Analysis

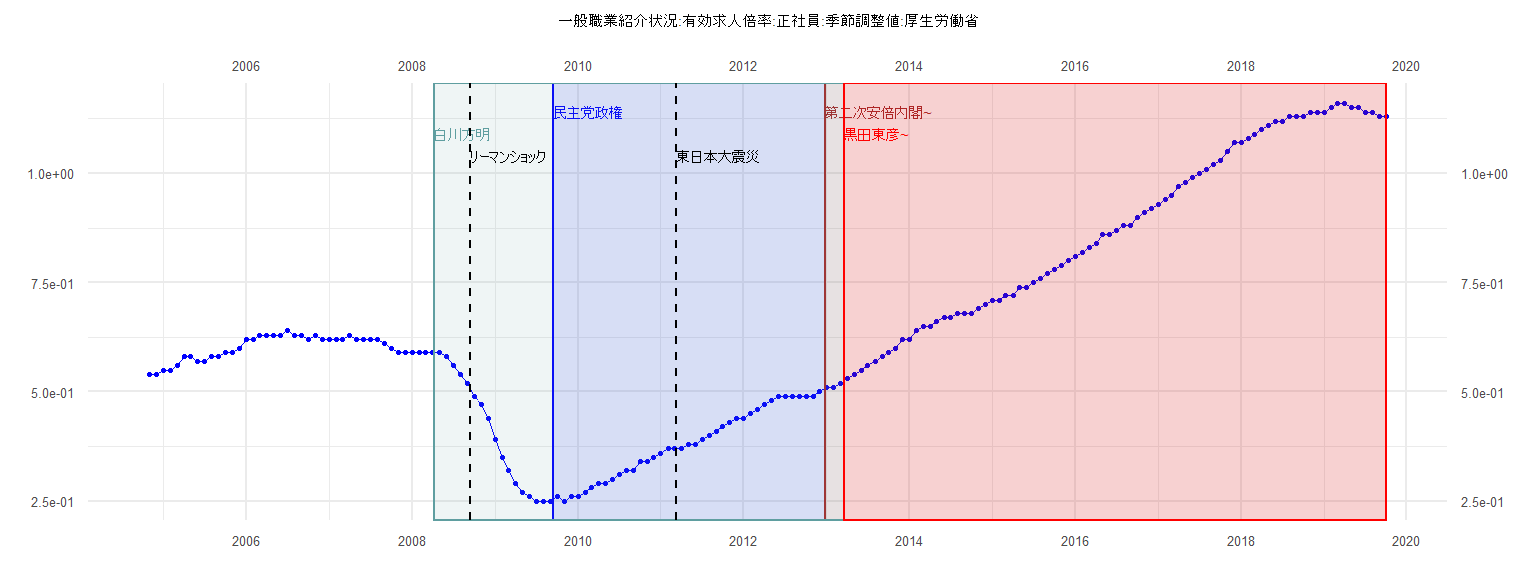

[1] "一般職業紹介状況:有効求人倍率:正社員:季節調整値:厚生労働省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2004 0.54 0.54

2005 0.55 0.55 0.56 0.58 0.58 0.57 0.57 0.58 0.58 0.59 0.59 0.60

2006 0.62 0.62 0.63 0.63 0.63 0.63 0.64 0.63 0.63 0.62 0.63 0.62

2007 0.62 0.62 0.62 0.63 0.62 0.62 0.62 0.62 0.61 0.60 0.59 0.59

2008 0.59 0.59 0.59 0.59 0.59 0.58 0.56 0.54 0.52 0.49 0.47 0.44

2009 0.39 0.35 0.32 0.29 0.27 0.26 0.25 0.25 0.25 0.26 0.25 0.26

2010 0.26 0.27 0.28 0.29 0.29 0.30 0.31 0.32 0.32 0.34 0.34 0.35

2011 0.36 0.37 0.37 0.37 0.38 0.38 0.39 0.40 0.41 0.42 0.43 0.44

2012 0.44 0.45 0.46 0.47 0.48 0.49 0.49 0.49 0.49 0.49 0.49 0.50

2013 0.51 0.51 0.52 0.53 0.54 0.55 0.56 0.57 0.58 0.59 0.60 0.62

2014 0.62 0.64 0.65 0.65 0.66 0.67 0.67 0.68 0.68 0.68 0.69 0.70

2015 0.71 0.71 0.72 0.72 0.74 0.74 0.75 0.76 0.77 0.78 0.79 0.80

2016 0.81 0.82 0.83 0.84 0.86 0.86 0.87 0.88 0.88 0.90 0.91 0.92

2017 0.93 0.94 0.95 0.97 0.98 0.99 1.00 1.01 1.02 1.03 1.05 1.07

2018 1.07 1.08 1.09 1.10 1.11 1.12 1.12 1.13 1.13 1.13 1.14 1.14

2019 1.14 1.15 1.16 1.16 1.15 1.15 1.14 1.14 1.13 1.13

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.0196545 -0.0051505 0.0001066 0.0058596 0.0157908

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.240270 0.002617 91.81 <0.0000000000000002 ***

ID 0.007089 0.000114 62.17 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.008015 on 37 degrees of freedom

Multiple R-squared: 0.9905, Adjusted R-squared: 0.9903

F-statistic: 3865 on 1 and 37 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.54989, p-value = 0.00000000809

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 8.3889, df = 1, p-value = 0.003775

Box-Ljung test

data: lm_residuals

X-squared = 16.832, df = 1, p-value = 0.00004084

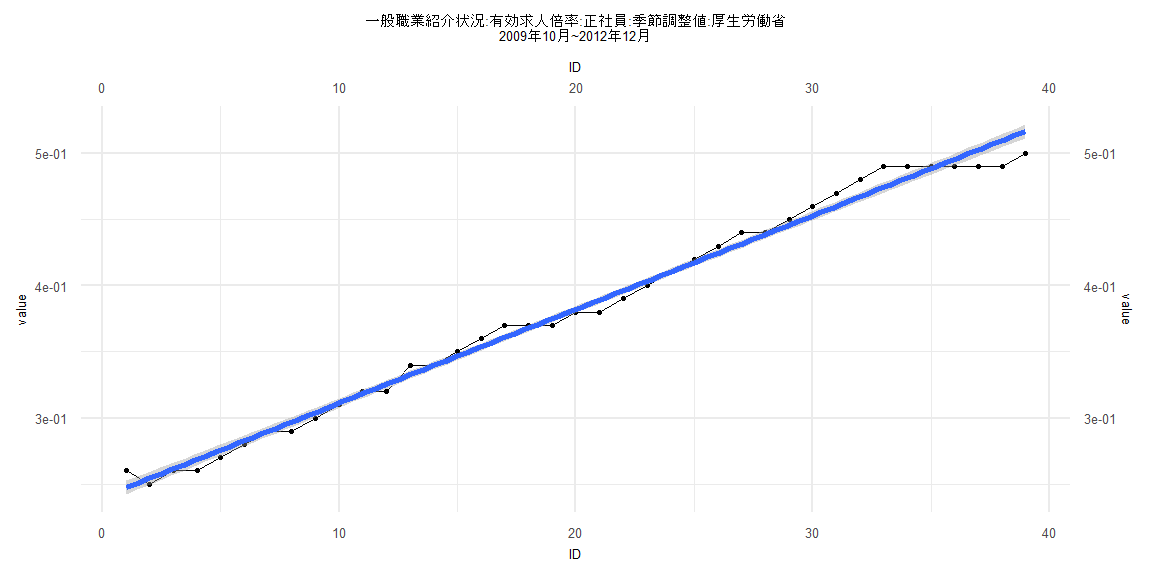

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.088290 -0.012121 0.000473 0.015751 0.044548

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.4995303 0.0054218 92.13 <0.0000000000000002 ***

ID 0.0087654 0.0001135 77.24 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02432 on 80 degrees of freedom

Multiple R-squared: 0.9868, Adjusted R-squared: 0.9866

F-statistic: 5966 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14634, p-value = 0.3453

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.079318, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 20.078, df = 1, p-value = 0.000007434

Box-Ljung test

data: lm_residuals

X-squared = 65.549, df = 1, p-value = 0.0000000000000005551

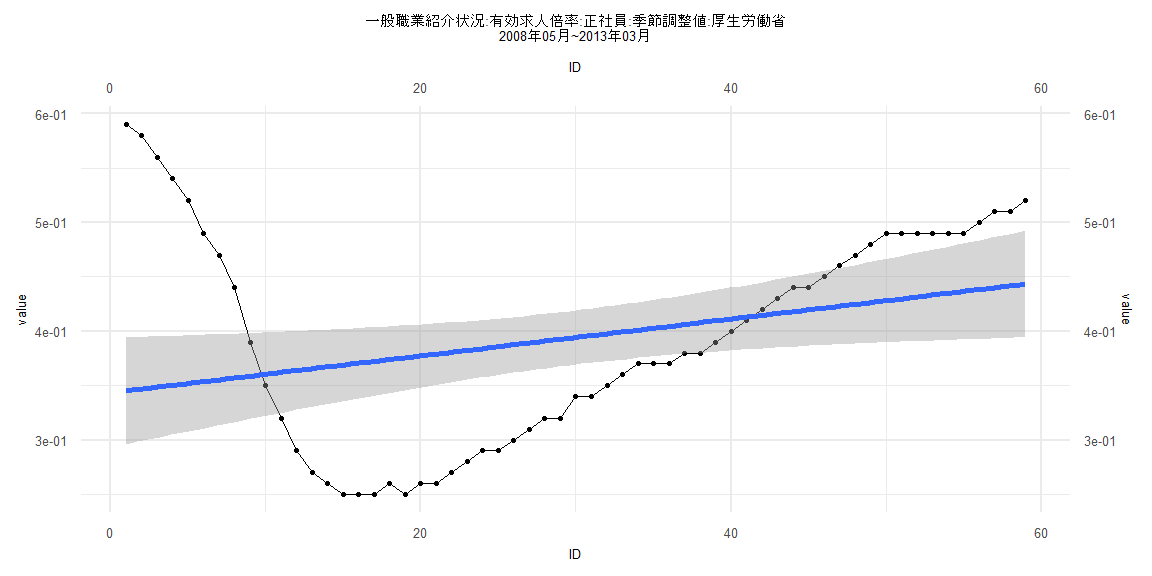

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.12562 -0.07647 -0.01116 0.05769 0.24483

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.3434775 0.0251566 13.65 <0.0000000000000002 ***

ID 0.0016920 0.0007293 2.32 0.0239 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.09539 on 57 degrees of freedom

Multiple R-squared: 0.08629, Adjusted R-squared: 0.07026

F-statistic: 5.383 on 1 and 57 DF, p-value: 0.02393

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11864, p-value = 0.8052

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.026034, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 23.441, df = 1, p-value = 0.000001288

Box-Ljung test

data: lm_residuals

X-squared = 52.924, df = 1, p-value = 0.0000000000003467

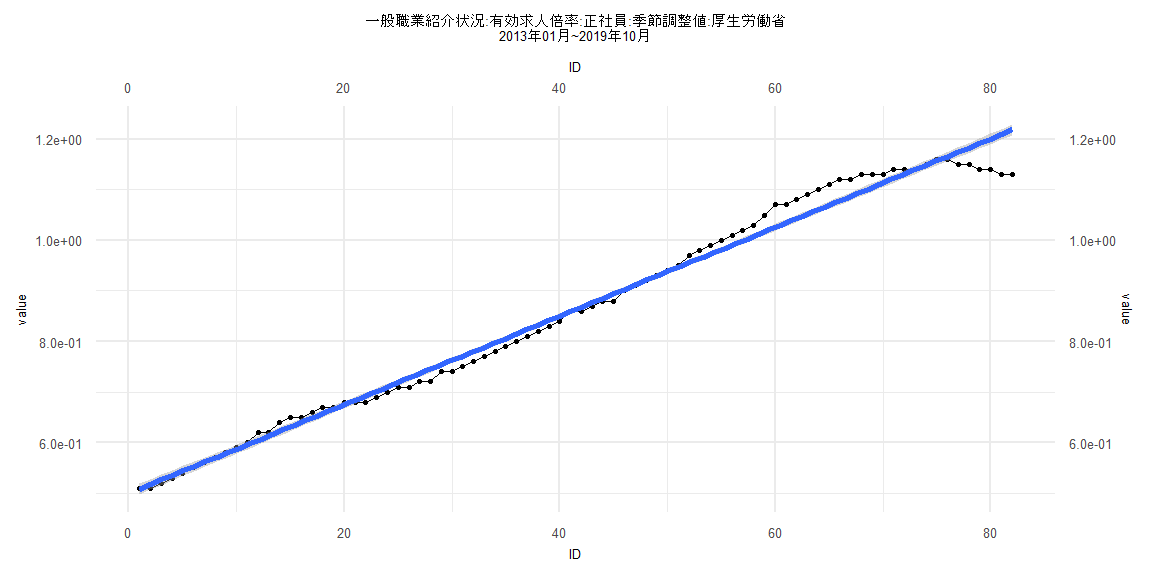

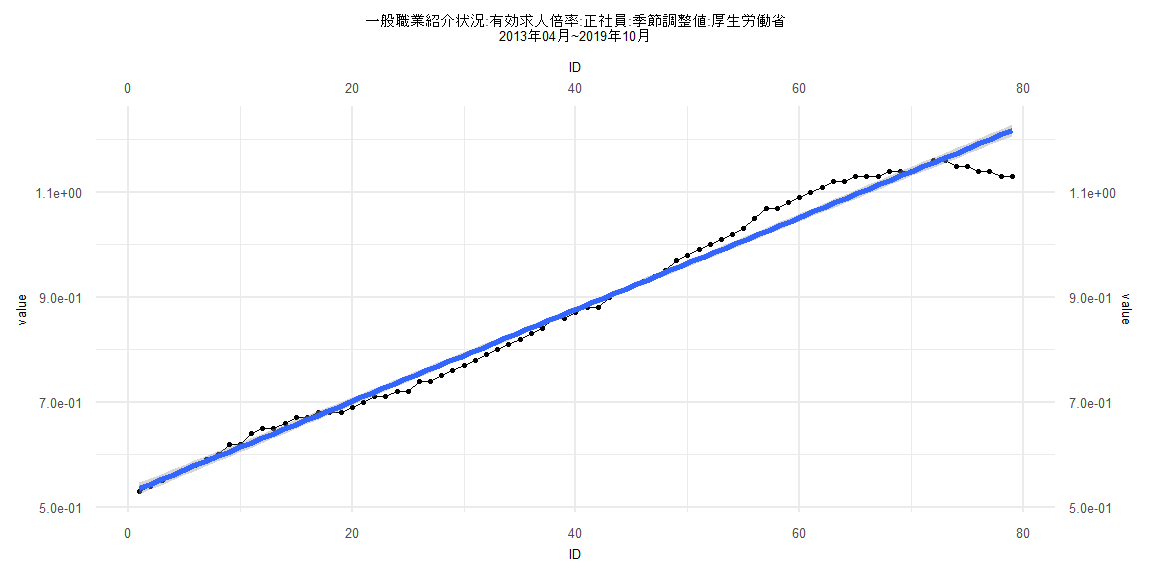

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.088003 -0.012775 0.000786 0.016462 0.044593

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.5264070 0.0056267 93.55 <0.0000000000000002 ***

ID 0.0087544 0.0001222 71.64 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02477 on 77 degrees of freedom

Multiple R-squared: 0.9852, Adjusted R-squared: 0.985

F-statistic: 5132 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16456, p-value = 0.2361

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.077745, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 19.429, df = 1, p-value = 0.00001044

Box-Ljung test

data: lm_residuals

X-squared = 63.368, df = 1, p-value = 0.000000000000001665