Analysis

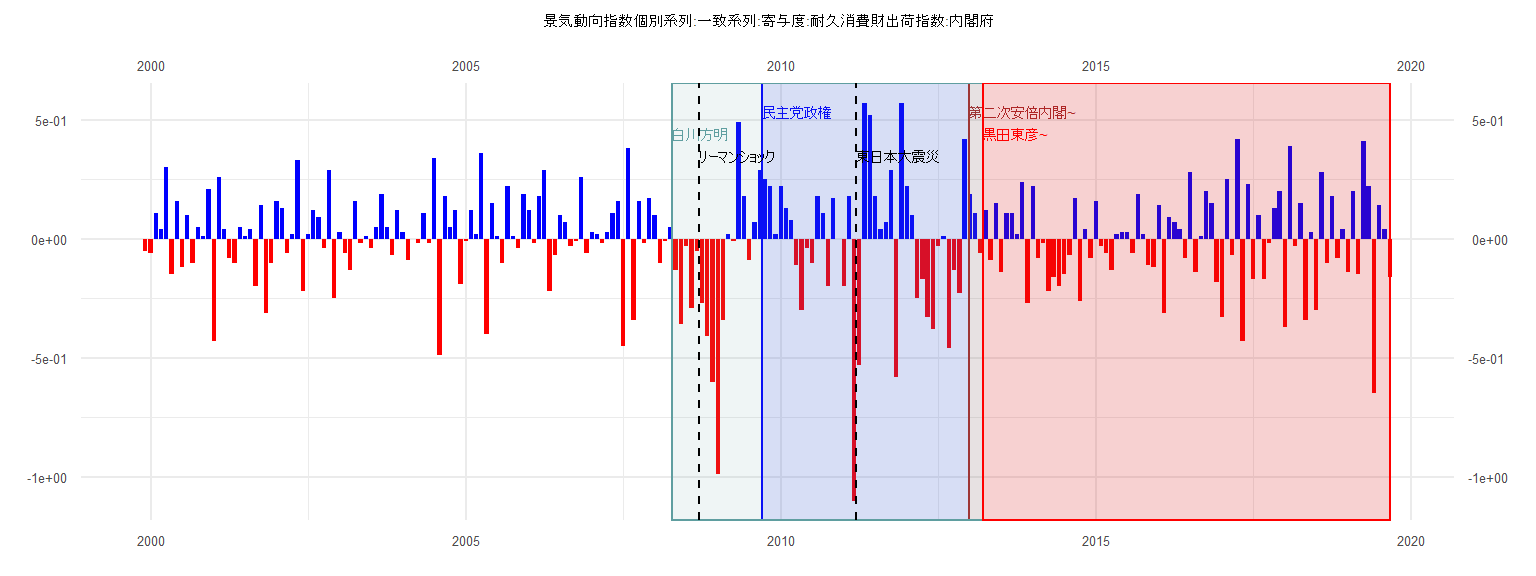

[1] "景気動向指数個別系列:一致系列:寄与度:耐久消費財出荷指数:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.05

2000 -0.06 0.11 0.04 0.30 -0.15 0.16 -0.12 0.10 -0.10 0.05 0.01 0.21

2001 -0.43 0.26 0.04 -0.08 -0.10 0.05 0.01 0.04 -0.20 0.14 -0.31 -0.10

2002 0.16 0.13 -0.06 0.02 0.33 -0.22 0.02 0.12 0.09 -0.04 0.29 -0.25

2003 0.03 -0.06 -0.13 0.16 -0.02 0.01 -0.04 0.05 0.19 0.05 -0.07 0.12

2004 0.03 -0.09 0.00 -0.02 0.11 -0.02 0.34 -0.49 0.18 0.05 0.12 -0.19

2005 -0.01 0.12 0.02 0.36 -0.40 0.15 0.01 -0.10 0.22 0.01 -0.04 0.19

2006 0.12 -0.02 0.18 0.29 -0.22 -0.07 0.10 0.07 -0.03 -0.01 0.26 -0.06

2007 0.03 0.02 -0.02 0.03 0.11 0.16 -0.45 0.38 -0.34 0.16 -0.02 0.17

2008 0.10 -0.10 -0.01 0.05 -0.13 -0.36 -0.03 -0.29 -0.05 -0.27 -0.41 -0.60

2009 -0.99 -0.34 0.02 -0.01 0.49 0.18 -0.09 0.07 0.29 0.25 0.22 0.02

2010 0.22 0.13 0.08 -0.11 -0.30 -0.04 -0.10 0.18 0.11 -0.20 0.17 0.00

2011 -0.20 0.18 -1.10 -0.53 0.57 0.52 0.18 0.04 0.07 0.29 -0.58 0.57

2012 0.22 0.10 -0.25 -0.17 -0.33 -0.38 -0.03 0.01 -0.46 -0.13 -0.23 0.42

2013 0.19 0.11 -0.06 0.12 -0.09 0.15 -0.14 0.11 0.11 0.02 0.24 -0.27

2014 0.22 -0.08 -0.02 -0.22 -0.16 -0.20 -0.15 -0.07 0.17 -0.26 0.04 -0.08

2015 0.16 -0.03 -0.06 -0.13 0.02 0.03 0.03 -0.06 0.19 0.02 -0.11 -0.12

2016 0.14 -0.31 0.09 0.07 0.04 -0.08 0.28 -0.14 0.01 0.20 0.15 -0.18

2017 -0.33 0.25 -0.07 0.42 -0.43 0.23 -0.17 0.10 -0.17 -0.02 0.13 0.20

2018 -0.37 0.39 -0.03 0.15 -0.34 0.03 -0.30 0.28 -0.10 0.18 -0.08 0.04

2019 -0.14 0.20 -0.15 0.41 0.22 -0.65 0.14 0.04 -0.16

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.09365 -0.17145 0.04654 0.16188 0.61583

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.072605 0.108836 0.667 0.509

ID -0.004387 0.004742 -0.925 0.361

Residual standard error: 0.3333 on 37 degrees of freedom

Multiple R-squared: 0.0226, Adjusted R-squared: -0.003815

F-statistic: 0.8556 on 1 and 37 DF, p-value: 0.361

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.7969, p-value = 0.2077

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.41938, df = 1, p-value = 0.5172

Box-Ljung test

data: lm_residuals

X-squared = 0.17701, df = 1, p-value = 0.674

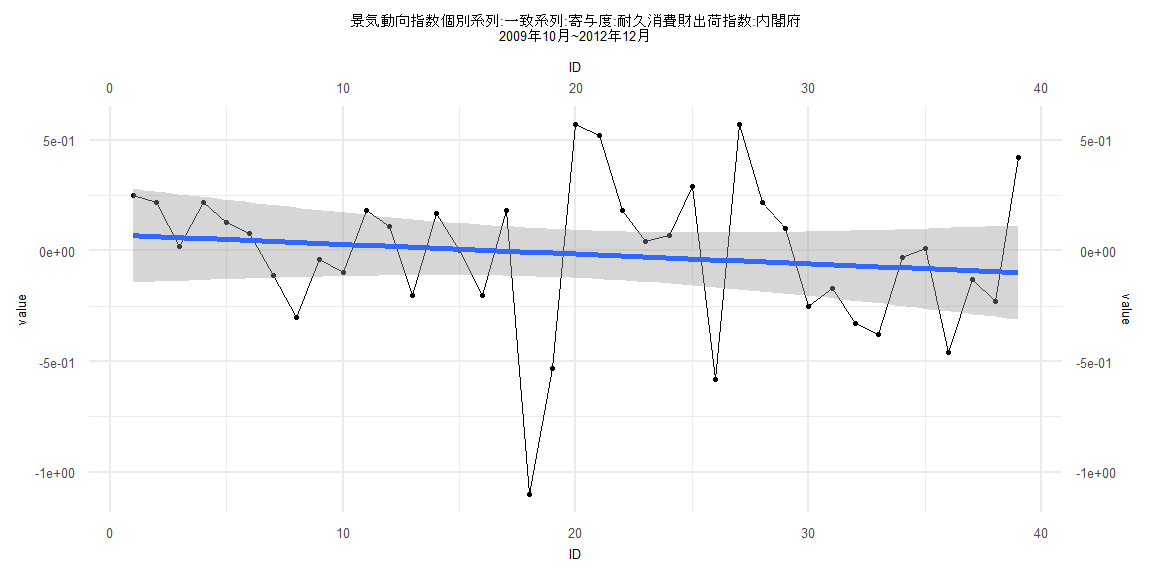

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.64406 -0.13451 0.01979 0.14942 0.42359

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.00112037 0.04477671 0.025 0.980

ID -0.00009056 0.00094870 -0.095 0.924

Residual standard error: 0.1996 on 79 degrees of freedom

Multiple R-squared: 0.0001153, Adjusted R-squared: -0.01254

F-statistic: 0.009112 on 1 and 79 DF, p-value: 0.9242

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12346, p-value = 0.5705

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.8689, p-value = 1

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.6231, df = 1, p-value = 0.005762

Box-Ljung test

data: lm_residuals

X-squared = 16.558, df = 1, p-value = 0.00004719

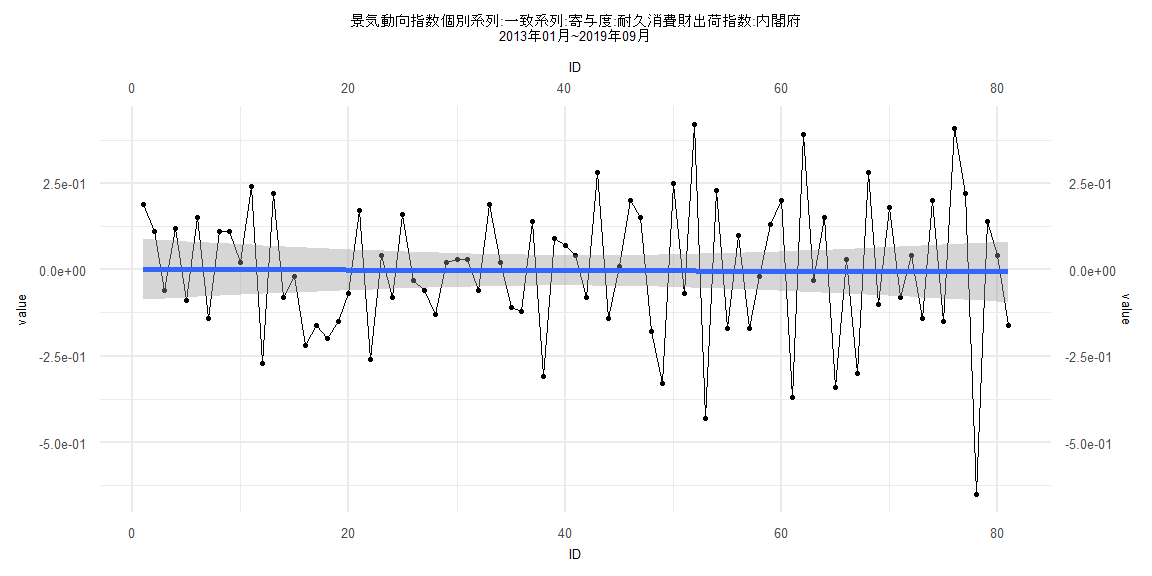

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.06480 -0.17060 0.06175 0.21020 0.59982

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.129316 0.087705 -1.474 0.146

ID 0.002689 0.002542 1.058 0.295

Residual standard error: 0.3326 on 57 degrees of freedom

Multiple R-squared: 0.01925, Adjusted R-squared: 0.002042

F-statistic: 1.119 on 1 and 57 DF, p-value: 0.2947

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4377, p-value = 0.009272

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.002346, df = 1, p-value = 0.9614

Box-Ljung test

data: lm_residuals

X-squared = 4.8827, df = 1, p-value = 0.02713

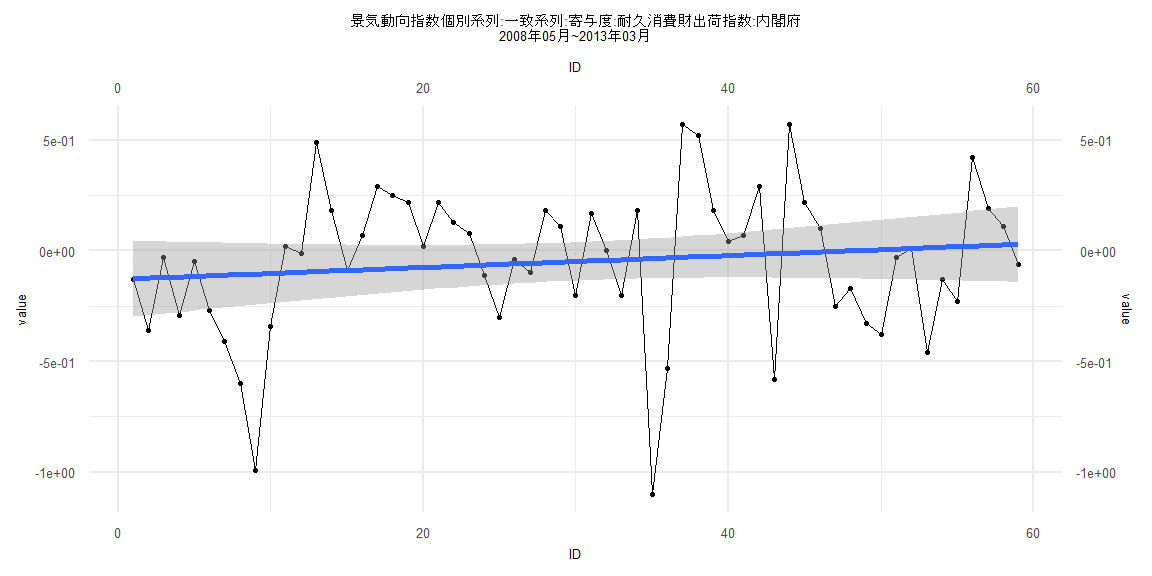

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.64986 -0.13300 0.02125 0.15093 0.42426

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0120380 0.0461338 -0.261 0.795

ID 0.0001587 0.0010147 0.156 0.876

Residual standard error: 0.2018 on 76 degrees of freedom

Multiple R-squared: 0.0003218, Adjusted R-squared: -0.01283

F-statistic: 0.02446 on 1 and 76 DF, p-value: 0.8761

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11538, p-value = 0.6802

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.8976, p-value = 1

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.0072, df = 1, p-value = 0.008118

Box-Ljung test

data: lm_residuals

X-squared = 16.833, df = 1, p-value = 0.00004081