Analysis

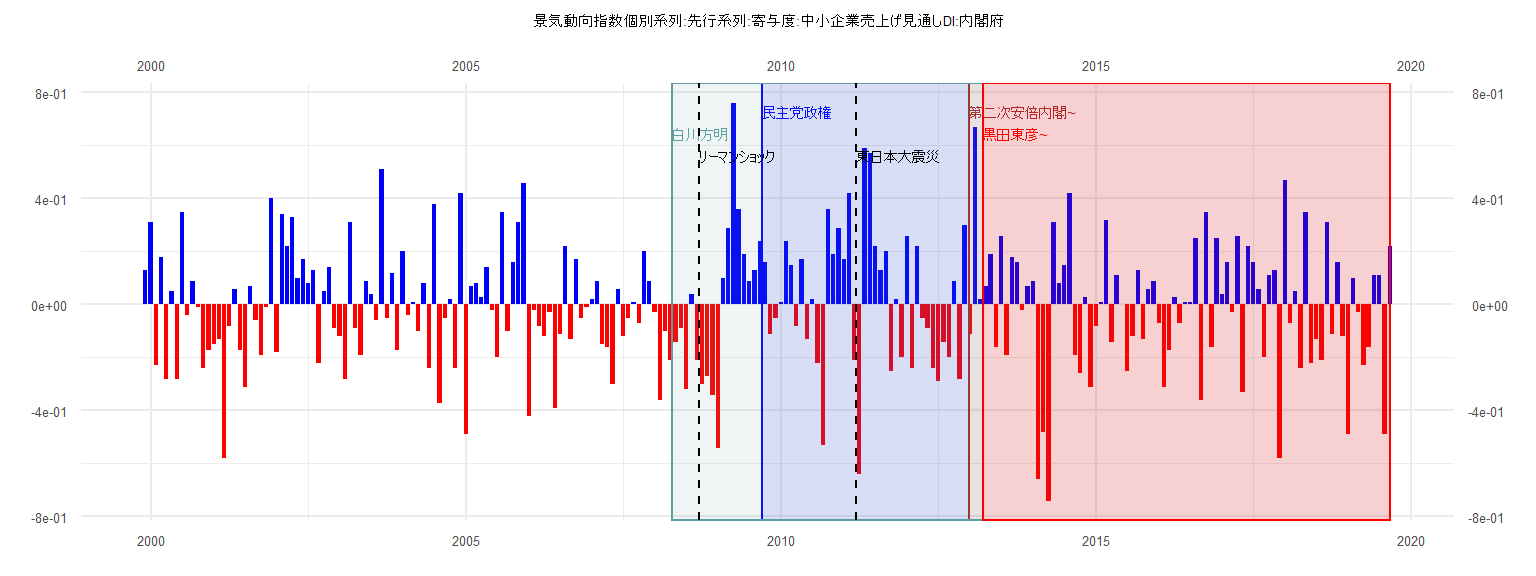

[1] "景気動向指数個別系列:先行系列:寄与度:中小企業売上げ見通しDI:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.13

2000 0.31 -0.23 0.18 -0.28 0.05 -0.28 0.35 -0.04 0.09 -0.01 -0.24 -0.17

2001 -0.15 -0.13 -0.58 -0.08 0.06 -0.17 -0.31 0.07 -0.06 -0.19 -0.01 0.40

2002 -0.18 0.34 0.22 0.33 0.10 0.17 0.08 0.13 -0.22 0.05 0.14 -0.09

2003 -0.12 -0.28 0.31 -0.09 -0.19 0.09 0.04 -0.06 0.51 -0.05 0.12 -0.17

2004 0.20 -0.04 0.01 -0.10 0.08 -0.24 0.38 -0.37 -0.05 0.02 -0.24 0.42

2005 -0.49 0.07 0.08 0.03 0.14 -0.02 -0.20 0.35 -0.10 0.16 0.31 0.46

2006 -0.42 -0.02 -0.08 -0.12 -0.03 -0.39 -0.11 0.22 -0.13 0.17 -0.05 -0.01

2007 0.02 0.09 -0.15 -0.16 -0.30 0.06 -0.12 -0.05 0.01 -0.07 0.20 0.09

2008 -0.03 -0.36 -0.10 -0.21 -0.14 -0.09 -0.32 0.04 -0.21 -0.30 -0.27 -0.34

2009 -0.54 0.10 0.29 0.76 0.36 0.19 0.09 0.13 0.24 0.16 -0.11 -0.05

2010 0.01 0.24 0.15 -0.08 0.17 -0.13 0.02 -0.22 -0.53 0.36 0.19 0.29

2011 0.17 0.42 -0.21 -0.64 0.59 0.57 0.22 0.13 0.20 -0.25 0.02 -0.20

2012 0.26 -0.24 0.22 -0.05 -0.09 -0.24 -0.29 -0.14 -0.20 0.09 -0.28 0.30

2013 -0.11 0.67 0.02 0.07 0.19 -0.16 0.26 -0.19 0.18 0.16 -0.02 0.07

2014 0.09 -0.66 -0.48 -0.74 0.31 0.08 0.15 0.42 -0.19 -0.26 0.03 -0.31

2015 -0.08 0.01 0.32 -0.14 0.11 0.00 -0.25 -0.12 0.13 -0.13 0.06 0.09

2016 -0.07 -0.31 -0.17 0.03 -0.07 0.01 0.01 0.25 -0.36 0.35 -0.16 0.25

2017 0.04 0.16 -0.03 0.26 -0.33 0.22 0.16 0.06 -0.20 0.11 0.13 -0.58

2018 0.47 -0.07 0.05 -0.24 0.35 -0.22 -0.13 -0.21 0.31 -0.11 0.16 -0.12

2019 -0.49 0.10 -0.03 -0.23 -0.16 0.11 0.11 -0.49 0.22

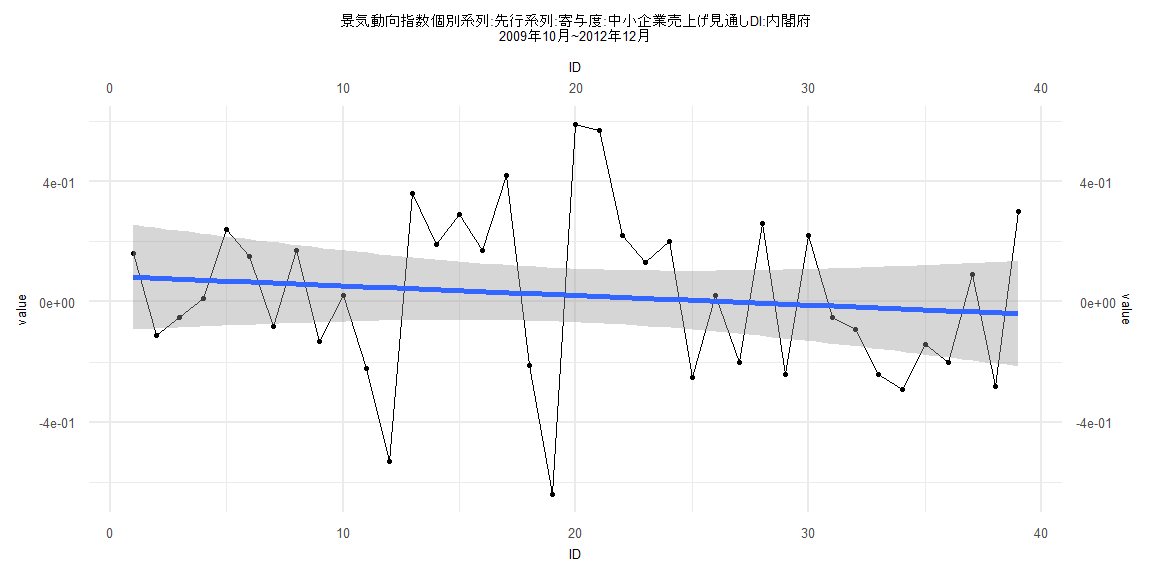

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.66447 -0.19381 -0.03314 0.18119 0.56872

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.085007 0.089605 0.949 0.349

ID -0.003186 0.003904 -0.816 0.420

Residual standard error: 0.2744 on 37 degrees of freedom

Multiple R-squared: 0.01768, Adjusted R-squared: -0.008869

F-statistic: 0.6659 on 1 and 37 DF, p-value: 0.4197

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.9173, p-value = 0.3324

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.008385, df = 1, p-value = 0.927

Box-Ljung test

data: lm_residuals

X-squared = 0.016181, df = 1, p-value = 0.8988

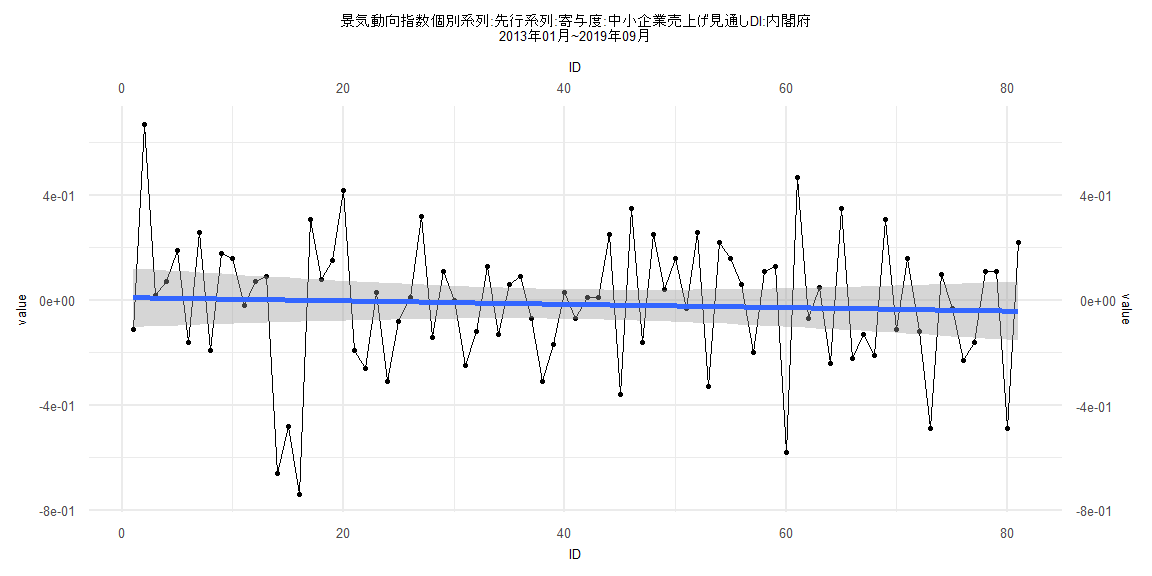

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.74028 -0.15548 0.02645 0.15586 0.66071

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0105772 0.0574214 0.184 0.854

ID -0.0006434 0.0012166 -0.529 0.598

Residual standard error: 0.256 on 79 degrees of freedom

Multiple R-squared: 0.003528, Adjusted R-squared: -0.009086

F-statistic: 0.2797 on 1 and 79 DF, p-value: 0.5984

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3533, p-value = 0.9323

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.87395, df = 1, p-value = 0.3499

Box-Ljung test

data: lm_residuals

X-squared = 2.8646, df = 1, p-value = 0.09055

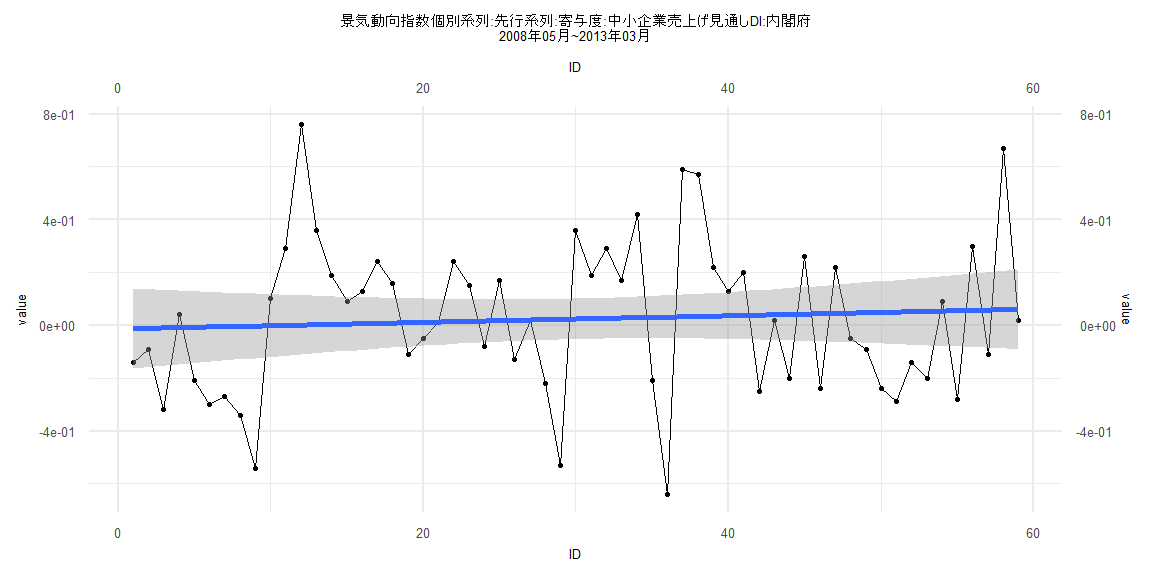

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.67125 -0.24061 -0.00244 0.17997 0.75885

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.013898 0.077492 -0.179 0.858

ID 0.001254 0.002246 0.558 0.579

Residual standard error: 0.2938 on 57 degrees of freedom

Multiple R-squared: 0.005439, Adjusted R-squared: -0.01201

F-statistic: 0.3117 on 1 and 57 DF, p-value: 0.5788

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.57, p-value = 0.03456

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.012466, df = 1, p-value = 0.9111

Box-Ljung test

data: lm_residuals

X-squared = 2.8197, df = 1, p-value = 0.09311

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.71831 -0.14461 0.03385 0.16775 0.49535

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.02063936 0.05692255 -0.363 0.718

ID -0.00008118 0.00125198 -0.065 0.948

Residual standard error: 0.249 on 76 degrees of freedom

Multiple R-squared: 5.532e-05, Adjusted R-squared: -0.0131

F-statistic: 0.004205 on 1 and 76 DF, p-value: 0.9485

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16667, p-value = 0.2297

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3673, p-value = 0.9363

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.23457, df = 1, p-value = 0.6282

Box-Ljung test

data: lm_residuals

X-squared = 2.9567, df = 1, p-value = 0.08552