Analysis

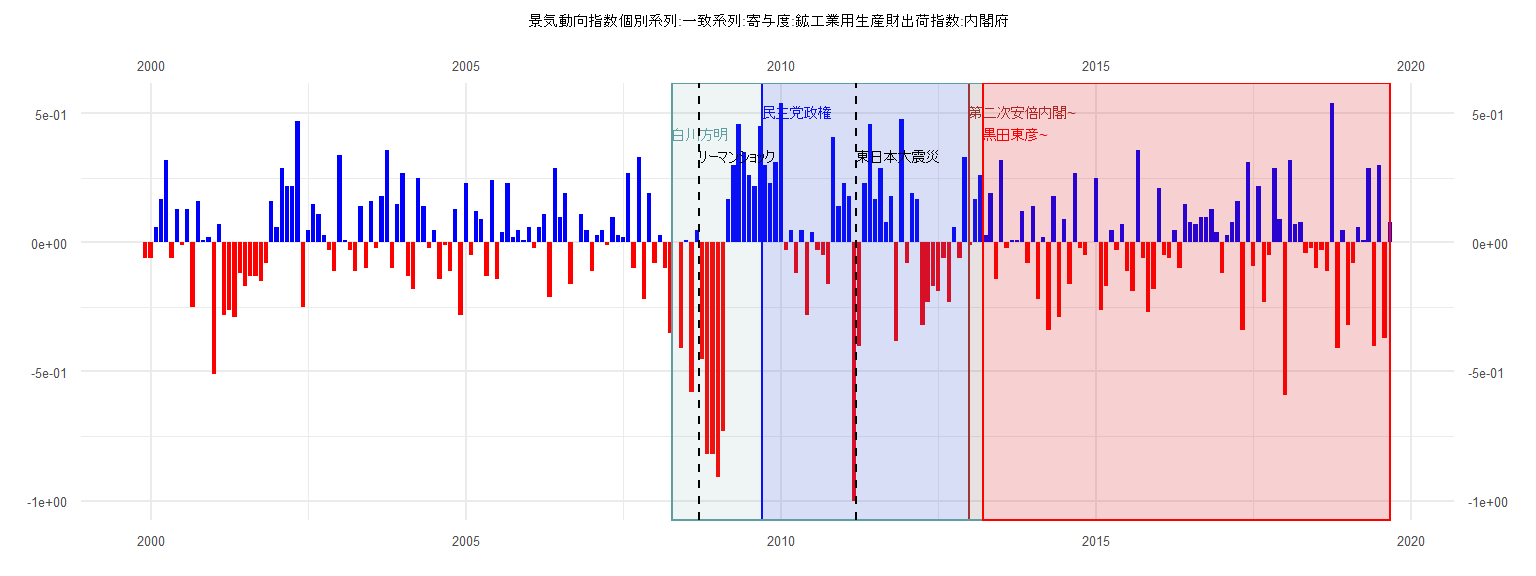

[1] "景気動向指数個別系列:一致系列:寄与度:鉱工業用生産財出荷指数:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.06

2000 -0.06 0.06 0.17 0.32 -0.06 0.13 -0.01 0.13 -0.25 0.16 0.01 0.02

2001 -0.51 0.07 -0.28 -0.26 -0.29 -0.12 -0.17 -0.13 -0.13 -0.15 -0.08 0.16

2002 0.06 0.29 0.22 0.22 0.47 -0.25 0.05 0.15 0.11 0.03 -0.03 -0.11

2003 0.34 0.01 -0.03 -0.11 0.14 -0.10 0.16 -0.02 0.18 0.36 -0.10 0.15

2004 0.27 -0.13 -0.18 0.25 0.14 -0.02 0.05 -0.14 -0.01 -0.11 0.13 -0.28

2005 0.23 -0.05 0.12 0.09 -0.13 0.24 -0.14 0.04 0.23 0.02 0.05 0.01

2006 0.06 -0.02 0.06 0.11 -0.21 0.29 0.10 0.19 -0.16 0.00 0.11 0.05

2007 -0.11 0.03 0.05 -0.01 0.10 0.03 0.02 0.27 -0.10 0.33 -0.22 0.19

2008 -0.08 0.03 -0.10 -0.35 0.00 -0.41 0.01 -0.58 0.05 -0.45 -0.82 -0.82

2009 -0.91 -0.73 0.17 0.30 0.46 0.35 0.26 0.22 0.45 0.30 0.23 0.31

2010 0.54 -0.03 0.05 -0.12 0.05 -0.28 0.04 -0.03 -0.05 -0.16 0.41 0.14

2011 0.23 0.18 -1.00 -0.40 0.23 0.46 0.17 0.29 0.08 0.18 -0.38 0.48

2012 -0.08 0.19 0.17 -0.32 -0.23 -0.17 -0.19 -0.06 -0.23 0.06 -0.06 0.33

2013 -0.01 0.17 0.26 0.03 0.19 -0.14 0.32 -0.02 0.01 0.01 0.12 -0.08

2014 0.14 -0.22 0.02 -0.34 0.18 -0.29 0.09 -0.16 0.27 -0.02 -0.05 0.00

2015 0.25 -0.26 -0.17 0.05 -0.03 0.07 -0.11 -0.19 0.36 -0.06 -0.27 -0.18

2016 0.21 -0.05 -0.06 0.05 -0.10 0.15 0.08 0.07 0.10 0.10 0.13 0.04

2017 -0.12 0.03 0.08 0.16 -0.34 0.31 -0.09 0.22 -0.23 -0.05 0.29 0.09

2018 -0.59 0.32 0.07 0.08 -0.04 -0.02 -0.10 -0.03 -0.11 0.54 -0.41 0.05

2019 -0.32 -0.08 0.06 0.01 0.29 -0.40 0.30 -0.37 0.08

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.04365 -0.14969 -0.00822 0.18021 0.47930

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.129528 0.095881 1.351 0.185

ID -0.004771 0.004178 -1.142 0.261

Residual standard error: 0.2936 on 37 degrees of freedom

Multiple R-squared: 0.03405, Adjusted R-squared: 0.007941

F-statistic: 1.304 on 1 and 37 DF, p-value: 0.2608

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.9885

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.7035, p-value = 0.1329

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0087293, df = 1, p-value = 0.9256

Box-Ljung test

data: lm_residuals

X-squared = 0.60605, df = 1, p-value = 0.4363

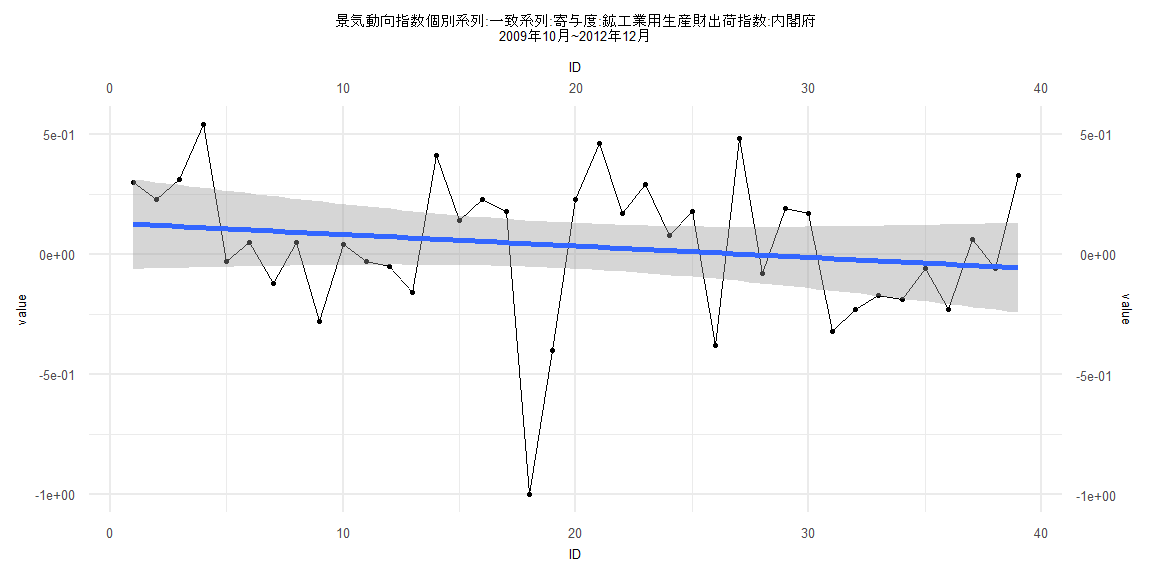

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.58115 -0.10312 -0.00116 0.10190 0.55472

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0309475 0.0455475 0.679 0.499

ID -0.0006524 0.0009650 -0.676 0.501

Residual standard error: 0.2031 on 79 degrees of freedom

Multiple R-squared: 0.005753, Adjusted R-squared: -0.006833

F-statistic: 0.4571 on 1 and 79 DF, p-value: 0.501

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16049, p-value = 0.2488

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.9014, p-value = 1

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.8274, df = 1, p-value = 0.02801

Box-Ljung test

data: lm_residuals

X-squared = 17.212, df = 1, p-value = 0.00003344

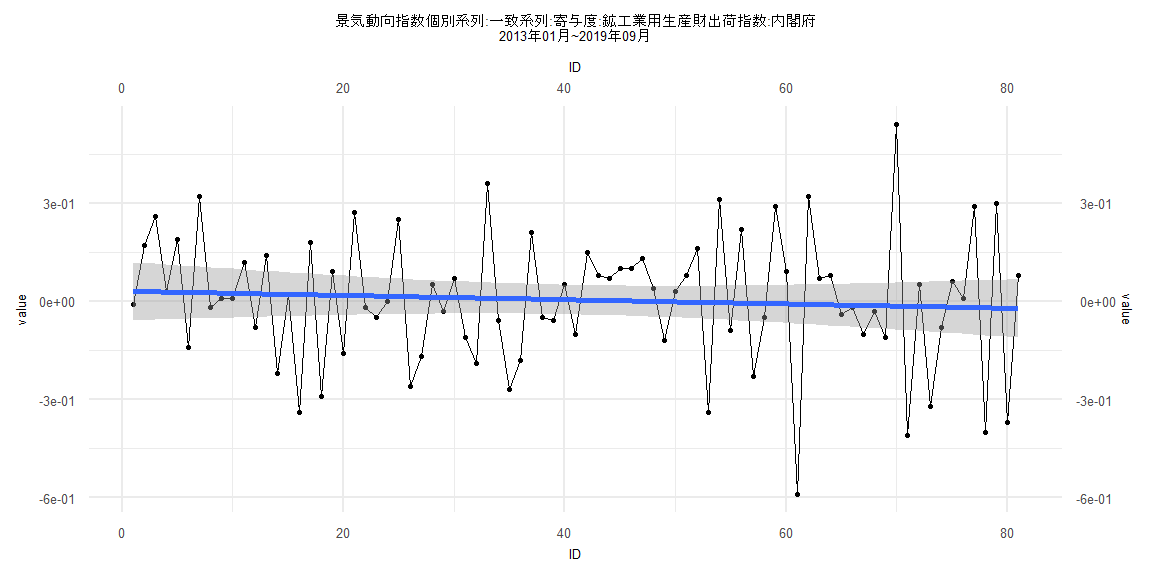

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.00840 -0.24556 0.08213 0.24768 0.58834

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.133442 0.094653 -1.410 0.164

ID 0.004053 0.002744 1.477 0.145

Residual standard error: 0.3589 on 57 degrees of freedom

Multiple R-squared: 0.03686, Adjusted R-squared: 0.01996

F-statistic: 2.181 on 1 and 57 DF, p-value: 0.1452

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.084746, p-value = 0.9854

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0971, p-value = 0.0000644

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.3148, df = 1, p-value = 0.02115

Box-Ljung test

data: lm_residuals

X-squared = 12.492, df = 1, p-value = 0.0004086

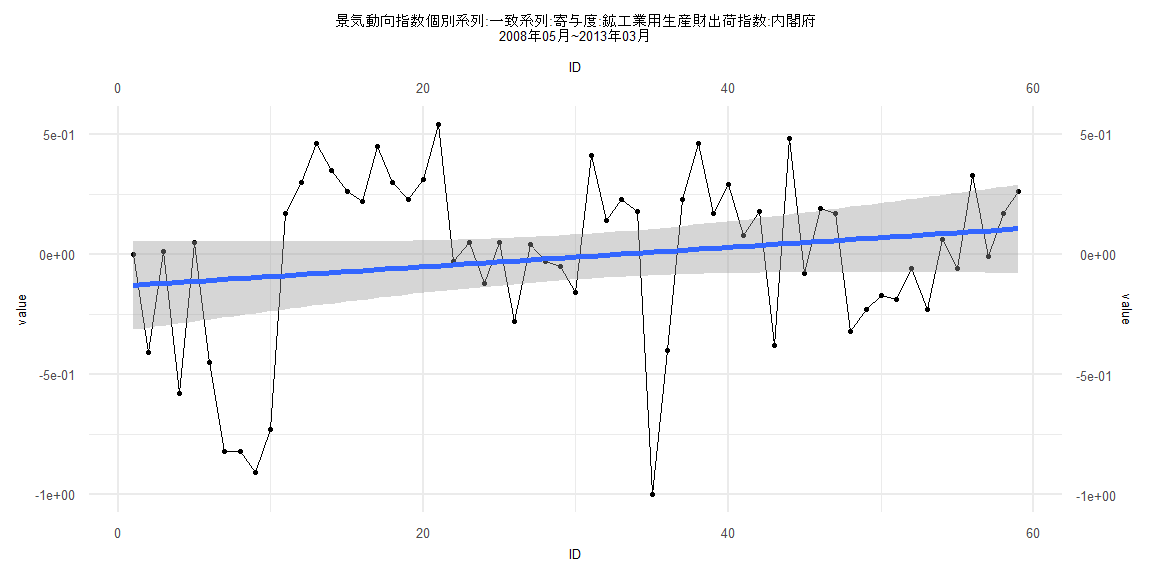

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.58305 -0.10023 0.00642 0.10207 0.54983

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0116217 0.0467511 0.249 0.804

ID -0.0003202 0.0010283 -0.311 0.756

Residual standard error: 0.2045 on 76 degrees of freedom

Multiple R-squared: 0.001274, Adjusted R-squared: -0.01187

F-statistic: 0.09696 on 1 and 76 DF, p-value: 0.7564

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.076923, p-value = 0.9766

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.9455, p-value = 1

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.6272, df = 1, p-value = 0.03147

Box-Ljung test

data: lm_residuals

X-squared = 18.22, df = 1, p-value = 0.00001968