Analysis

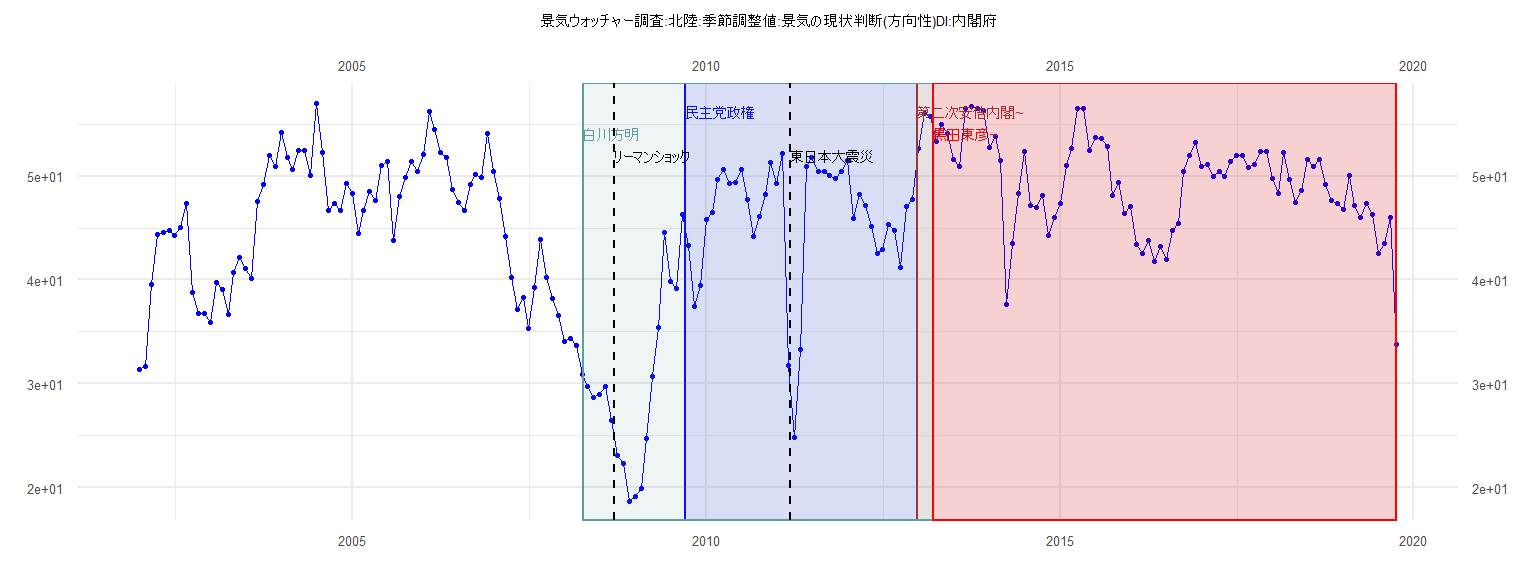

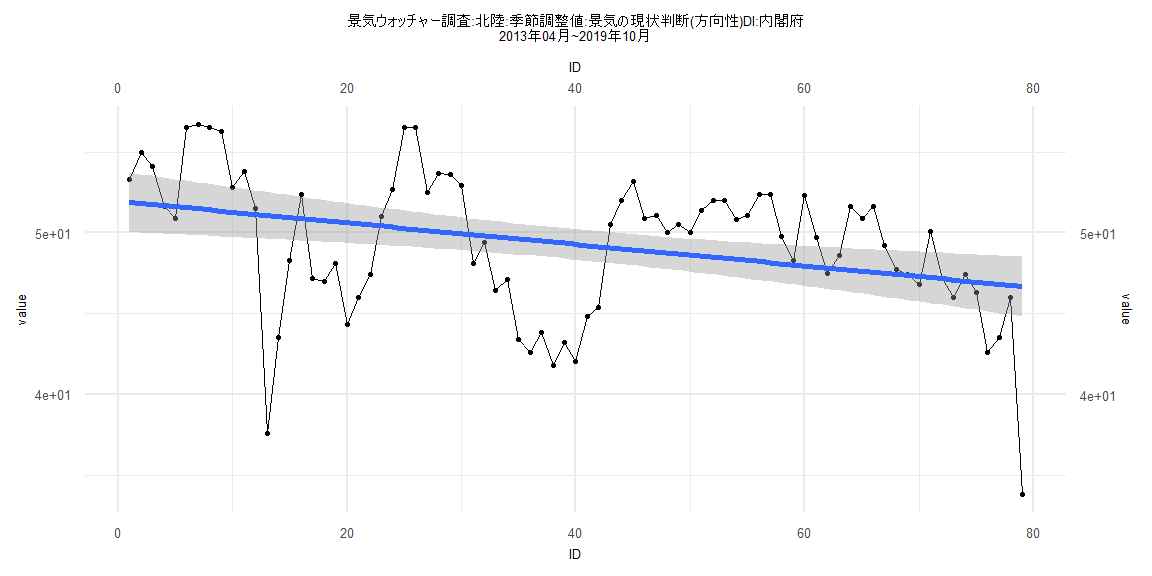

[1] "景気ウォッチャー調査:北陸:季節調整値:景気の現状判断(方向性)DI:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2002 31.4 31.7 39.6 44.4 44.6 44.8 44.3 45.1 47.4 38.8 36.8 36.8

2003 35.9 39.8 39.1 36.7 40.7 42.2 41.1 40.1 47.6 49.2 52.0 50.9

2004 54.2 51.8 50.6 52.5 52.5 50.1 57.0 52.3 46.7 47.4 46.7 49.3

2005 48.3 44.5 46.7 48.5 47.7 51.0 51.4 43.8 48.0 49.9 51.4 50.5

2006 52.1 56.2 54.5 52.3 51.8 48.7 47.5 46.7 49.2 50.2 49.9 54.1

2007 50.5 47.9 44.2 40.2 37.2 38.3 35.3 39.3 43.9 40.2 38.2 36.6

2008 34.1 34.4 33.7 30.9 29.7 28.7 29.0 29.7 26.5 23.1 22.3 18.7

2009 19.1 19.9 24.7 30.7 35.4 44.6 39.9 39.2 46.3 43.3 37.4 39.5

2010 45.8 46.5 49.7 50.6 49.3 49.4 50.6 47.8 44.2 46.1 48.2 51.3

2011 49.3 52.2 31.8 24.8 33.3 50.9 51.8 50.5 50.5 50.1 49.8 50.5

2012 51.5 45.9 48.2 47.2 45.2 42.6 42.9 45.3 44.8 41.2 47.1 47.8

2013 52.7 56.0 55.8 53.3 55.0 54.1 51.6 50.9 56.5 56.7 56.5 56.3

2014 52.8 53.8 51.5 37.6 43.5 48.3 52.4 47.2 47.0 48.1 44.3 46.0

2015 47.4 51.0 52.7 56.5 56.5 52.5 53.7 53.6 52.9 48.1 49.4 46.4

2016 47.1 43.4 42.6 43.8 41.8 43.2 42.0 44.8 45.4 50.5 52.0 53.2

2017 50.9 51.1 50.0 50.5 50.0 51.4 52.0 52.0 50.8 51.1 52.4 52.4

2018 49.8 48.3 52.3 49.7 47.5 48.6 51.6 50.9 51.6 49.2 47.7 47.4

2019 46.8 50.1 47.2 46.0 47.4 46.3 42.6 43.5 46.0 33.8

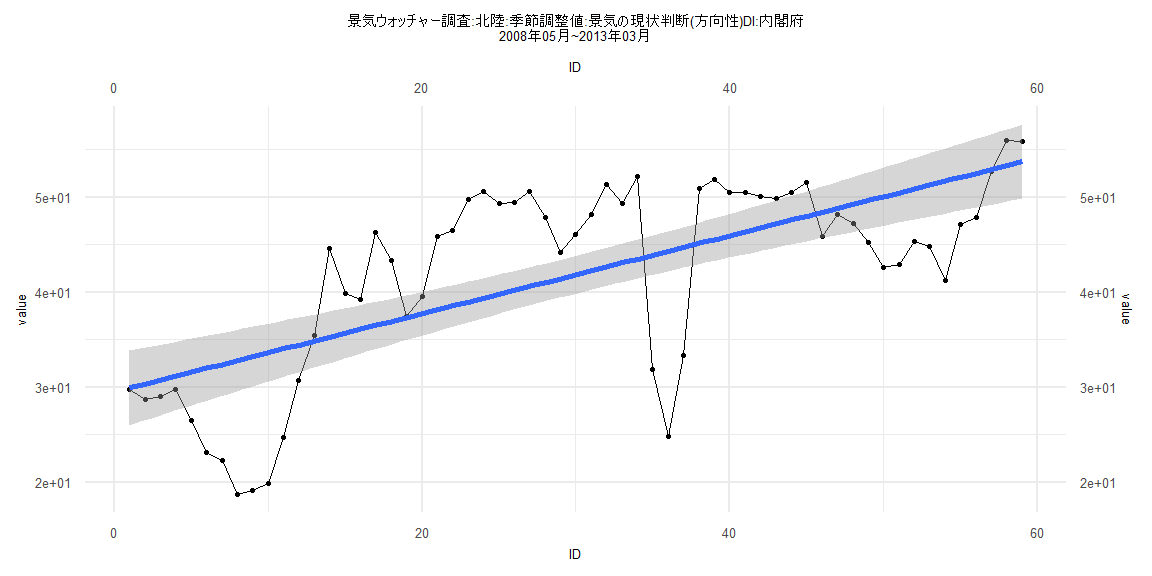

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-21.203 -1.604 1.393 4.156 6.238

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 45.61862 1.96405 23.227 <0.0000000000000002 ***

ID 0.02022 0.08558 0.236 0.815

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.015 on 37 degrees of freedom

Multiple R-squared: 0.001507, Adjusted R-squared: -0.02548

F-statistic: 0.05584 on 1 and 37 DF, p-value: 0.8145

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.8205, p-value = 0.000008207

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.22105, df = 1, p-value = 0.6382

Box-Ljung test

data: lm_residuals

X-squared = 14.498, df = 1, p-value = 0.0001403

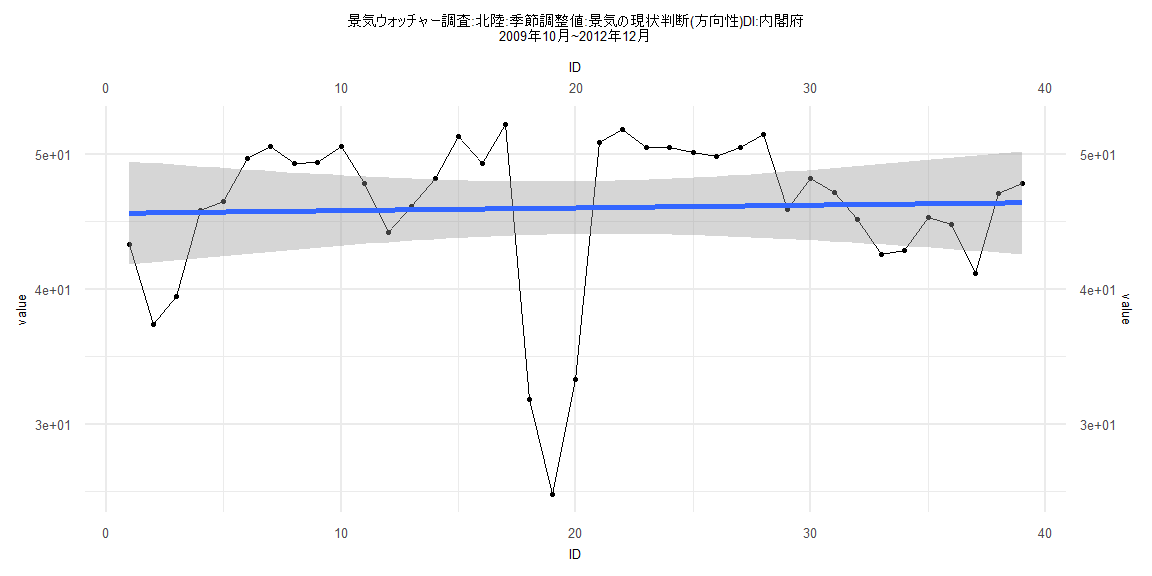

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-13.761 -2.792 1.135 2.906 6.098

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 52.54201 0.91958 57.137 < 0.0000000000000002 ***

ID -0.07380 0.01925 -3.834 0.00025 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.126 on 80 degrees of freedom

Multiple R-squared: 0.1552, Adjusted R-squared: 0.1447

F-statistic: 14.7 on 1 and 80 DF, p-value: 0.0002499

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15854, p-value = 0.2552

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.58504, p-value = 0.000000000000006782

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.3062, df = 1, p-value = 0.58

Box-Ljung test

data: lm_residuals

X-squared = 35.743, df = 1, p-value = 0.000000002251

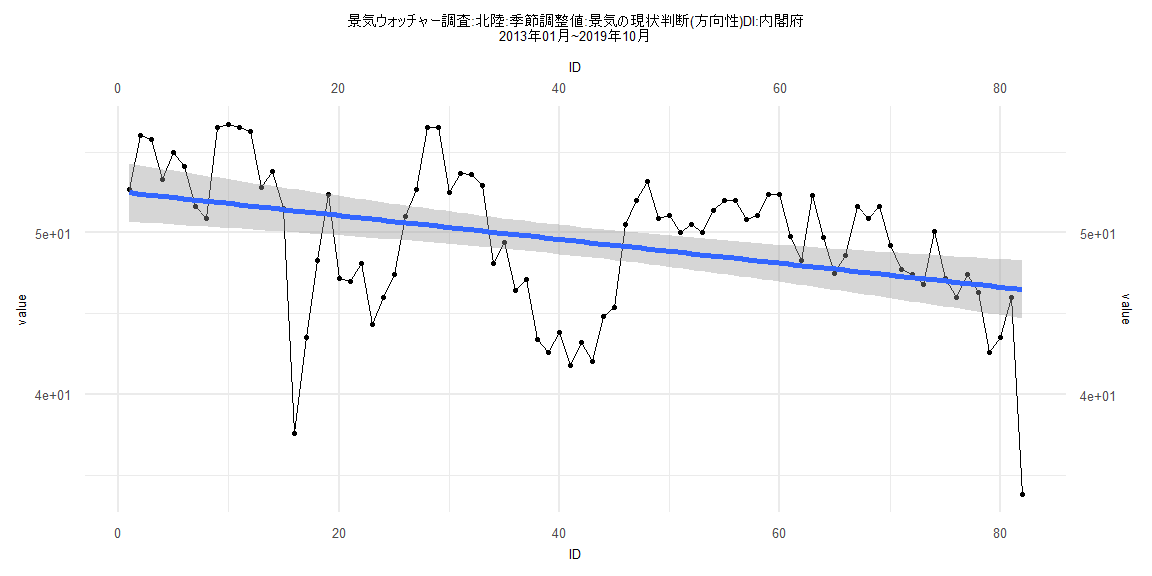

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-19.476 -5.012 1.795 6.117 11.252

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 29.49205 2.00150 14.735 < 0.0000000000000002 ***

ID 0.41066 0.05802 7.078 0.00000000236 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.589 on 57 degrees of freedom

Multiple R-squared: 0.4678, Adjusted R-squared: 0.4584

F-statistic: 50.1 on 1 and 57 DF, p-value: 0.00000000236

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11864, p-value = 0.8052

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.42869, p-value = 0.000000000000005205

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.867, df = 1, p-value = 0.1718

Box-Ljung test

data: lm_residuals

X-squared = 38.237, df = 1, p-value = 0.0000000006265

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-13.473 -2.608 1.257 2.923 6.292

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 51.93905 0.94542 54.937 < 0.0000000000000002 ***

ID -0.06658 0.02053 -3.242 0.00175 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.162 on 77 degrees of freedom

Multiple R-squared: 0.1201, Adjusted R-squared: 0.1087

F-statistic: 10.51 on 1 and 77 DF, p-value: 0.001753

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.1519, p-value = 0.3233

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.58451, p-value = 0.00000000000001885

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.56371, df = 1, p-value = 0.4528

Box-Ljung test

data: lm_residuals

X-squared = 34.108, df = 1, p-value = 0.000000005214