Analysis

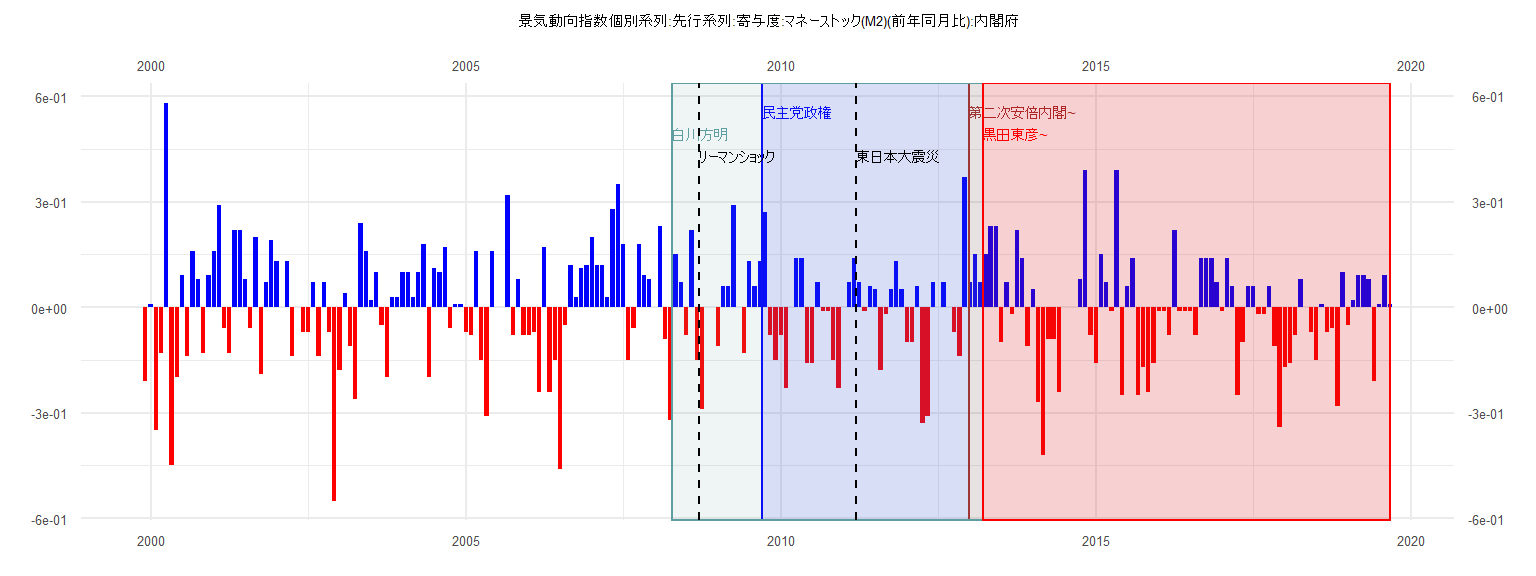

[1] "景気動向指数個別系列:先行系列:寄与度:マネーストック(M2)(前年同月比):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.21

2000 0.01 -0.35 -0.13 0.58 -0.45 -0.20 0.09 -0.14 0.16 0.08 -0.13 0.09

2001 0.16 0.29 -0.06 -0.13 0.22 0.22 0.08 -0.06 0.20 -0.19 0.07 0.19

2002 0.13 0.00 0.13 -0.14 0.00 -0.07 -0.07 0.07 -0.14 0.07 -0.07 -0.55

2003 -0.18 0.04 -0.11 -0.26 0.24 0.16 0.02 0.10 -0.05 -0.20 0.03 0.03

2004 0.10 0.10 0.03 0.10 0.18 -0.20 0.11 0.10 0.17 -0.06 0.01 0.01

2005 -0.07 -0.08 0.16 -0.15 -0.31 0.16 0.00 0.00 0.32 -0.08 0.08 -0.08

2006 -0.08 -0.07 -0.24 0.17 -0.24 -0.15 -0.46 -0.05 0.12 0.03 0.11 0.12

2007 0.20 0.12 0.12 0.03 0.28 0.35 0.18 -0.15 -0.06 0.18 0.09 0.08

2008 0.00 0.23 -0.09 -0.32 0.15 0.07 -0.08 0.22 -0.15 -0.29 0.00 0.00

2009 -0.11 0.06 0.06 0.29 0.00 -0.13 0.13 0.06 0.13 0.27 -0.08 -0.15

2010 -0.08 -0.23 0.00 0.14 0.14 -0.16 -0.16 0.07 -0.01 -0.01 -0.15 -0.23

2011 0.00 0.07 0.14 0.07 -0.01 0.06 0.05 -0.18 -0.02 0.05 0.13 0.05

2012 -0.10 -0.10 0.06 -0.33 -0.31 0.07 0.00 0.07 0.00 -0.07 -0.14 0.37

2013 0.07 0.15 0.07 0.15 0.23 0.23 -0.10 0.07 -0.02 0.22 0.14 -0.11

2014 0.05 -0.27 -0.42 -0.09 -0.09 -0.24 0.00 0.00 0.00 0.08 0.39 -0.08

2015 -0.16 0.15 0.07 -0.01 0.39 -0.25 0.06 0.14 -0.25 -0.17 -0.24 -0.16

2016 -0.01 -0.01 -0.08 0.22 -0.01 -0.01 -0.01 -0.08 0.14 0.14 0.14 0.07

2017 -0.01 0.14 0.06 -0.25 -0.10 0.06 0.06 -0.02 -0.02 0.06 -0.11 -0.34

2018 -0.17 -0.16 -0.08 0.08 0.00 -0.07 -0.15 0.01 -0.07 -0.06 -0.28 0.10

2019 -0.05 0.02 0.09 0.09 0.08 -0.21 0.01 0.09 0.01

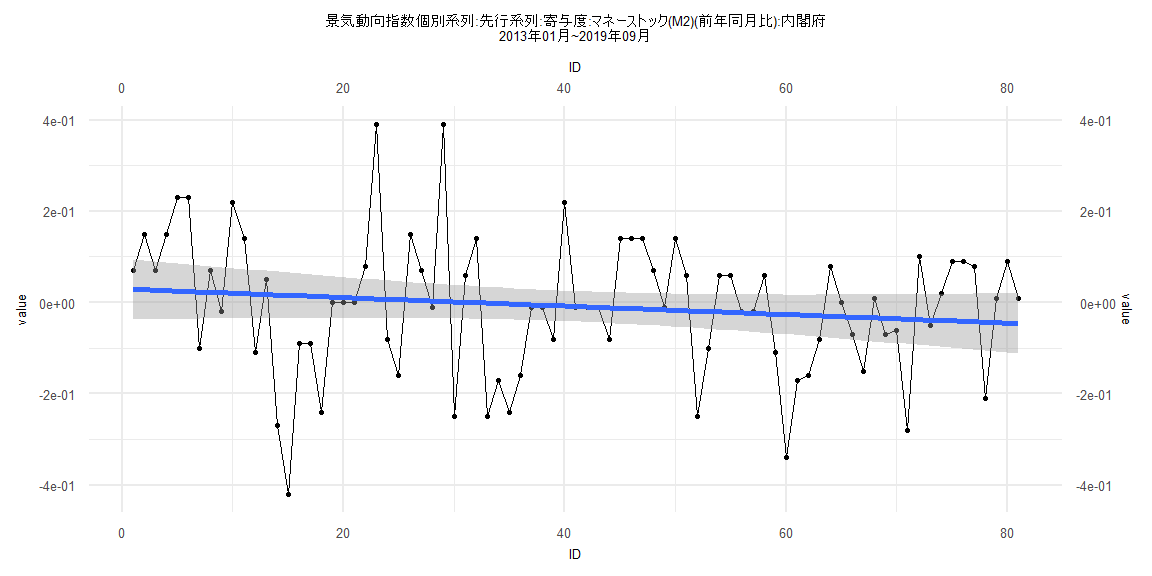

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.31672 -0.10501 0.01178 0.08194 0.37971

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0271525 0.0482569 -0.563 0.577

ID 0.0004474 0.0021028 0.213 0.833

Residual standard error: 0.1478 on 37 degrees of freedom

Multiple R-squared: 0.001222, Adjusted R-squared: -0.02577

F-statistic: 0.04526 on 1 and 37 DF, p-value: 0.8327

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4939, p-value = 0.03625

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.58251, df = 1, p-value = 0.4453

Box-Ljung test

data: lm_residuals

X-squared = 0.50369, df = 1, p-value = 0.4779

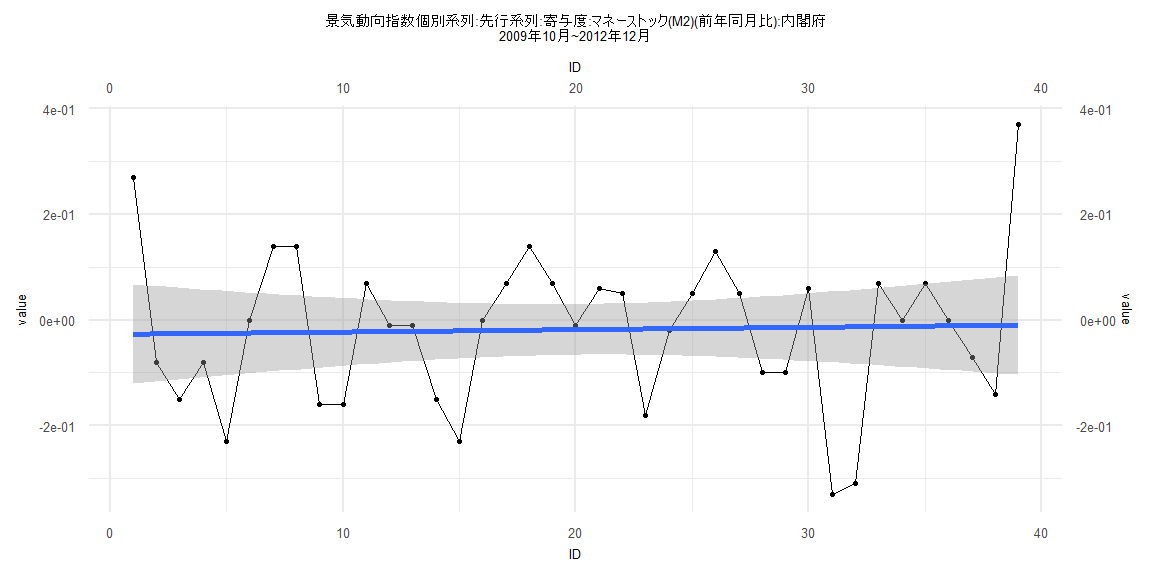

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43572 -0.08733 0.00250 0.10996 0.38733

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0297037 0.0338354 0.878 0.383

ID -0.0009322 0.0007169 -1.300 0.197

Residual standard error: 0.1509 on 79 degrees of freedom

Multiple R-squared: 0.02096, Adjusted R-squared: 0.008565

F-statistic: 1.691 on 1 and 79 DF, p-value: 0.1972

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12346, p-value = 0.5705

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.6142, p-value = 0.03041

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.9248, df = 1, p-value = 0.08723

Box-Ljung test

data: lm_residuals

X-squared = 3.0834, df = 1, p-value = 0.0791

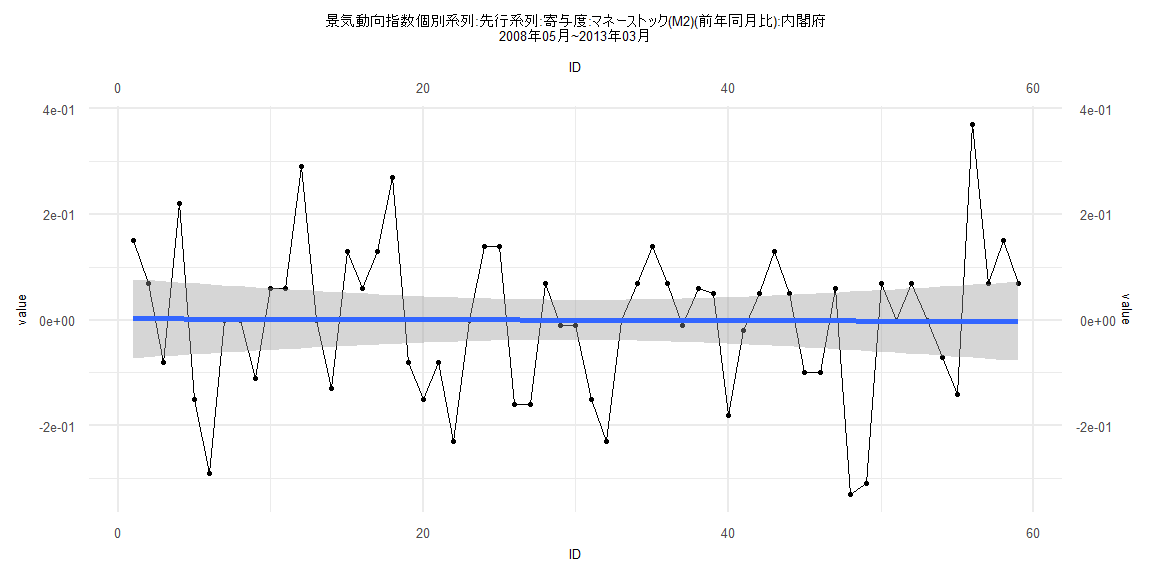

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.32831 -0.09852 0.00195 0.07195 0.37237

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.00237288 0.03827736 0.062 0.951

ID -0.00008475 0.00110961 -0.076 0.939

Residual standard error: 0.1451 on 57 degrees of freedom

Multiple R-squared: 0.0001023, Adjusted R-squared: -0.01744

F-statistic: 0.005833 on 1 and 57 DF, p-value: 0.9394

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.6336, p-value = 0.05886

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.051074, df = 1, p-value = 0.8212

Box-Ljung test

data: lm_residuals

X-squared = 1.834, df = 1, p-value = 0.1757

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.42726 -0.09325 0.00225 0.10268 0.39283

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0159074 0.0349625 0.455 0.650

ID -0.0007208 0.0007690 -0.937 0.352

Residual standard error: 0.1529 on 76 degrees of freedom

Multiple R-squared: 0.01143, Adjusted R-squared: -0.001579

F-statistic: 0.8786 on 1 and 76 DF, p-value: 0.3516

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.316

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.6222, p-value = 0.03531

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.3851, df = 1, p-value = 0.03625

Box-Ljung test

data: lm_residuals

X-squared = 2.7154, df = 1, p-value = 0.09938