Analysis

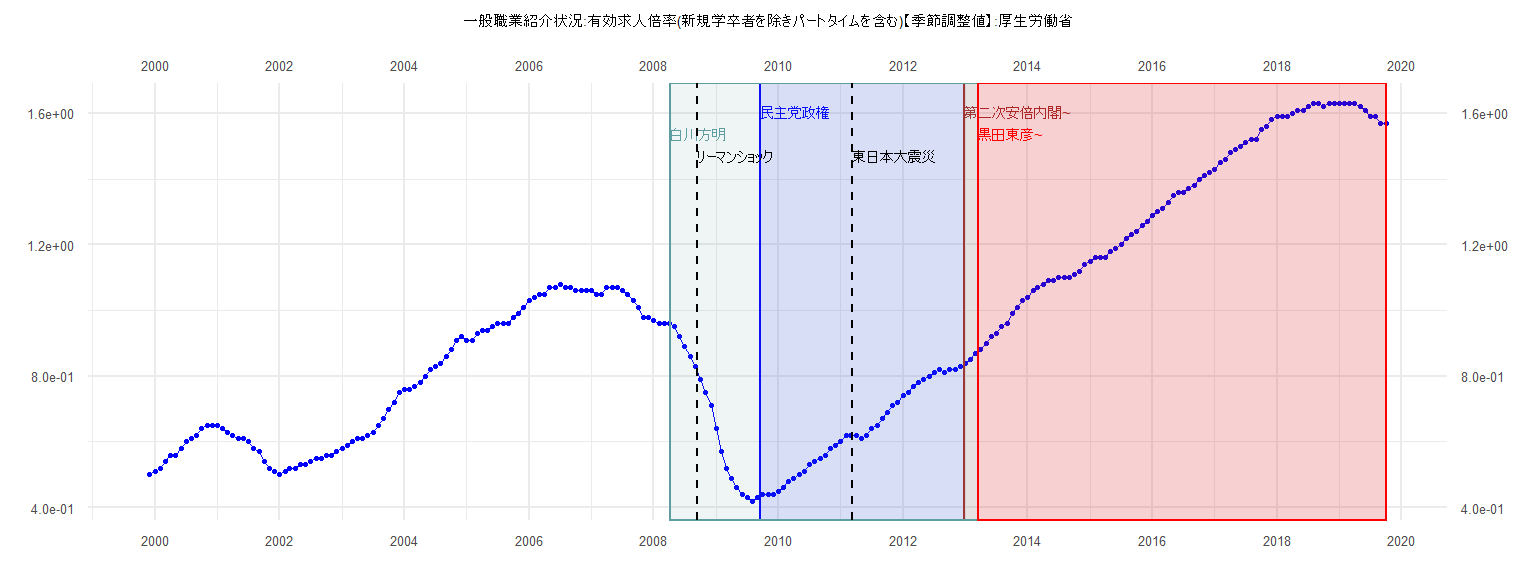

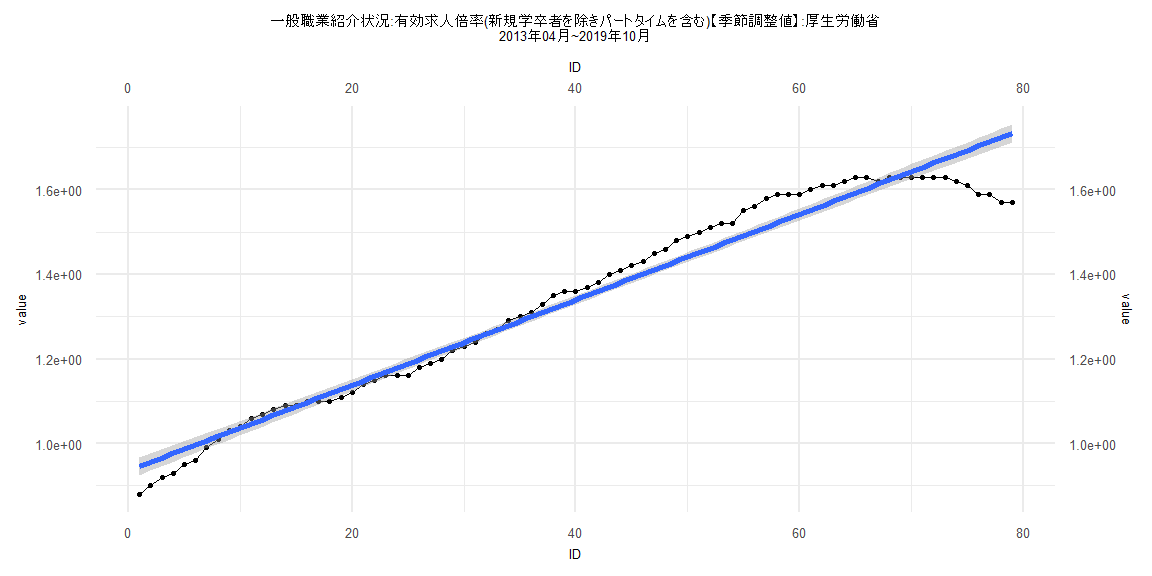

[1] "一般職業紹介状況:有効求人倍率(新規学卒者を除きパートタイムを含む)【季節調整値】:厚生労働省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.50

2000 0.51 0.52 0.54 0.56 0.56 0.58 0.60 0.61 0.62 0.64 0.65 0.65

2001 0.65 0.64 0.63 0.62 0.61 0.61 0.60 0.58 0.57 0.54 0.52 0.51

2002 0.50 0.51 0.52 0.52 0.53 0.53 0.54 0.55 0.55 0.56 0.56 0.57

2003 0.58 0.59 0.60 0.61 0.61 0.62 0.63 0.65 0.67 0.70 0.72 0.75

2004 0.76 0.76 0.77 0.78 0.80 0.82 0.83 0.84 0.86 0.88 0.91 0.92

2005 0.91 0.91 0.93 0.94 0.94 0.95 0.96 0.96 0.96 0.98 0.99 1.01

2006 1.03 1.04 1.05 1.05 1.07 1.07 1.08 1.07 1.07 1.06 1.06 1.06

2007 1.06 1.05 1.05 1.07 1.07 1.07 1.06 1.05 1.03 1.01 0.98 0.98

2008 0.97 0.96 0.96 0.96 0.95 0.92 0.89 0.86 0.83 0.79 0.75 0.71

2009 0.64 0.57 0.52 0.49 0.46 0.44 0.43 0.42 0.43 0.44 0.44 0.44

2010 0.45 0.46 0.48 0.49 0.50 0.51 0.53 0.54 0.55 0.56 0.58 0.59

2011 0.60 0.62 0.62 0.62 0.61 0.62 0.64 0.65 0.67 0.69 0.71 0.72

2012 0.74 0.75 0.77 0.78 0.79 0.80 0.81 0.82 0.81 0.82 0.82 0.83

2013 0.84 0.85 0.87 0.88 0.90 0.92 0.93 0.95 0.96 0.99 1.01 1.03

2014 1.04 1.06 1.07 1.08 1.09 1.09 1.10 1.10 1.10 1.11 1.12 1.14

2015 1.15 1.16 1.16 1.16 1.18 1.19 1.20 1.22 1.23 1.24 1.26 1.27

2016 1.29 1.30 1.31 1.33 1.35 1.36 1.36 1.37 1.38 1.40 1.41 1.42

2017 1.43 1.45 1.46 1.48 1.49 1.50 1.51 1.52 1.52 1.55 1.56 1.58

2018 1.59 1.59 1.59 1.60 1.61 1.61 1.62 1.63 1.63 1.62 1.63 1.63

2019 1.63 1.63 1.63 1.63 1.62 1.61 1.59 1.59 1.57 1.57

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.028945 -0.007692 0.002332 0.010428 0.019777

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.412632 0.004406 93.66 <0.0000000000000002 ***

ID 0.011253 0.000192 58.62 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.01349 on 37 degrees of freedom

Multiple R-squared: 0.9893, Adjusted R-squared: 0.9891

F-statistic: 3436 on 1 and 37 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.076923, p-value = 0.9999

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.34659, p-value = 0.00000000000133

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.6803, df = 1, p-value = 0.01716

Box-Ljung test

data: lm_residuals

X-squared = 25.151, df = 1, p-value = 0.0000005301

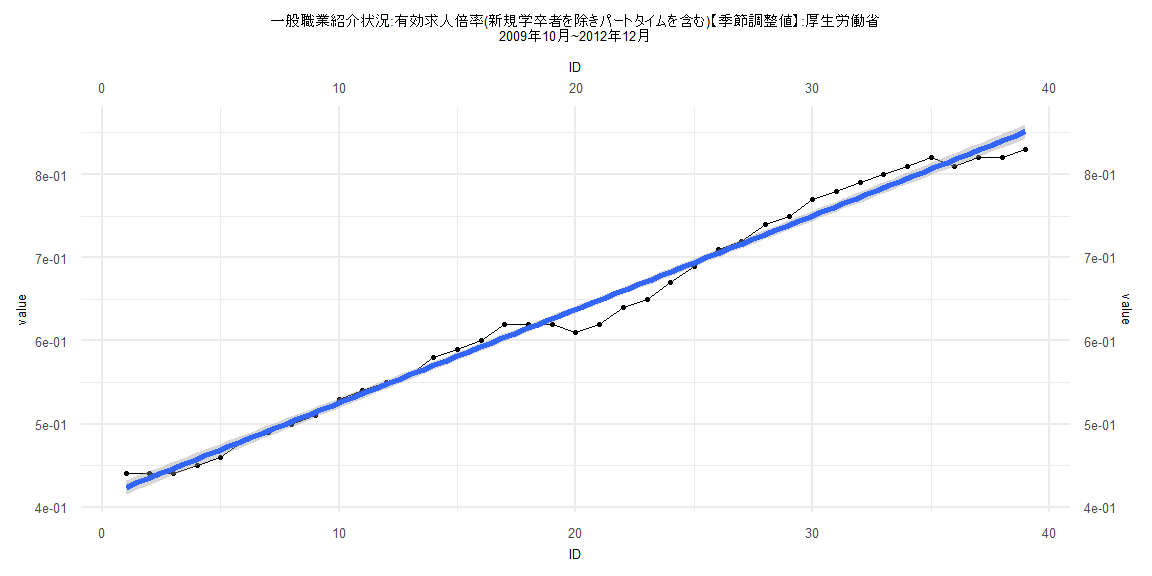

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.168310 -0.013936 0.007207 0.032628 0.067860

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.8953117 0.0106177 84.32 <0.0000000000000002 ***

ID 0.0102805 0.0002222 46.26 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.04763 on 80 degrees of freedom

Multiple R-squared: 0.964, Adjusted R-squared: 0.9635

F-statistic: 2140 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12195, p-value = 0.5785

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.041048, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 14.699, df = 1, p-value = 0.0001261

Box-Ljung test

data: lm_residuals

X-squared = 67.297, df = 1, p-value = 0.000000000000000222

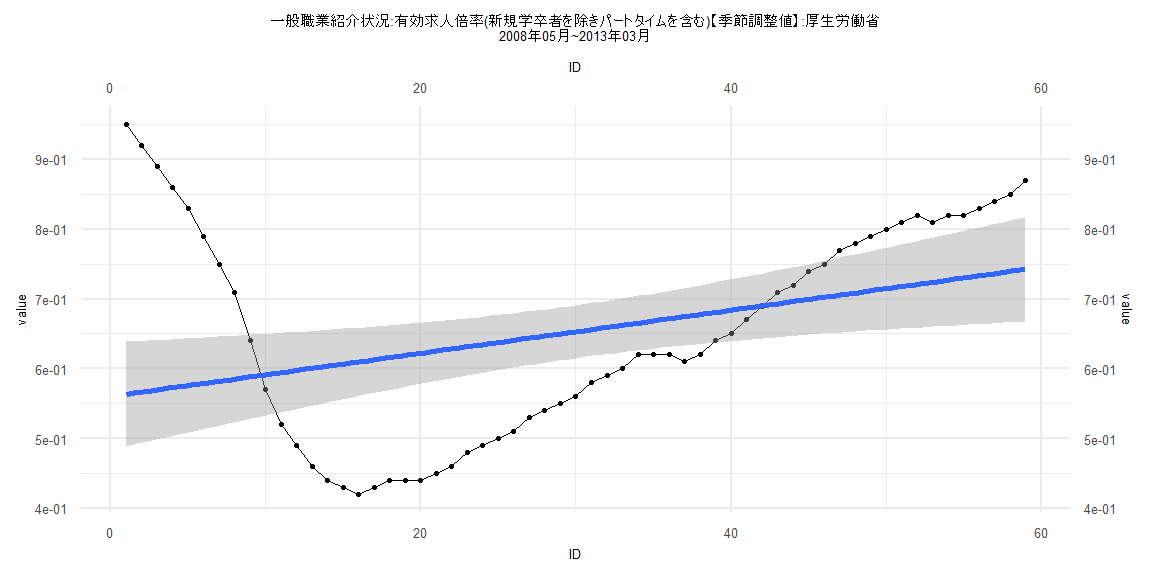

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.18986 -0.11065 -0.03390 0.09099 0.38642

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.560491 0.038398 14.597 < 0.0000000000000002 ***

ID 0.003085 0.001113 2.772 0.00752 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1456 on 57 degrees of freedom

Multiple R-squared: 0.1188, Adjusted R-squared: 0.1033

F-statistic: 7.683 on 1 and 57 DF, p-value: 0.007517

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.025858, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 22.327, df = 1, p-value = 0.0000023

Box-Ljung test

data: lm_residuals

X-squared = 52.356, df = 1, p-value = 0.0000000000004629

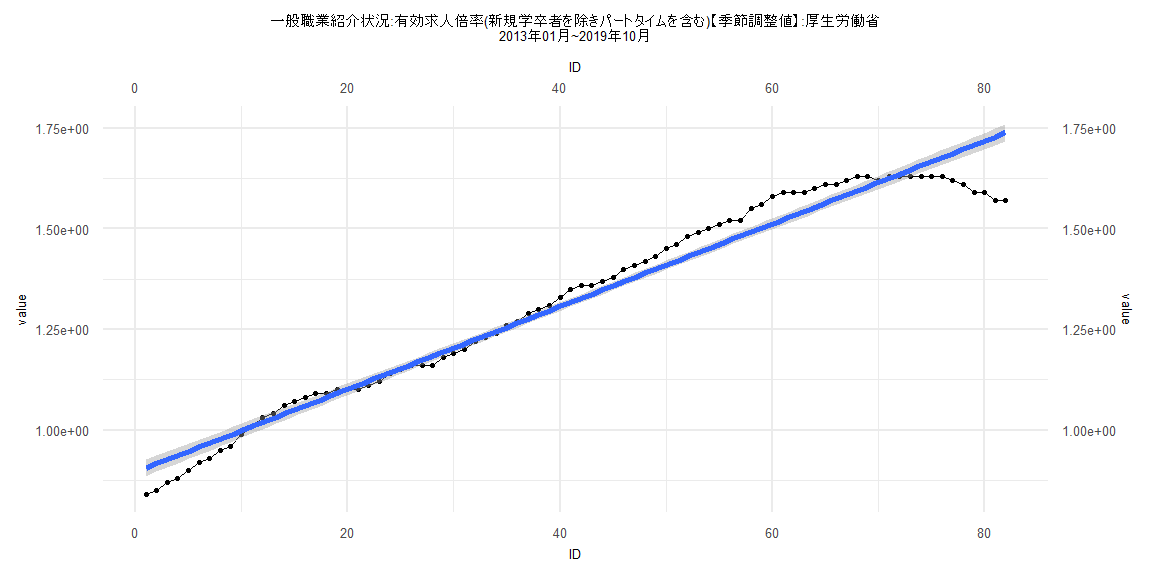

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.163373 -0.018073 0.003136 0.030393 0.068672

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.9360273 0.0106061 88.25 <0.0000000000000002 ***

ID 0.0100930 0.0002303 43.82 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.04669 on 77 degrees of freedom

Multiple R-squared: 0.9614, Adjusted R-squared: 0.9609

F-statistic: 1920 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.13924, p-value = 0.4302

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.043598, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 16.176, df = 1, p-value = 0.00005773

Box-Ljung test

data: lm_residuals

X-squared = 64.351, df = 1, p-value = 0.0000000000000009992