Analysis

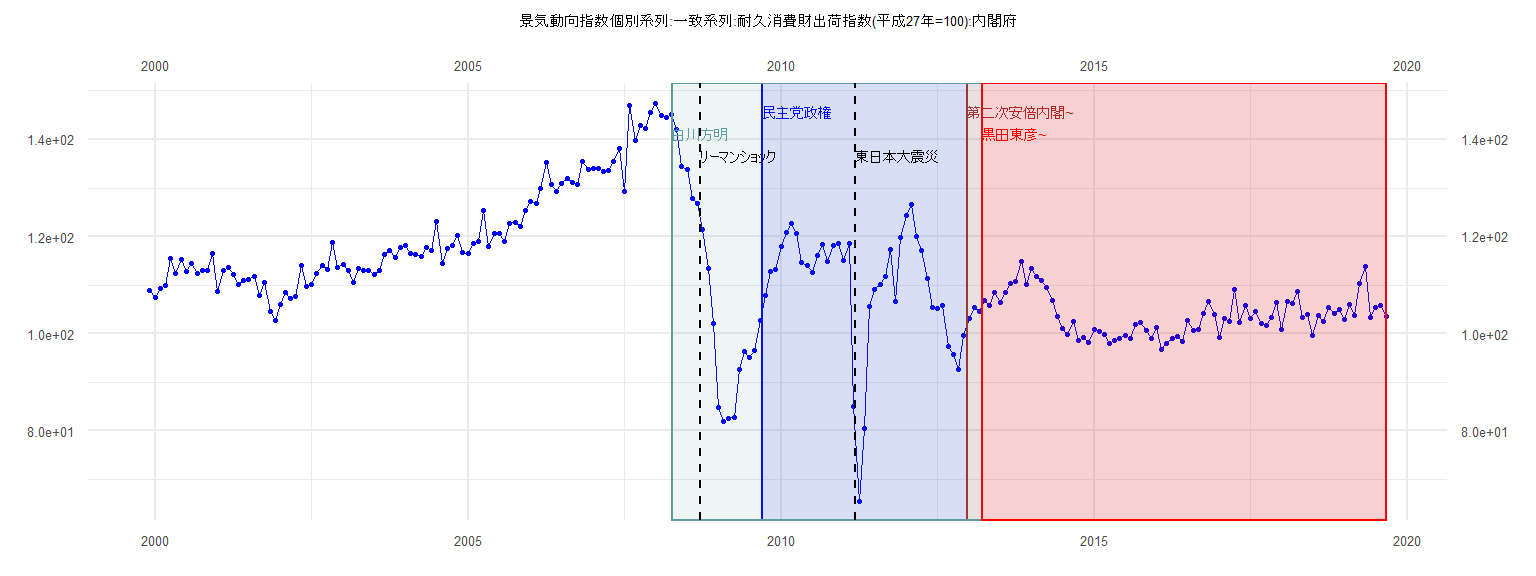

[1] "景気動向指数個別系列:一致系列:耐久消費財出荷指数(平成27年=100):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 108.8

2000 107.4 109.3 109.9 115.4 112.4 115.2 112.8 114.5 112.4 113.1 113.0 116.6

2001 108.7 113.1 113.7 112.1 110.2 111.0 111.1 111.7 107.8 110.5 104.6 102.7

2002 105.9 108.5 107.3 107.7 114.0 109.8 110.2 112.4 114.1 113.3 118.7 113.7

2003 114.2 113.0 110.5 113.4 113.0 113.1 112.2 113.0 116.4 117.2 115.7 117.7

2004 118.2 116.5 116.4 115.9 117.7 117.2 123.2 114.4 117.5 118.2 120.2 116.7

2005 116.5 118.6 118.9 125.4 118.0 120.7 120.7 118.9 122.7 122.8 122.0 125.4

2006 127.3 126.8 129.9 135.2 130.8 129.2 130.9 132.0 131.2 130.8 135.4 133.8

2007 134.0 134.1 133.4 133.6 135.4 138.2 129.3 147.0 139.8 142.8 142.3 145.5

2008 147.4 145.0 144.5 145.2 142.1 134.5 133.8 127.9 126.8 121.4 113.4 102.1

2009 84.7 81.8 82.5 82.7 92.6 96.4 95.0 96.6 102.6 107.9 112.7 113.3

2010 118.0 120.8 122.6 120.6 114.7 114.1 112.5 116.1 118.4 114.8 118.2 118.5

2011 115.0 118.6 84.9 65.5 80.4 105.5 109.1 110.2 111.8 117.4 106.6 119.9

2012 124.4 126.6 120.0 117.1 111.4 105.3 105.1 105.7 97.3 95.7 92.6 99.6

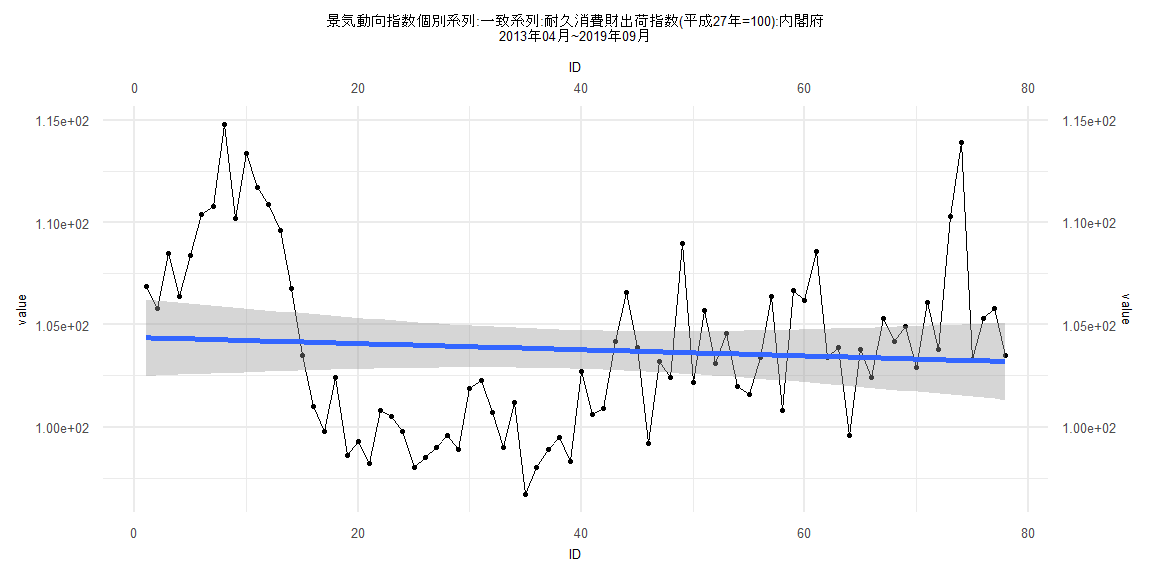

2013 103.1 105.3 104.6 106.9 105.8 108.5 106.4 108.4 110.4 110.8 114.8 110.2

2014 113.4 111.7 110.9 109.6 106.8 103.5 101.0 99.8 102.4 98.6 99.3 98.2

2015 100.8 100.5 99.8 98.0 98.5 99.0 99.6 98.9 101.9 102.3 100.7 99.0

2016 101.2 96.7 98.0 98.9 99.5 98.3 102.7 100.6 100.9 104.2 106.6 103.9

2017 99.2 103.2 102.4 109.0 102.2 105.7 103.1 104.6 102.0 101.6 103.4 106.4

2018 100.8 106.7 106.2 108.6 103.4 103.9 99.6 103.8 102.4 105.3 104.2 104.9

2019 102.9 106.1 103.8 110.3 113.9 103.3 105.3 105.8 103.5

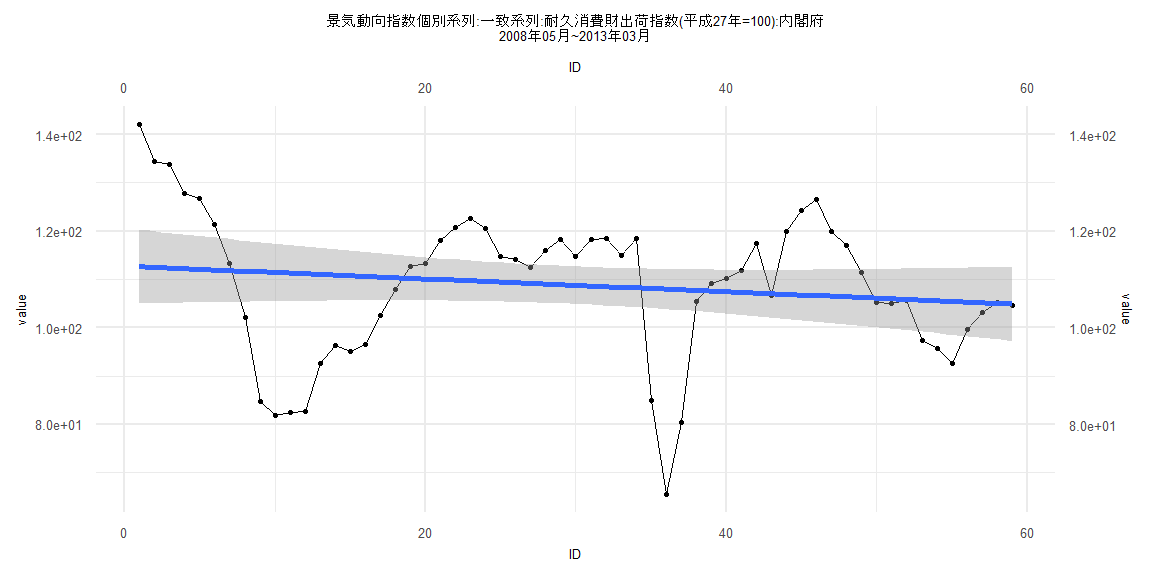

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-44.795 -2.634 1.199 6.354 19.540

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 116.4430 3.9893 29.189 <0.0000000000000002 ***

ID -0.3236 0.1738 -1.861 0.0707 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 12.22 on 37 degrees of freedom

Multiple R-squared: 0.08562, Adjusted R-squared: 0.06091

F-statistic: 3.465 on 1 and 37 DF, p-value: 0.07065

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.28205, p-value = 0.08974

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.57024, p-value = 0.0000000156

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.091639, df = 1, p-value = 0.7621

Box-Ljung test

data: lm_residuals

X-squared = 21.042, df = 1, p-value = 0.000004493

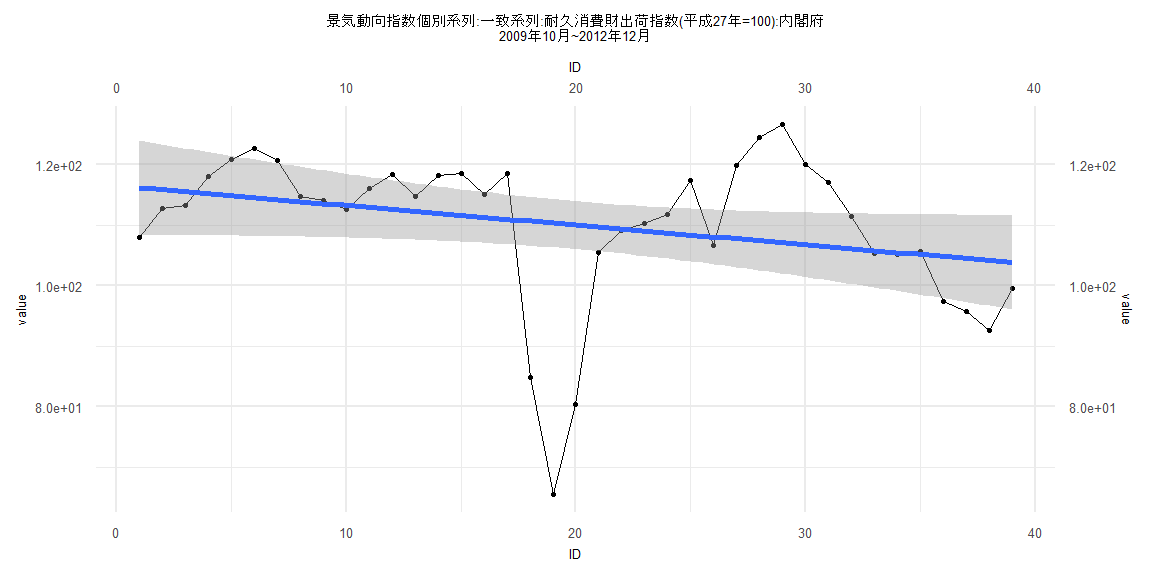

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-7.152 -3.197 -0.139 2.574 10.629

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 104.41870 0.92907 112.390 <0.0000000000000002 ***

ID -0.01491 0.01968 -0.757 0.451

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.142 on 79 degrees of freedom

Multiple R-squared: 0.00721, Adjusted R-squared: -0.005357

F-statistic: 0.5737 on 1 and 79 DF, p-value: 0.451

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.098765, p-value = 0.8277

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.5538, p-value = 0.000000000000001387

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.7687, df = 1, p-value = 0.02898

Box-Ljung test

data: lm_residuals

X-squared = 43.861, df = 1, p-value = 0.00000000003525

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-42.496 -8.179 2.735 10.086 29.456

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 112.7770 3.9271 28.718 <0.0000000000000002 ***

ID -0.1328 0.1138 -1.166 0.248

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 14.89 on 57 degrees of freedom

Multiple R-squared: 0.02332, Adjusted R-squared: 0.00618

F-statistic: 1.361 on 1 and 57 DF, p-value: 0.2483

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.28814, p-value = 0.01452

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.3139, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.7816, df = 1, p-value = 0.01619

Box-Ljung test

data: lm_residuals

X-squared = 40.584, df = 1, p-value = 0.0000000001884

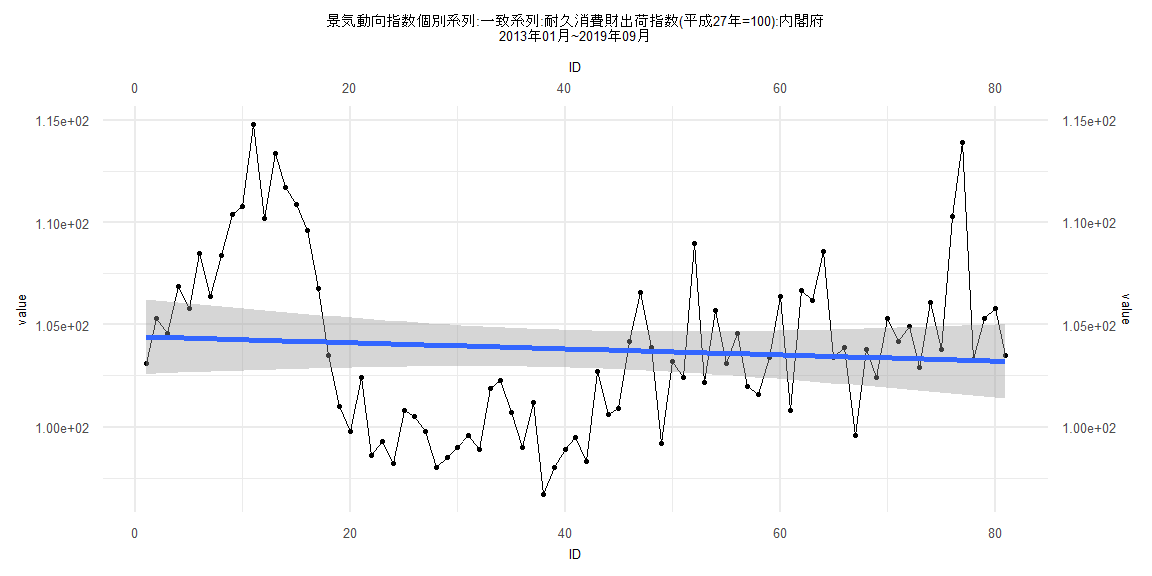

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-7.1552 -3.2390 -0.2819 2.6154 10.6344

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 104.38438 0.96470 108.204 <0.0000000000000002 ***

ID -0.01512 0.02122 -0.713 0.478

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.219 on 76 degrees of freedom

Multiple R-squared: 0.006636, Adjusted R-squared: -0.006434

F-statistic: 0.5077 on 1 and 76 DF, p-value: 0.4783

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.81

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.54692, p-value = 0.000000000000002773

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.3808, df = 1, p-value = 0.006592

Box-Ljung test

data: lm_residuals

X-squared = 42.495, df = 1, p-value = 0.00000000007086