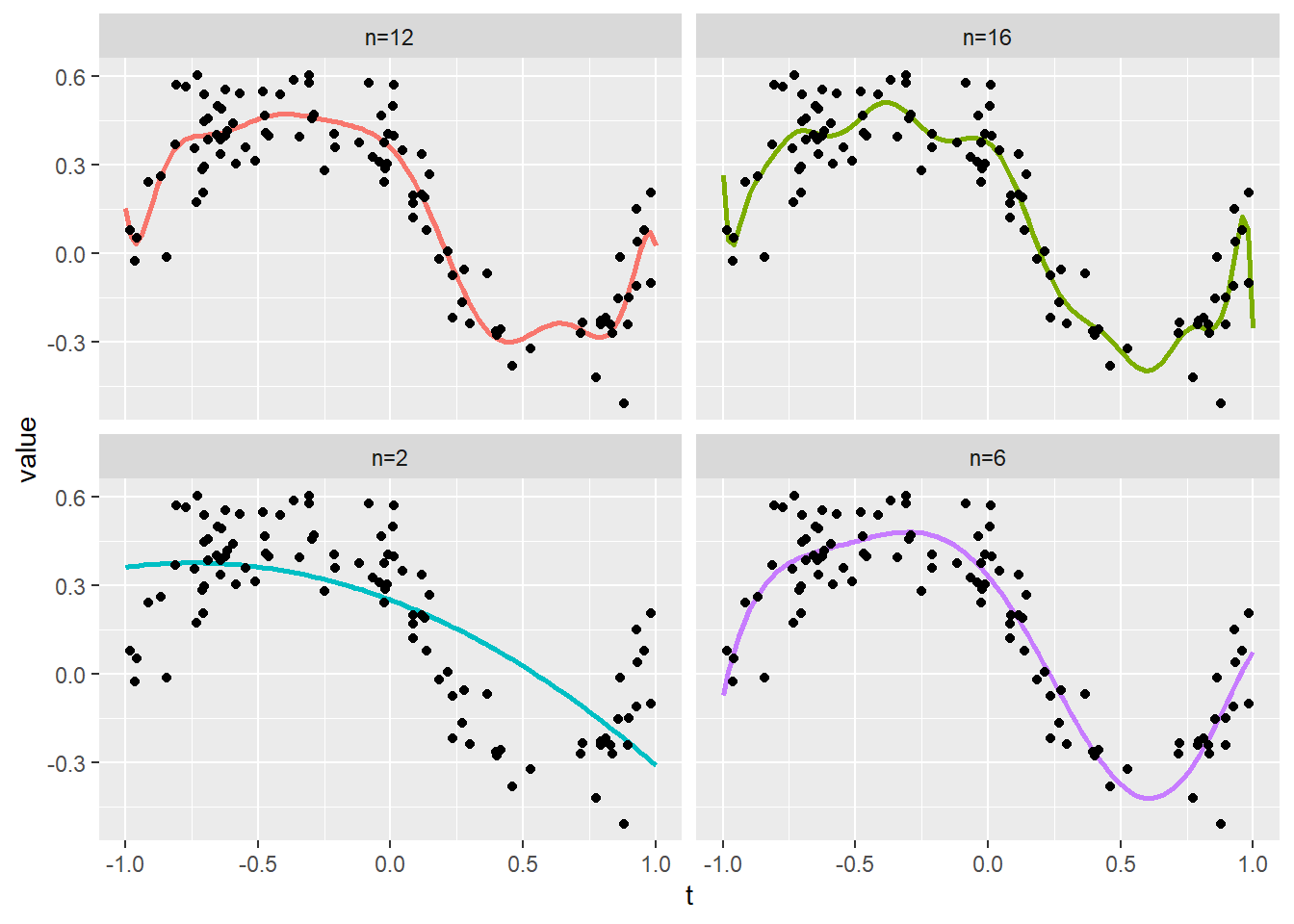

# 多項式回帰関数 <- function (n, t, y, t_plot) {# https://stackoverflow.com/questions/61207545/create-a-vandermonde-matrix-in-r <- outer (X = t, Y = seq (n + 1 ) - 1 , FUN = "^" )# <- qr (x = vandermonde_matrix)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% b# <- outer (X = t_plot, Y = seq (length (x_hat)) - 1 , FUN = "^" ) %*% x_hatreturn (polyeval)

# 対象多項式次数 <- c (2 , 6 , 12 , 16 )

# プロット <- seq (- 1 , 1 , length.out = 100 )<- sapply (n, function (x) func_polynomial_regression (n = x, y = y, t_plot = t_plot, t = t)) %>% data.frame (t = t_plot, .)colnames (polyeval)[- 1 ] <- paste0 ("n=" , n)<- gather (data = polyeval, key = "key" , value = "value" , colnames (polyeval)[- 1 ])<- data.frame (t, y)ggplot () + geom_line (data = tidydf, mapping = aes (x = t, y = value, color = key), size = 1 ) + facet_wrap (facets = ~ key, nrow = 2 , scales = "fixed" ) + geom_point (data = pointdf, mapping = aes (x = t, y = y)) + theme (legend.position = "none" ) + ylim (range (pointdf$ y))

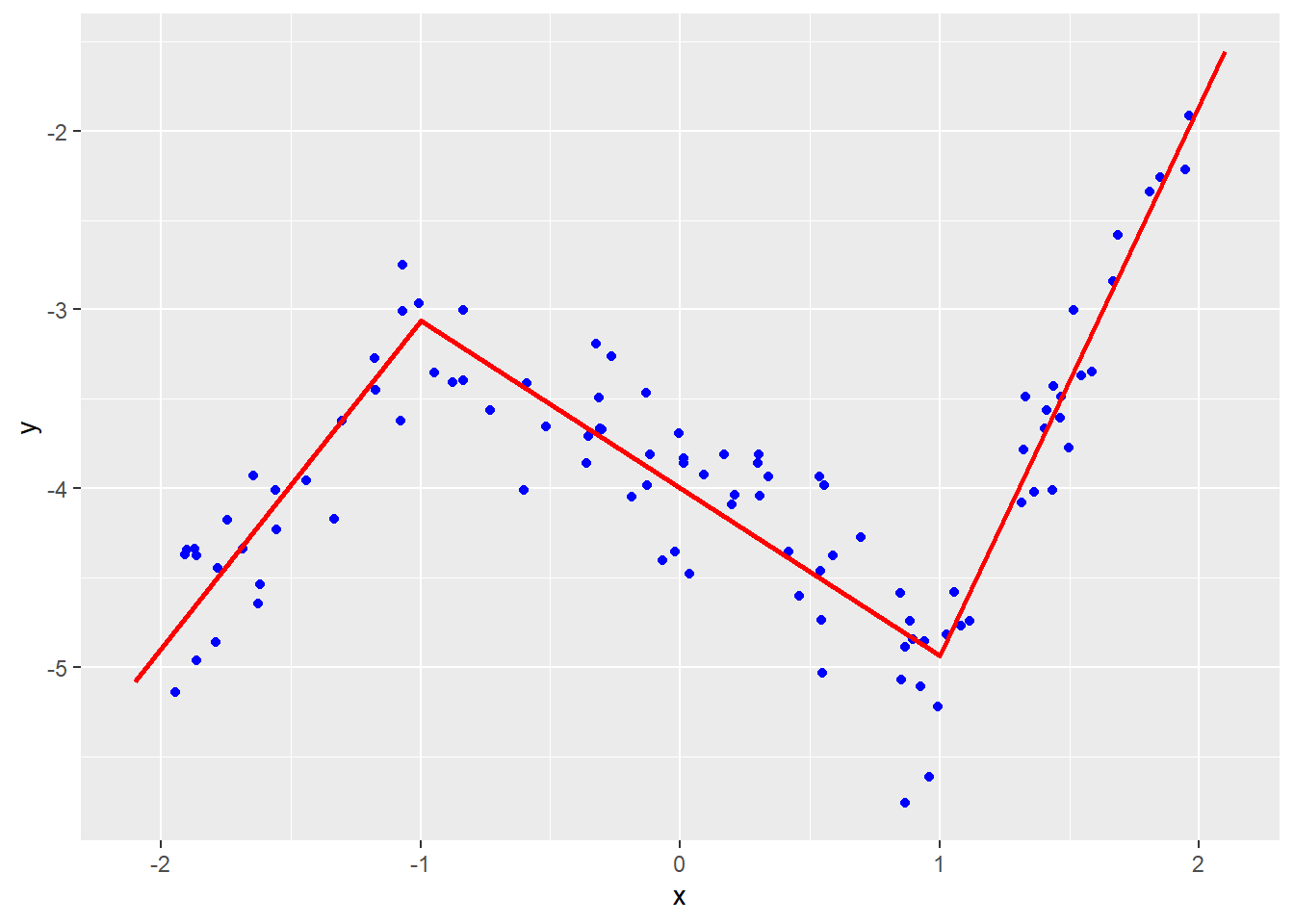

Piecewise-linear fit. (p.256)

# サンプルデータ <- 100 <- - 2 + 4 * runif (n = m)<- sapply (X = x, function (x) max (x + 1 , 0 ))<- sapply (X = x, function (x) max (x - 1 , 0 ))<- 1 + 2 * (x - 1 ) - 3 * tmp1 + 4 * tmp2 + 0.3 * rnorm (n = m)

# 区分線形関数 <- cbind (rep (1 , m), x, tmp1, tmp2)<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% b<- c (- 2.1 , - 1 , 1 , 2.1 )<- 1 ] + 2 ] * t + 3 ] * sapply (X = t + 1 , FUN = function (x) max (x, 0 )) + 4 ] * sapply (X = t - 1 , FUN = function (x) max (x, 0 ))ggplot () + geom_point (mapping = aes (x = x, y = y), color = "blue" ) + geom_line (mapping = aes (x = t, y = y_hat), color = "red" , size = 1 )

13 Least squares data fitting > 13.1 Least squares data fitting > 13.1.2 Regression (p.257)

House price regression. (p.258)

# 重回帰分析 list (area = summary (area), beds = table (beds), price = summary (price))

$area

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.539 1.146 1.419 1.583 1.836 4.303

$beds

beds

1 2 3 4 5 6

8 116 380 223 46 1

$price

Min. 1st Qu. Median Mean 3rd Qu. Max.

55.42 150.00 208.00 228.77 284.84 699.00

# 係数の推定 <- length (price)<- cbind (constant = rep (1 , m), area, beds)<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% price<- solve (a = R) %*% b

[,1]

constant 54.40167

area 148.72507

beds -18.85336

# 誤差の二乗平均平方根(RMS) sum ((price - A %*% x_hat)^ 2 ) / m)^ 0.5

# 標本標準偏差 sqrt (var (price) * (length (price) - 1 ) / length (price))

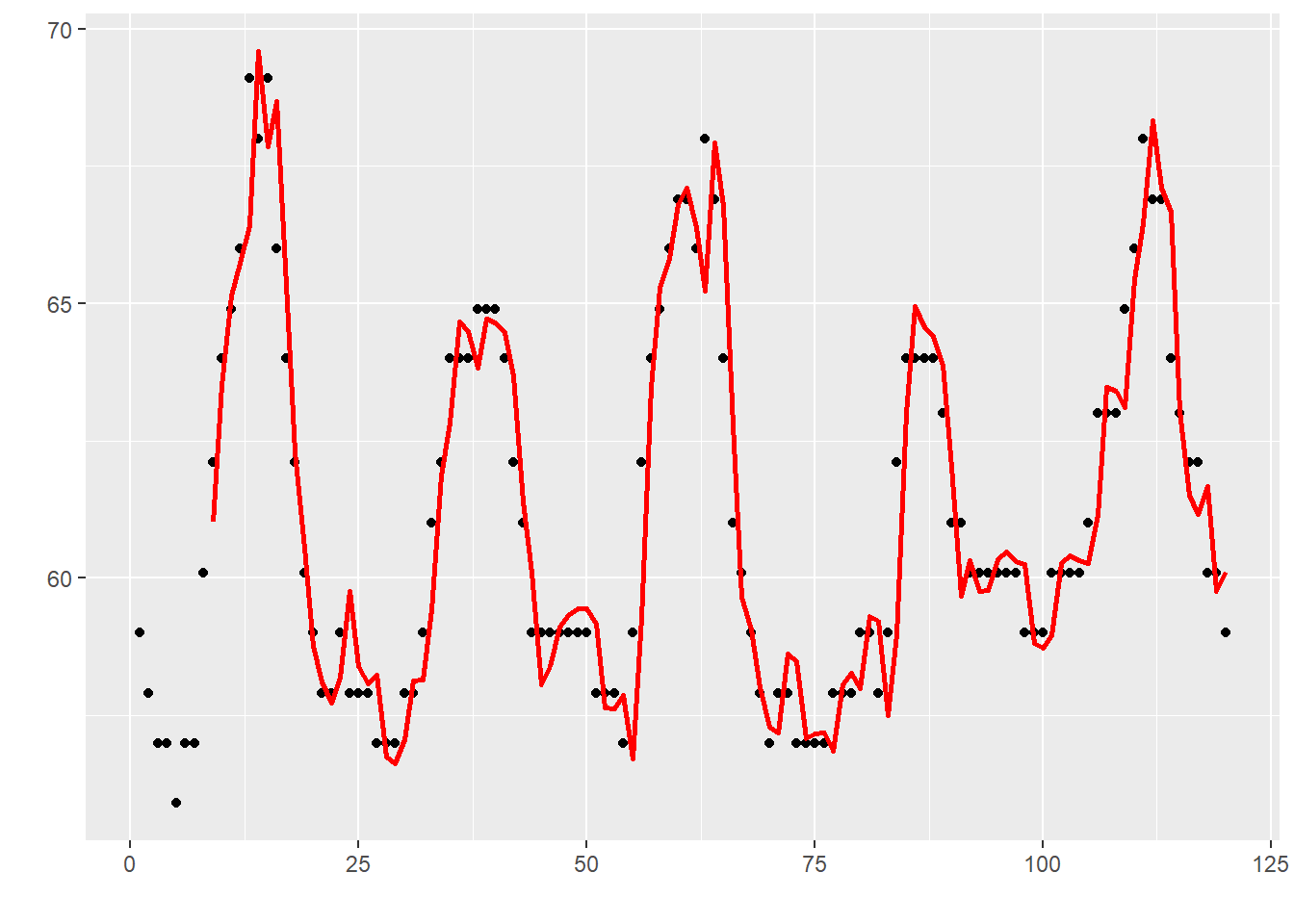

Auto-regressive time series model. (p.259)

# サンプルデータ library (ggplot2)summary (t)<- length (t)

Min. 1st Qu. Median Mean 3rd Qu. Max.

54.00 59.00 61.00 61.76 64.00 70.00

# 標準偏差 sqrt (var (t) * (length (t) - 1 ) / length (t))

# ラグ次数=1の場合の二乗平均平方根 sum ((tail (t, - 1 ) - head (t, - 1 ))^ 2 ) / (N - 1 )^ 0.5

# ラグ次数=24の場合の二乗平均平方根 sum ((tail (t, - 24 ) - head (t, - 24 ))^ 2 ) / (N - 24 )^ 0.5

# 自己回帰ラグ次数を 8 とした最小二乗法 <- 8 <- tail (t, - M)<- sapply (rev (seq (M)), function (i) t[i: (i + N - M - 1 )])list (dim_A = dim (A), head_A = head (A), tail_A = tail (A))

$dim_A

[1] 736 8

$head_A

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8]

[1,] 60.1 57.0 57.0 55.9 57.0 57.0 57.9 59.0

[2,] 62.1 60.1 57.0 57.0 55.9 57.0 57.0 57.9

[3,] 64.0 62.1 60.1 57.0 57.0 55.9 57.0 57.0

[4,] 64.9 64.0 62.1 60.1 57.0 57.0 55.9 57.0

[5,] 66.0 64.9 64.0 62.1 60.1 57.0 57.0 55.9

[6,] 69.1 66.0 64.9 64.0 62.1 60.1 57.0 57.0

$tail_A

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8]

[731,] 63.0 64.9 66.0 68.0 68.0 68.0 64.9 63.0

[732,] 62.1 63.0 64.9 66.0 68.0 68.0 68.0 64.9

[733,] 62.1 62.1 63.0 64.9 66.0 68.0 68.0 68.0

[734,] 62.1 62.1 62.1 63.0 64.9 66.0 68.0 68.0

[735,] 62.1 62.1 62.1 62.1 63.0 64.9 66.0 68.0

[736,] 62.1 62.1 62.1 62.1 62.1 63.0 64.9 66.0

# QR分解による最小二乗法 <- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% b<- A %*% x_hatlist (x_hat = x_hat)

$x_hat

[,1]

[1,] 1.233765489

[2,] 0.007910523

[3,] -0.214893749

[4,] 0.043416077

[5,] -0.118176365

[6,] -0.131813798

[7,] 0.091479893

[8,] 0.088167609

# 予測誤差の二乗平均平方根 sum ((y_predict - y)^ 2 ) / length (y))^ 0.5

<- 24 * 5 ggplot () + geom_point (mapping = aes (x = seq (Nplot), y = head (t, Nplot))) + geom_line (mapping = aes (x = tail (seq (Nplot), - M), y = head (y_predict, Nplot - M)), color = "red" , size = 1 ) + labs (x = "" , y = "" )

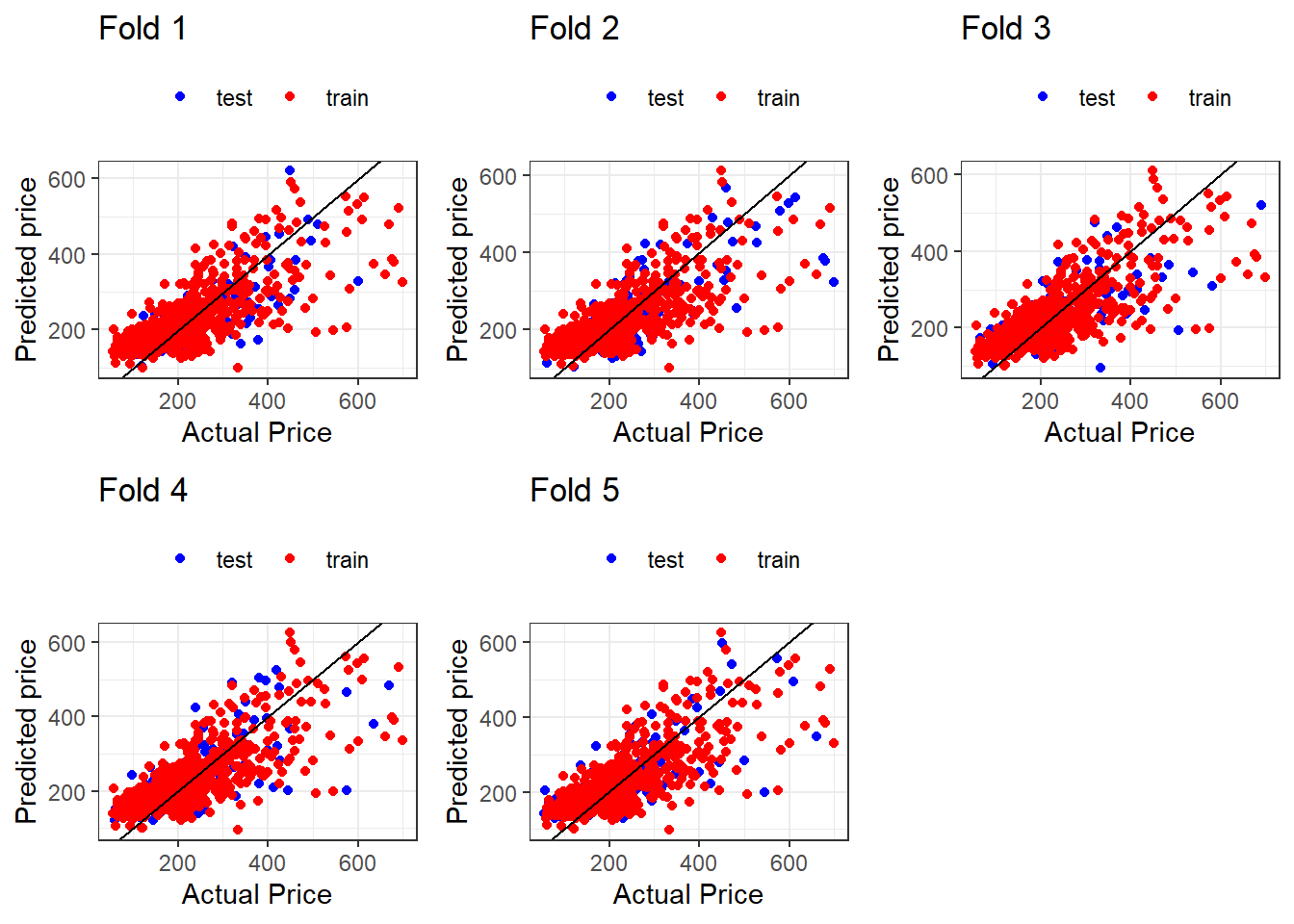

13 Least squares data fitting > 13.2. Validation (p.260)

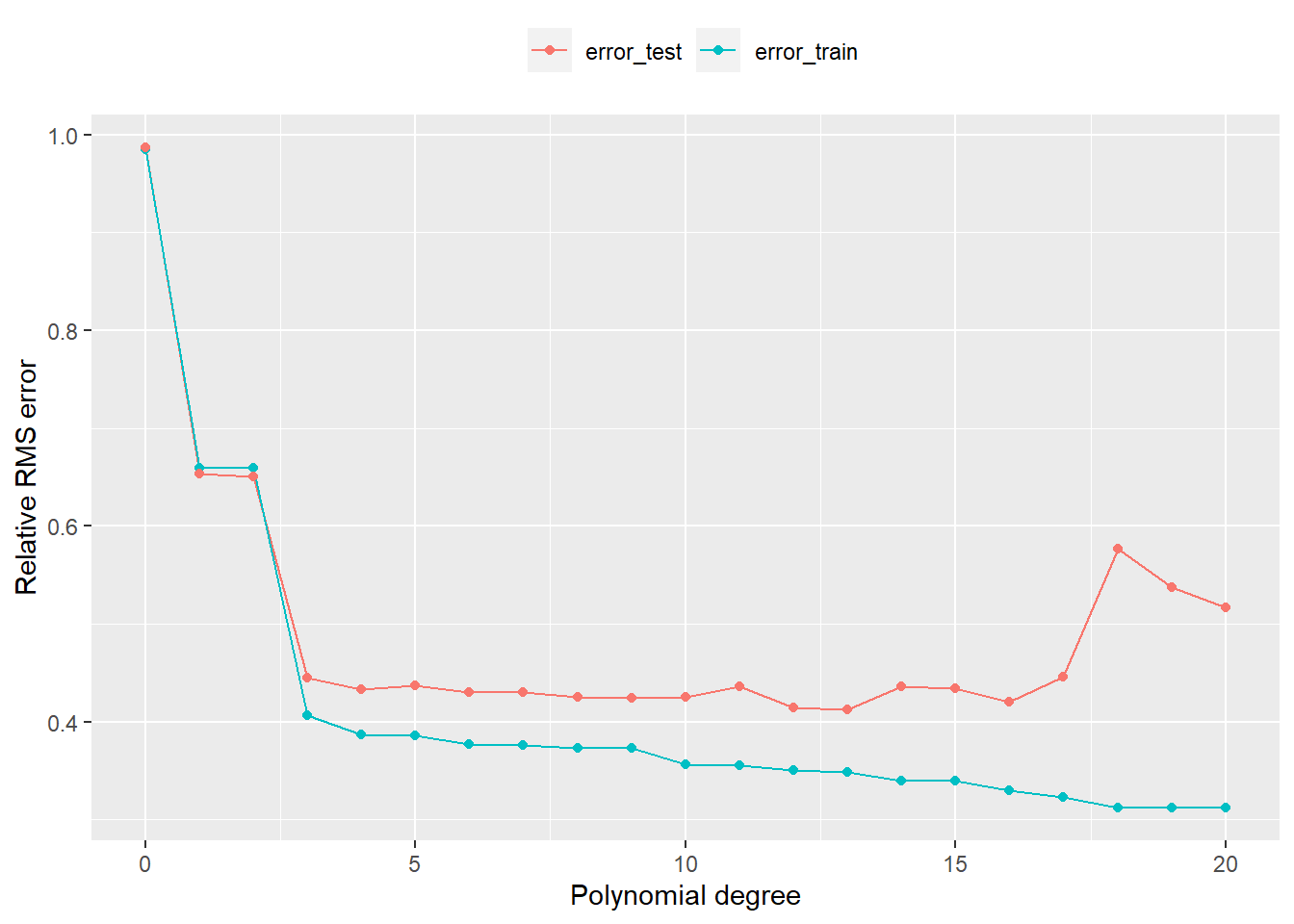

Example. (p.263)

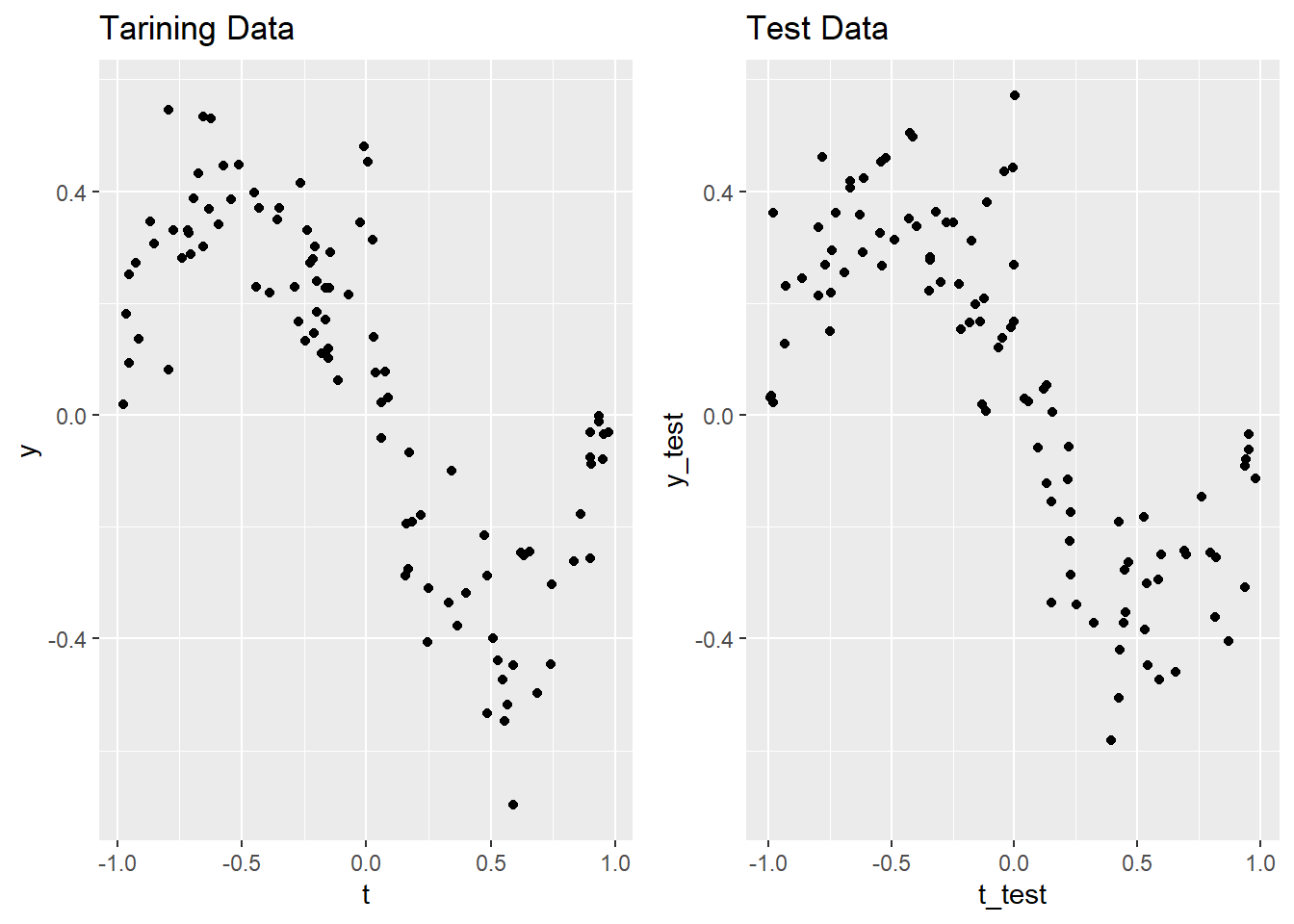

library (dplyr)library (ggplot2)library (tidyr)library (gridExtra)# サンプルデータ作成 <- function (m) {<- - 1 + 2 * runif (n = m)<- t^ 3 - t + 0.4 / (1 + (25 * t)^ 2 ) + 0.10 * rnorm (n = m)return (list (t = t, y = y))<- 100 <- func_generate_sample (m = m)<- tmp$ t<- tmp$ y<- func_generate_sample (m = m)<- tmp$ t<- tmp$ y

<- list ()1 ]] <- ggplot (mapping = aes (x = t, y = y)) + geom_point () + labs (title = "Tarining Data" ) + ylim (range (y, y_test))2 ]] <- ggplot (mapping = aes (x = t_test, y = y_test)) + geom_point () + labs (title = "Test Data" ) + ylim (range (y, y_test))arrangeGrob (grobs = g, ncol = 2 , nrow = 1 , widths = c (1 , 1 )) %>% ggpubr:: as_ggplot ()

<- error_test <- vector ()for (p in 1 : 21 ) {<- outer (X = t, Y = seq (p) - 1 , FUN = "^" )<- outer (X = t_test, Y = seq (p) - 1 , FUN = "^" )<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% b<- norm (x = A %*% x_hat - matrix (y, ncol = 1 ), type = "2" ) / norm (x = y, type = "2" )<- norm (x = A_test %*% x_hat - matrix (y_test, ncol = 1 ), type = "2" ) / norm (x = y_test, type = "2" )data.frame (` polynomial degree ` = seq (p) - 1 , error_train, error_test, check.names = F) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ]) %>% ggplot (mapping = aes (x = .[, 1 ], y = .[, 3 ], color = .[, 2 ])) + geom_line () + geom_point () + labs (x = "Polynomial degree" , y = "Relative RMS error" ) + theme (legend.title = element_blank (), legend.position = "top" )

House price regression model. (p.265)

# 重回帰分析 list (baths = table (baths), location = table (location), price = summary (price),beds = table (beds), area = summary (area), condo = table (condo)

$baths

baths

1 2 3 4 5

166 493 106 8 1

$location

location

1 2 3 4

26 340 338 70

$price

Min. 1st Qu. Median Mean 3rd Qu. Max.

55.42 150.00 208.00 228.77 284.84 699.00

$beds

beds

1 2 3 4 5 6

8 116 380 223 46 1

$area

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.539 1.146 1.419 1.583 1.836 4.303

$condo

condo

0 1

735 39

<- length (price)<- cbind (rep (1 , length (price)), area, beds)<- 5 <- sample (x = seq (N), size = N, replace = F) %>% split (f = 1 : split_n)<- rms_test <- vector ()<- matrix ()<- result_test <- list ()for (k in seq (split_n)) {<- I[[k]]<- sapply (setdiff (seq (split_n), k), function (x) I[[x]]) %>% Reduce (function (x, y) c (x, y), .)# <- qr (x = X[Itrain, ])<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% price[Itrain]<- solve (a = R) %*% b# if (k == 1 ) {<- x_hat %>% t ()else {<- rbind (coeff, x_hat %>% t ())<- (sum ((X[Itrain, ] %*% x_hat - price[Itrain])^ 2 ) / N)^ 0.5 <- (sum ((X[Itest, ] %*% x_hat - price[Itest])^ 2 ) / N)^ 0.5 <- data.frame (price[Itrain], X[Itrain, ] %*% x_hat)colnames (tmp01) <- c ("Actual Price for training" , "Predicted price(Training)" )<- tmp01head (tmp01) %>% print ()<- data.frame (price[Itest], X[Itest, ] %*% x_hat)colnames (tmp02) <- c ("Actual Price for test" , "Predicted price(Test)" )<- tmp02head (tmp02) %>% print ()colnames (coeff)[1 ] <- "constant"

constant area beds

[1,] 59.84812 150.3868 -21.52018

[2,] 62.51126 146.9928 -20.71722

[3,] 46.17634 144.4939 -14.61995

[4,] 46.62748 150.1279 -16.72811

[5,] 57.01122 151.2613 -20.57694

cbind (rms_train, rms_test)

rms_train rms_test

[1,] 68.71690 29.71196

[2,] 66.59759 34.24948

[3,] 66.60560 34.24997

[4,] 66.03077 35.35007

[5,] 66.57772 34.23061

<- function (k) {<- ggplot () + geom_point (mapping = aes (x = result_test[[k]][, 1 ], y = result_test[[k]][, 2 ], color = "test" )) + geom_point (mapping = aes (x = result_train[[k]][, 1 ], y = result_train[[k]][, 2 ], color = "train" )) + geom_abline (intercept = 0 , slope = 1 ) + labs (title = paste ("Fold" , k), x = "Actual Price" , y = "Predicted price" ) + scale_color_manual (values = c ("test" = "blue" , "train" = "red" )) + theme_bw () + theme (legend.title = element_blank (), legend.position = "top" )return (g)<- list ()for (k in seq (split_n)) {<- func_plot (k = k)arrangeGrob (grobs = g, ncol = 3 , widths = c (1 , 1 , 1 )) %>% ggpubr:: as_ggplot ()

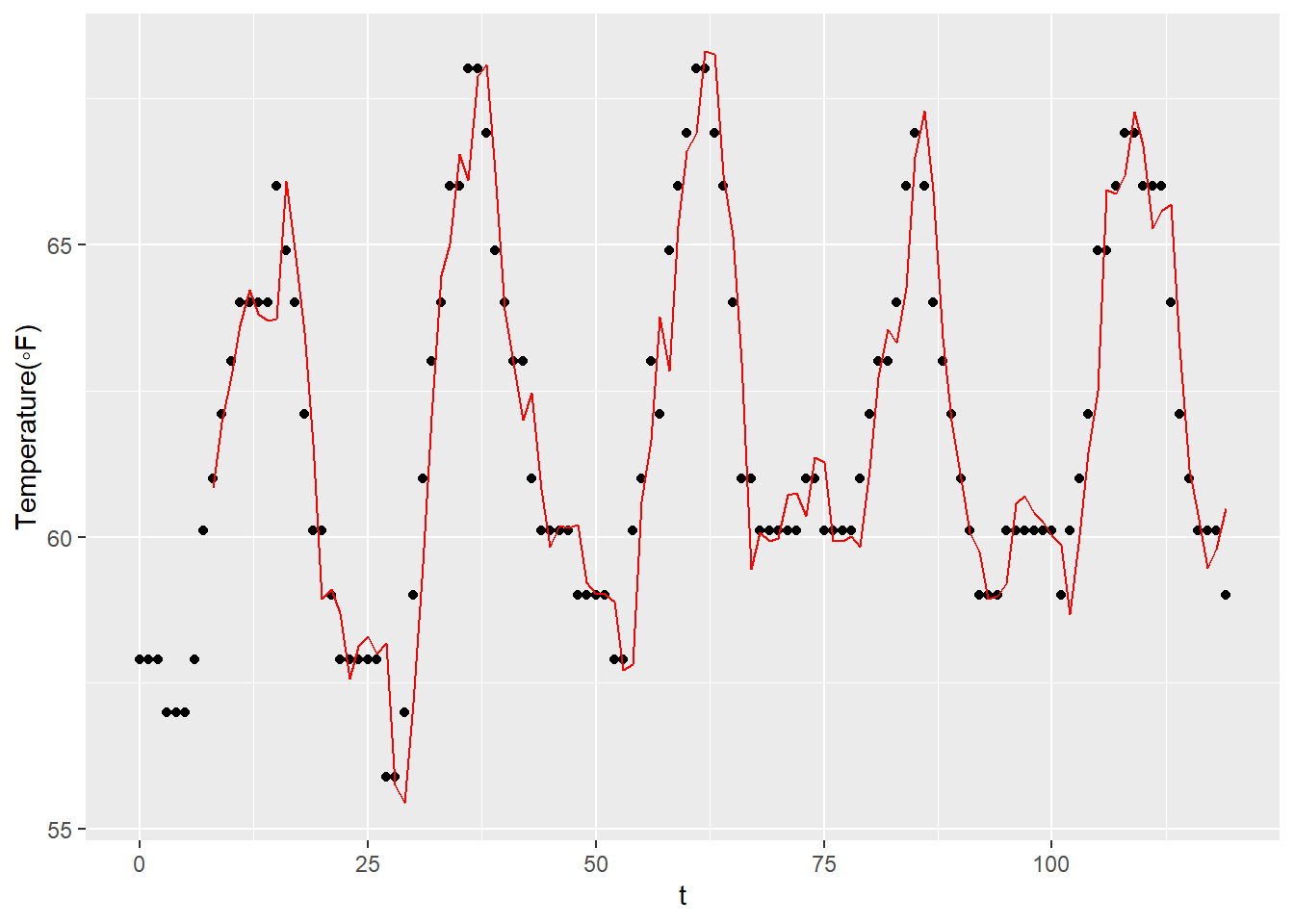

Validating time series predictions. (p.266)

Min. 1st Qu. Median Mean 3rd Qu. Max.

54.00 59.00 61.00 61.76 64.00 70.00

<- length (t)# 最初の24日分(24日×24時間)のデータを訓練データとして利用 <- 24 * 24 <- t %>% head (Ntrain) # ;head(t_train);tail(t_train) <- t %>% tail (- Ntrain) # ;head(t_test);tail(t_test) # 自己回帰のラグ次数を 8 とした線形回帰 <- 8 <- Ntrain - M<- t_train %>% tail (- M)<- sapply (rev (seq (M)), function (i) t[c (i: (i + m - 1 ))]) # ;head(A);tail(A) # <- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% y<- solve (a = R) %*% b<- (sum ((A %*% x_hat - y)^ 2 ) / length (y))^ 0.5 <- t_test %>% tail (- M)<- length (ytest)<- sapply (rev (seq (M)), function (i) t_test[c (i: (i + mtest - 1 ))]) %*% x_hat<- (sum ((ypred - ytest)^ 2 ) / length (ytest))^ 0.5 list (x_hat = x_hat, rms_test = rms_test, rms_train = rms_train)

$x_hat

[,1]

[1,] 1.20868426

[2,] 0.05067080

[3,] -0.23411924

[4,] 0.05710085

[5,] -0.14244840

[6,] -0.14097707

[7,] 0.13142279

[8,] 0.06944674

$rms_test

[1] 0.9755114

$rms_train

[1] 1.025358

<- 24 * 5 ggplot () + geom_point (mapping = aes (x = seq (Nplot) - 1 , y = t_test %>% head (Nplot))) + geom_line (mapping = aes (x = (seq (Nplot) - 1 ) %>% tail (- M), y = ypred[seq (Nplot - M)]), color = "red" ) + labs (x = "t" , y = "Temperature(◦F)" )

13 Least squares data fitting > 13.3. Feature engineering > 13.3.5 House price prediction (p.274)

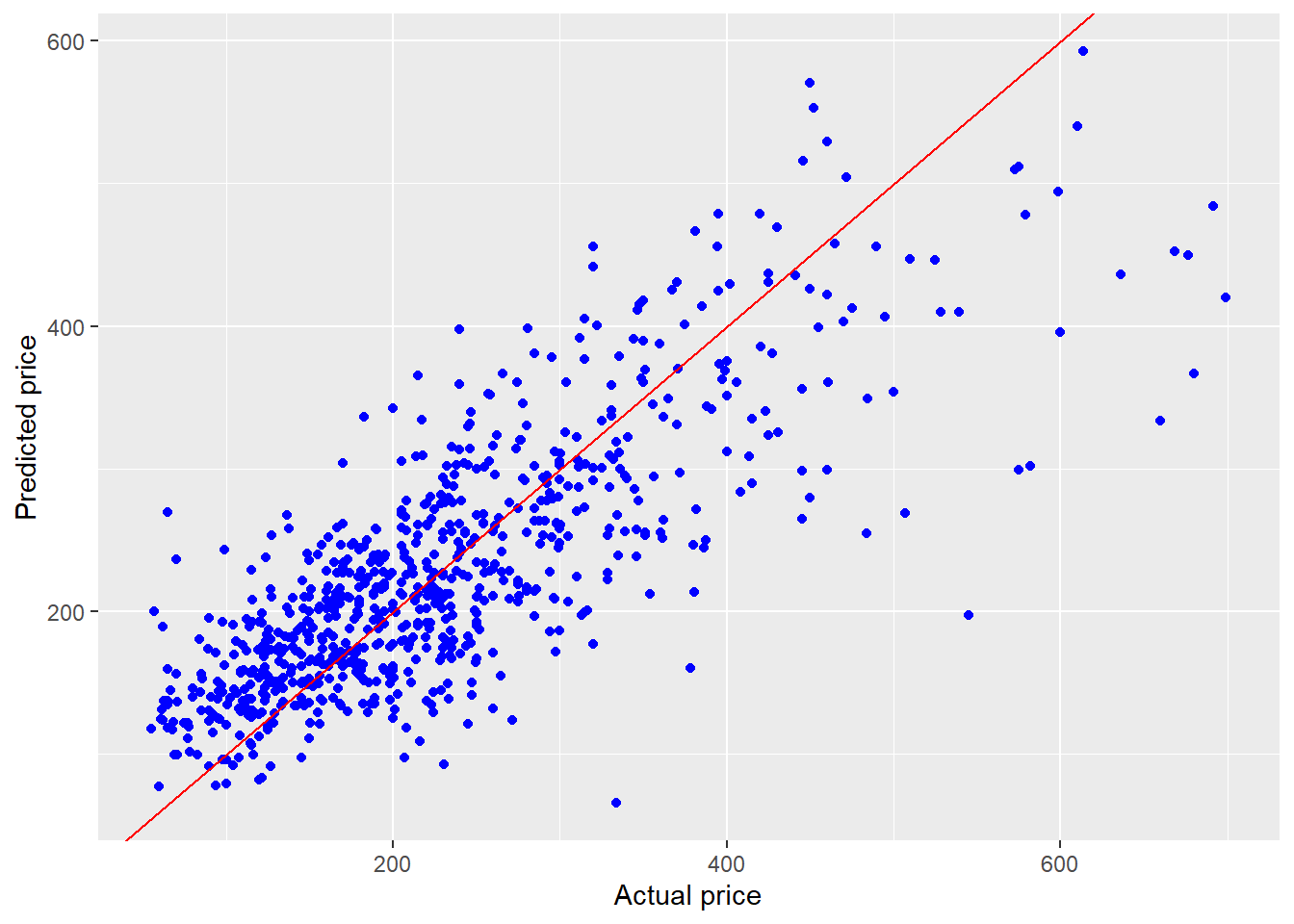

The resulting model. (p.275)

# 重回帰分析 list (baths = table (baths), location = table (location), price = summary (price),beds = table (beds), area = summary (area), condo = table (condo)

$baths

baths

1 2 3 4 5

166 493 106 8 1

$location

location

1 2 3 4

26 340 338 70

$price

Min. 1st Qu. Median Mean 3rd Qu. Max.

55.42 150.00 208.00 228.77 284.84 699.00

$beds

beds

1 2 3 4 5 6

8 116 380 223 46 1

$area

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.539 1.146 1.419 1.583 1.836 4.303

$condo

condo

0 1

735 39

<- length (price)<- cbind (constant = rep (1 , N),` area exceeds 1.5 ` = sapply (area - 1.5 , function (x) max (x, 0 )),location2 = {== 2 %>% as.numeric (),location3 = {== 3 %>% as.numeric (),location4 = {== 4 %>% as.numeric ()<- qr (x = X)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% price<- solve (a = R) %*% b

[,1]

constant 115.61682

area 175.41314

area exceeds 1.5 -42.74777

beds -17.87836

condo -19.04473

location2 -100.91050

location3 -108.79112

location4 -24.76525

# 予測値のRMS sum ((X %*% x_hat - price)^ 2 ) / N)^ 0.5

ggplot () + geom_point (mapping = aes (x = price, y = X %*% x_hat), color = "blue" ) + geom_abline (intercept = 0 , slope = 1 , color = "red" ) + labs (x = "Actual price" , y = "Predicted price" )

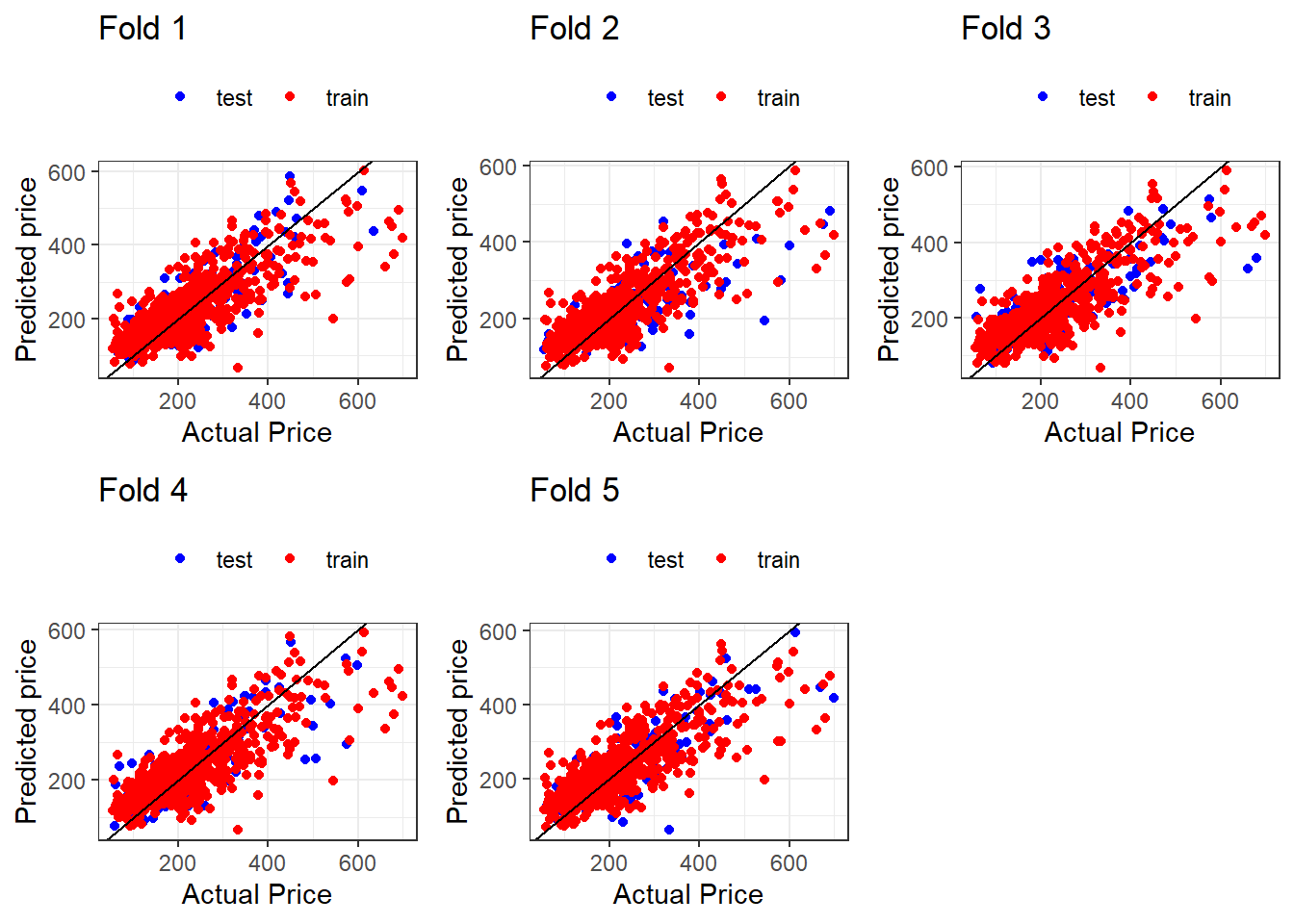

<- 5 <- sample (x = seq (N), size = N, replace = F) %>% split (f = 1 : split_n)<- rms_test <- vector ()<- matrix ()<- result_test <- list ()for (k in seq (split_n)) {<- I[[k]]<- sapply (setdiff (seq (split_n), k), function (x) I[[x]]) %>% Reduce (function (x, y) c (x, y), .)# <- qr (x = X[Itrain, ])<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% price[Itrain]<- solve (a = R) %*% b# if (k == 1 ) {<- x_hat %>% t ()else {<- rbind (coeff, x_hat %>% t ())<- (sum ((X[Itrain, ] %*% x_hat - price[Itrain])^ 2 ) / N)^ 0.5 <- (sum ((X[Itest, ] %*% x_hat - price[Itest])^ 2 ) / N)^ 0.5 <- data.frame (price[Itrain], X[Itrain, ] %*% x_hat)colnames (tmp01) <- c ("Actual Price for training" , "Predicted price(Training)" )<- tmp01head (tmp01) %>% print ()<- data.frame (price[Itest], X[Itest, ] %*% x_hat)colnames (tmp02) <- c ("Actual Price for test" , "Predicted price(Test)" )<- tmp02head (tmp02) %>% print ()colnames (coeff)[1 ] <- "constant"

constant area area exceeds 1.5 beds condo location2

[1,] 113.7676 178.6647 -39.56686 -19.70668 -14.71673 -96.28126

[2,] 123.3538 163.4534 -31.54539 -15.86756 -21.35463 -100.51723

[3,] 122.0812 179.1469 -52.46999 -19.06668 -19.10166 -107.97952

[4,] 112.6868 172.4583 -35.89811 -16.51583 -17.39511 -98.54583

[5,] 107.2806 184.2586 -54.30090 -18.71864 -23.81243 -102.39729

location3 location4

[1,] -105.7506 -26.00201

[2,] -109.4503 -26.71720

[3,] -113.8584 -20.72117

[4,] -106.4789 -33.09194

[5,] -108.9944 -18.19249

cbind (rms_train, rms_test)

rms_train rms_test

[1,] 63.14063 26.41506

[2,] 58.52871 35.42335

[3,] 60.07720 32.89232

[4,] 61.62543 29.78823

[5,] 61.73048 29.50860

<- function (k) {<- ggplot () + geom_point (mapping = aes (x = result_test[[k]][, 1 ], y = result_test[[k]][, 2 ], color = "test" )) + geom_point (mapping = aes (x = result_train[[k]][, 1 ], y = result_train[[k]][, 2 ], color = "train" )) + geom_abline (intercept = 0 , slope = 1 ) + labs (title = paste ("Fold" , k), x = "Actual Price" , y = "Predicted price" ) + scale_color_manual (values = c ("test" = "blue" , "train" = "red" )) + theme_bw () + theme (legend.title = element_blank (), legend.position = "top" )return (g)<- list ()for (k in seq (split_n)) {<- func_plot (k = k)arrangeGrob (grobs = g, ncol = 3 , widths = c (1 , 1 , 1 )) %>% ggpubr:: as_ggplot ()

14 Least squares classification > 14.2. Least squares classifier > 14.2.1 Iris flower classification (p.289)

$ Species %>% unique ()

[1] setosa versicolor virginica

Levels: setosa versicolor virginica

lapply (iris$ Species %>% unique (), function (x) iris[x == iris$ Species, ] %>% nrow ())

[[1]]

[1] 50

[[2]]

[1] 50

[[3]]

[1] 50

# setosa または versicolor:-1、virginica:1 <- c (rep (- 1 , 50 * 2 ), rep (1 , 50 ))<- cbind (constant = rep (1 , 50 * 3 ), iris[, - 5 ])<- qr (x = A)<- qr.Q (qr = QR)<- qr.R (qr = QR)# setosa または versicolor:-1、virginica:1 <- t (Q) %*% y<- solve (a = R) %*% b

[,1]

constant -2.390563727

Sepal.Length -0.091752169

Sepal.Width 0.405536771

Petal.Length 0.007975822

Petal.Width 1.103558650

# 混同行列 # 予測結果が 0 を超えている場合を TRUE、0 以下の場合を FALSE とする。 <- {%>% as.matrix (ncol = 5 )%*% {%>% matrix (ncol = 1 )> 0 <- matrix (nrow = 3 , ncol = 3 )1 , 1 ] <- {> 0 & yhat%>% sum ()1 , 2 ] <- {> 0 & ! yhat%>% sum ()2 , 1 ] <- {<= 0 & yhat%>% sum ()2 , 2 ] <- {<= 0 & ! yhat%>% sum ()1 , 3 ] <- sum (result[1 , ], na.rm = T)2 , 3 ] <- sum (result[2 , ], na.rm = T)3 , 1 ] <- sum (result[, 1 ], na.rm = T)3 , 2 ] <- sum (result[, 2 ], na.rm = T)3 , 3 ] <- sum (result[, 3 ], na.rm = T)

[,1] [,2] [,3]

[1,] 46 4 50

[2,] 7 93 100

[3,] 53 97 150

# エラーレート(混同行列より) 2 , 1 ] + result[1 , 2 ]) / result[3 , 3 ] * 100

# エラーレート(直接) > 0 != yhat%>% sum (.) / length (.)* 100

15 Multi-objective least squares > 15.1 Multi-objective least squares (p.309)

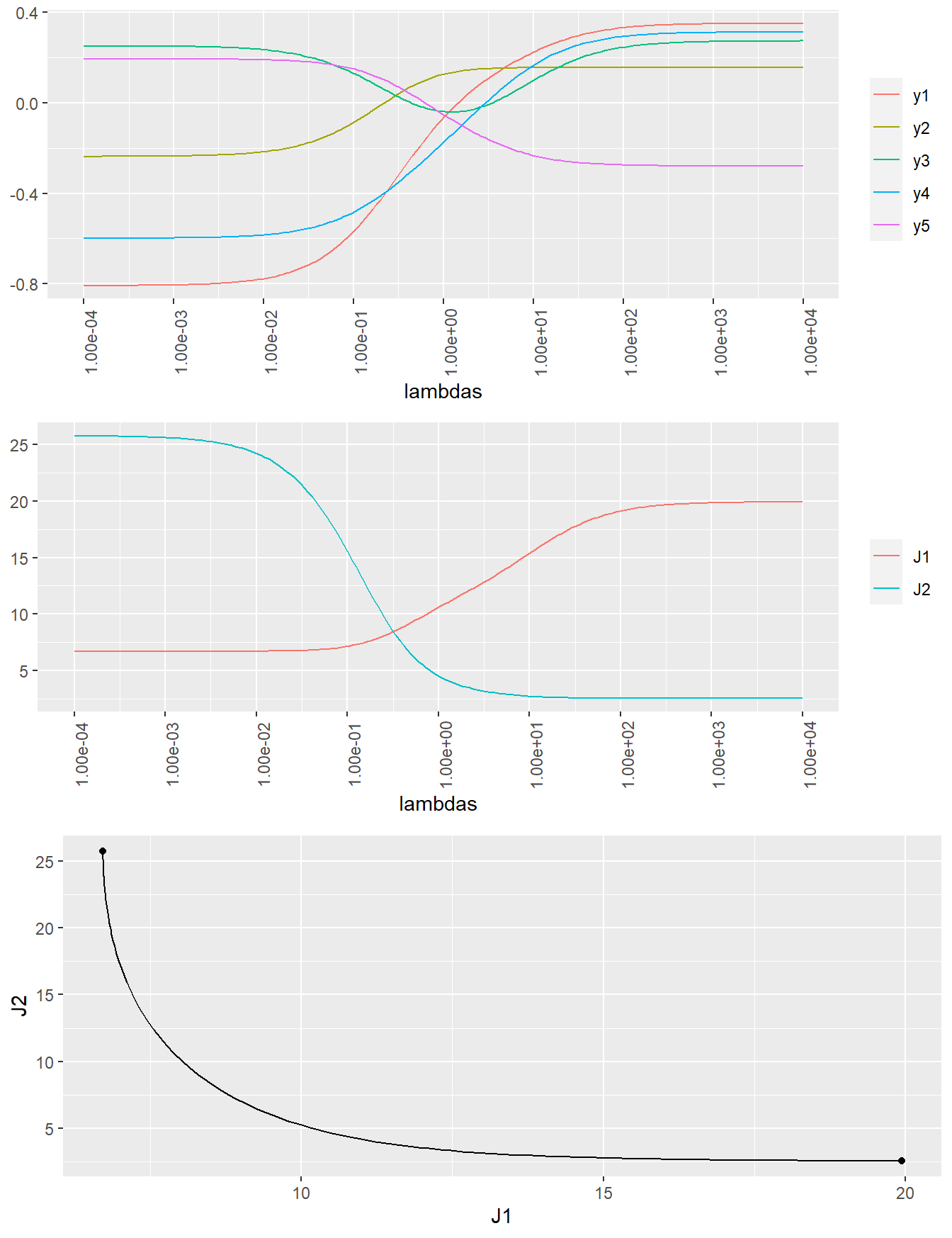

Simple example. (p.311)

\[\textbf{J}_1+\pmb{\lambda}\,\textbf{J}_2=\|\textbf{A}_1\textbf{x}-\textbf{b}_1\|^2+\pmb{\lambda}\|\textbf{A}_2\textbf{x}-\textbf{b}_2\|^2\]

# 各成分を正規分布に従う乱数とする、10行5列の係数行列Asを2つ作成。A1,A2。 <- lapply (1 : 2 , function (x) rnorm (n = 10 * 5 ) %>% matrix (nrow = 10 ))

[[1]]

[,1] [,2] [,3] [,4] [,5]

[1,] -0.5764545 -1.2517794 -1.3194900 0.18314402 0.5819281

[2,] -0.3555892 -0.2350122 0.6910679 0.80742416 1.7557272

[3,] -0.2114378 0.2855546 -0.2730222 0.08816272 -0.1411785

[4,] -0.1265300 -1.0962285 -1.4525525 0.09323329 1.0301720

[5,] 0.3060832 -0.1173152 2.4873203 -0.81418482 0.4714445

[6,] -1.5783925 -0.8069189 -0.1399969 0.05974993 -0.8550522

[7,] 1.1555883 -1.8666035 -1.0254329 0.21135256 0.1310137

[8,] -0.3858997 -0.7980896 -1.9238427 -1.45321751 -0.2958475

[9,] -1.9126730 0.7222369 -1.5591818 0.86685282 -1.0525068

[10,] 0.3190208 0.4045224 -0.9810830 -2.47484050 -0.6824009

[[2]]

[,1] [,2] [,3] [,4] [,5]

[1,] -0.1192845080 0.09184665 -0.44677671 0.92305104 1.09375793

[2,] 0.0398167849 0.47012014 1.03793019 0.02403625 0.11670805

[3,] -0.0120158994 -0.41944969 -1.41912126 -0.03405822 -0.04802264

[4,] -0.5286360872 -0.47469296 -0.36026265 0.25609285 0.02248308

[5,] 1.8154152537 0.11621730 -0.81834900 -0.55309170 -1.66909138

[6,] -1.9669145494 -0.91310054 0.91149666 0.25743373 0.14615414

[7,] 0.0007931109 -1.27830980 0.01939041 1.61988551 1.12395816

[8,] 0.2012440621 0.78542964 -0.64569148 1.43332374 1.12957959

[9,] -0.2799596661 -0.36944560 0.36293862 -0.49902198 -2.61827575

[10,] -1.2678346877 -1.57077281 1.14957028 -1.15634153 -0.27903538

# 各成分を正規分布に従う乱数とする、2行10列の目的変数行列bsを1つ作成。b1,b2。 <- rnorm (n = 2 * 10 ) %>% matrix (nrow = 2 )

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 0.9828555 0.08449577 1.0097209 0.25264180 -0.10292107 2.127883

[2,] -0.1374668 1.24323172 0.2357958 0.01651677 0.09162188 -1.200878

[,7] [,8] [,9] [,10]

[1,] -1.6337884 0.1521818 -1.1949303 0.9391474

[2,] 0.2111483 -0.2835552 0.8503887 -0.7893407

# 係数ラムダ。200次元。 <- 200 <- 10 ^ seq (- 4 , 4 , length.out = N)head (lambdas)tail (lambdas)

[1] 0.0001000000 0.0001096986 0.0001203378 0.0001320088 0.0001448118

[6] 0.0001588565

[1] 6294.989 6905.514 7575.250 8309.942 9115.888 10000.000

# 5行200列のゼロ行列xを1つ作成。 <- matrix (0 , 5 , 200 )# ゼロベクトル(N次元)J1、j2を作成。 <- J2 <- rep (0 , N)

<- function (As, bs, lambdas) {<- length (lambdas)# Atill 20(10*2)行5列の行列Atilを作成。 <- lapply (seq (k), function (i) (lambdas[i]^ 0.5 ) * As[[i]]) %>% Reduce (function (x, y) rbind (x, y), .)# btill 1行20列の行列btilを作成。 <- lapply (seq (k), function (i) (lambdas[i]^ 0.5 ) * bs[i, ]) %>% Reduce (function (x, y) c (x, y), .)# <- qr (x = Atil)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% btil<- solve (a = R) %*% breturn (x_hat)for (k in seq (N)) {# xのk列目に推定量を代入 <- func_mols_solve (As = As, bs = bs, lambdas = c (1 , lambdas[k]))<- norm (As[[1 ]] %*% x[, k] - bs[1 , ], type = "2" )^ 2 <- norm (As[[2 ]] %*% x[, k] - bs[2 , ], type = "2" )^ 2 <- t (x)colnames (x_t) <- c ("y1" , "y2" , "y3" , "y4" , "y5" )<- data.frame (lambdas, x_t) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ])# https://stackoverflow.com/questions/55113333/ggplot2-introduce-breaks-on-a-x-log-scale <- 10 ^ pretty (log10 (lambdas), n = 10 )<- formatC (x_breaks, format = "e" , digits = 2 )<- ggplot (data = df, mapping = aes (x = lambdas, y = value, color = key)) + geom_line () + scale_x_log10 (breaks = x_breaks, labels = x_labels) + theme (axis.title.y = element_blank (), legend.title = element_blank (),axis.text.x = element_text (angle = 90 )

<- data.frame (lambdas, J1, J2) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ])<- ggplot (data = df, mapping = aes (x = lambdas, y = value, color = key)) + geom_line () + scale_x_log10 (breaks = x_breaks, labels = x_labels) + theme (axis.title.y = element_blank (), legend.title = element_blank (),axis.text.x = element_text (angle = 90 )

<- qr (x = As[[1 ]])<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% bs[1 , ]<- solve (a = R) %*% b# <- qr (x = As[[2 ]])<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q) %*% bs[2 , ]<- solve (a = R) %*% b# <- c (norm (As[[1 ]] %*% x1 - bs[1 , ], type = "2" )^ 2 , norm (As[[1 ]] %*% x2 - bs[1 , ], type = "2" )^ 2 )<- c (norm (As[[2 ]] %*% x1 - bs[2 , ], type = "2" )^ 2 , norm (As[[2 ]] %*% x2 - bs[2 , ], type = "2" )^ 2 )# <- ggplot () + geom_line (mapping = aes (x = J1, y = J2)) + geom_point (mapping = aes (x = J1p, y = J2p))

arrangeGrob (g1, g2, g3, ncol = 1 , nrow = 3 , heights = c (1 , 1 , 1 )) %>% ggpubr:: as_ggplot ()

15 Multi-objective least squares > 15.3 Estimation and inversion > 15.3.2 Estimating a periodic time series (p.318)

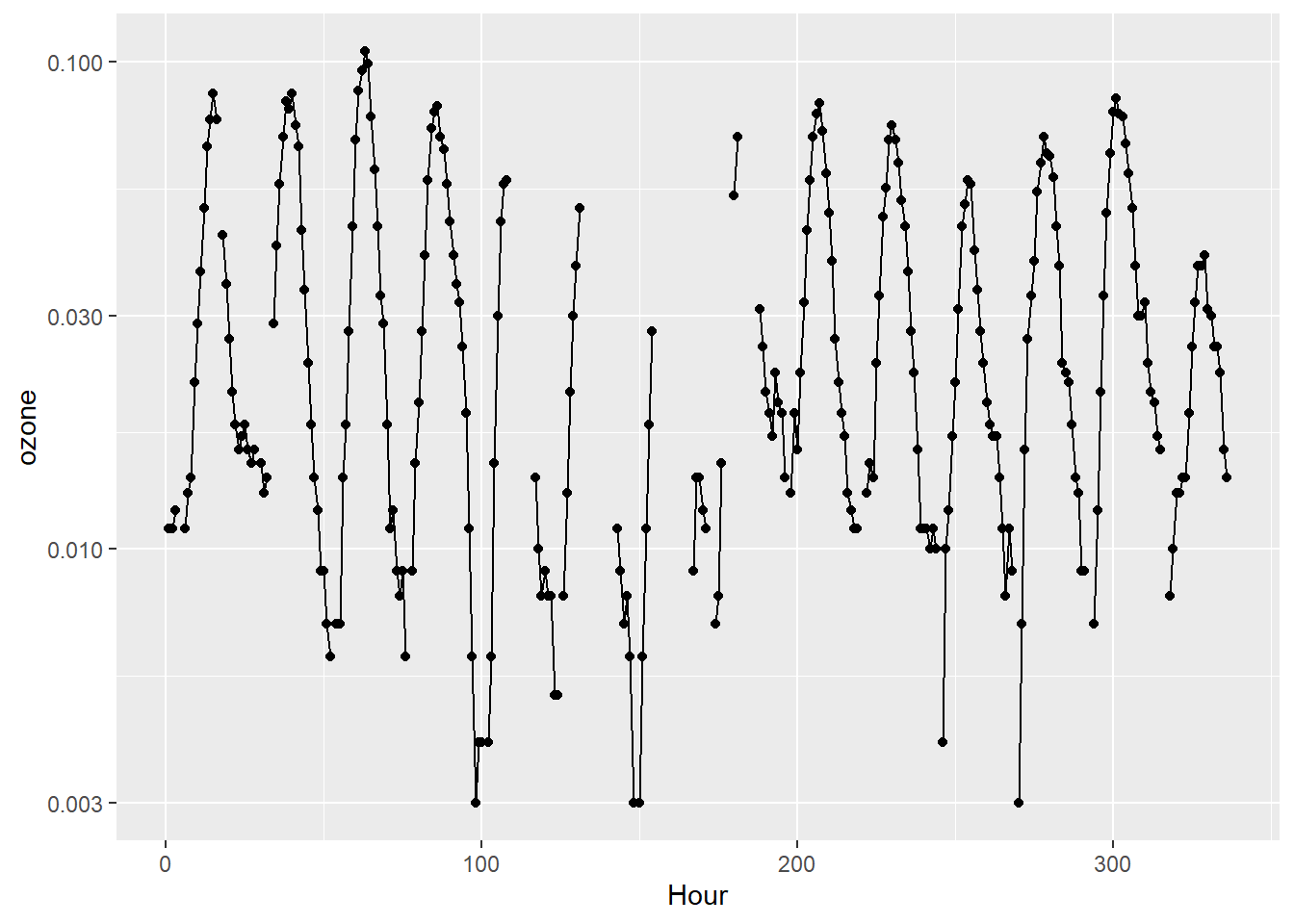

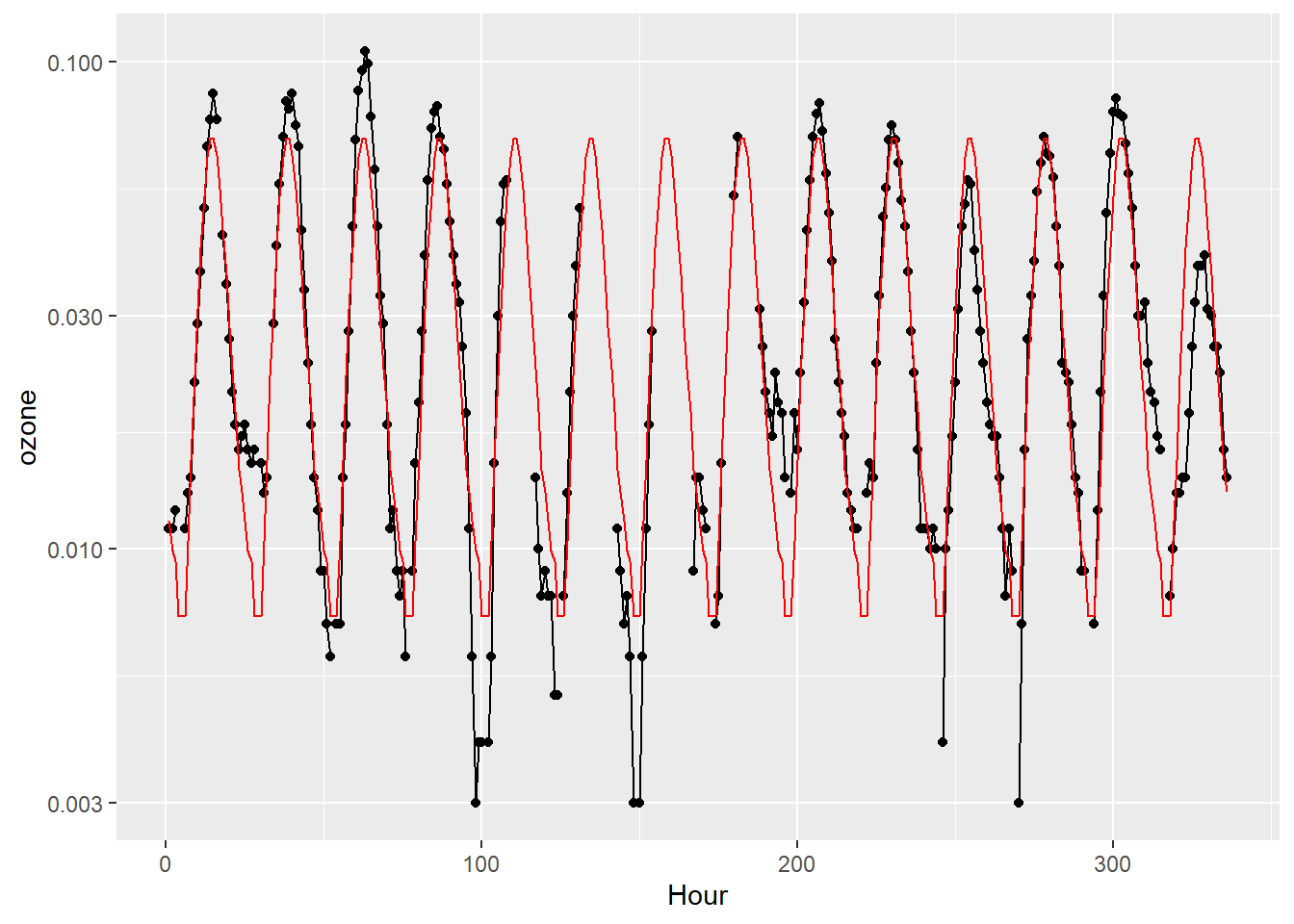

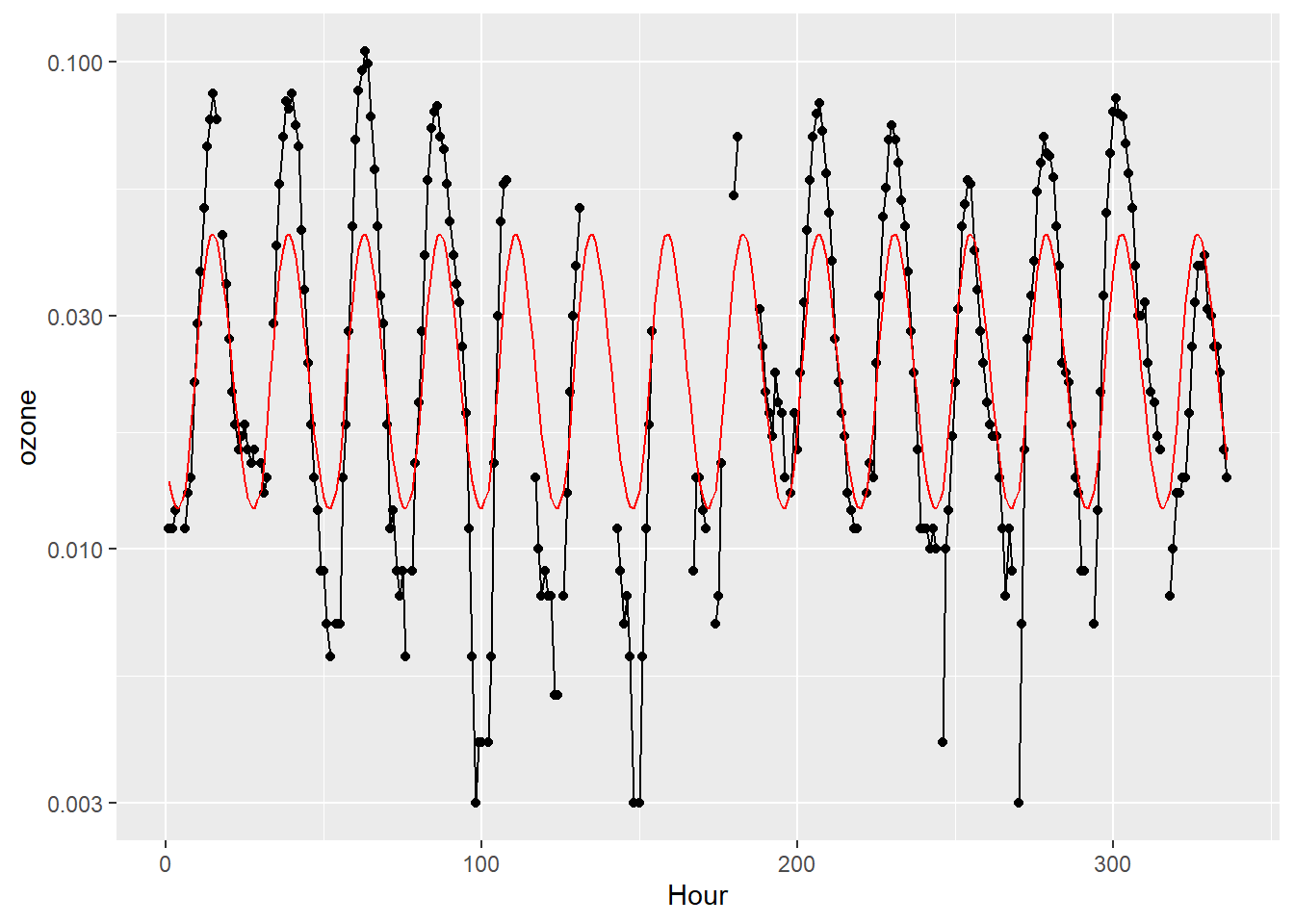

Example. (p.319)

# サンプルデータ # カリフォルニア州アズサ 2014年6月最初の14日間の1時間毎オゾン量データ summary (ozone)length (ozone)

Min. 1st Qu. Median Mean 3rd Qu. Max. NA's

0.00300 0.01200 0.02100 0.03046 0.04600 0.10500 61

[1] 336

以下を最小にする。 \[\|\textbf{Ax}-\textbf{y}\|^2+\lambda\|\textbf{Dx}\|^2\]

library (ggplot2)library (dplyr)<- 14 <- k * 24 <- seq (N)<- ggplot (mapping = aes (x = Hour, y = ozone)) + geom_line () + geom_point () + scale_y_log10 ()

正規方程式 \[\textbf{x}=\left(\textbf{A}^{'}\textbf{A}\right)^{-1}\textbf{A}^{'}\textbf{b}\]

<- lapply (seq (k), function (x) diag (1 , 24 )) %>% Reduce (function (x, y) rbind (x, y), .)<- diag (- 1 , 24 ) + rbind (cbind (rep (0 , 23 ), diag (1 , 23 )), c (1 , rep (0 , 23 )) %>% matrix (nrow = 1 ))<- ! is.na (ozone)%>% which ()<- list (A[ind, ], D)<- list (log (ozone[ind]), rep (0 , 24 ))<- function (lambdas) {<- length (lambdas)<- lapply (seq (n), function (i) sqrt (lambdas[i]) * As[[i]]) %>% Reduce (function (x, y) rbind (x, y), .)<- lapply (seq (n), function (i) sqrt (lambdas[i]) * bs[[i]]) %>% Reduce (function (x, y) c (x, y), .)<- {t (Atil) %*% Atil%>% solve ()%*% {t (Atil) %*% btil+ geom_line (mapping = aes (x = seq (N), y = rep (exp (x) %>% as.vector (), k)), color = "red" )%>% print ()list (head_A = head (A) %>% data.frame (), tail_A = tail (A) %>% data.frame (),head_D = head (D) %>% data.frame (), tail_D = tail (D) %>% data.frame (), dim_A = dim (A), dim_D = dim (D)

$head_A

X1 X2 X3 X4 X5 X6 X7 X8 X9 X10 X11 X12 X13 X14 X15 X16 X17 X18 X19 X20 X21

1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

3 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

4 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

5 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

6 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

X22 X23 X24

1 0 0 0

2 0 0 0

3 0 0 0

4 0 0 0

5 0 0 0

6 0 0 0

$tail_A

X1 X2 X3 X4 X5 X6 X7 X8 X9 X10 X11 X12 X13 X14 X15 X16 X17 X18 X19 X20

[331,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0

[332,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1

[333,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[334,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[335,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[336,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

X21 X22 X23 X24

[331,] 0 0 0 0

[332,] 0 0 0 0

[333,] 1 0 0 0

[334,] 0 1 0 0

[335,] 0 0 1 0

[336,] 0 0 0 1

$head_D

X1 X2 X3 X4 X5 X6 X7 X8 X9 X10 X11 X12 X13 X14 X15 X16 X17 X18 X19 X20 X21

1 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2 0 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

3 0 0 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

4 0 0 0 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

5 0 0 0 0 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

6 0 0 0 0 0 -1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0

X22 X23 X24

1 0 0 0

2 0 0 0

3 0 0 0

4 0 0 0

5 0 0 0

6 0 0 0

$tail_D

X1 X2 X3 X4 X5 X6 X7 X8 X9 X10 X11 X12 X13 X14 X15 X16 X17 X18 X19 X20

[19,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 -1 1

[20,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 -1

[21,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[22,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[23,] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

[24,] 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

X21 X22 X23 X24

[19,] 0 0 0 0

[20,] 1 0 0 0

[21,] -1 1 0 0

[22,] 0 -1 1 0

[23,] 0 0 -1 1

[24,] 0 0 0 -1

$dim_A

[1] 336 24

$dim_D

[1] 24 24

# λ = 1の場合 <- c (1 , 1 )func_plot (lambdas = lambdas)

# λ = 100の場合 <- c (1 , 100 )func_plot (lambdas = lambdas)

15 Multi-objective least squares > 15.4 Regularized data fitting (p.325)

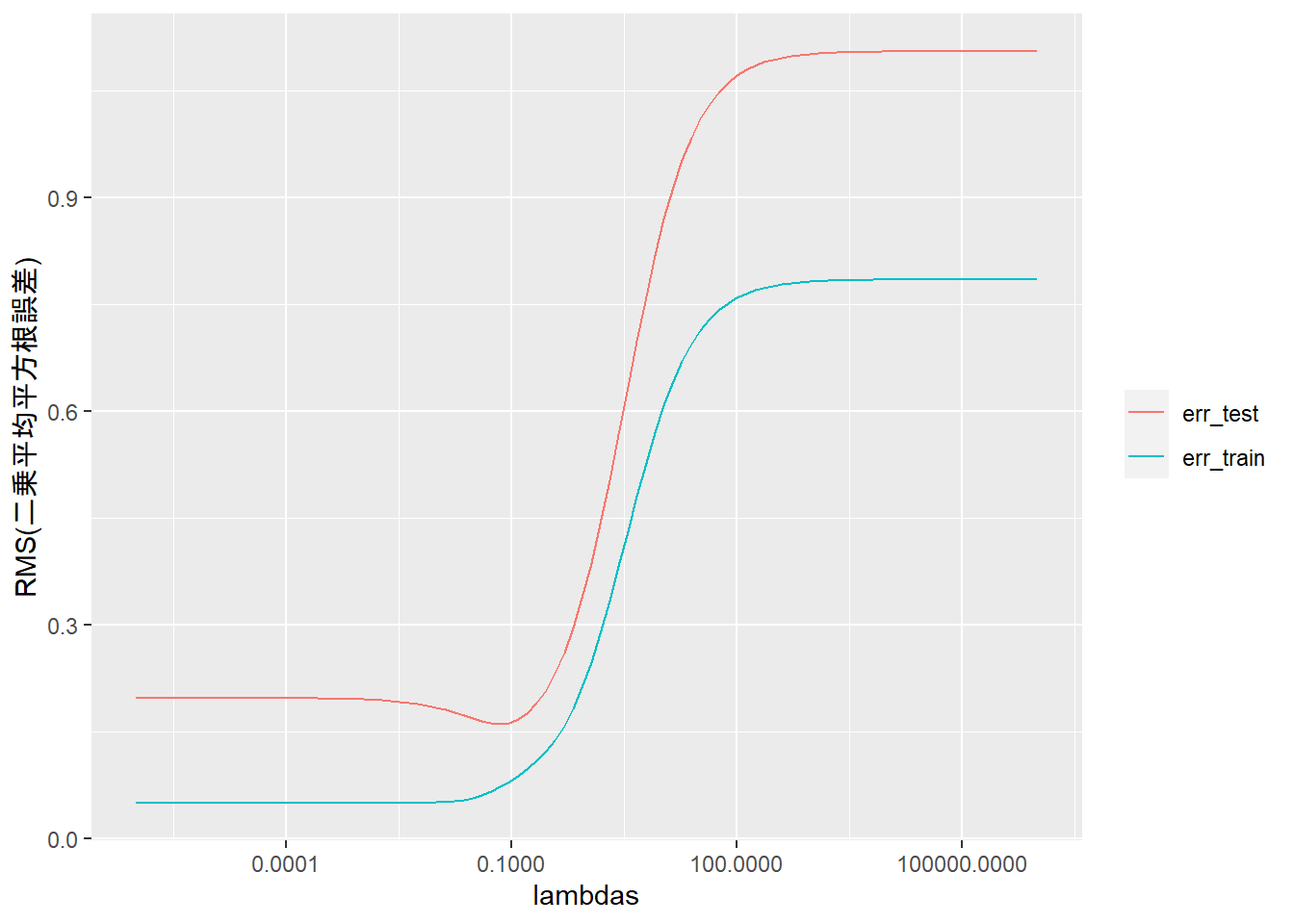

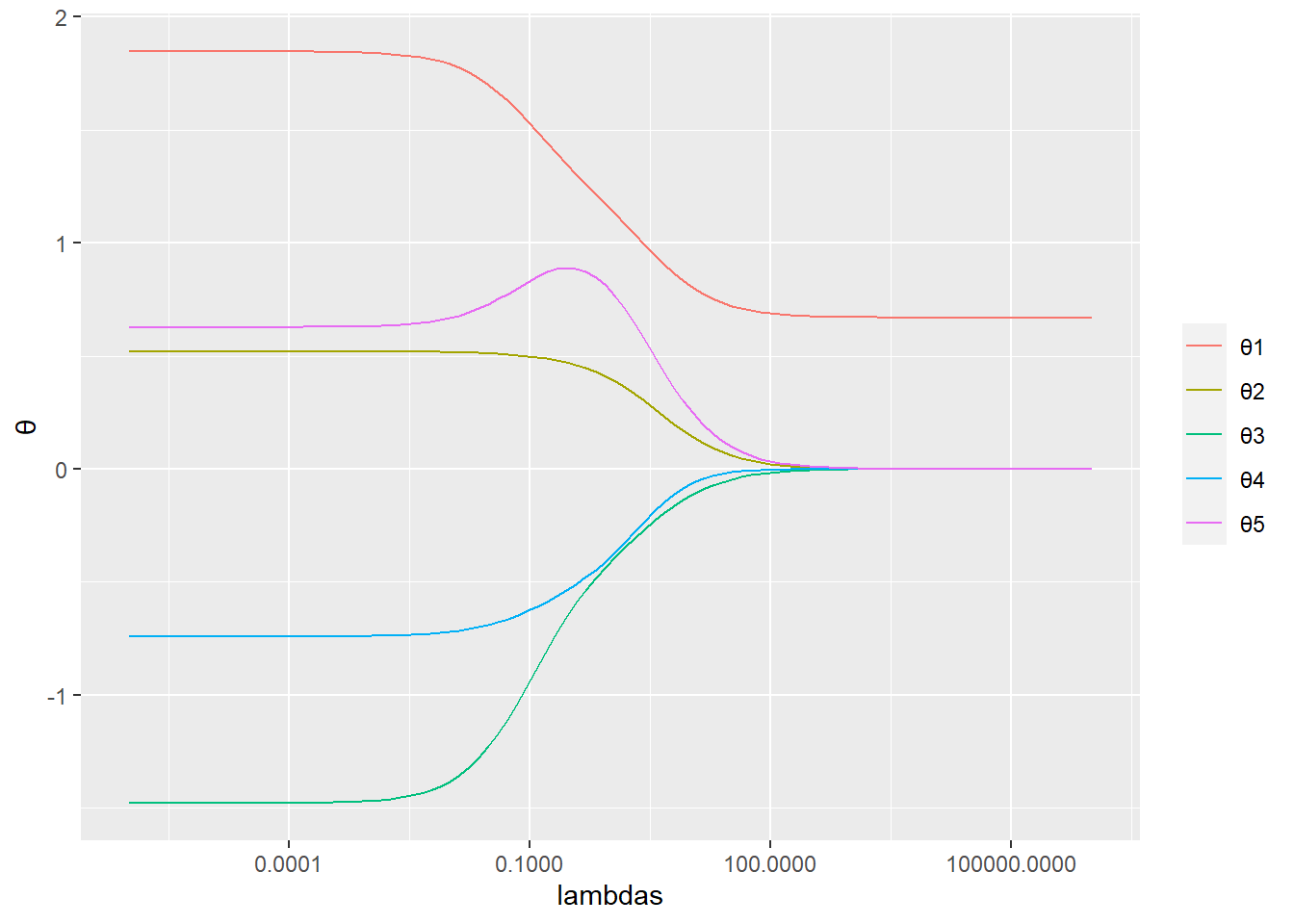

Example. (p.329)

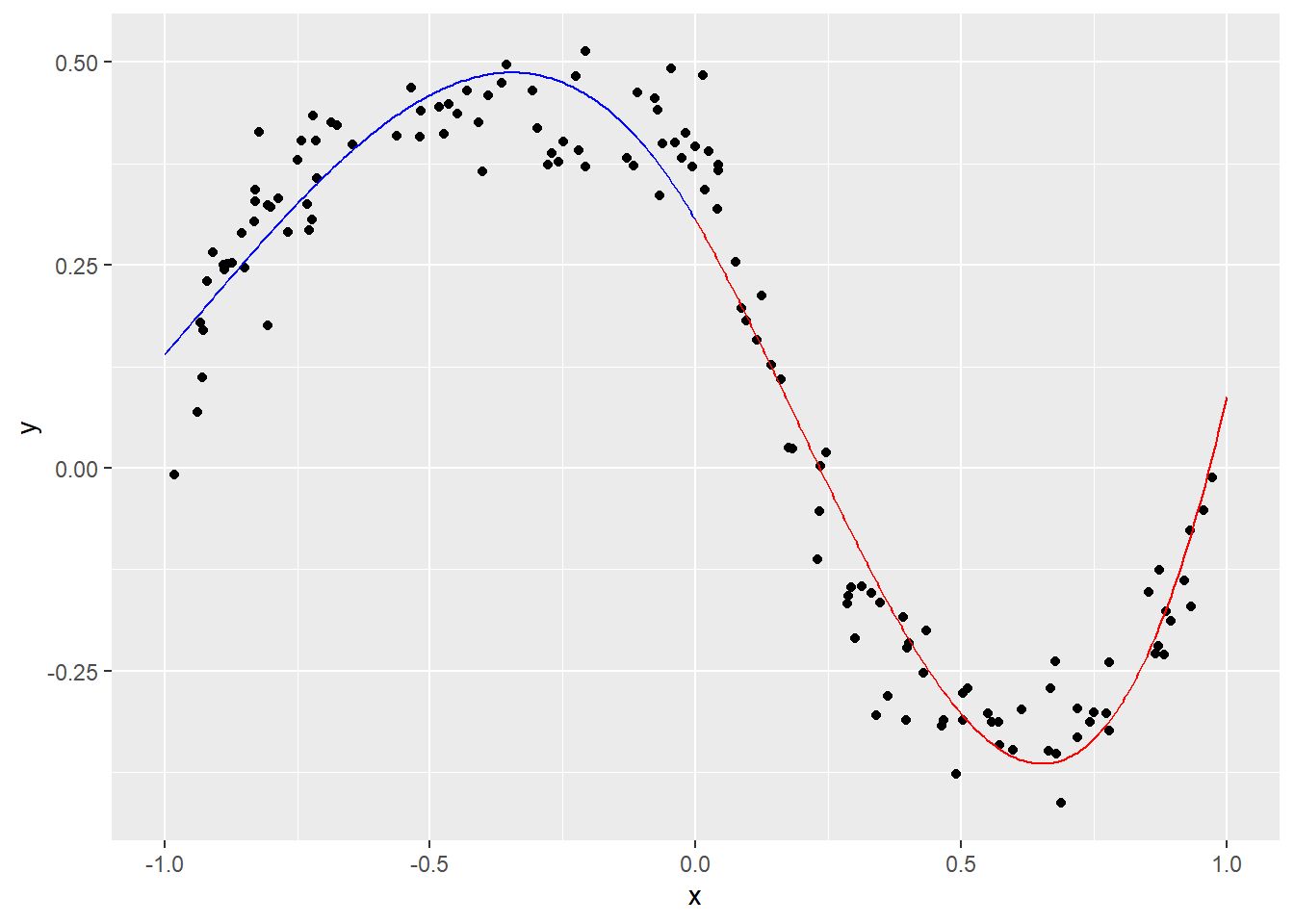

モデルは以下の通り。 \[\hat{f}(x)=\displaystyle\sum_{k=1}^5\theta_k\,f_k(x)\] ここで、\[f_1(x)=1,\quad f_{k+1}(x)=\textrm{sin}(\omega_k\,x+\phi_k)\]

以下を最小にする。 \[\displaystyle\sum_{i=1}^N\left(y^{(i)}-\displaystyle\sum_{k=1}^5\theta_k\,f_k\left(x^{(i)}\right)\right)^2+\lambda\displaystyle\sum_{k=2}^5\theta_k^2\]

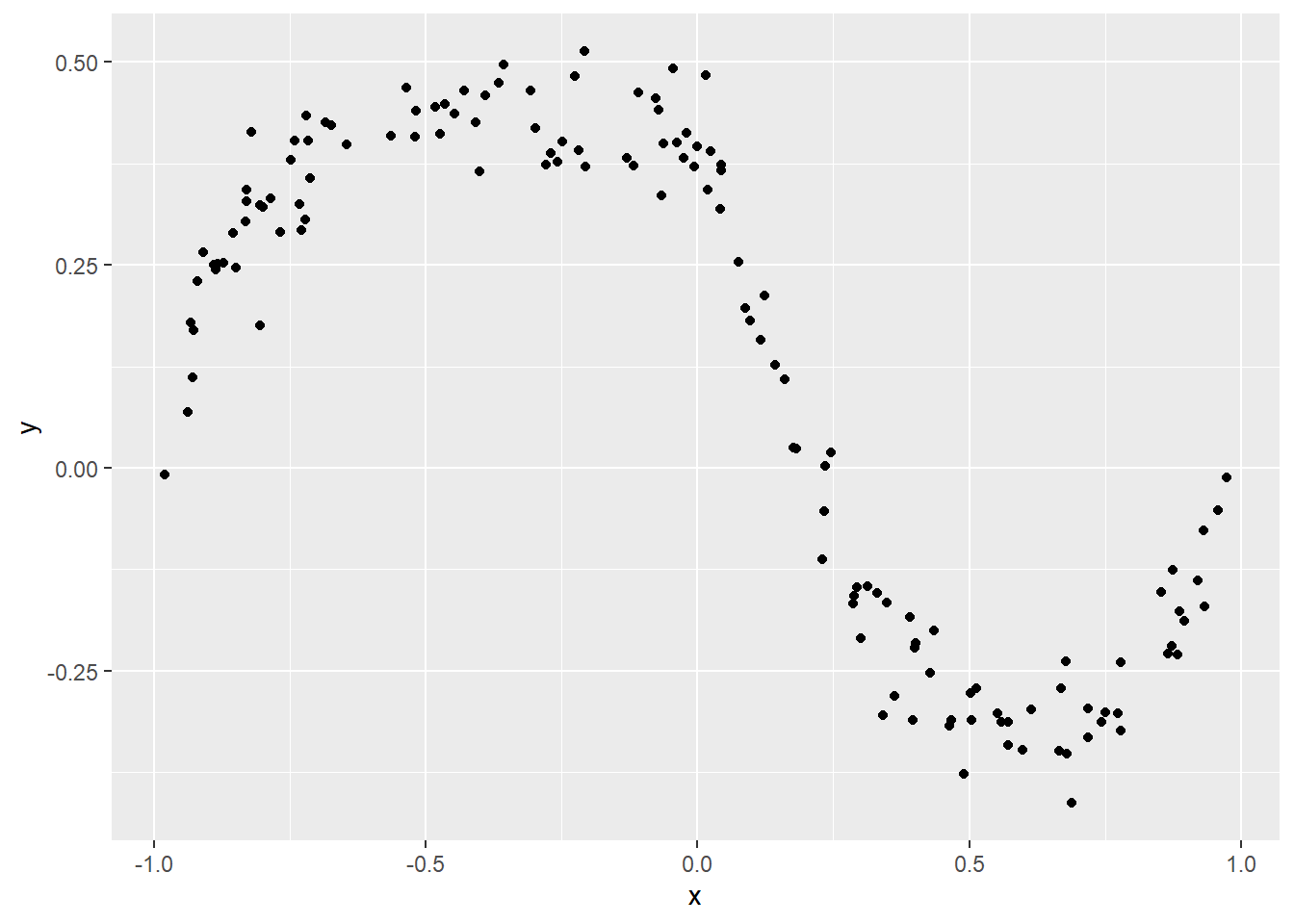

# サンプルデータ <- c (0.10683 , 0.25578 , 0.27112 , 0.30299 , 0.50204 , 0.65845 , 0.68423 , 0.70259 , 0.73406 , 0.94035 )<- c (1.82422 , 0.813549 , 0.92406 , 0.42067 , 0.446178 , - 0.0373407 , - 0.210935 , - 0.103327 , 0.332097 , 2.29278 )<- c (0.396674 , 0.777517 , 0.1184 , 0.223266 , 0.901463 , 0.358033 , 0.260402 , 0.804281 , 0.631664 , 0.149704 ,0.551333 , 0.663999 , 0.164948 , 0.651698 , 0.123026 , 0.337066 , 0.083208 , 0.204422 , 0.978 , 0.403676 <- c (- 1.05772 , 0.879117 , 1.98136 , 0.867012 , 2.1365 , - 0.701948 , 0.941469 , 1.49755 , 0.550205 , 1.34245 ,1.21445 , 0.00449111 , 0.957535 , 0.077864 , 1.73558 , - 0.325244 , 2.56555 , 1.10081 , 2.70644 , - 1.10049 sapply (list (xtrain, ytrain, xtest, ytest), function (x) length (x))

library (tensor)<- length (ytrain)<- length (ytest)<- 5 # 本例では ω と Φ は以下の通りに設定。 <- c (13.69 , 3.55 , 23.25 , 6.03 )<- c (0.21 , 0.02 , - 1.87 , 1.72 )<- cbind (rep (1 , N), {tensor (xtrain, omega) + tensor (rep (1 , N), phi)%>% sin ())<- cbind (rep (1 , Ntest), {tensor (xtest, omega) + tensor (rep (1 , Ntest), phi)%>% sin ())<- 100 <- 10 ^ (seq (- 6 , 6 , length.out = npts))<- rep (0 , npts)<- rep (0 , npts)<- matrix (0 , nrow = p, ncol = npts)<- bs <- list ()1 ]] <- A2 ]] <- cbind (rep (0 , p - 1 ), diag (1 , p - 1 ))1 ]] <- ytrain2 ]] <- rep (0 , p - 1 )list (As = As, bs = bs)

$As

$As[[1]]

[,1] [,2] [,3] [,4] [,5]

[1,] 1 0.9948324 0.3887242 0.5759759 0.7014342

[2,] 1 -0.5396620 0.8004341 -0.8047726 -0.1204674

[3,] 1 -0.7033080 0.8318740 -0.9613729 -0.2116481

[4,] 1 -0.9378355 0.8892096 -0.8951055 -0.3944204

[5,] 1 0.7171765 0.9733358 -0.3687390 -0.9993906

[6,] 1 0.1992548 0.7061848 0.7659977 -0.5586289

[7,] 1 -0.1517423 0.6385219 0.9951213 -0.4234755

[8,] 1 -0.3928044 0.5870404 0.9466722 -0.3207939

[9,] 1 -0.7409631 0.4931262 0.4891093 -0.1363772

[10,] 1 0.4942926 -0.2149590 0.9101233 0.8944167

$As[[2]]

[,1] [,2] [,3] [,4] [,5]

[1,] 0 1 0 0 0

[2,] 0 0 1 0 0

[3,] 0 0 0 1 0

[4,] 0 0 0 0 1

$bs

$bs[[1]]

[1] 1.8242200 0.8135490 0.9240600 0.4206700 0.4461780 -0.0373407

[7] -0.2109350 -0.1033270 0.3320970 2.2927800

$bs[[2]]

[1] 0 0 0 0

for (k in seq (npts)) {<- c (1 , lambdas[k])<- length (lam)<- lapply (seq (n), function (i) sqrt (lam[i]) * As[[i]]) %>% Reduce (function (x, y) rbind (x, y), .)<- lapply (seq (n), function (i) sqrt (lam[i]) * bs[[i]]) %>% Reduce (function (x, y) c (x, y), .)# 正規方程式 <- solve (t (Atil) %*% Atil) %*% (t (Atil) %*% btil)<- (sum ((ytrain - A %*% theta)^ 2 ) / length (ytrain))^ 0.5 <- (sum ((ytest - Atest %*% theta)^ 2 ) / length (ytest))^ 0.5 <- thetadata.frame (lambdas, err_train, err_test) %>% gather (key = "key" , value = "value" , colnames (.)[- 1 ]) %>% ggplot (mapping = aes (x = lambdas, y = value, color = key)) + geom_line () + scale_x_log10 () + labs (y = "RMS(二乗平均平方根誤差)" ) + theme (legend.title = element_blank ())

data.frame (lambdas, t (thetas)) %>% colnames (.)[- 1 ] <- paste0 ("θ" , seq (p))%>% gather (key = "key" , value = "value" , colnames (.)[- 1 ]) %>% ggplot (mapping = aes (x = lambdas, y = value, color = key)) + geom_line () + scale_x_log10 () + labs (y = "θ" ) + theme (legend.title = element_blank ())

16 Constrained least squares > 16.1 Constrained least squares problem (p.339)

Example. (p.340)

\(\textbf{Cx}=\textbf{d}\) を制約条件とした上で\[\|\textbf{Ax}-\textbf{b}\|^2+\lambda\|\textbf{Cx}-\textbf{d}\|^2\] を最小にする\(\hat{\textbf{x}}\) を求める。

<- 70 <- 2 * M<- runif (n = M) - 1 # 左半分 <= 0 <- runif (n = M) # 右半分 > 0 <- c (xleft, xright)<- x^ 3 - x + 0.4 / (1 + 25 * (x^ 2 )) + 0.05 * rnorm (n = N)<- 4 # (n-1)次多項式回帰 <- outer (X = xleft, Y = seq (n) - 1 , FUN = "^" )<- outer (X = xright, Y = seq (n) - 1 , FUN = "^" )<- rbind (cbind (vandermonde_matrix_l, matrix (0 , M, n)), cbind (matrix (0 , M, n), vandermonde_matrix_r))<- y# 制約条件 <- rbind (c (1 , rep (0 , n - 1 ), - 1 , rep (0 , n - 1 )), c (0 , 1 , rep (0 , n - 2 ), 0 , - 1 , rep (0 , n - 2 )))<- rep (0 , 2 ) # p(a)=q(a) かつ p'(a)=q'(a) list (A_head = head (A), A_tail = tail (A), b_head = head (b), b_tail = tail (b), C = C, d = d)

$A_head

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8]

[1,] 1 -0.22584533 0.051006113 -0.0115194923 0 0 0 0

[2,] 1 -0.93850066 0.880783494 -0.8266158924 0 0 0 0

[3,] 1 -0.82990560 0.688743308 -0.5715919297 0 0 0 0

[4,] 1 -0.12982116 0.016853534 -0.0021879453 0 0 0 0

[5,] 1 -0.07648605 0.005850116 -0.0004474523 0 0 0 0

[6,] 1 -0.83134750 0.691138662 -0.5745763970 0 0 0 0

$A_tail

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8]

[135,] 0 0 0 0 1 0.08709203 0.007585021 0.0006605948

[136,] 0 0 0 0 1 0.71907624 0.517070641 0.3718132130

[137,] 0 0 0 0 1 0.74376411 0.553185047 0.4114391830

[138,] 0 0 0 0 1 0.93150453 0.867700695 0.8082671305

[139,] 0 0 0 0 1 0.16058614 0.025787909 0.0041411809

[140,] 0 0 0 0 1 0.33064966 0.109329197 0.0361496619

$b_head

[1] 0.48326432 0.06828323 0.32857088 0.38150143 0.45600392 0.30391248

$b_tail

[1] 0.19722631 -0.29644311 -0.31285371 -0.07743325 0.10955205 -0.15481355

$C

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8]

[1,] 1 0 0 0 -1 0 0 0

[2,] 0 1 0 0 0 -1 0 0

$d

[1] 0 0

\(\hat{f}(x)\) は\(x=a\) を境に以下の2式からなる(本例では\(a=0\) )。

\[\begin{aligned}p(x|x\leq a)=\theta_1+\theta_2x+\theta_3x^2+\theta_4x^3\\

q(x|x>a)=\theta_5+\theta_6x+\theta_7x^2+\theta_8x^3\end{aligned}\]

よって誤差自乗平方和は、

\[\displaystyle\sum_{i=1}^M\left(\theta_1+\theta_2x_i+\theta_3x_i^2+\theta_4x_i^3-y_i\right)^2+\displaystyle\sum_{i=M+1}^N\left(\theta_5+\theta_6x_i+\theta_7x_i^2+\theta_8x_i^3-y_i\right)^2\] であり、連続データであるため\[p(x=a)-q(x=a)=0\] かつ\[p^{'}(x=a)-q^{'}(x=a)=0\] から\[p(a)-q(a)=0\,\therefore \theta_1+\theta_2a+\theta_3a^2+\theta_4a^3-\theta_5-\theta_6a-\theta_7a^2-\theta_8a^3=0\] および\[p^{'}(x=a)-q^{'}(x=a)=0\,\therefore \theta_2+2\theta_3a+3\theta_4a^2-\theta_6-2\theta_7a-3\theta_8a^2=0\] を満たす必要があり(スプライン)、行列で表すと\[C\theta=\begin{bmatrix}1&a&a^2&a^3&-1&-a&-a^2&-a^3\\0&1&2a&3a^2&0&-1&-2a&-3a^2\end{bmatrix}\theta=\begin{bmatrix}0\\0\end{bmatrix}\]

ggplot (mapping = aes (x = x, y = y)) + geom_point ()

# step1 <- qr (x = rbind (A, C))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- head (Q, nrow (A))<- tail (Q, - nrow (A))# step2 <- qr (x = t (Q2))<- qr.Q (qr = QR)<- qr.R (qr = QR)# step3 <- qr (x = t (Rtil))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% d<- solve (a = R0) %*% b0# step4 <- qr (x = Rtil)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% ({2 * t (Qtil)) %*% (t (Q1) %*% b)- 2 * x_hat)<- solve (a = R0) %*% b0<- x_hat# step5 <- qr (x = R)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% {{t (Q1) %*% b- {t (Q2) %*% (w / 2 )<- solve (a = R0) %*% b0

[,1]

[1,] 0.3055131

[2,] -1.1355761

[3,] -2.0067202

[4,] -0.7055567

[5,] 0.3055131

[6,] -1.1355761

[7,] -1.2440561

[8,] 2.1613579

<- 200 # <- seq (- 1 , 0 , length.out = Npl)<- outer (X = xpl_left, Y = seq (n) - 1 , FUN = "^" ) %*% head (theta, n)# <- seq (0 , 1 , length.out = Npl)<- outer (X = xpl_right, Y = seq (n) - 1 , FUN = "^" ) %*% tail (theta, - n)# ggplot () + geom_point (mapping = aes (x = x, y = y)) + geom_line (mapping = aes (x = xpl_left, y = ypl_left), color = "blue" ) + geom_line (mapping = aes (x = xpl_right, y = ypl_right), color = "red" )

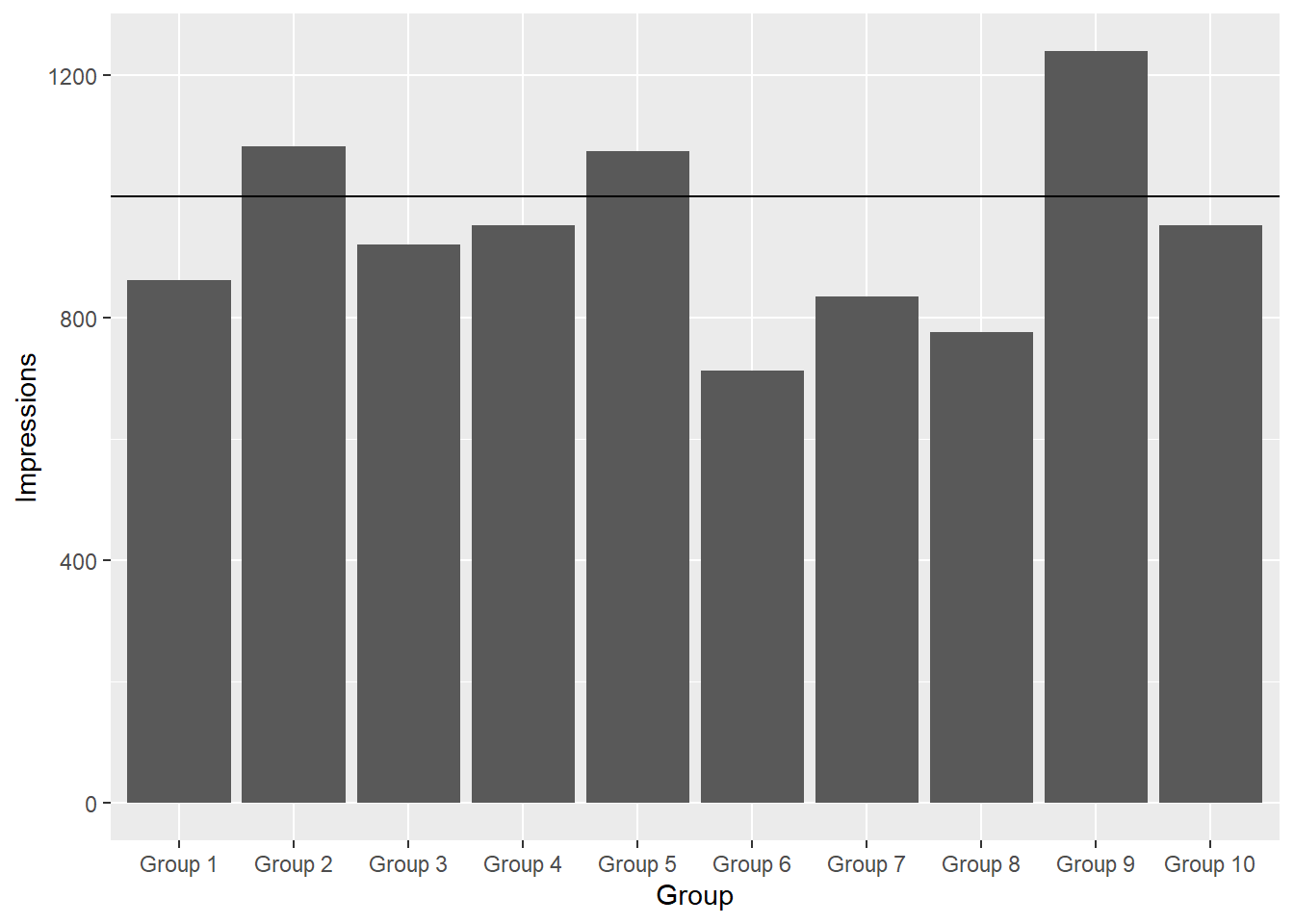

Advertising budget allocation. (p.341)

<- 3 # チャンネル数 <- 10 # 属性数 <- c ( # 1ドル当たり視聴数(単位:1000views) 0.97 , 1.86 , 0.41 ,1.23 , 2.18 , 0.53 ,0.80 , 1.24 , 0.62 ,1.29 , 0.98 , 0.51 ,1.10 , 1.23 , 0.69 ,0.67 , 0.34 , 0.54 ,0.87 , 0.26 , 0.62 ,1.10 , 0.16 , 0.48 ,1.92 , 0.22 , 0.71 ,1.29 , 0.12 , 0.62 %>% matrix (ncol = 3 , byrow = T)# s:広告支出 # v^des:目標視聴数 <- 1284

以下を最小にする。 \[\|Rs-v^{\textrm{des}}\|^2\]

但し制約として広告総予算を\(B\) とする。

\[\textbf{1}^{'}s=B\]

なお本例では\(B=1284\) とする。

<- R<- rep (10 ^ 3 , m) # 百万視聴/チャンネル <- rep (1 , n)<- B

# step1 <- qr (x = rbind (A, C))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- head (Q, nrow (A))<- tail (Q, - nrow (A))# step2 <- qr (x = t (Q2))<- qr.Q (qr = QR)<- qr.R (qr = QR)# step3 <- qr (x = t (Rtil))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% d<- solve (a = R0) %*% b0# step4 <- qr (x = Rtil)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% ({2 * t (Qtil)) %*% (t (Q1) %*% b)- 2 * x_hat)<- solve (a = R0) %*% b0<- x_hat# step5 <- qr (x = R)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% {{t (Q1) %*% b- {t (Q2) %*% (w / 2 )<- solve (a = R0) %*% b0

[,1]

[1,] 315.1682

[2,] 109.8664

[3,] 858.9654

<- A %*% theta %>% data.frame () %>% <- add_column (.data = ., Group = paste0 ("Group " , seq (nrow (.))), .before = 1 )%>% colnames (.)[2 ] <- "Impressions" $ Group <- factor (result$ Group, levels = result$ Group)ggplot (data = result) + geom_bar (mapping = aes (x = Group, y = Impressions), stat = "identity" , ) + geom_hline (yintercept = 1000 )

Group Impressions

1 Group 1 862.2405

2 Group 2 1082.4173

3 Group 3 920.9275

4 Group 4 952.3084

5 Group 5 1074.5068

6 Group 6 712.3586

7 Group 7 835.3201

8 Group 8 776.5670

9 Group 9 1239.1590

10 Group 10 952.3095

16 Constrained least squares > 16.1 Constrained least squares problem > 16.1.1 Least norm problem (p.342)

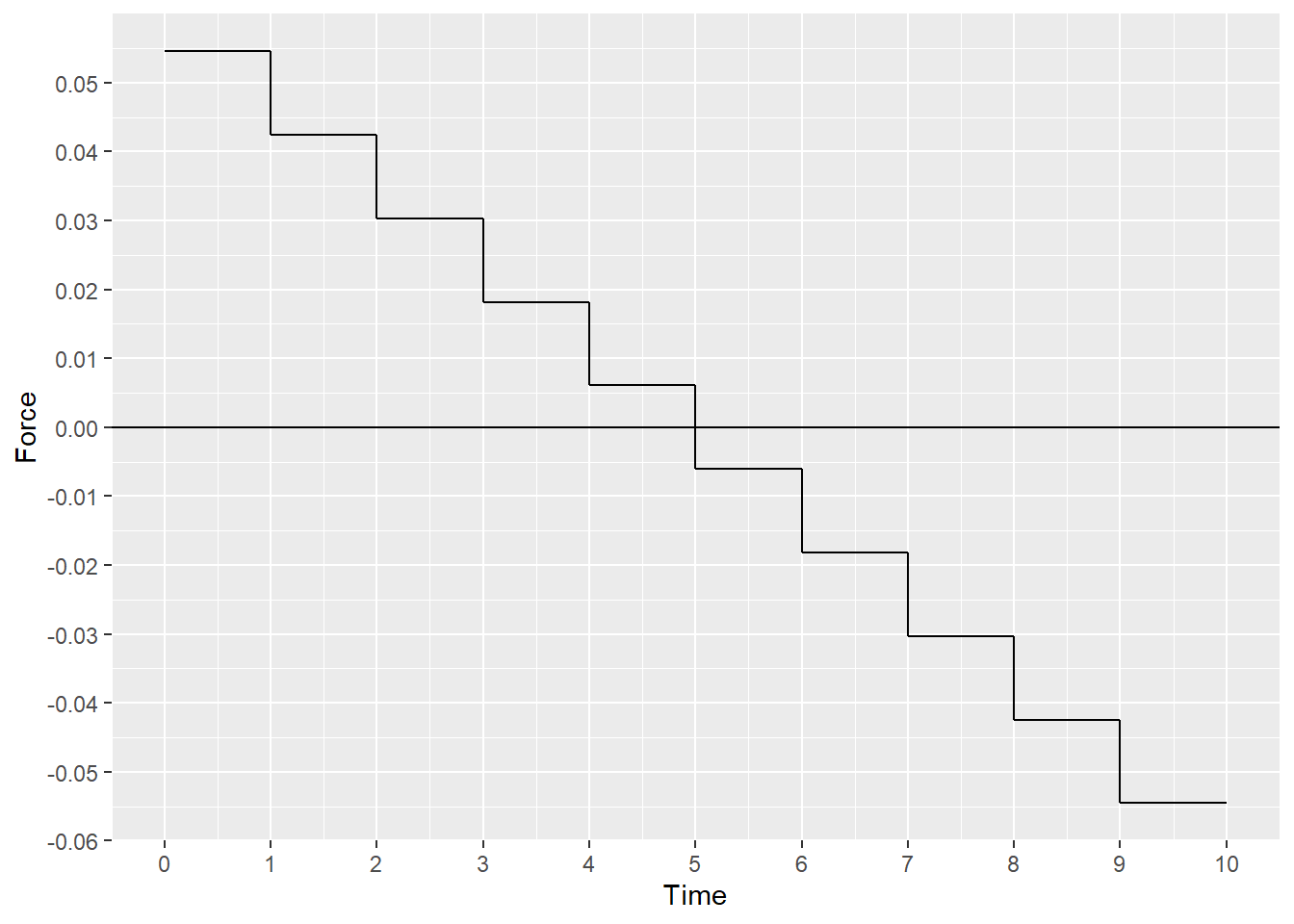

Example. (p.343)

最小ノルム問題は、\[\textbf{Cx}=\textbf{d}\] の制約を満たし、\[\|\textbf{Ax}-\textbf{b}\|^2=\|\textbf{Ix}-\textbf{0}\|^2=\|\textbf{x}\|^2\] が最小となる\(\hat{x}\) を求める問題。

<- diag (1 , nrow = 10 , ncol = 10 )<- rep (0 , 10 )<- rbind (rep (1 , 10 ), seq (9.5 , 0.4 , - 1 ))<- c (0 , 1 )

# step1 <- qr (x = rbind (A, C))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- head (Q, nrow (A))<- tail (Q, - nrow (A))# step2 <- qr (x = t (Q2))<- qr.Q (qr = QR)<- qr.R (qr = QR)# step3 <- qr (x = t (Rtil))<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% d<- solve (a = R0) %*% b0# step4 <- qr (x = Rtil)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% ({2 * t (Qtil)) %*% (t (Q1) %*% b)- 2 * x_hat)<- solve (a = R0) %*% b0<- x_hat# step5 <- qr (x = R)<- qr.Q (qr = QR)<- qr.R (qr = QR)<- t (Q0) %*% {{t (Q1) %*% b- {t (Q2) %*% (w / 2 )<- solve (a = R0) %*% b0

[,1]

[1,] 0.054545455

[2,] 0.042424242

[3,] 0.030303030

[4,] 0.018181818

[5,] 0.006060606

[6,] -0.006060606

[7,] -0.018181818

[8,] -0.030303030

[9,] -0.042424242

[10,] -0.054545455

ggplot () + geom_step (mapping = aes (x = seq (11 ) - 1 , y = c (theta, tail (theta, 1 ))), direction = "hv" ) + scale_x_continuous (breaks = scales:: pretty_breaks (10 )) + scale_y_continuous (breaks = scales:: pretty_breaks (10 )) + geom_hline (yintercept = 0 ) + labs (x = "Time" , y = "Force" )

\(v^{\textrm{fin}}=0\)

[,1]

[1,] -0.0000000000000001595946

\(p^{\textrm{fin}}=1\)

\(\|f^{\textrm{least norm}}\|^2\)

%>% norm (type = "2" ) %>% ^ 2

16 Constrained least squares > 16.2 Solution (p.344)

Optimality conditions via Lagrange multipliers. (p.344)

\(\textbf{Cx}=\textbf{d}\) を制約として、\(\|\textbf{Ax}-\textbf{b}\|^2\) が最小となる\(\hat{\textbf{x}}\) を求める。

ここで\(\textbf{A}\) は\((m\times n)\) 行列、\(\textbf{b}\) は\(m\) 次元ベクトル\(\begin{bmatrix}b_1\cdots b_m\end{bmatrix}^{T}\) 、\(\textbf{C}\) は\((p\times n)\) 行列、\(\textbf{d}\) は\(p\) 次元ベクトル\(\begin{bmatrix}d_1\cdots d_p\end{bmatrix}^{T}\) 、\(\textbf{c}^{T}_i\) は\(\textbf{C}\) の\(i\) 行目、\(\textbf{x}\) は\(n\) 次元ベクトル\(\begin{bmatrix}x_1\cdots x_n\end{bmatrix}^{T}\) 。

ラグランジュ乗数を\(p\) 次元ベクトル\(\textbf{z}=\begin{bmatrix}z_1\cdots z_p\end{bmatrix}\) とすると、ラグランジュ関数は \[L(\textbf{x},\textbf{z})=\|\textbf{Ax}-\textbf{b}\|^2+z_1(\textbf{c}^{T}_1\textbf{x}-d_1)+\cdots+z_p(\textbf{c}^{T}_p\textbf{x}-d_p)\]

\(\hat{\textbf{x}}\) が上記制約のもとでの最小化解ならば、推定されたラグランジュ乗数\(\hat{\textbf{z}}\) は \[\dfrac{\partial L}{\partial x_i}\left(\hat{\textbf{x}},\hat{\textbf{z}}\right)=0,\quad i=1,\cdots,n\] および\[\dfrac{\partial L}{\partial z_i}\left(\hat{\textbf{x}},\hat{\textbf{z}}\right)=0,\quad i=1,\cdots,p\] を満たす。

後者は\[\dfrac{\partial L}{\partial z_i}\left(\hat{\textbf{x}},\hat{\textbf{z}}\right)=\textbf{c}^{T}_i\hat{\textbf{x}}-d_i=0,\quad i=1,\cdots,p\] と表され、\(\hat{\textbf{x}}\) は\[\textbf{C}\hat{\textbf{x}}=\textbf{d}\] を満たす。

前者は最小化を求める\[\|\textbf{Ax}-\textbf{b}\|^2=\displaystyle\sum_{i=1}^m\left(\displaystyle\sum_{j=1}^n\textbf{A}_{ij}\textbf{x}_j-\textbf{b}_i\right)^2\] を\(x_i\) で偏微分して

\[\dfrac{\partial L}{\partial x_i}\left(\hat{\textbf{x}},\hat{\textbf{z}}\right)=2\displaystyle\sum_{j=1}^n\left(\textbf{A}^{T}\textbf{A}\right)_{ij}\hat{x}_j-2\left(\textbf{A}^{T}\textbf{b}\right)_i+\displaystyle\sum_{j=1}^p{\hat{\textbf{z}}_j(\textbf{c}_j)_i}=0\] と変形し、行列表現にすると、\[2\left(\textbf{A}^{T}\textbf{A}\right)\hat{x}-2\textbf{A}^{T}\textbf{b}+\textbf{C}^{T}\hat{\textbf{z}}=0\] と表せられる。

ここに制約条件\[\textbf{C}\hat{\textbf{x}}=\textbf{d}\] を組み合わせると、次の\((n+p)\) 元連立方程式となる。 \[\begin{bmatrix}2\textbf{A}^{T}\textbf{A} & \textbf{C}^{T}\\\textbf{C}&\textbf{0}\end{bmatrix}\begin{bmatrix}\hat{\textbf{x}}\\\hat{\textbf{z}}\end{bmatrix}=\begin{bmatrix}2\textbf{A}^{T}\textbf{b}\\\textbf{d}\end{bmatrix}\]

これはカルーシュ・クーン・タッカー条件(KKT matrix)と呼ばれ、制約なしの場合の正規方程式の拡張であり、制約付き最小二乗法問題は変数が\((n+p)\) 個の\((n+p)\) 連立方程式を解くことになる。

Invertibility of KKT matrix. (p.345)

また上記\((n+p)\times(n+p)\) 行列はカルーシュ・クーン・タッカー行列と呼ばれ、\(\textbf{C}\) の行が線形独立かつ\(\begin{bmatrix}\textbf{A}\\\textbf{C}\end{bmatrix}\) の列が線形独立の場合に限り、逆行列を持つ。

なお\(\textbf{C}\) の行が線形独立であるには\(\textbf{C}\) は横長行列または正方行列(\(p\leq n\) )である必要があり、\(\textbf{A}\) の列が線形独立の場合でも、\(\begin{bmatrix}\textbf{A}\\\textbf{C}\end{bmatrix}\) の列が線形独立となることがある。

\[\begin{bmatrix}\hat{\textbf{x}}\\\hat{\textbf{z}}\end{bmatrix}=\begin{bmatrix}2\textbf{A}^{T}\textbf{A} & \textbf{C}^{T}\\\textbf{C}&\textbf{0}\end{bmatrix}^{-1}\begin{bmatrix}2\textbf{A}^{T}\textbf{b}\\\textbf{d}\end{bmatrix}\]

上記式より\(\hat{\textbf{x}}\) は\(\textbf{b},\,\textbf{d}\) の線形関数となることがわかる。

16 Constrained least squares > 16.3 Solving constrained least squares problems (p.347)

Solving constrained least squares problems via QR factorization. (p.348)

次に\(\pmb{\omega}=\hat{\textbf{z}}-2\textbf{d}\) とし、カルーシュ・クーン・タッカー条件を変形する。 \[\begin{aligned}

&2\left(\textbf{A}^{T}\textbf{A}\right)\hat{\textbf{x}}+\textbf{C}^{T}\hat{\textbf{z}}\\

&=2\left(\textbf{A}^{T}\textbf{A}\right)\hat{\textbf{x}}+\textbf{C}^{T}(\pmb{\omega}+2\textbf{d})\\

&=2\left(\textbf{A}^{T}\textbf{A}\right)\hat{\textbf{x}}+\textbf{C}^{T}\pmb{\omega}+\textbf{C}^{T}2\textbf{d}\\

&=2\left(\textbf{A}^{T}\textbf{A}\right)\hat{\textbf{x}}+\textbf{C}^{T}\pmb{\omega}+\textbf{C}^{T}2\textbf{C}\hat{\textbf{x}}\\

&=2\left(\textbf{A}^{T}\textbf{A}+\textbf{C}^{T}\textbf{C}\right)\hat{\textbf{x}}+\textbf{C}^{T}\pmb{\omega}\\

&=2\textbf{A}^{T}\textbf{b},\quad \textbf{C}\hat{\textbf{x}}=\textbf{d}\end{aligned}\]

Step 1

続いて\(\begin{bmatrix}\textbf{A}\\\textbf{C}\end{bmatrix}\) をQR分解し、さらに\(\textbf{Q}\) を\(\textbf{Q}_1(m\times n)\) と\(\textbf{Q}_2(p\times n)\) に分割する。\[\begin{bmatrix}\textbf{A}\\\textbf{C}\end{bmatrix}=\textbf{QR}=\begin{bmatrix}\textbf{Q}_1\\\textbf{Q}_2\end{bmatrix}\textbf{R}\]

その後\(\textbf{A}=\textbf{Q}_1\textbf{R}\) 、\(\textbf{C}=\textbf{Q}_2\textbf{R}\) および \[\begin{aligned}

\textbf{A}^{T}\textbf{A}+\textbf{C}^{T}\textbf{C}&=(\textbf{Q}_1\textbf{R})^{T}(\textbf{Q}_1\textbf{R})+(\textbf{Q}_2\textbf{R})^{T}(\textbf{Q}_2\textbf{R})\\

&=\textbf{R}^{T}\textbf{Q}_1^{T}\textbf{Q}_1\textbf{R}+\textbf{R}^{T}\textbf{Q}_2^{T}\textbf{Q}_2\textbf{R}\\

&=\textbf{R}^{T}\left(\textbf{Q}_1^{T}\textbf{Q}_1+\textbf{Q}_2^{T}\textbf{Q}_2\right)\textbf{R}\\

&=\textbf{R}^{T}\left(\textbf{Q}^{T}\textbf{Q}\right)\textbf{R}\\

&=\textbf{R}^{T}\textbf{I}\textbf{R}=\textbf{R}^{T}\textbf{R}

\end{aligned}\] を代入して、 \[2\textbf{R}^{T}\textbf{R}\hat{\textbf{x}}+\textbf{R}^{T}\textbf{Q}_2^T\omega=2\textbf{R}^T\textbf{Q}_1^T\textbf{b},\quad \textbf{Q}_2\textbf{R}\hat{\textbf{x}}=\textbf{d}\] が得られる。

\(\textbf{Q}\) は直交行列であるため\(\textbf{Q}^T\textbf{Q}=\textbf{I}\)

\(\textbf{Q}_1^{T}\textbf{Q}_1+\textbf{Q}_2^{T}\textbf{Q}_2=\textbf{Q}^{T}\textbf{Q}\) の例

<- sample (seq (100 ), 36 , replace = F) %>% matrix (nrow = 6 )<- Q[1 : 4 , ] # 4行6列 <- Q[5 : 6 , ] # 2行6列 <- (t (Q1) %*% Q1) + (t (Q2) %*% Q2)<- t (Q) %*% Q== b

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] TRUE TRUE TRUE TRUE TRUE TRUE

[2,] TRUE TRUE TRUE TRUE TRUE TRUE

[3,] TRUE TRUE TRUE TRUE TRUE TRUE

[4,] TRUE TRUE TRUE TRUE TRUE TRUE

[5,] TRUE TRUE TRUE TRUE TRUE TRUE

[6,] TRUE TRUE TRUE TRUE TRUE TRUE

前者の式に左から\(\left(\textbf{R}^T\right)^{-1}\) を乗じると、

\[\begin{aligned}

\left(\textbf{R}^T\right)^{-1}\left(2\textbf{R}^{T}\textbf{R}\hat{\textbf{x}}+\textbf{R}^{T}\textbf{Q}_2^T\omega\right)&=\left(\textbf{R}^T\right)^{-1}2\textbf{R}^T\textbf{Q}_1^T\textbf{b}\\

\left(\textbf{R}^T\right)^{-1}\left(2\textbf{R}^{T}\textbf{R}\hat{\textbf{x}}\right)+\left(\textbf{R}^T\right)^{-1}\left(\textbf{R}^{T}\textbf{Q}_2^T\omega\right)&=2\left(\textbf{R}^T\right)^{-1}\textbf{R}^T\textbf{Q}_1^T\textbf{b}\\

2\left(\textbf{R}^T\right)^{-1}\textbf{R}^{T}\textbf{R}\hat{\textbf{x}}+\left(\textbf{R}^T\right)^{-1}\textbf{R}^{T}\textbf{Q}_2^T\omega&=2\textbf{I}\textbf{Q}_1^T\textbf{b}\\

2\textbf{I}\textbf{R}\hat{\textbf{x}}+\textbf{I}\textbf{Q}_2^T\omega&=2\textbf{I}\textbf{Q}_1^T\textbf{b}\\

\textbf{R}\hat{\textbf{x}}&=\textbf{I}\textbf{Q}_1^T\textbf{b}-(1/2)\textbf{I}\textbf{Q}_2^T\omega\\

\textbf{R}\hat{\textbf{x}}&=\textbf{Q}_1^T\textbf{b}-(1/2)\textbf{Q}_2^T\omega\\

\end{aligned}\]

これを\(\textbf{C}\hat{\textbf{x}}=\textbf{d}\) に代入すると、 \[\textbf{C}\hat{\textbf{x}}=\textbf{Q}_2\textbf{R}\hat{\textbf{x}}=\textbf{Q}_2\left(\textbf{Q}_1^T\textbf{b}-(1/2)\textbf{Q}_2^T\omega\right)=\textbf{Q}_2\textbf{Q}_1^T\textbf{b}-\textbf{Q}_2(1/2)\textbf{Q}_2^T\omega=\textbf{d}\] より、\[\textbf{Q}_2\textbf{Q}_2^T\omega=2\textbf{Q}_2\textbf{Q}_1^T\textbf{b}-2\textbf{d}\]

\(\begin{bmatrix}\textbf{A}\\\textbf{C}\end{bmatrix}\) の列ベクトルは線形独立(フルランク)を仮定しているため、そのQR分解による行列Rは、対角成分が非ゼロ(すべて正の値)であり、行列式(対角成分の積)もゼロではなく、つまり特異行列ではない(正則行列である)。よってRの逆行列は存在し、Rの転置の逆行列(Rのランクは変わらない)も存在する。

Step 2

次に\(\textbf{Q}_2^T\) (線形独立の行列(証明はVMLSのp.348)。故に以下の\(\tilde{\textbf{R}}\) は逆行列を持つ)をQR分解し、\(\textbf{Q}_2^T=\tilde{\textbf{Q}}\tilde{\textbf{R}}\Leftrightarrow \textbf{Q}_2=\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\) を代入すると

\[\begin{aligned}

\textbf{Q}_2\textbf{Q}_2^T\omega&=2\textbf{Q}_2\textbf{Q}_1^T\textbf{b}-2\textbf{d}\\

\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\tilde{\textbf{Q}}\tilde{\textbf{R}}\omega&=2\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\textbf{d}\\

\tilde{\textbf{R}}^T\textbf{I}\tilde{\textbf{R}}\omega&=2\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\textbf{d}\\

\tilde{\textbf{R}}^T\tilde{\textbf{R}}\omega&=2\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\textbf{d}\\

\left(\tilde{\textbf{R}}^T\right)^{-1} \tilde{\textbf{R}}^T\tilde{\textbf{R}}\omega&=2\left(\tilde{\textbf{R}}^T\right)^{-1}\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\\

\textbf{I}\tilde{\textbf{R}}\omega&=2\textbf{I}\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\\

\tilde{\textbf{R}}\omega&=2\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\\

\end{aligned}\] が得られる。

\(\textbf{Q}_2^T=\tilde{\textbf{Q}}\tilde{\textbf{R}}\Leftrightarrow\textbf{Q}_2=\tilde{\textbf{R}}^T\tilde{\textbf{Q}}^T\) の例

<- sample (seq (100 ), 36 , replace = F) %>% matrix (nrow = 6 )<- qr (t (A))<- qr.Q (QR)<- qr.R (QR)list (A_t = t (A), QR = Q %*% R, A = A, R_tQ_t = t (R) %*% t (Q))

$A_t

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 3 8 17 1 18 21

[2,] 46 100 14 97 62 27

[3,] 7 43 36 24 68 88

[4,] 55 73 86 98 28 50

[5,] 31 15 38 45 64 49

[6,] 16 41 80 87 57 76

$QR

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 3 8 17 1 18 21

[2,] 46 100 14 97 62 27

[3,] 7 43 36 24 68 88

[4,] 55 73 86 98 28 50

[5,] 31 15 38 45 64 49

[6,] 16 41 80 87 57 76

$A

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 3 46 7 55 31 16

[2,] 8 100 43 73 15 41

[3,] 17 14 36 86 38 80

[4,] 1 97 24 98 45 87

[5,] 18 62 68 28 64 57

[6,] 21 27 88 50 49 76

$R_tQ_t

[,1] [,2] [,3] [,4] [,5] [,6]

[1,] 3 46 7 55 31 16

[2,] 8 100 43 73 15 41

[3,] 17 14 36 86 38 80

[4,] 1 97 24 98 45 87

[5,] 18 62 68 28 64 57

[6,] 21 27 88 50 49 76

Step 3

上記の通り\(\textbf{Q}_2^T\) は線形独立であるため、そのQR分解の行列Rの行列式は非ゼロ、逆行列を持つ。

そこで始めに\[\left(\tilde{\textbf{R}}^T\right)\left(\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\right)=\textbf{d}\] から\(\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\) からを求め、

Step 4

求めた\(\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\) を\[\tilde{\textbf{R}}\omega=2\tilde{\textbf{Q}}^T\textbf{Q}_1^T\textbf{b}-2\left(\tilde{\textbf{R}}^T\right)^{-1}\textbf{d}\] に代入して\(\omega\) を求める。

Step 5

最後に求めた\(\omega\) を\[\textbf{R}\hat{\textbf{x}}=\textbf{Q}_1^T\textbf{b}-(1/2)\textbf{Q}_2^T\omega\] に代入して\(\hat{\textbf{x}}\) を求める。

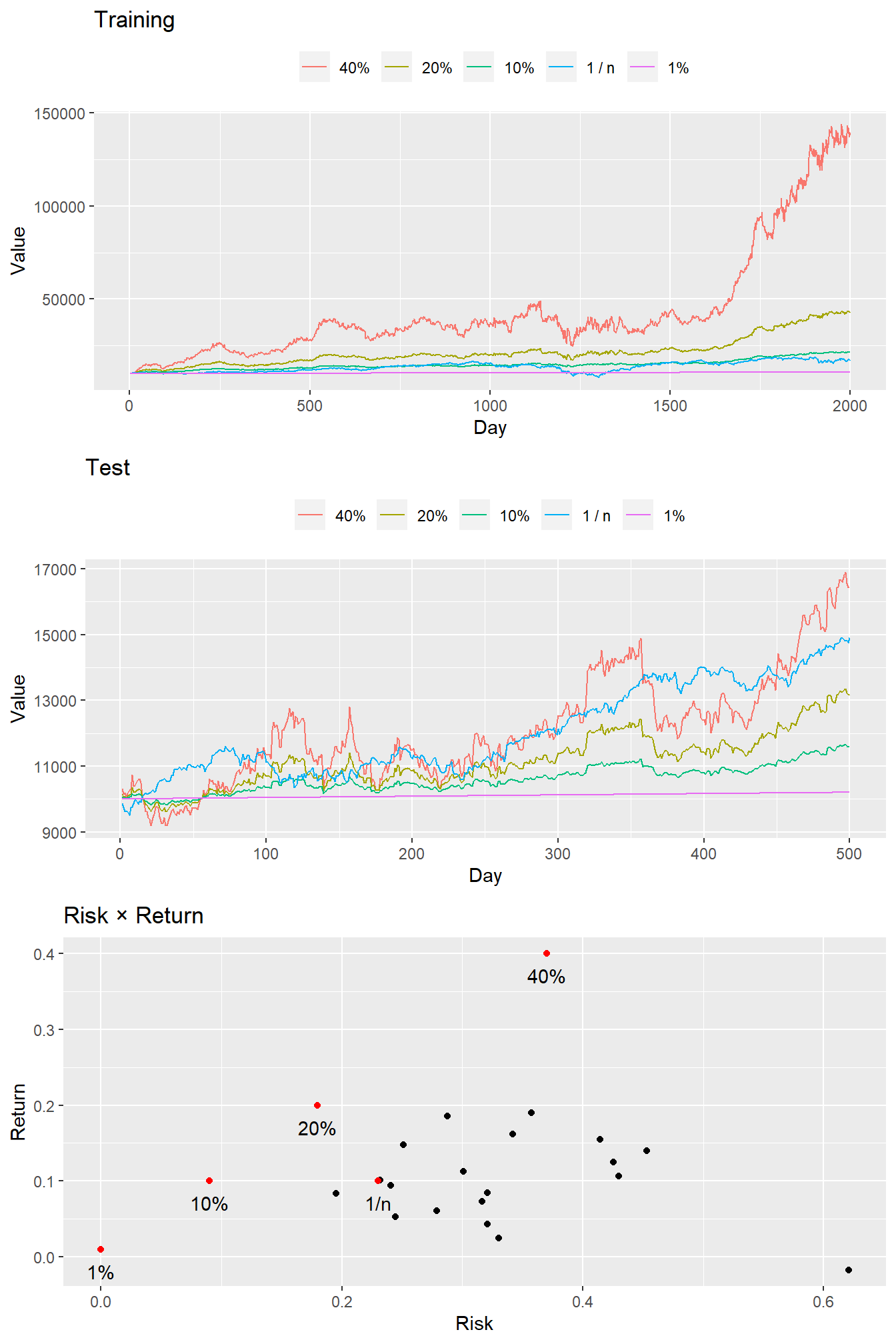

17 Constrained least squares applications > 17.1 Portfolio optimization > 17.1.3 Example (p.362)

# R:2000日分(8年)の日次リターン。1:19列は19銘柄のリターン。20列はリスクフリー資産のリターン(年間リターン1%。250*(4/10^5)=0.01) # Rtest:Rとは異なる500日分(2年)の日次リターン。 # 列:銘柄(n)、行:日(T) lapply (list (R, Rtest), dim)

[[1]]

[1] 2000 20

[[2]]

[1] 500 20

ハイリターン・ローリスクの資産アロケーション(\(w\) )を求める。

\(T\) をピリオド、\(\rho\) を望むポートフォリオリターン、\(\mu=R^T\,\textbf{1}/T\) は各銘柄毎の\(T\) 期間における平均リターン(n次元ベクトル)とすると、\(\rho\) は、

\[\textbf{avg}(r)=(1/T)\,\textbf{1}^T\,(Rw)=\mu^Tw=\rho\]

と表せられ、リスク(標準偏差)の2乗は \[\textbf{std}(r)^2=(1/T)\|r-\textbf{avg}(r)\textbf{1}\|^2=(1/T)\|r-\rho\textbf{1}\|^2\] となる。

ポートフォリオリターン\(\rho\) の制約のもと、リスクの2乗を最小化するとは \[\begin{bmatrix}\textbf{1}^T\\\mu^T\end{bmatrix}w=\begin{bmatrix}1\\\rho\end{bmatrix}\] の制約のもと\[\|Rw-\rho\textbf{1}\|\] を最小化することである。

なお\(1/T\) は結果に影響しないため含めない。

上段は各銘柄への割当ウエイトの合計が1になることを、下段は平均ポートフォリオリターンが\(\rho\) になる制約を表している。

つまりポートフォリオ最適化問題は以下の式を解くことになる。 \[\begin{bmatrix}w\\z_1\\z_2\end{bmatrix}=\begin{bmatrix}2R^TR&1&\mu\\\textbf{1}^T&0&0\\\mu^T&0&0\end{bmatrix}^{-1}\begin{bmatrix}2\rho T\mu\\1\\\rho\end{bmatrix}\]