Analysis

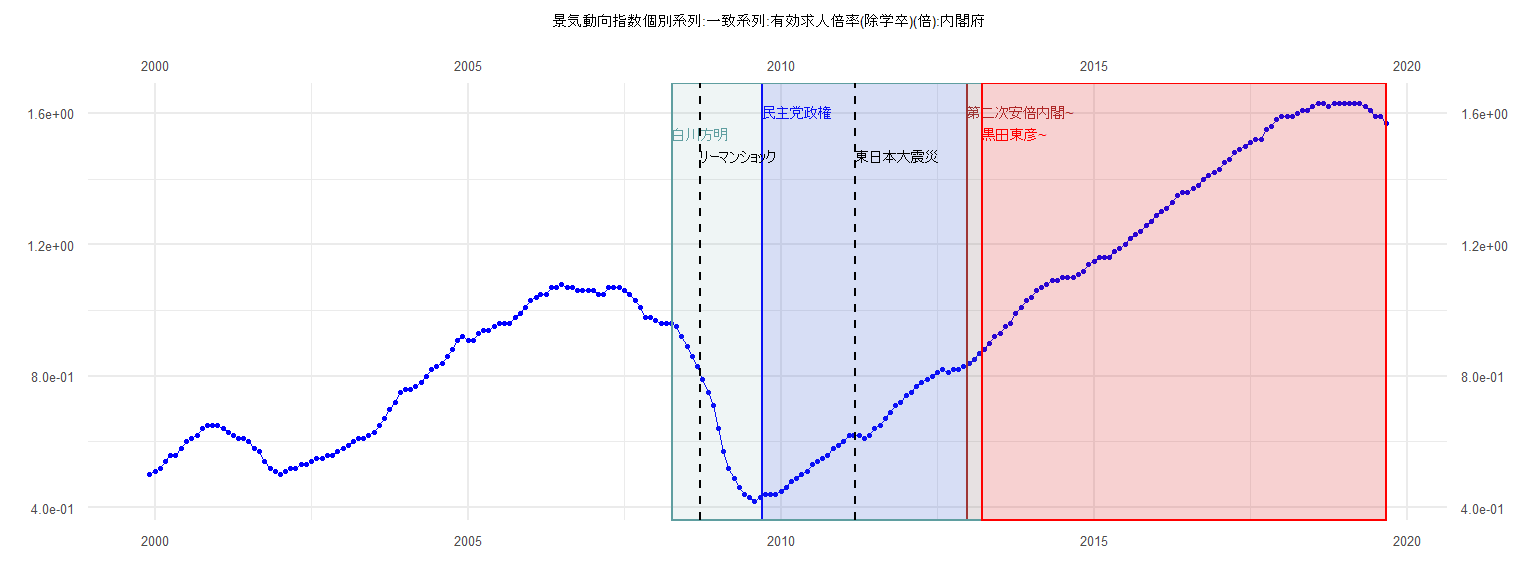

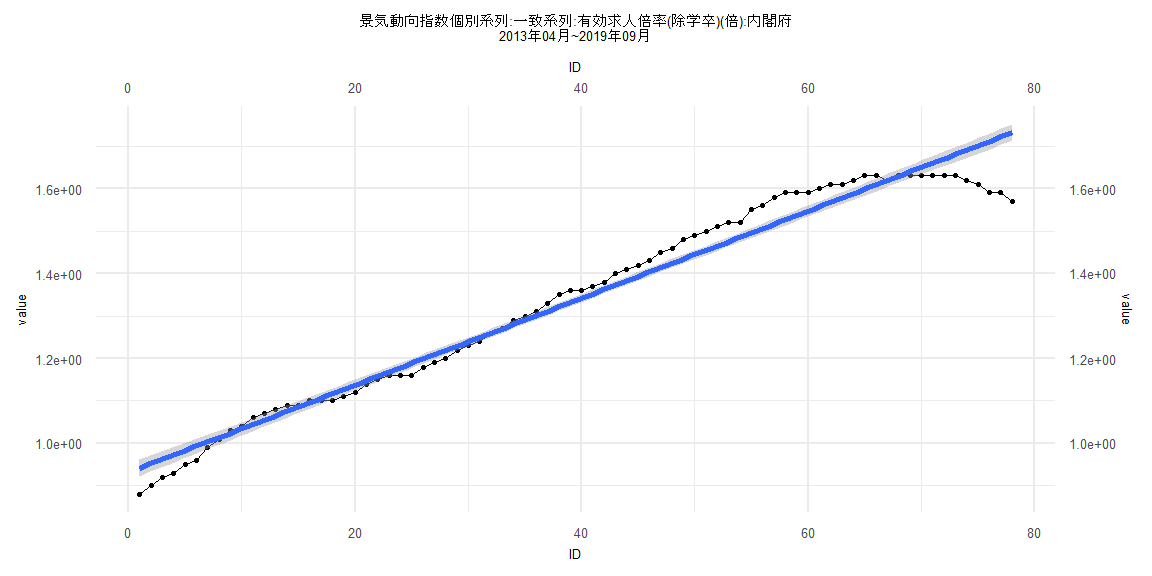

[1] "景気動向指数個別系列:一致系列:有効求人倍率(除学卒)(倍):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.50

2000 0.51 0.52 0.54 0.56 0.56 0.58 0.60 0.61 0.62 0.64 0.65 0.65

2001 0.65 0.64 0.63 0.62 0.61 0.61 0.60 0.58 0.57 0.54 0.52 0.51

2002 0.50 0.51 0.52 0.52 0.53 0.53 0.54 0.55 0.55 0.56 0.56 0.57

2003 0.58 0.59 0.60 0.61 0.61 0.62 0.63 0.65 0.67 0.70 0.72 0.75

2004 0.76 0.76 0.77 0.78 0.80 0.82 0.83 0.84 0.86 0.88 0.91 0.92

2005 0.91 0.91 0.93 0.94 0.94 0.95 0.96 0.96 0.96 0.98 0.99 1.01

2006 1.03 1.04 1.05 1.05 1.07 1.07 1.08 1.07 1.07 1.06 1.06 1.06

2007 1.06 1.05 1.05 1.07 1.07 1.07 1.06 1.05 1.03 1.01 0.98 0.98

2008 0.97 0.96 0.96 0.96 0.95 0.92 0.89 0.86 0.83 0.79 0.75 0.71

2009 0.64 0.57 0.52 0.49 0.46 0.44 0.43 0.42 0.43 0.44 0.44 0.44

2010 0.45 0.46 0.48 0.49 0.50 0.51 0.53 0.54 0.55 0.56 0.58 0.59

2011 0.60 0.62 0.62 0.62 0.61 0.62 0.64 0.65 0.67 0.69 0.71 0.72

2012 0.74 0.75 0.77 0.78 0.79 0.80 0.81 0.82 0.81 0.82 0.82 0.83

2013 0.84 0.85 0.87 0.88 0.90 0.92 0.93 0.95 0.96 0.99 1.01 1.03

2014 1.04 1.06 1.07 1.08 1.09 1.09 1.10 1.10 1.10 1.11 1.12 1.14

2015 1.15 1.16 1.16 1.16 1.18 1.19 1.20 1.22 1.23 1.24 1.26 1.27

2016 1.29 1.30 1.31 1.33 1.35 1.36 1.36 1.37 1.38 1.40 1.41 1.42

2017 1.43 1.45 1.46 1.48 1.49 1.50 1.51 1.52 1.52 1.55 1.56 1.58

2018 1.59 1.59 1.59 1.60 1.61 1.61 1.62 1.63 1.63 1.62 1.63 1.63

2019 1.63 1.63 1.63 1.63 1.62 1.61 1.59 1.59 1.57

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.028945 -0.007692 0.002332 0.010428 0.019777

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.412632 0.004406 93.66 <0.0000000000000002 ***

ID 0.011253 0.000192 58.62 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.01349 on 37 degrees of freedom

Multiple R-squared: 0.9893, Adjusted R-squared: 0.9891

F-statistic: 3436 on 1 and 37 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.34659, p-value = 0.00000000000133

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.6803, df = 1, p-value = 0.01716

Box-Ljung test

data: lm_residuals

X-squared = 25.151, df = 1, p-value = 0.0000005301

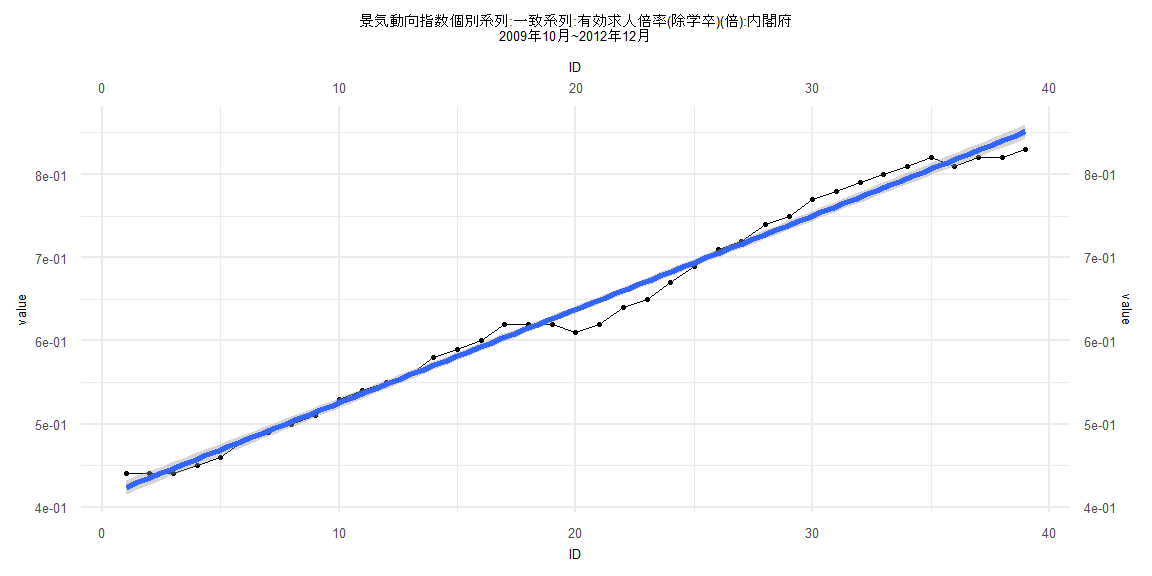

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.16634 -0.01409 0.01071 0.02933 0.06282

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.8910000 0.0098311 90.63 <0.0000000000000002 ***

ID 0.0104363 0.0002083 50.10 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.04383 on 79 degrees of freedom

Multiple R-squared: 0.9695, Adjusted R-squared: 0.9691

F-statistic: 2510 on 1 and 79 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.1358, p-value = 0.4462

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.048602, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 13.131, df = 1, p-value = 0.0002905

Box-Ljung test

data: lm_residuals

X-squared = 63.917, df = 1, p-value = 0.000000000000001332

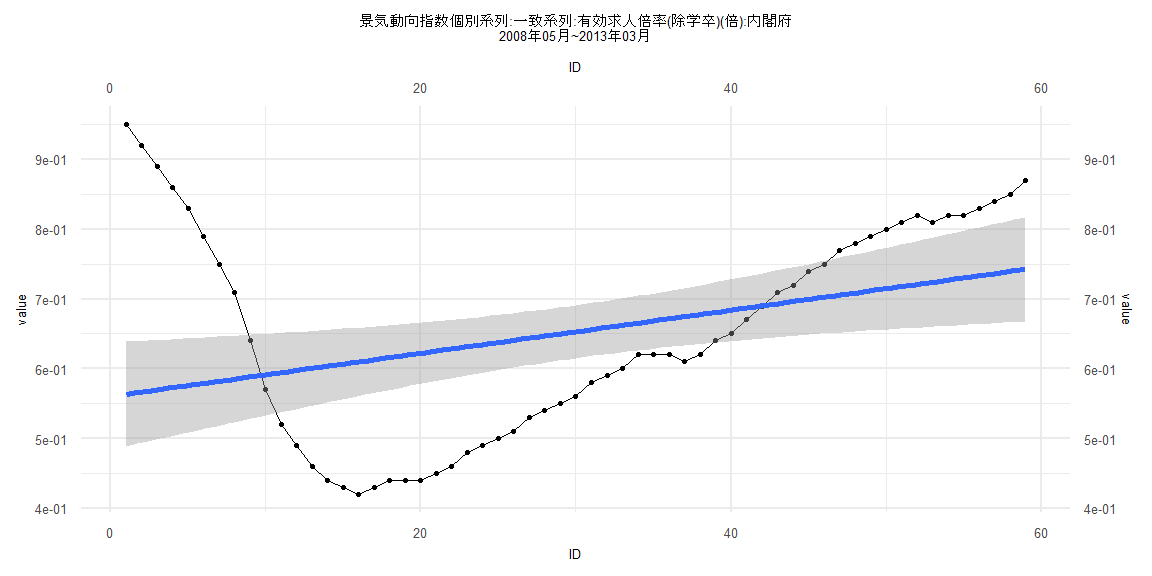

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.18986 -0.11065 -0.03390 0.09099 0.38642

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.560491 0.038398 14.597 < 0.0000000000000002 ***

ID 0.003085 0.001113 2.772 0.00752 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1456 on 57 degrees of freedom

Multiple R-squared: 0.1188, Adjusted R-squared: 0.1033

F-statistic: 7.683 on 1 and 57 DF, p-value: 0.007517

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.13559, p-value = 0.6544

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.025858, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 22.327, df = 1, p-value = 0.0000023

Box-Ljung test

data: lm_residuals

X-squared = 52.356, df = 1, p-value = 0.0000000000004629

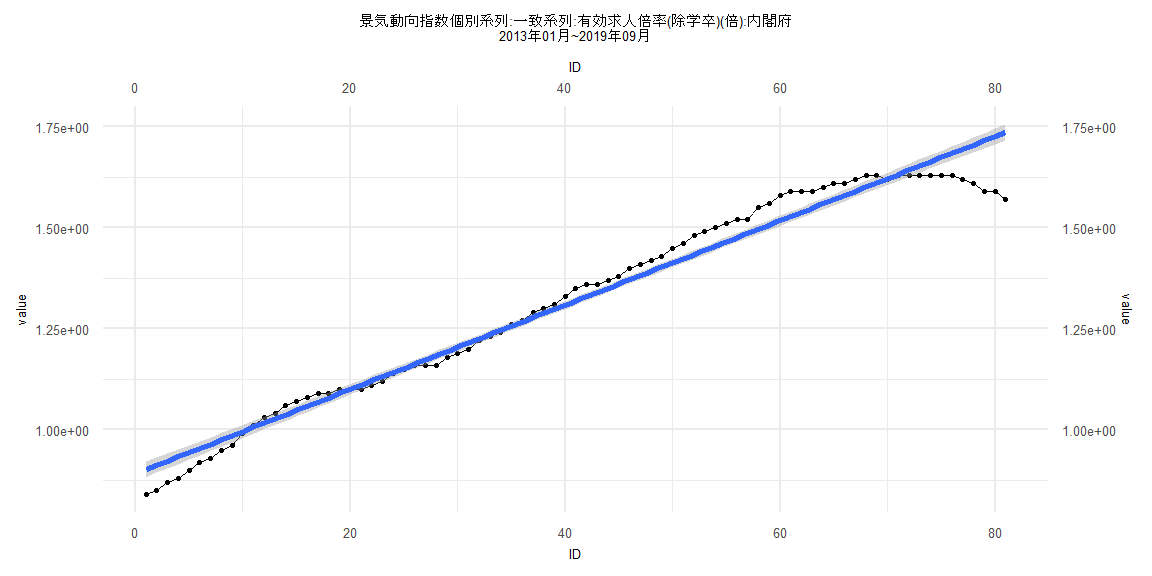

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.161659 -0.017568 0.005123 0.028525 0.063722

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.9316750 0.0098050 95.02 <0.0000000000000002 ***

ID 0.0102562 0.0002157 47.56 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.04288 on 76 degrees of freedom

Multiple R-squared: 0.9675, Adjusted R-squared: 0.9671

F-statistic: 2262 on 1 and 76 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.1624

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.051849, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 14.617, df = 1, p-value = 0.0001317

Box-Ljung test

data: lm_residuals

X-squared = 60.896, df = 1, p-value = 0.000000000000005995