Analysis

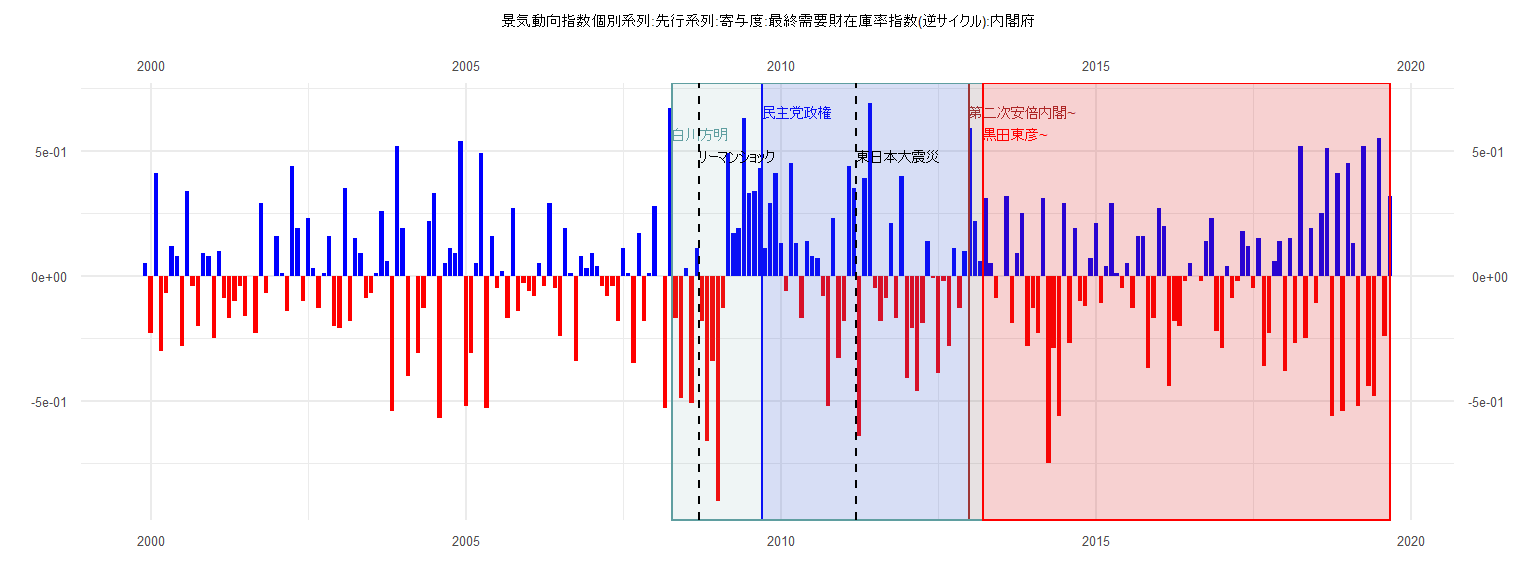

[1] "景気動向指数個別系列:先行系列:寄与度:最終需要財在庫率指数(逆サイクル):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.05

2000 -0.23 0.41 -0.30 -0.07 0.12 0.08 -0.28 0.34 -0.04 -0.20 0.09 0.08

2001 -0.25 0.10 -0.09 -0.17 -0.10 -0.04 -0.16 0.00 -0.23 0.29 -0.07 0.00

2002 0.16 0.01 -0.14 0.44 0.19 -0.10 0.23 0.03 -0.13 0.01 0.16 -0.20

2003 -0.21 0.35 -0.18 0.15 0.09 -0.09 -0.07 0.01 0.26 0.06 -0.54 0.52

2004 0.19 -0.40 0.00 -0.31 -0.13 0.22 0.33 -0.57 0.05 0.11 0.09 0.54

2005 -0.52 -0.31 0.05 0.49 -0.53 0.16 -0.05 0.02 -0.17 0.27 -0.14 -0.03

2006 -0.06 -0.08 0.05 -0.04 0.29 -0.05 -0.24 0.19 0.01 -0.34 0.08 0.03

2007 0.09 0.04 -0.04 -0.08 -0.04 -0.18 0.11 0.01 -0.35 0.17 -0.18 0.01

2008 0.28 0.00 -0.53 0.67 -0.17 -0.49 0.03 -0.51 0.11 -0.18 -0.66 -0.34

2009 -0.90 -0.13 0.49 0.17 0.19 0.63 0.33 0.34 0.43 0.11 0.29 0.41

2010 0.13 -0.06 0.45 0.13 -0.17 0.14 0.08 0.07 -0.08 -0.52 0.23 -0.33

2011 -0.18 0.44 0.35 -0.64 0.39 0.69 -0.05 -0.18 -0.09 0.21 -0.17 0.40

2012 -0.41 -0.21 -0.46 -0.19 0.14 -0.01 -0.39 -0.02 -0.28 0.11 -0.13 0.10

2013 0.59 0.22 0.06 0.31 0.05 -0.09 0.00 0.32 -0.19 0.09 0.25 -0.28

2014 -0.13 -0.23 0.31 -0.75 -0.29 -0.56 0.29 -0.27 0.19 -0.10 -0.12 0.07

2015 0.21 -0.11 0.04 0.29 0.01 -0.05 0.05 -0.13 0.16 0.16 -0.37 -0.17

2016 0.27 0.20 -0.44 -0.18 -0.20 -0.02 0.05 0.00 -0.02 0.14 0.23 -0.22

2017 -0.29 0.04 -0.09 -0.02 0.18 0.12 -0.05 0.15 -0.36 -0.23 0.06 0.14

2018 -0.38 0.15 -0.27 0.52 -0.25 0.19 -0.11 0.25 0.51 -0.56 0.41 -0.54

2019 0.45 0.13 -0.52 0.52 -0.44 -0.48 0.55 -0.24 0.32

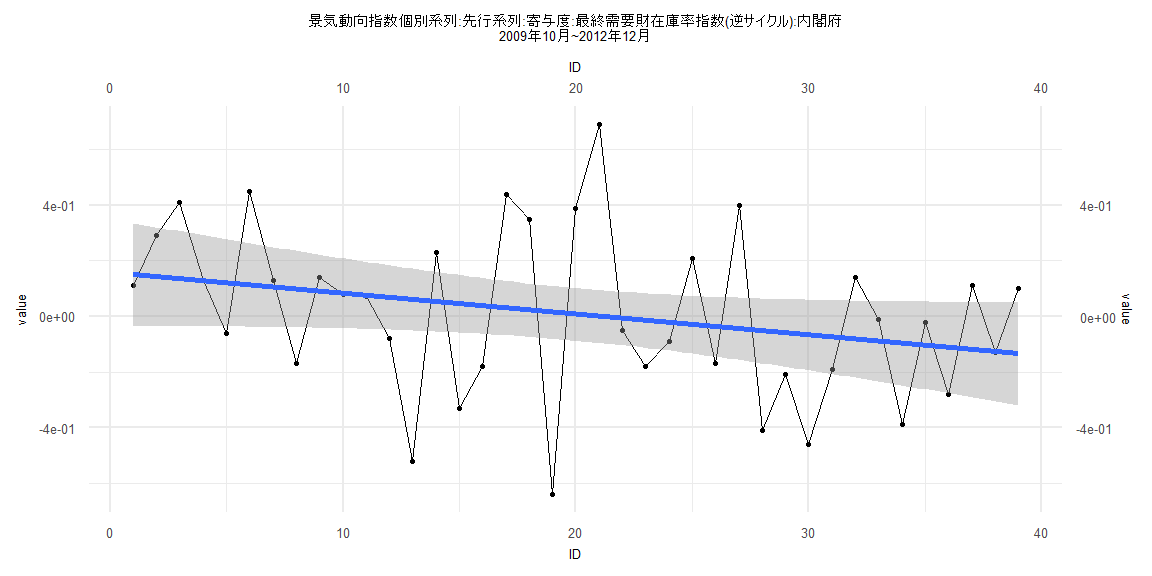

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.65520 -0.16637 -0.00277 0.22618 0.68982

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.157854 0.095023 1.661 0.1051

ID -0.007508 0.004141 -1.813 0.0779 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.291 on 37 degrees of freedom

Multiple R-squared: 0.08161, Adjusted R-squared: 0.05679

F-statistic: 3.288 on 1 and 37 DF, p-value: 0.0779

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.253, p-value = 0.735

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.00073433, df = 1, p-value = 0.9784

Box-Ljung test

data: lm_residuals

X-squared = 0.77346, df = 1, p-value = 0.3791

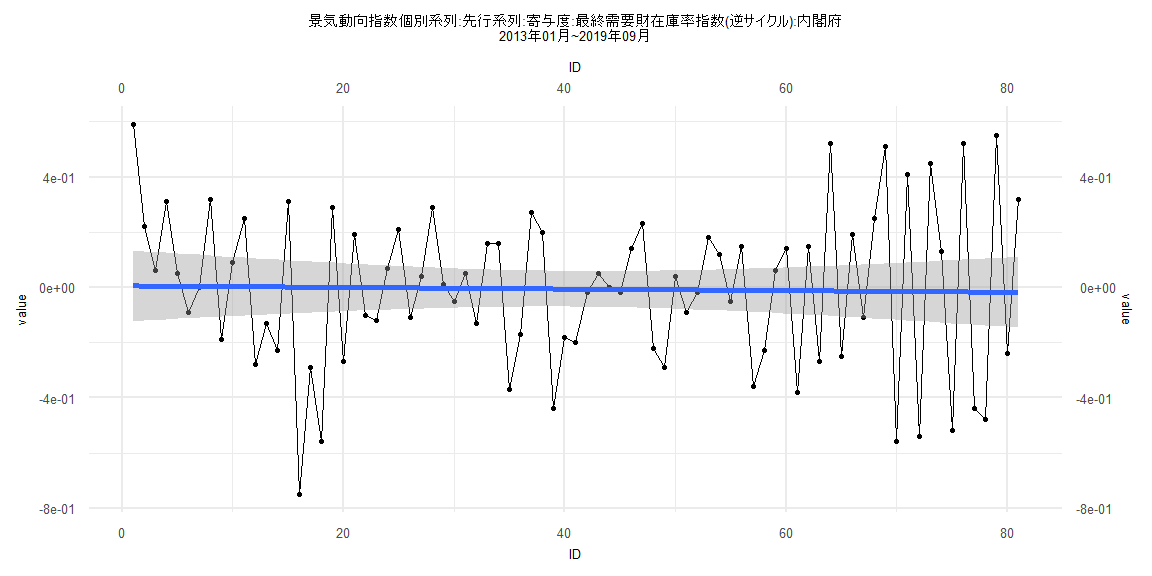

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.7511 -0.2118 0.0127 0.2034 0.5846

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0056975 0.0655884 0.087 0.931

ID -0.0002895 0.0013896 -0.208 0.835

Residual standard error: 0.2924 on 79 degrees of freedom

Multiple R-squared: 0.0005492, Adjusted R-squared: -0.0121

F-statistic: 0.04341 on 1 and 79 DF, p-value: 0.8355

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11111, p-value = 0.7027

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.575, p-value = 0.9944

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.2385, df = 1, p-value = 0.03952

Box-Ljung test

data: lm_residuals

X-squared = 8.6726, df = 1, p-value = 0.00323

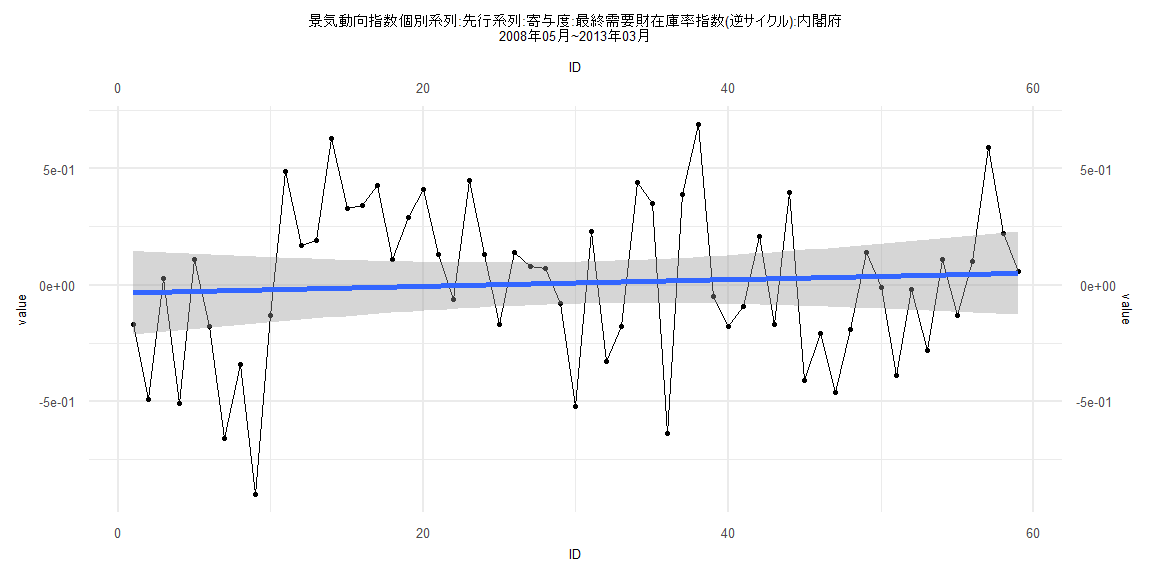

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.87834 -0.20024 0.05384 0.21290 0.66981

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.034646 0.091346 -0.379 0.706

ID 0.001443 0.002648 0.545 0.588

Residual standard error: 0.3464 on 57 degrees of freedom

Multiple R-squared: 0.005183, Adjusted R-squared: -0.01227

F-statistic: 0.297 on 1 and 57 DF, p-value: 0.5879

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5667, p-value = 0.03354

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.1022, df = 1, p-value = 0.1471

Box-Ljung test

data: lm_residuals

X-squared = 2.8758, df = 1, p-value = 0.08992

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.71656 -0.20314 0.02616 0.19293 0.54569

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0412354 0.0659552 -0.625 0.534

ID 0.0005993 0.0014506 0.413 0.681

Residual standard error: 0.2885 on 76 degrees of freedom

Multiple R-squared: 0.00224, Adjusted R-squared: -0.01089

F-statistic: 0.1707 on 1 and 76 DF, p-value: 0.6807

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.7152, p-value = 0.9992

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.7838, df = 1, p-value = 0.009199

Box-Ljung test

data: lm_residuals

X-squared = 11.405, df = 1, p-value = 0.0007326