Analysis

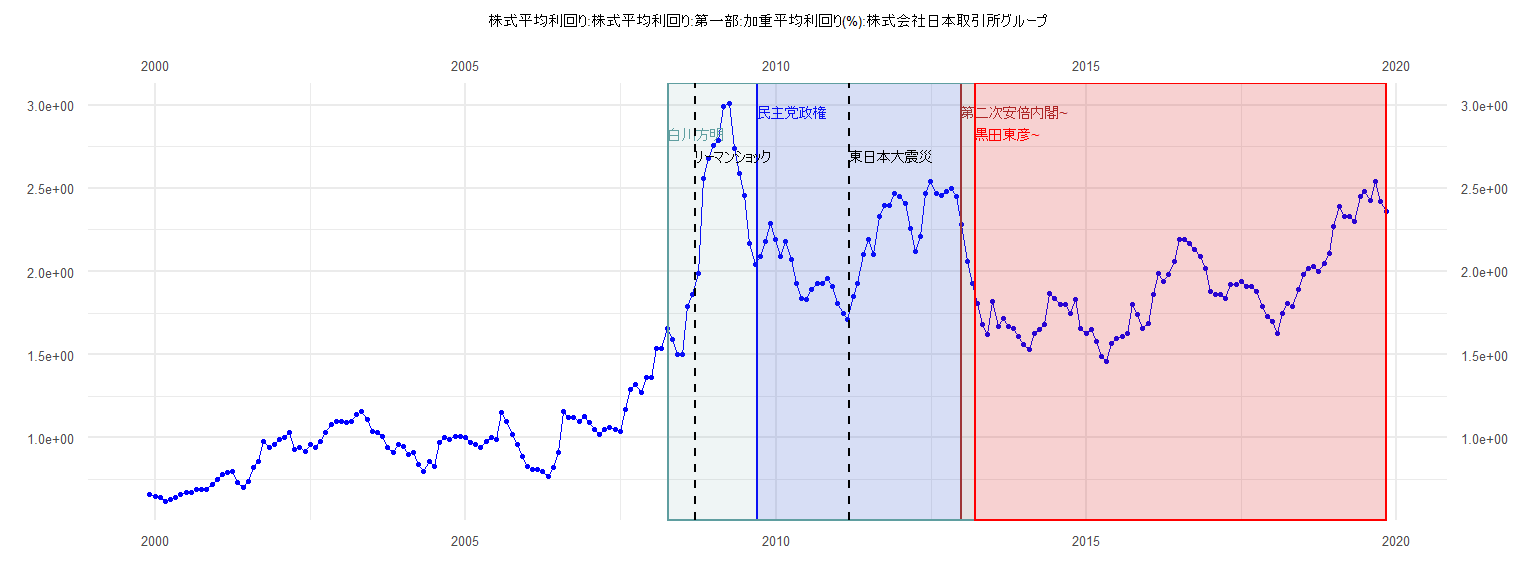

[1] "株式平均利回り:株式平均利回り:第一部:加重平均利回り(%):株式会社日本取引所グループ"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.66 0.65

2000 0.64 0.62 0.63 0.64 0.66 0.67 0.67 0.69 0.69 0.69 0.72 0.75

2001 0.78 0.79 0.80 0.73 0.70 0.74 0.82 0.86 0.98 0.94 0.96 0.99

2002 1.00 1.03 0.93 0.94 0.92 0.96 0.94 0.98 1.03 1.08 1.10 1.10

2003 1.09 1.10 1.14 1.16 1.11 1.04 1.03 1.01 0.94 0.91 0.96 0.95

2004 0.90 0.91 0.84 0.80 0.86 0.83 0.97 1.00 0.99 1.01 1.01 1.00

2005 0.97 0.96 0.94 0.98 1.00 0.99 1.15 1.10 1.02 0.96 0.89 0.83

2006 0.81 0.81 0.80 0.77 0.82 0.91 1.16 1.12 1.12 1.10 1.13 1.09

2007 1.05 1.02 1.05 1.06 1.05 1.04 1.17 1.29 1.32 1.27 1.36 1.36

2008 1.54 1.54 1.66 1.59 1.50 1.50 1.79 1.86 1.99 2.56 2.68 2.76

2009 2.79 2.99 3.01 2.74 2.59 2.46 2.17 2.04 2.09 2.18 2.29 2.19

2010 2.09 2.18 2.07 1.93 1.84 1.83 1.89 1.93 1.93 1.96 1.91 1.81

2011 1.75 1.71 1.85 1.93 2.10 2.19 2.10 2.33 2.40 2.40 2.47 2.45

2012 2.41 2.26 2.12 2.21 2.47 2.54 2.47 2.46 2.48 2.50 2.45 2.28

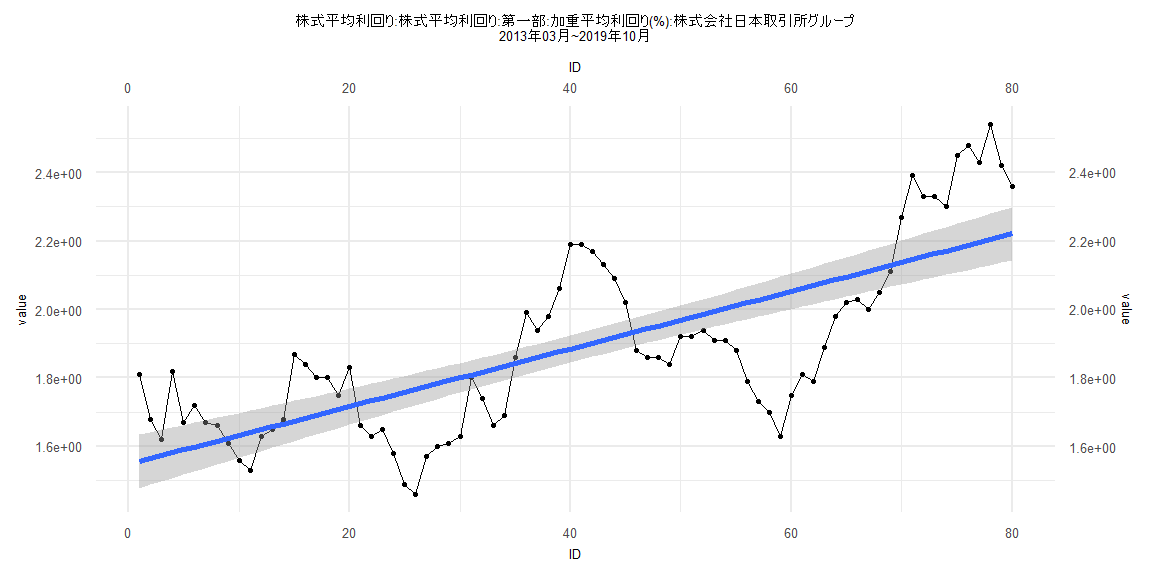

2013 2.06 1.93 1.81 1.68 1.62 1.82 1.67 1.72 1.67 1.66 1.61 1.56

2014 1.53 1.63 1.65 1.68 1.87 1.84 1.80 1.80 1.75 1.83 1.66 1.63

2015 1.65 1.58 1.49 1.46 1.57 1.60 1.61 1.63 1.80 1.74 1.66 1.69

2016 1.86 1.99 1.94 1.98 2.06 2.19 2.19 2.17 2.13 2.09 2.02 1.88

2017 1.86 1.86 1.84 1.92 1.92 1.94 1.91 1.91 1.88 1.79 1.73 1.70

2018 1.63 1.75 1.81 1.79 1.89 1.98 2.02 2.03 2.00 2.05 2.11 2.27

2019 2.39 2.33 2.33 2.30 2.45 2.48 2.43 2.54 2.42 2.36

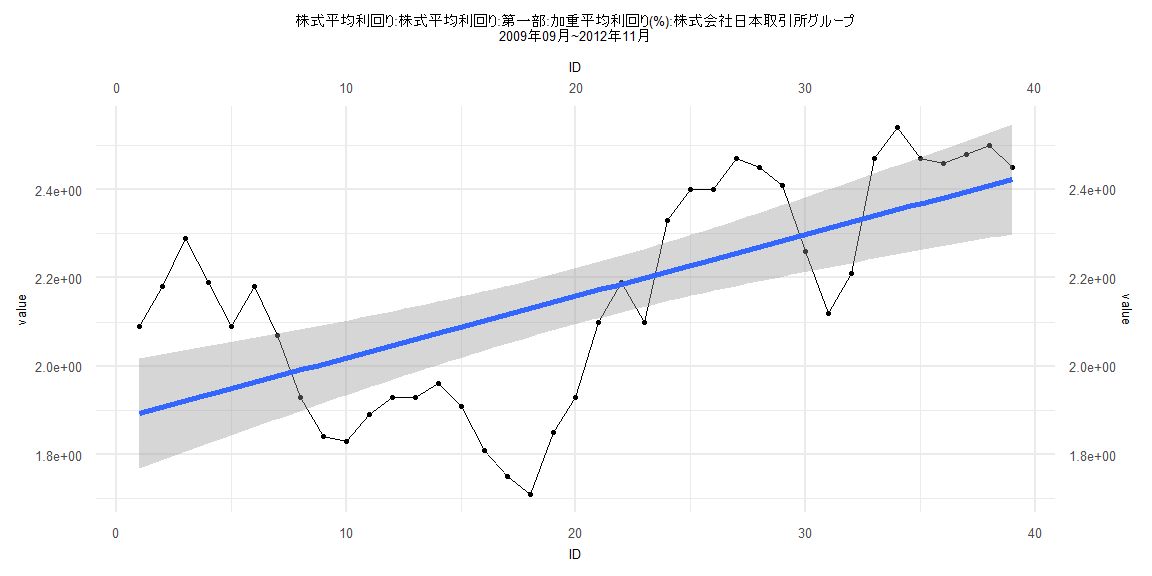

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.42032 -0.13666 0.02687 0.14954 0.36883

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.879339 0.063540 29.577 < 0.0000000000000002 ***

ID 0.013943 0.002769 5.036 0.0000126 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1946 on 37 degrees of freedom

Multiple R-squared: 0.4067, Adjusted R-squared: 0.3906

F-statistic: 25.36 on 1 and 37 DF, p-value: 0.00001262

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.28205, p-value = 0.08974

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.26846, p-value = 0.000000000000008286

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.7625, df = 1, p-value = 0.02909

Box-Ljung test

data: lm_residuals

X-squared = 30.524, df = 1, p-value = 0.00000003297

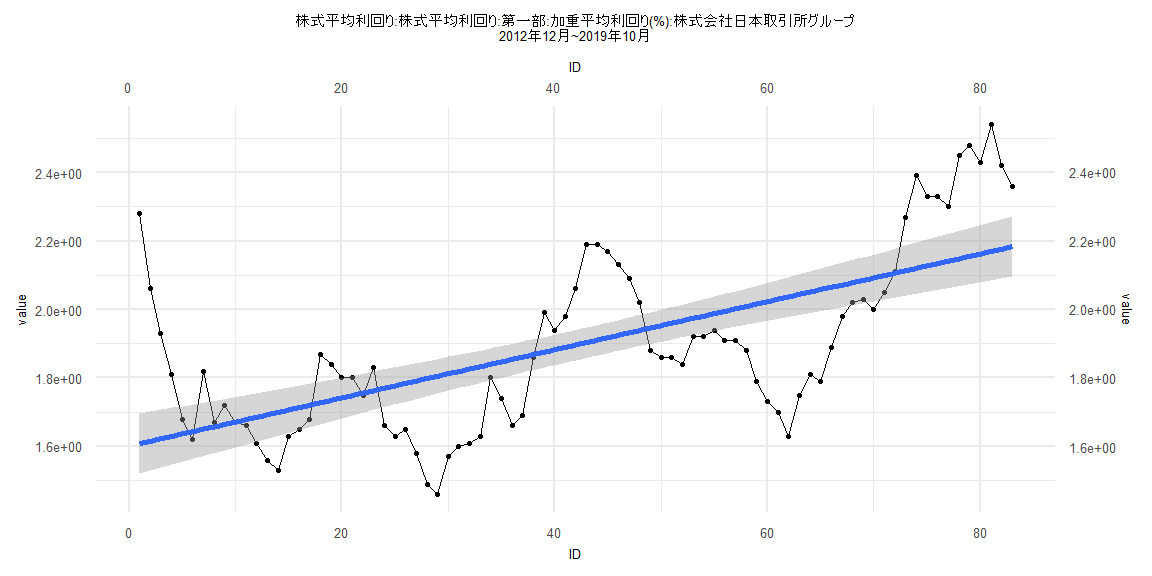

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.40633 -0.13026 -0.04037 0.15739 0.67198

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.6009991 0.0447650 35.765 < 0.0000000000000002 ***

ID 0.0070215 0.0009258 7.584 0.0000000000492 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2021 on 81 degrees of freedom

Multiple R-squared: 0.4153, Adjusted R-squared: 0.408

F-statistic: 57.52 on 1 and 81 DF, p-value: 0.00000000004924

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.072289, p-value = 0.9829

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.18343, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0087354, df = 1, p-value = 0.9255

Box-Ljung test

data: lm_residuals

X-squared = 60.034, df = 1, p-value = 0.000000000000009326

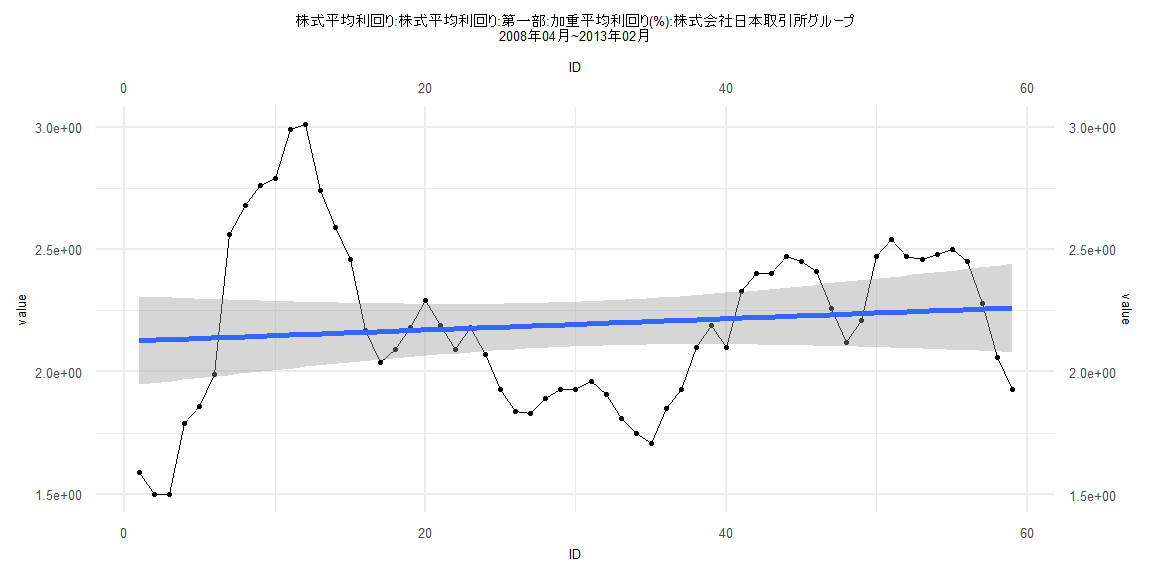

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.63197 -0.27041 -0.02499 0.22310 0.85728

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.125050 0.092123 23.068 <0.0000000000000002 ***

ID 0.002306 0.002671 0.864 0.391

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3493 on 57 degrees of freedom

Multiple R-squared: 0.01292, Adjusted R-squared: -0.004402

F-statistic: 0.7458 on 1 and 57 DF, p-value: 0.3914

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.17088, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 15.023, df = 1, p-value = 0.0001062

Box-Ljung test

data: lm_residuals

X-squared = 48.701, df = 1, p-value = 0.000000000002981

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.4143 -0.1107 -0.0160 0.1346 0.3358

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.5477690 0.0400436 38.652 < 0.0000000000000002 ***

ID 0.0084162 0.0008589 9.799 0.00000000000000308 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1774 on 78 degrees of freedom

Multiple R-squared: 0.5518, Adjusted R-squared: 0.546

F-statistic: 96.01 on 1 and 78 DF, p-value: 0.000000000000003079

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.1375, p-value = 0.4383

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.212, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.5914, df = 1, p-value = 0.005865

Box-Ljung test

data: lm_residuals

X-squared = 63.859, df = 1, p-value = 0.000000000000001332