Analysis

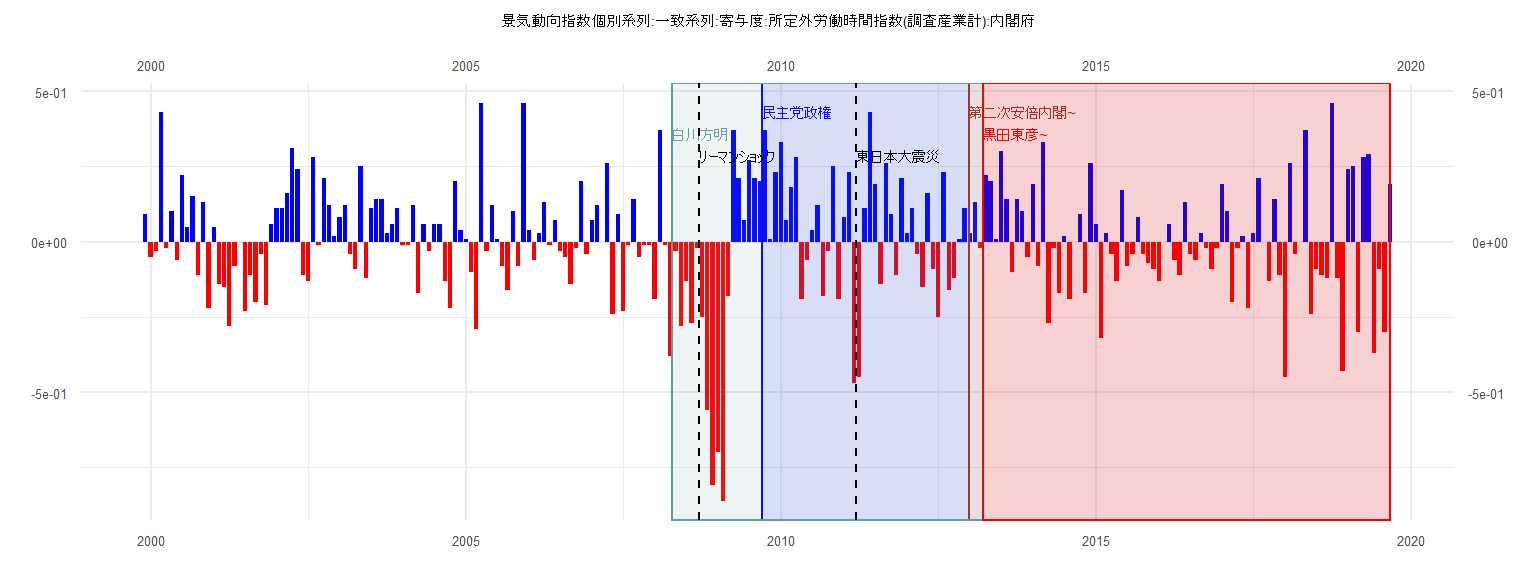

[1] "景気動向指数個別系列:一致系列:寄与度:所定外労働時間指数(調査産業計):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.09

2000 -0.05 -0.03 0.43 -0.02 0.10 -0.06 0.22 0.05 0.15 -0.11 0.13 -0.22

2001 0.05 -0.14 -0.15 -0.28 -0.08 0.00 -0.23 -0.11 -0.20 -0.04 -0.21 0.06

2002 0.11 0.11 0.16 0.31 0.24 -0.11 -0.13 0.28 -0.01 0.21 0.12 0.02

2003 0.08 0.12 -0.04 -0.09 0.25 -0.12 0.11 0.14 0.14 0.03 0.06 0.11

2004 -0.01 -0.01 0.12 -0.17 0.06 -0.03 0.06 0.06 -0.13 -0.22 0.20 0.04

2005 0.01 -0.10 -0.29 0.46 -0.03 0.12 0.01 -0.08 -0.16 0.10 -0.08 0.46

2006 0.04 -0.06 0.03 0.13 -0.01 0.07 -0.03 -0.05 -0.14 -0.02 0.20 -0.04

2007 0.07 0.12 0.00 0.26 -0.24 0.09 -0.23 -0.01 0.14 -0.05 -0.01 -0.01

2008 -0.19 0.37 -0.01 -0.38 -0.03 -0.28 -0.13 -0.27 -0.02 -0.25 -0.56 -0.81

2009 -0.70 -0.86 -0.18 0.37 0.21 0.07 0.27 0.21 0.20 0.37 0.01 0.23

2010 0.33 0.07 0.18 0.28 -0.19 -0.06 0.04 0.12 -0.18 -0.03 0.25 -0.19

2011 0.08 0.23 -0.47 -0.45 0.11 0.43 0.19 -0.14 0.26 0.09 -0.11 0.21

2012 0.03 0.11 -0.04 -0.15 0.16 -0.09 -0.25 0.23 -0.16 -0.12 0.01 0.11

2013 0.03 0.13 -0.02 0.22 0.20 0.01 0.30 0.14 -0.10 0.14 0.10 -0.05

2014 0.19 -0.08 0.33 -0.27 -0.02 -0.17 0.02 -0.19 0.00 0.09 -0.17 0.26

2015 0.06 -0.32 0.03 -0.04 -0.13 0.17 -0.08 -0.04 0.08 -0.04 -0.07 -0.09

2016 -0.13 0.00 0.06 -0.06 -0.11 0.13 -0.04 -0.06 0.03 -0.02 -0.09 -0.02

2017 0.19 0.10 -0.20 -0.02 0.02 -0.22 0.03 0.21 0.00 -0.13 0.14 -0.11

2018 -0.45 0.26 -0.04 0.00 0.37 -0.24 -0.09 -0.11 -0.12 0.46 -0.12 -0.43

2019 0.24 0.25 -0.30 0.28 0.29 -0.37 -0.09 -0.30 0.19

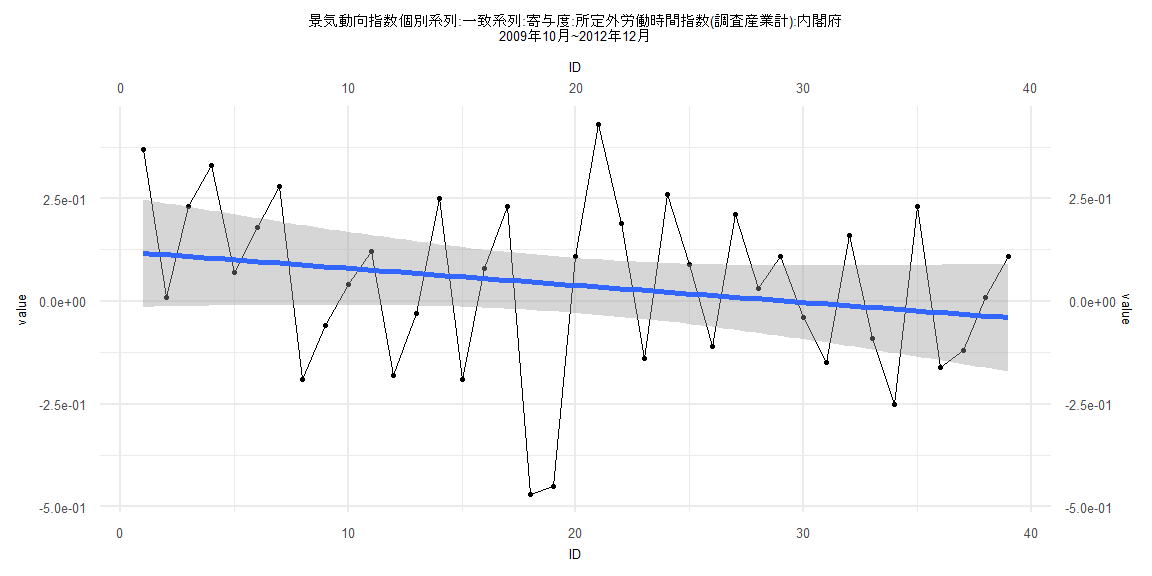

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.5167 -0.1280 0.0250 0.1655 0.3957

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.121174 0.067166 1.804 0.0794 .

ID -0.004136 0.002927 -1.413 0.1660

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2057 on 37 degrees of freedom

Multiple R-squared: 0.0512, Adjusted R-squared: 0.02556

F-statistic: 1.997 on 1 and 37 DF, p-value: 0.166

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.9693, p-value = 0.3939

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.2193, df = 1, p-value = 0.6396

Box-Ljung test

data: lm_residuals

X-squared = 0.0063251, df = 1, p-value = 0.9366

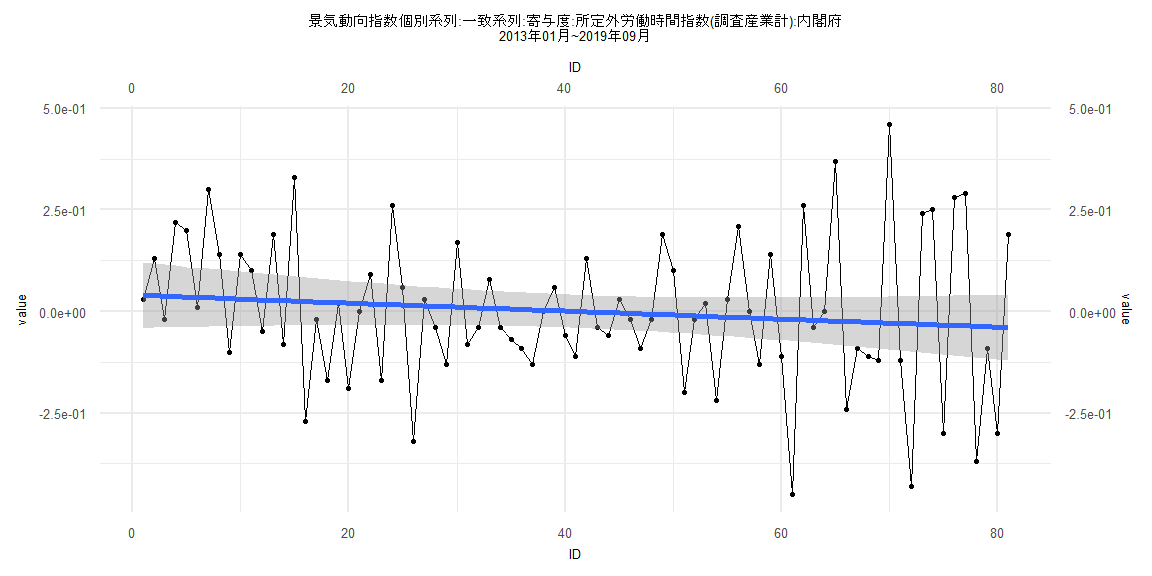

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43034 -0.09247 -0.01837 0.10885 0.48851

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0403056 0.0410491 0.982 0.329

ID -0.0009831 0.0008697 -1.130 0.262

Residual standard error: 0.183 on 79 degrees of freedom

Multiple R-squared: 0.01592, Adjusted R-squared: 0.003458

F-statistic: 1.278 on 1 and 79 DF, p-value: 0.2618

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.098765, p-value = 0.8277

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.4831, p-value = 0.9821

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 10.032, df = 1, p-value = 0.001538

Box-Ljung test

data: lm_residuals

X-squared = 5.3165, df = 1, p-value = 0.02113

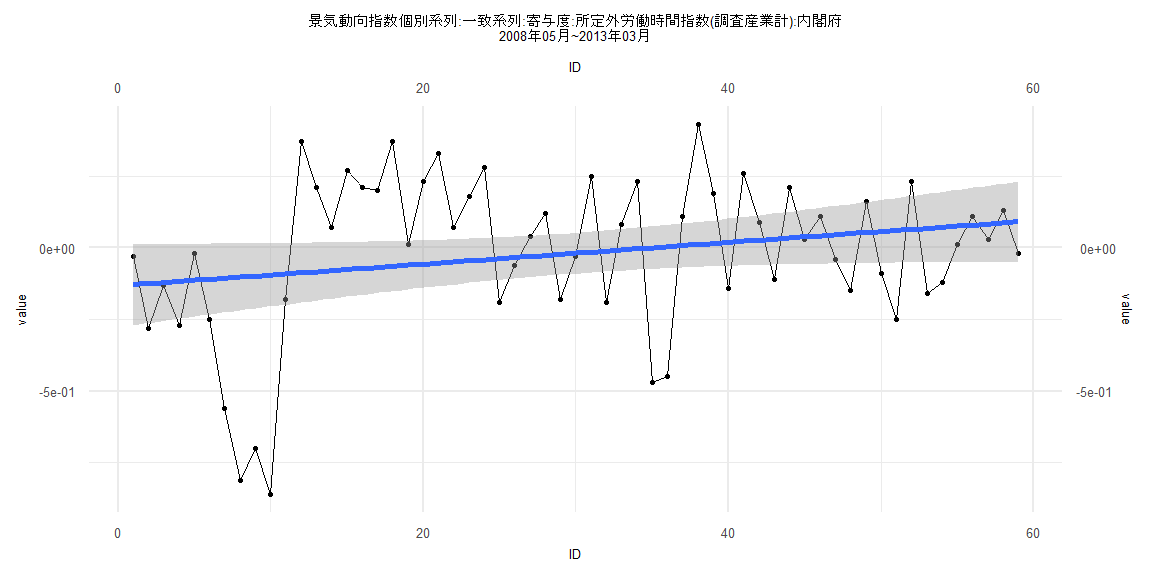

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.76532 -0.15235 0.04301 0.17546 0.45711

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.132531 0.072149 -1.837 0.0714 .

ID 0.003785 0.002092 1.810 0.0756 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2736 on 57 degrees of freedom

Multiple R-squared: 0.05433, Adjusted R-squared: 0.03774

F-statistic: 3.275 on 1 and 57 DF, p-value: 0.07562

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.084746, p-value = 0.9854

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0368, p-value = 0.00001979

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.0489, df = 1, p-value = 0.007931

Box-Ljung test

data: lm_residuals

X-squared = 14.238, df = 1, p-value = 0.0001611

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43051 -0.09403 -0.01868 0.11028 0.48809

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0359774 0.0425686 0.845 0.401

ID -0.0009563 0.0009363 -1.021 0.310

Residual standard error: 0.1862 on 76 degrees of freedom

Multiple R-squared: 0.01354, Adjusted R-squared: 0.0005601

F-statistic: 1.043 on 1 and 76 DF, p-value: 0.3103

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14103, p-value = 0.4221

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.4599, p-value = 0.9743

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 8.6254, df = 1, p-value = 0.003315

Box-Ljung test

data: lm_residuals

X-squared = 4.9192, df = 1, p-value = 0.02656