Analysis

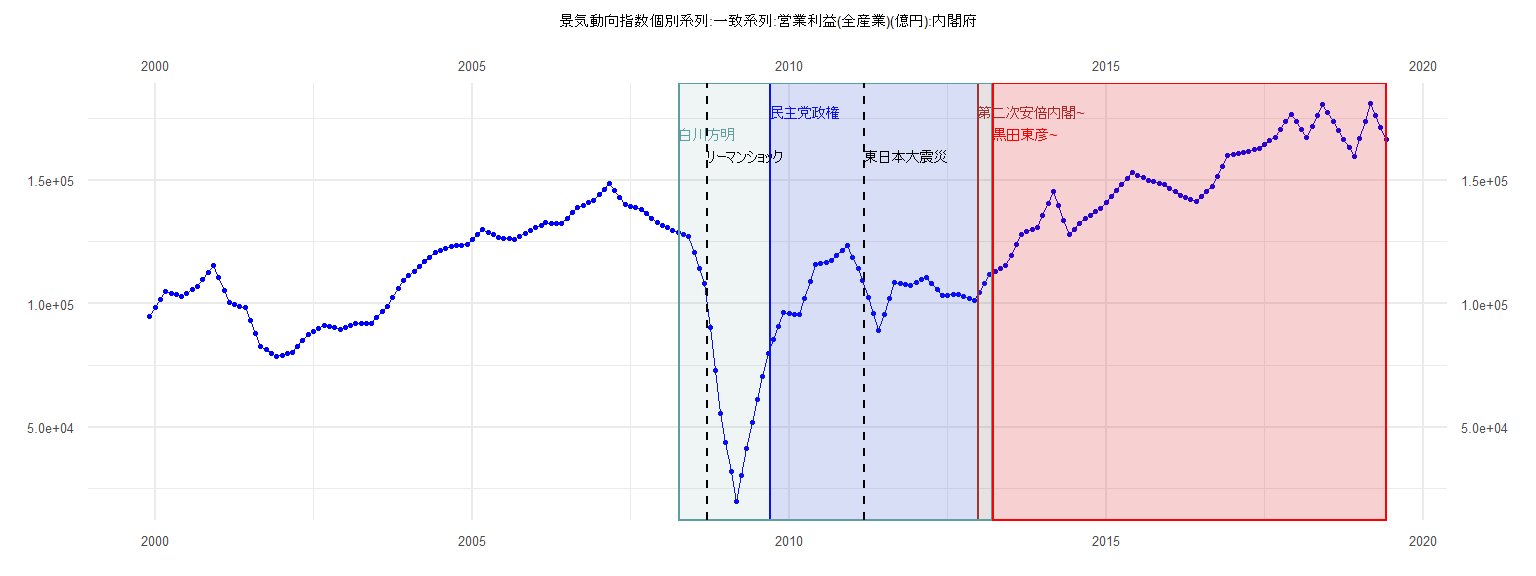

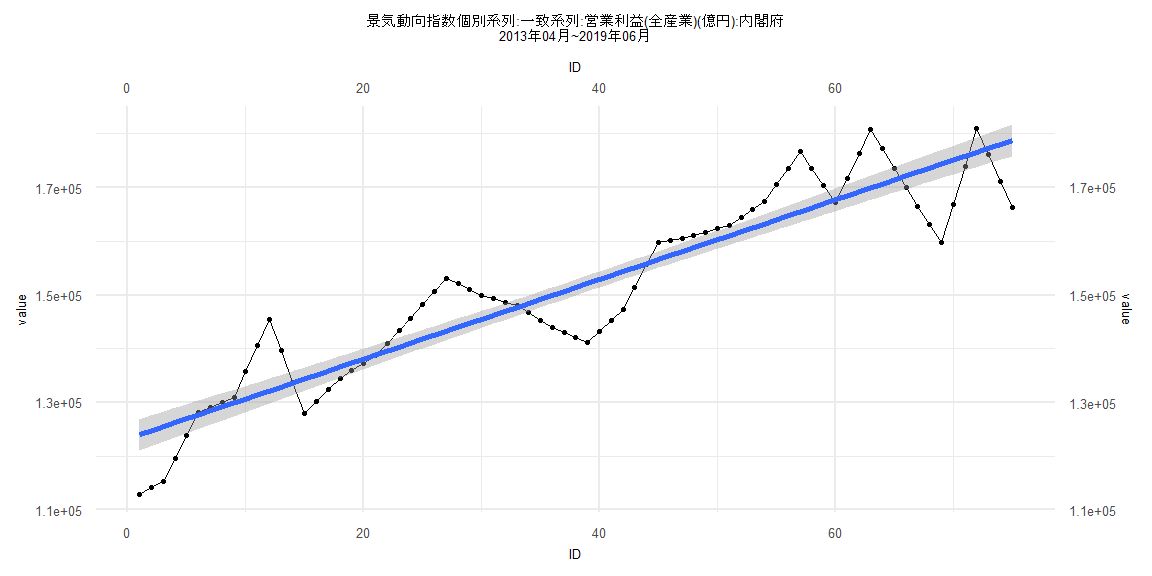

[1] "景気動向指数個別系列:一致系列:営業利益(全産業)(億円):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 94921

2000 98261 101601 104941 104275 103609 102943 104307 105672 107036 109835 112633 115432

2001 110445 105457 100470 99746 99021 98297 93112 87926 82741 81337 79933 78529

2002 79151 79772 80394 82833 85273 87712 88914 90116 91318 90743 90168 89593

2003 90333 91073 91813 91890 91968 92045 94364 96684 99003 102507 106010 109514

2004 111346 113179 115011 116921 118830 120740 121543 122345 123148 123412 123677 123941

2005 125982 128024 130065 128962 127858 126755 126494 126232 125971 127191 128411 129631

2006 130675 131720 132764 132646 132527 132409 134583 136756 138930 139903 140876 141849

2007 144056 146264 148471 145663 142856 140048 139424 138800 138176 136404 134632 132860

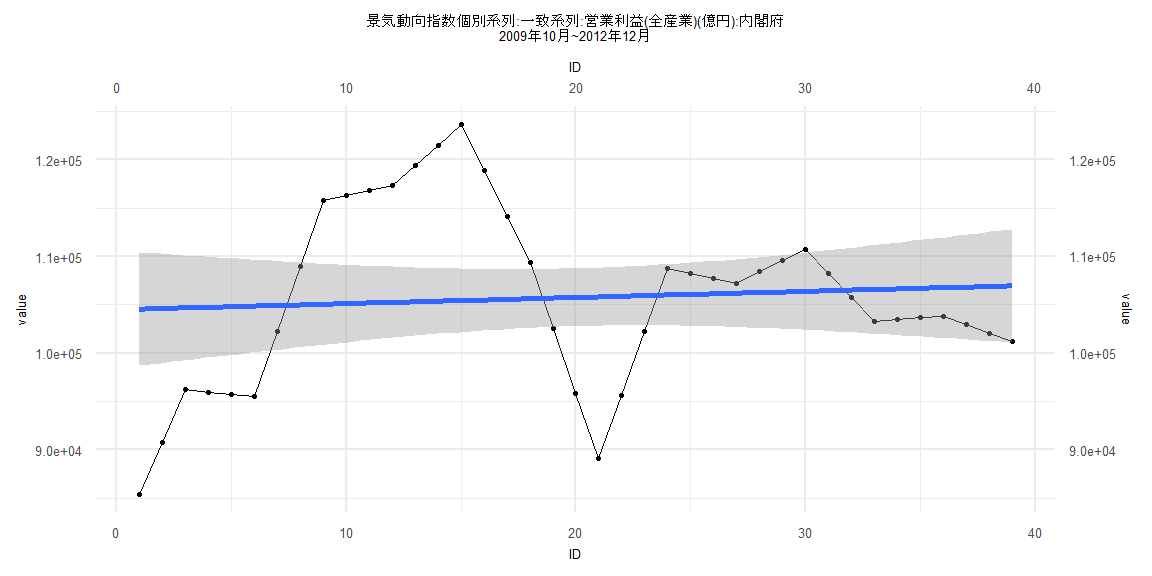

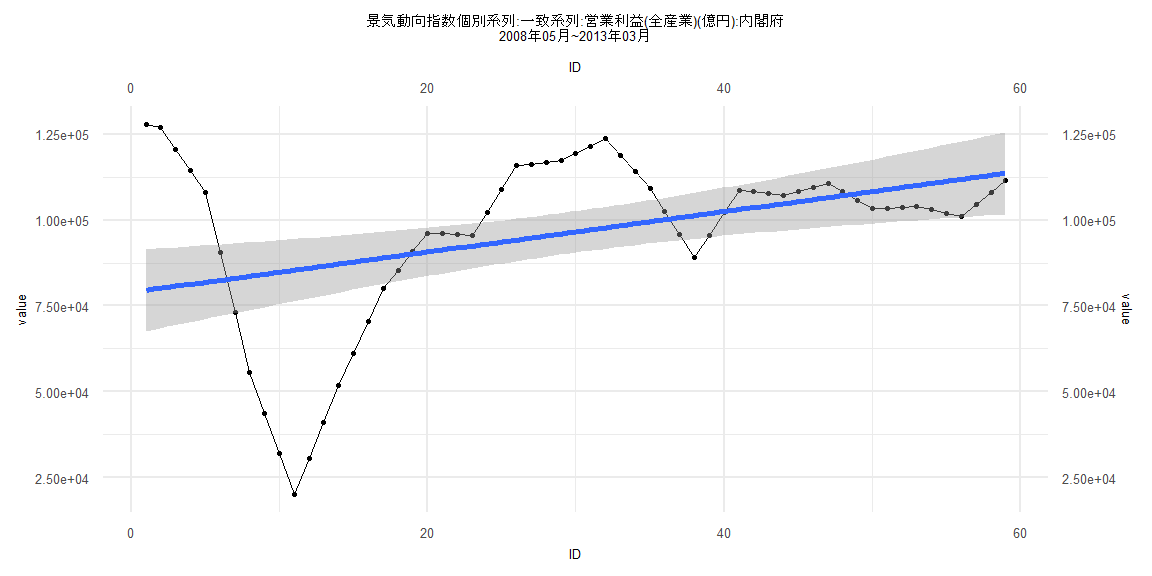

2008 131751 130641 129532 128685 127837 126990 120652 114314 107976 90498 73019 55541

2009 43727 31912 20098 30645 41193 51740 61155 70571 79986 85403 90819 96236

2010 95985 95734 95483 102250 109017 115784 116288 116793 117297 119412 121528 123643

2011 118873 114104 109334 102600 95865 89131 95667 102203 108739 108245 107750 107256

2012 108421 109587 110752 108273 105793 103314 103489 103664 103839 102958 102077 101196

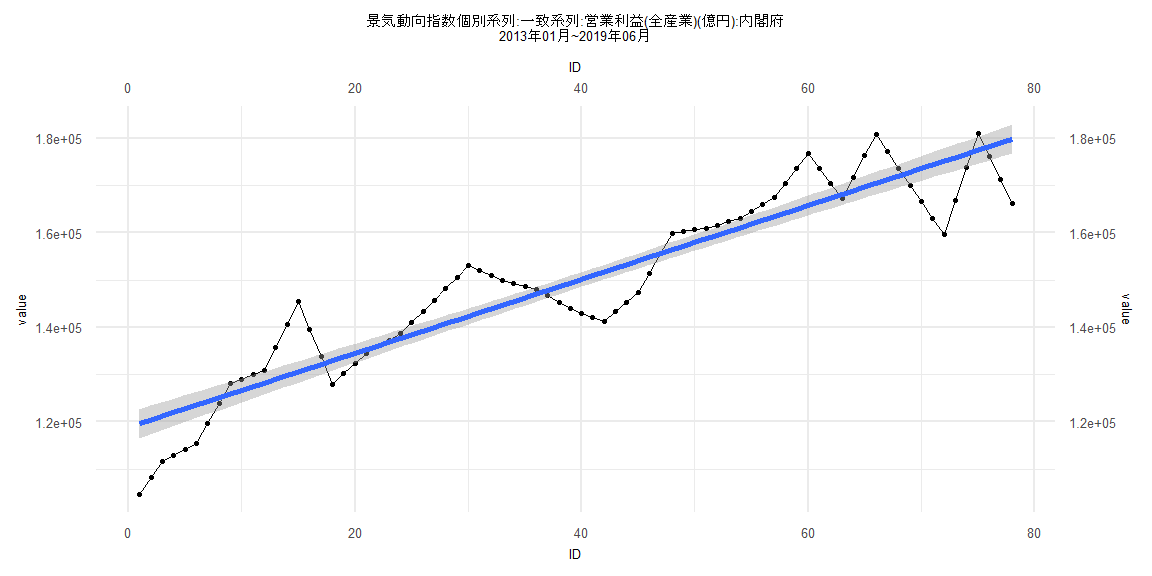

2013 104674 108152 111630 112877 114124 115371 119615 123858 128102 129065 130027 130990

2014 135788 140585 145383 139593 133803 128013 130169 132325 134481 135879 137278 138676

2015 141023 143371 145718 148185 150653 153120 152083 151045 150008 149354 148700 148046

2016 146676 145307 143937 143035 142132 141230 143262 145294 147326 151490 155655 159819

2017 160217 160614 161012 161660 162307 162955 164434 165914 167393 170509 173624 176740

2018 173567 170394 167221 171755 176288 180822 177204 173587 169969 166551 163134 159716

2019 166812 173909 181005 176095 171184 166274

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-19156.6 -5300.5 -731.9 4183.7 18195.8

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 104496.2 3009.4 34.723 <0.0000000000000002 ***

ID 63.4 131.1 0.483 0.632

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 9217 on 37 degrees of freedom

Multiple R-squared: 0.006278, Adjusted R-squared: -0.02058

F-statistic: 0.2337 on 1 and 37 DF, p-value: 0.6316

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.23077, p-value = 0.2523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.18031, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 11.6, df = 1, p-value = 0.0006594

Box-Ljung test

data: lm_residuals

X-squared = 30.128, df = 1, p-value = 0.00000004044

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-15438 -4866 1766 3955 14799

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 118854.91 1564.71 75.96 <0.0000000000000002 ***

ID 781.92 34.41 22.72 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6843 on 76 degrees of freedom

Multiple R-squared: 0.8717, Adjusted R-squared: 0.87

F-statistic: 516.2 on 1 and 76 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.21484, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.11212, df = 1, p-value = 0.7377

Box-Ljung test

data: lm_residuals

X-squared = 56.537, df = 1, p-value = 0.00000000000005518

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-65303 -7723 2472 12515 48309

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 78940.2 6113.9 12.912 <0.0000000000000002 ***

ID 587.4 177.2 3.314 0.0016 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 23180 on 57 degrees of freedom

Multiple R-squared: 0.1616, Adjusted R-squared: 0.1468

F-statistic: 10.98 on 1 and 57 DF, p-value: 0.001602

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.13559, p-value = 0.6544

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.089094, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 20.604, df = 1, p-value = 0.000005647

Box-Ljung test

data: lm_residuals

X-squared = 52.213, df = 1, p-value = 0.000000000000498

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-14657.6 -4404.7 850.7 4271.0 13243.0

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 123248.76 1499.39 82.20 <0.0000000000000002 ***

ID 740.94 34.28 21.61 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6428 on 73 degrees of freedom

Multiple R-squared: 0.8648, Adjusted R-squared: 0.863

F-statistic: 467.1 on 1 and 73 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17333, p-value = 0.2107

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.24855, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.48633, df = 1, p-value = 0.4856

Box-Ljung test

data: lm_residuals

X-squared = 53.653, df = 1, p-value = 0.0000000000002391