Analysis

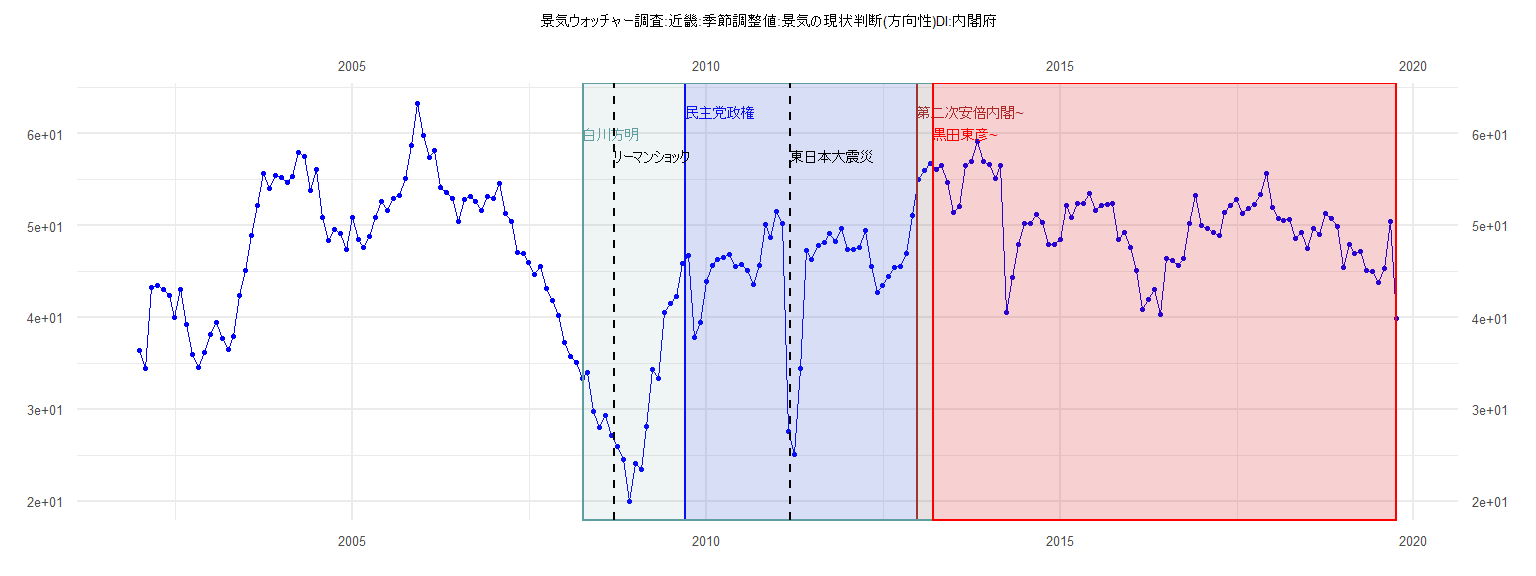

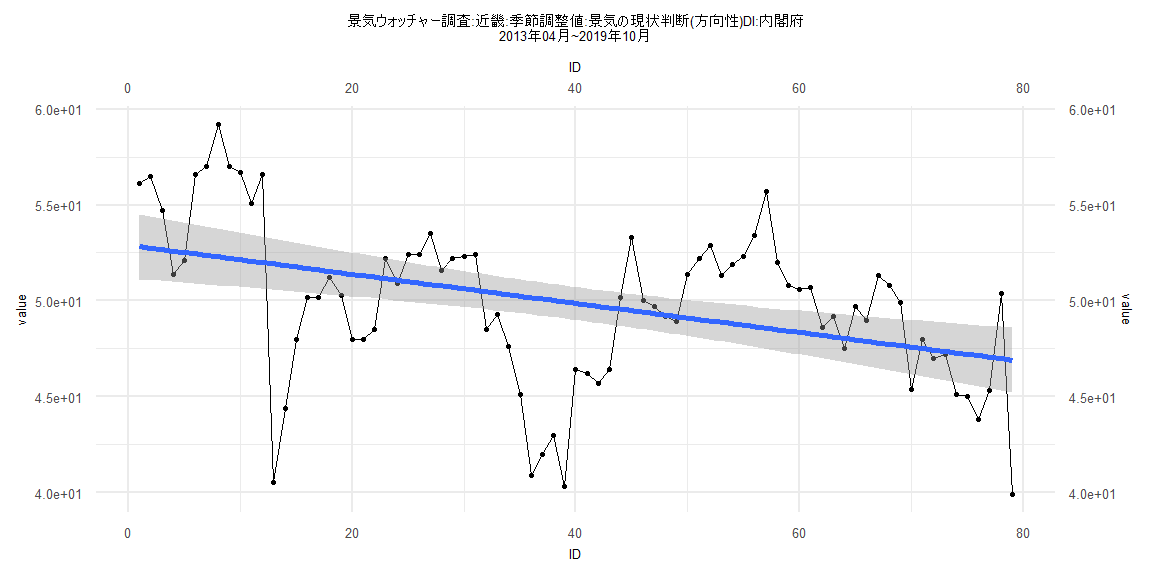

[1] "景気ウォッチャー調査:近畿:季節調整値:景気の現状判断(方向性)DI:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2002 36.4 34.4 43.3 43.5 43.0 42.4 40.0 43.0 39.2 36.0 34.5 36.2

2003 38.1 39.5 37.7 36.5 37.9 42.4 45.1 48.9 52.2 55.7 54.1 55.5

2004 55.2 54.7 55.4 58.0 57.5 53.8 56.1 50.9 48.4 49.6 49.1 47.4

2005 50.9 48.5 47.6 48.8 50.9 52.6 51.6 53.0 53.3 55.1 58.7 63.3

2006 59.8 57.4 58.2 54.2 53.6 53.0 50.5 52.9 53.2 52.6 51.7 53.2

2007 53.0 54.6 51.3 50.5 47.1 47.0 46.0 44.7 45.6 43.2 41.9 40.2

2008 37.3 35.7 35.1 33.4 34.0 29.8 28.0 29.3 27.1 25.9 24.5 20.0

2009 24.1 23.4 28.1 34.3 33.3 40.5 41.5 42.3 45.9 46.7 37.8 39.5

2010 43.9 45.7 46.3 46.5 46.9 45.5 45.8 45.1 43.6 45.7 50.1 48.7

2011 51.5 50.2 27.6 25.1 34.4 47.3 46.3 47.8 48.2 49.1 48.3 49.7

2012 47.4 47.4 47.6 49.5 45.6 42.7 43.5 44.5 45.4 45.6 47.0 51.1

2013 55.0 56.0 56.8 56.1 56.5 54.7 51.4 52.1 56.6 57.0 59.2 57.0

2014 56.7 55.1 56.6 40.5 44.4 48.0 50.2 50.2 51.2 50.3 48.0 48.0

2015 48.5 52.2 50.9 52.4 52.4 53.5 51.6 52.2 52.3 52.4 48.5 49.3

2016 47.6 45.1 40.9 42.0 43.0 40.3 46.4 46.2 45.7 46.4 50.2 53.3

2017 50.0 49.7 49.2 48.9 51.4 52.2 52.9 51.3 51.9 52.3 53.4 55.7

2018 52.0 50.8 50.6 50.7 48.6 49.2 47.5 49.7 49.0 51.3 50.8 49.9

2019 45.4 48.0 47.0 47.2 45.1 45.0 43.8 45.3 50.4 39.9

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-19.9573 -0.9318 1.5192 2.7515 6.7015

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 43.41808 1.81510 23.921 <0.0000000000000002 ***

ID 0.08628 0.07909 1.091 0.282

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.559 on 37 degrees of freedom

Multiple R-squared: 0.03116, Adjusted R-squared: 0.004972

F-statistic: 1.19 on 1 and 37 DF, p-value: 0.2824

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25641, p-value = 0.1547

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.85307, p-value = 0.00001542

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.10741, df = 1, p-value = 0.7431

Box-Ljung test

data: lm_residuals

X-squared = 13.236, df = 1, p-value = 0.0002746

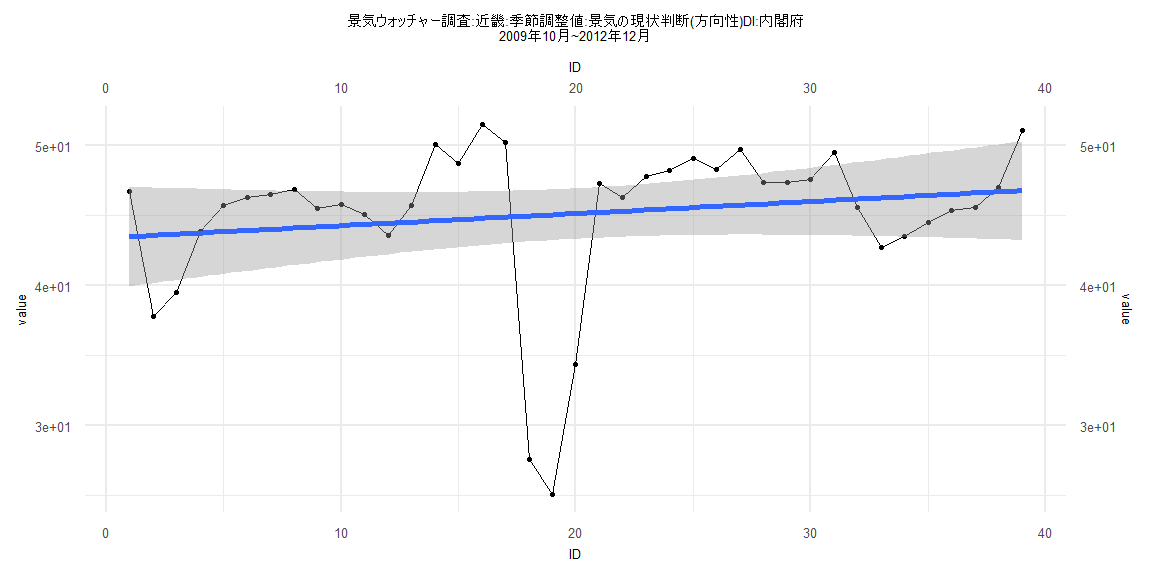

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-11.7161 -2.0314 0.6338 2.6911 7.1605

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 53.55303 0.84704 63.224 < 0.0000000000000002 ***

ID -0.08356 0.01773 -4.713 0.0000102 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.8 on 80 degrees of freedom

Multiple R-squared: 0.2173, Adjusted R-squared: 0.2075

F-statistic: 22.21 on 1 and 80 DF, p-value: 0.00001016

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15854, p-value = 0.2552

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.62473, p-value = 0.00000000000006865

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.1647, df = 1, p-value = 0.2805

Box-Ljung test

data: lm_residuals

X-squared = 37.787, df = 1, p-value = 0.0000000007892

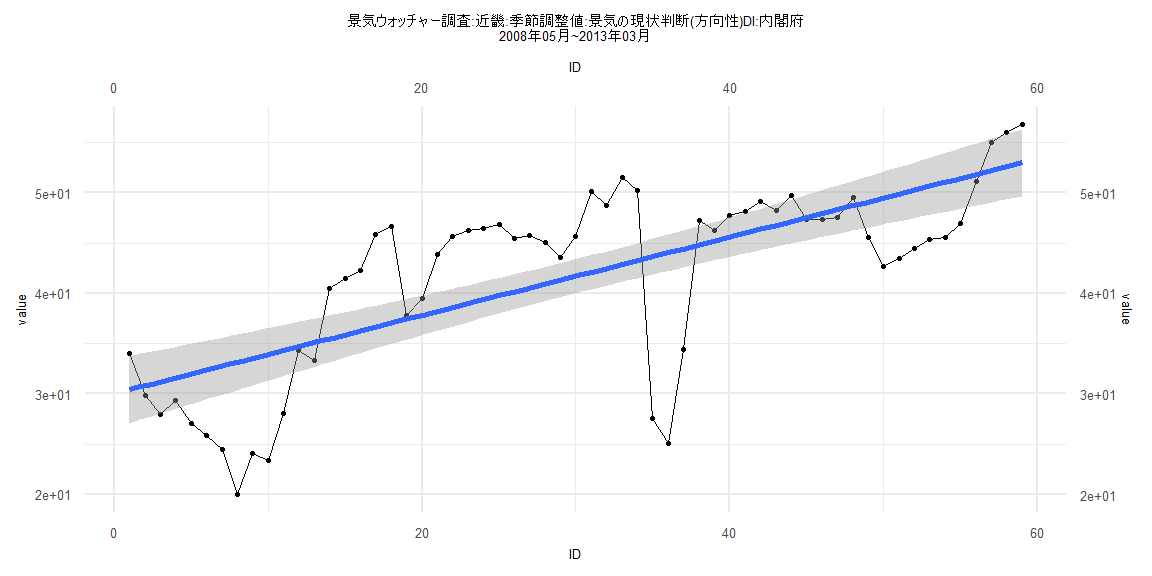

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-18.937 -4.652 1.539 5.146 9.668

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 30.02624 1.71368 17.521 < 0.0000000000000002 ***

ID 0.38918 0.04968 7.834 0.00000000013 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.498 on 57 degrees of freedom

Multiple R-squared: 0.5185, Adjusted R-squared: 0.51

F-statistic: 61.38 on 1 and 57 DF, p-value: 0.0000000001296

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.49058, p-value = 0.0000000000002056

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.88974, df = 1, p-value = 0.3455

Box-Ljung test

data: lm_residuals

X-squared = 34.813, df = 1, p-value = 0.000000003629

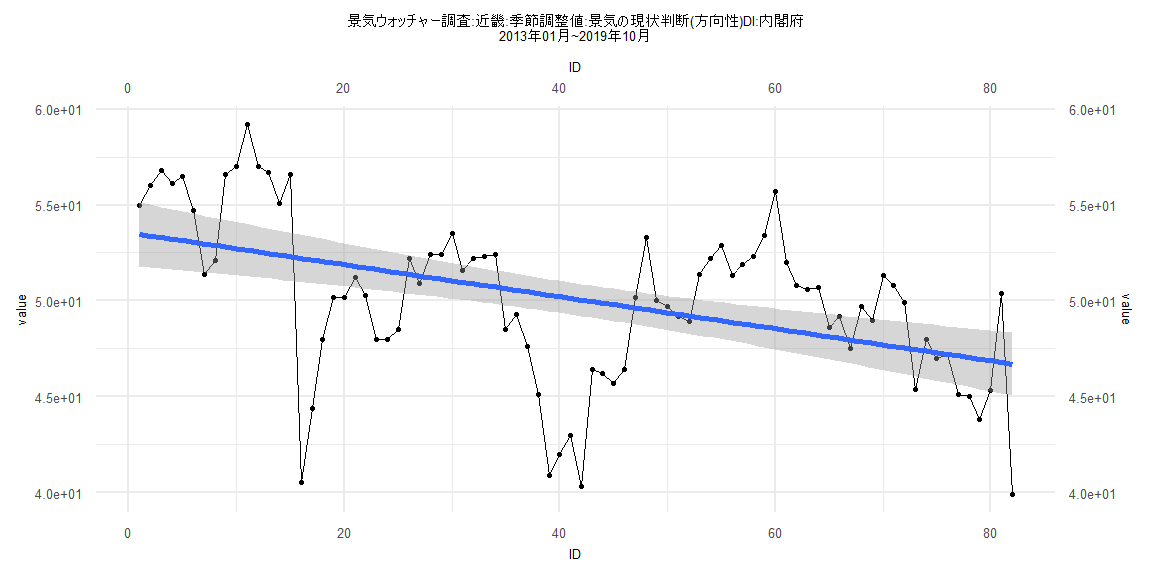

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-11.4147 -2.1820 0.5926 2.8412 7.1283

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 52.90243 0.87055 60.769 < 0.0000000000000002 ***

ID -0.07598 0.01891 -4.019 0.000135 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.832 on 77 degrees of freedom

Multiple R-squared: 0.1734, Adjusted R-squared: 0.1626

F-statistic: 16.15 on 1 and 77 DF, p-value: 0.0001353

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12658, p-value = 0.5543

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.63634, p-value = 0.0000000000003379

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.9765, df = 1, p-value = 0.1598

Box-Ljung test

data: lm_residuals

X-squared = 35.242, df = 1, p-value = 0.000000002912