Analysis

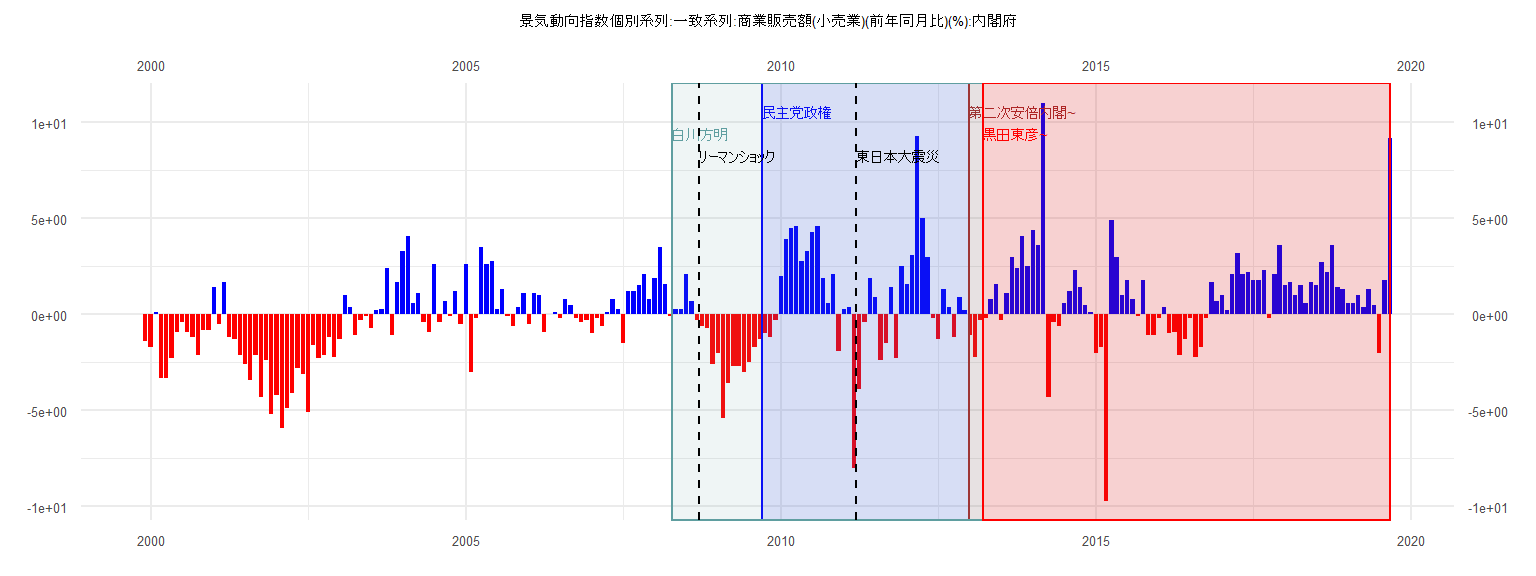

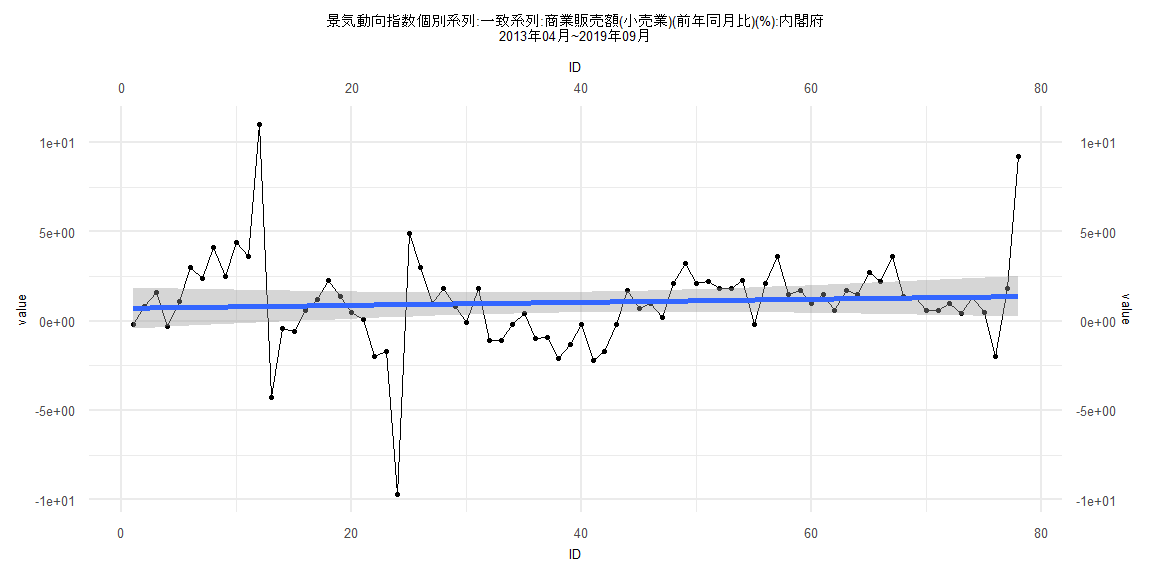

[1] "景気動向指数個別系列:一致系列:商業販売額(小売業)(前年同月比)(%):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -1.4

2000 -1.7 0.1 -3.3 -3.3 -2.3 -0.9 -0.4 -0.9 -1.2 -2.1 -0.8 -0.8

2001 1.4 -0.5 1.7 -1.2 -1.3 -2.1 -2.6 -3.4 -2.1 -4.3 -2.4 -5.2

2002 -4.2 -5.9 -4.9 -4.1 -2.8 -3.1 -5.1 -1.6 -2.3 -2.1 -1.2 -2.2

2003 -1.3 1.0 0.4 -1.1 -0.3 -0.1 -0.7 0.2 0.3 2.4 -1.1 1.7

2004 3.3 4.1 0.6 1.1 -0.4 -0.9 2.6 -0.4 0.7 -0.1 1.2 -0.5

2005 2.6 -3.0 -0.2 3.5 2.6 2.8 0.3 1.3 -0.1 -0.6 0.4 1.1

2006 -0.5 1.1 1.0 -0.9 0.0 0.1 -0.2 0.8 0.5 -0.2 -0.4 -0.3

2007 -1.0 -0.2 -0.6 0.1 0.8 0.3 -1.5 1.2 1.2 1.5 2.1 0.8

2008 1.9 3.5 1.6 -0.1 0.3 0.3 2.1 0.7 -0.3 -0.6 -0.7 -2.6

2009 -2.0 -5.4 -3.6 -2.7 -2.7 -3.0 -2.5 -1.7 -1.3 -1.0 -1.2 -0.3

2010 2.0 3.9 4.5 4.6 2.8 3.3 4.3 4.6 1.9 0.6 2.1 -1.9

2011 0.3 0.4 -8.0 -3.9 -0.4 1.9 0.9 -2.4 -1.5 1.4 -2.3 2.5

2012 1.6 3.1 9.3 5.0 3.0 -0.2 -1.3 1.3 0.4 -1.2 0.9 0.2

2013 -1.1 -2.2 -0.3 -0.2 0.8 1.6 -0.3 1.1 3.0 2.4 4.1 2.5

2014 4.4 3.6 11.0 -4.3 -0.4 -0.6 0.6 1.2 2.3 1.4 0.5 0.1

2015 -2.0 -1.7 -9.7 4.9 3.0 1.0 1.8 0.8 -0.1 1.8 -1.1 -1.1

2016 -0.2 0.4 -1.0 -0.9 -2.1 -1.3 -0.2 -2.2 -1.7 -0.2 1.7 0.7

2017 1.0 0.2 2.1 3.2 2.1 2.2 1.8 1.8 2.3 -0.2 2.1 3.6

2018 1.5 1.7 1.0 1.5 0.6 1.7 1.5 2.7 2.2 3.6 1.4 1.3

2019 0.6 0.6 1.0 0.4 1.3 0.5 -2.0 1.8 9.2

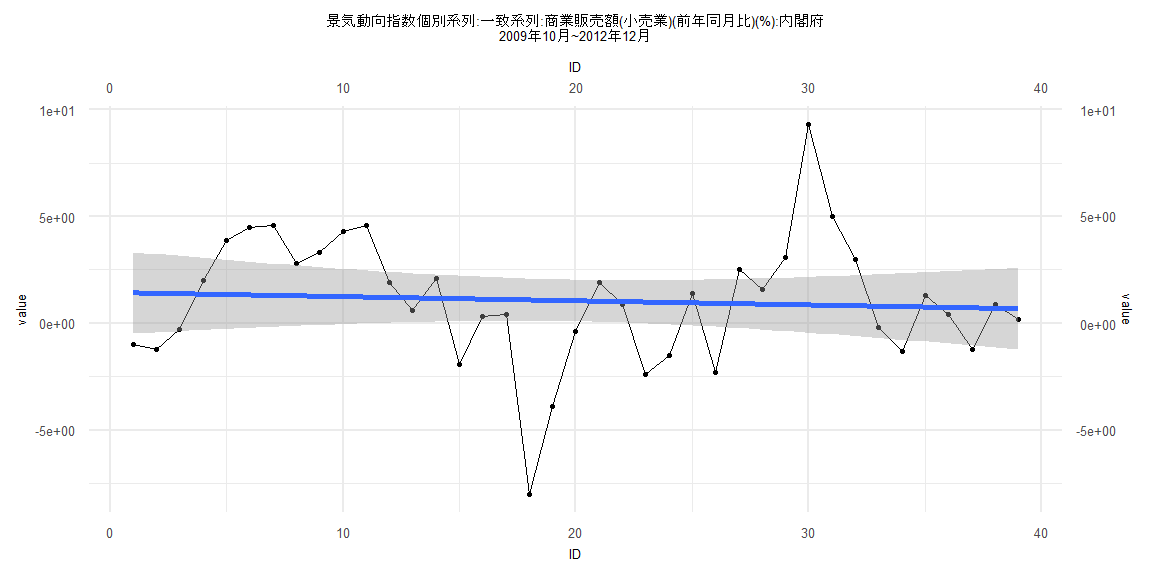

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-9.0954 -1.8064 0.1945 1.8046 8.4385

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.44629 0.97837 1.478 0.148

ID -0.01949 0.04263 -0.457 0.650

Residual standard error: 2.996 on 37 degrees of freedom

Multiple R-squared: 0.005619, Adjusted R-squared: -0.02126

F-statistic: 0.2091 on 1 and 37 DF, p-value: 0.6502

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.90326, p-value = 0.00003831

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0084302, df = 1, p-value = 0.9268

Box-Ljung test

data: lm_residuals

X-squared = 12.232, df = 1, p-value = 0.0004699

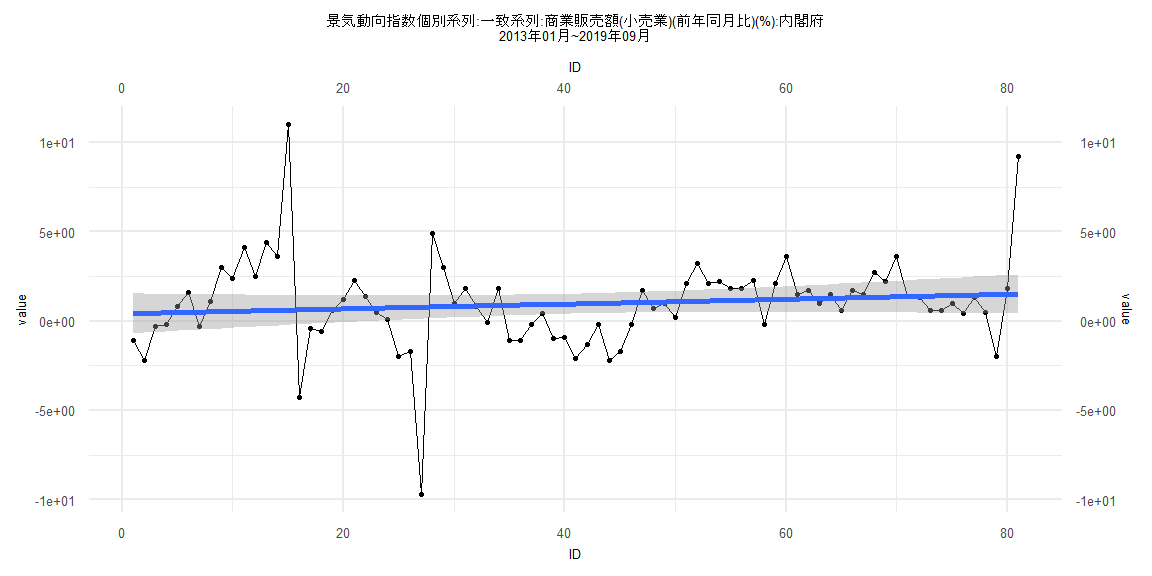

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-10.4747 -1.0394 -0.0665 0.9711 10.3876

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.40938 0.56598 0.723 0.472

ID 0.01353 0.01199 1.128 0.263

Residual standard error: 2.523 on 79 degrees of freedom

Multiple R-squared: 0.01586, Adjusted R-squared: 0.003406

F-statistic: 1.273 on 1 and 79 DF, p-value: 0.2625

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.22222, p-value = 0.03633

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5312, p-value = 0.01181

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.1294, df = 1, p-value = 0.2879

Box-Ljung test

data: lm_residuals

X-squared = 2.5215, df = 1, p-value = 0.1123

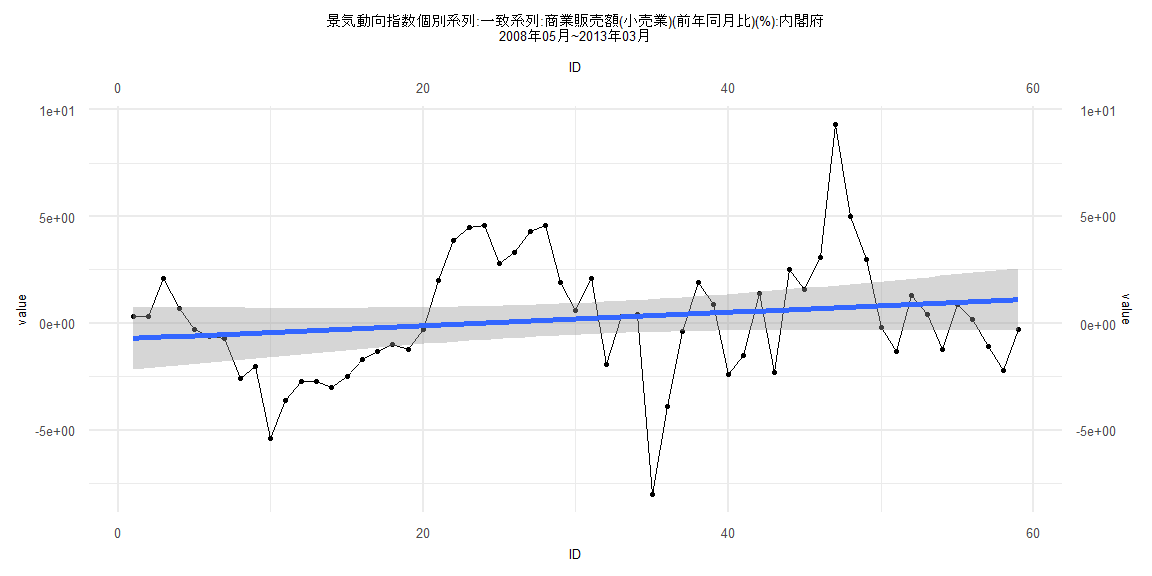

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-8.3579 -2.1298 -0.0825 1.7953 8.5673

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.73530 0.74752 -0.984 0.329

ID 0.03123 0.02167 1.441 0.155

Residual standard error: 2.834 on 57 degrees of freedom

Multiple R-squared: 0.03516, Adjusted R-squared: 0.01824

F-statistic: 2.077 on 1 and 57 DF, p-value: 0.155

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.7287, p-value = 0.000000005786

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.38366, df = 1, p-value = 0.5357

Box-Ljung test

data: lm_residuals

X-squared = 24.815, df = 1, p-value = 0.0000006309

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-10.6159 -1.0617 0.0305 0.9239 10.1859

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.712321 0.581688 1.225 0.225

ID 0.008484 0.012794 0.663 0.509

Residual standard error: 2.544 on 76 degrees of freedom

Multiple R-squared: 0.005753, Adjusted R-squared: -0.00733

F-statistic: 0.4397 on 1 and 76 DF, p-value: 0.5093

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.316

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5564, p-value = 0.01744

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.2818, df = 1, p-value = 0.2576

Box-Ljung test

data: lm_residuals

X-squared = 2.041, df = 1, p-value = 0.1531