Analysis

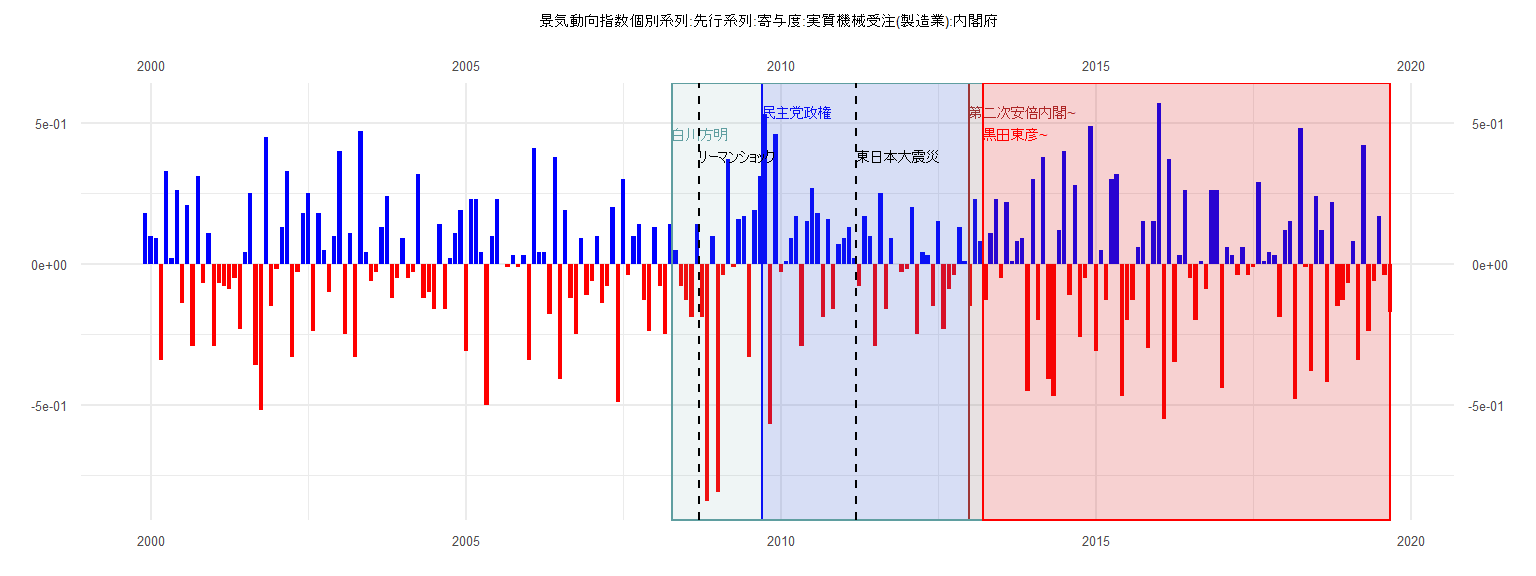

[1] "景気動向指数個別系列:先行系列:寄与度:実質機械受注(製造業):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.18

2000 0.10 0.09 -0.34 0.33 0.02 0.26 -0.14 0.21 -0.29 0.31 -0.07 0.11

2001 -0.29 -0.07 -0.08 -0.09 -0.05 -0.23 0.04 0.25 -0.36 -0.52 0.45 -0.15

2002 -0.02 0.13 0.33 -0.33 -0.03 0.18 0.25 -0.24 0.18 0.05 -0.10 0.10

2003 0.40 -0.25 0.11 -0.33 0.47 0.04 -0.06 -0.03 0.13 0.24 -0.12 -0.05

2004 0.09 -0.05 -0.03 0.32 -0.12 -0.10 -0.16 0.14 -0.16 0.02 0.11 0.19

2005 -0.31 0.23 0.23 0.04 -0.50 0.10 0.23 0.00 -0.01 0.03 -0.01 0.03

2006 -0.34 0.41 0.04 0.04 -0.18 0.38 -0.41 0.19 -0.12 -0.25 0.09 -0.11

2007 -0.06 0.10 -0.14 -0.08 0.20 -0.49 0.30 -0.04 0.10 0.14 -0.13 -0.24

2008 0.13 -0.08 -0.25 0.14 0.05 -0.08 -0.13 -0.19 0.14 -0.19 -0.84 0.10

2009 -0.81 -0.04 0.37 -0.01 0.16 0.17 -0.33 0.19 0.31 0.53 -0.57 0.46

2010 -0.03 0.01 0.09 0.17 -0.29 0.15 0.27 0.18 -0.19 0.16 -0.16 0.07

2011 0.09 0.13 0.02 -0.08 0.17 0.10 -0.29 0.25 -0.16 0.09 0.00 -0.03

2012 -0.02 0.20 -0.25 0.04 0.03 -0.15 0.15 -0.23 -0.09 -0.04 0.13 0.01

2013 -0.15 0.23 0.08 -0.13 0.11 0.23 -0.05 0.22 0.01 0.08 0.09 -0.45

2014 0.30 -0.20 0.38 -0.41 -0.47 0.12 0.40 -0.11 0.28 -0.26 -0.05 0.49

2015 -0.31 0.05 -0.13 0.30 0.32 -0.47 -0.20 -0.13 0.06 0.15 -0.30 0.15

2016 0.57 -0.55 0.37 -0.35 0.03 0.26 -0.05 -0.20 0.01 -0.09 0.26 0.26

2017 -0.44 0.06 0.03 -0.04 0.06 -0.04 -0.01 0.29 0.01 0.04 0.03 -0.19

2018 0.12 0.15 -0.48 0.48 -0.01 -0.38 0.24 0.12 -0.42 0.22 -0.15 -0.13

2019 -0.07 0.08 -0.34 0.42 -0.24 -0.06 0.17 -0.04 -0.17

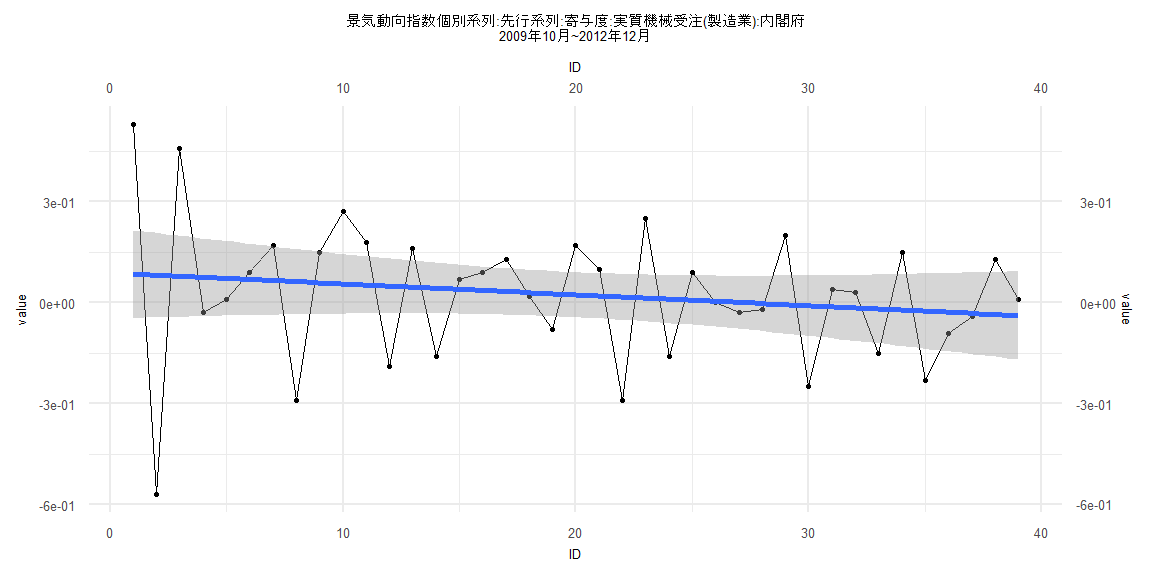

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.65204 -0.10619 0.03018 0.10894 0.44472

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.088529 0.067208 1.317 0.196

ID -0.003247 0.002929 -1.109 0.275

Residual standard error: 0.2058 on 37 degrees of freedom

Multiple R-squared: 0.03215, Adjusted R-squared: 0.005997

F-statistic: 1.229 on 1 and 37 DF, p-value: 0.2747

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.9885

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 3.0665, p-value = 0.9997

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.818, df = 1, p-value = 0.009025

Box-Ljung test

data: lm_residuals

X-squared = 15, df = 1, p-value = 0.0001075

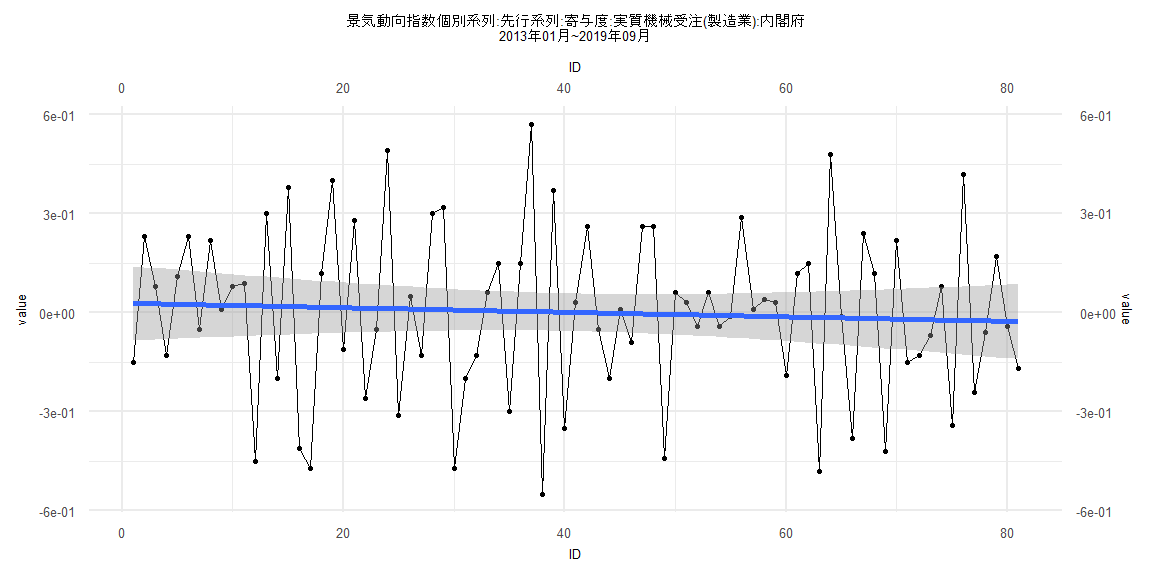

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.5528 -0.1563 0.0203 0.1955 0.5665

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0290278 0.0577919 0.502 0.617

ID -0.0006899 0.0012245 -0.563 0.575

Residual standard error: 0.2577 on 79 degrees of freedom

Multiple R-squared: 0.004003, Adjusted R-squared: -0.008605

F-statistic: 0.3175 on 1 and 79 DF, p-value: 0.5747

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14815, p-value = 0.338

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.8258, p-value = 0.9999

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.27838, df = 1, p-value = 0.5978

Box-Ljung test

data: lm_residuals

X-squared = 14.675, df = 1, p-value = 0.0001277

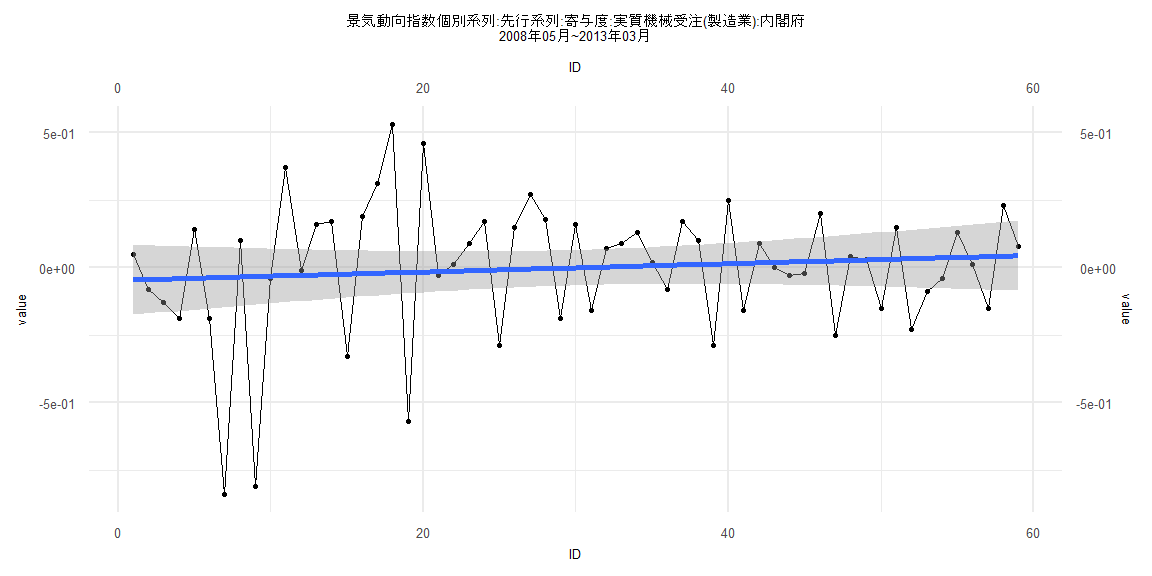

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.80379 -0.13685 0.01853 0.16047 0.54930

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.046978 0.066334 -0.708 0.482

ID 0.001538 0.001923 0.800 0.427

Residual standard error: 0.2515 on 57 degrees of freedom

Multiple R-squared: 0.01109, Adjusted R-squared: -0.006255

F-statistic: 0.6395 on 1 and 57 DF, p-value: 0.4272

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.18644, p-value = 0.2582

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.4666, p-value = 0.9545

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.9013, df = 1, p-value = 0.01513

Box-Ljung test

data: lm_residuals

X-squared = 3.4197, df = 1, p-value = 0.06442

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.55149 -0.15059 0.01653 0.18618 0.56789

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0230836 0.0596295 0.387 0.700

ID -0.0006169 0.0013115 -0.470 0.639

Residual standard error: 0.2608 on 76 degrees of freedom

Multiple R-squared: 0.002902, Adjusted R-squared: -0.01022

F-statistic: 0.2212 on 1 and 76 DF, p-value: 0.6395

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.8264, p-value = 0.9999

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.72088, df = 1, p-value = 0.3959

Box-Ljung test

data: lm_residuals

X-squared = 14.126, df = 1, p-value = 0.000171