Analysis

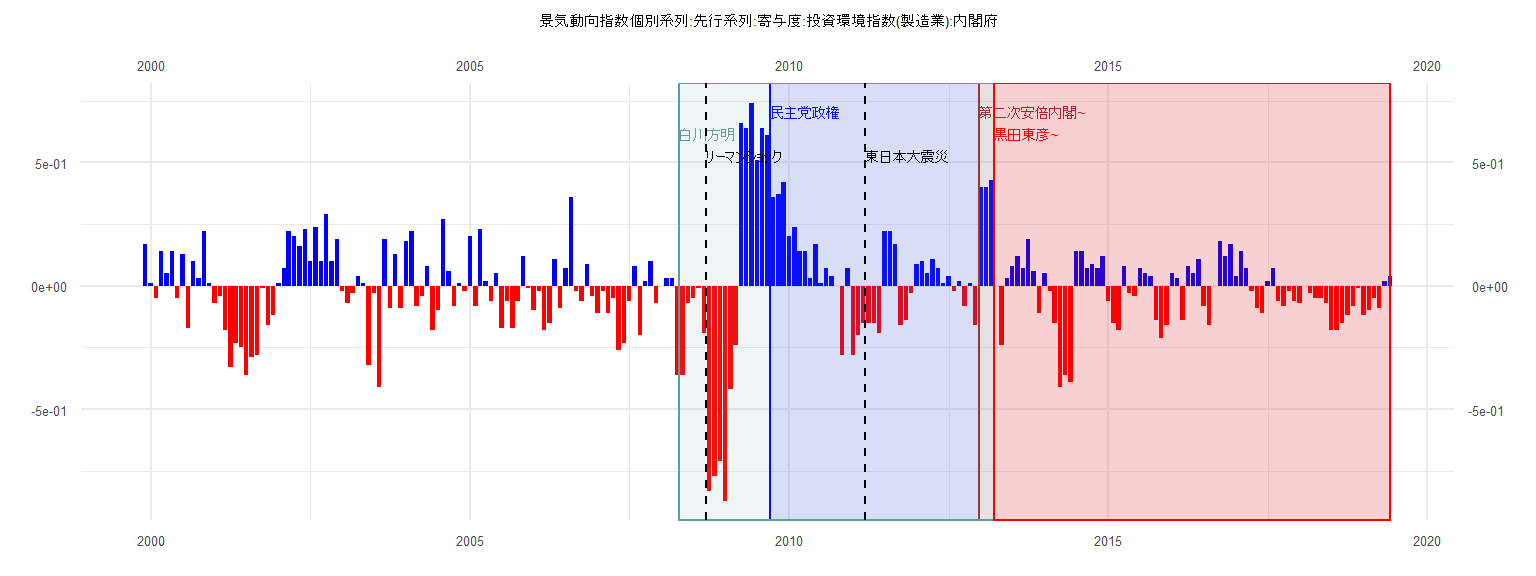

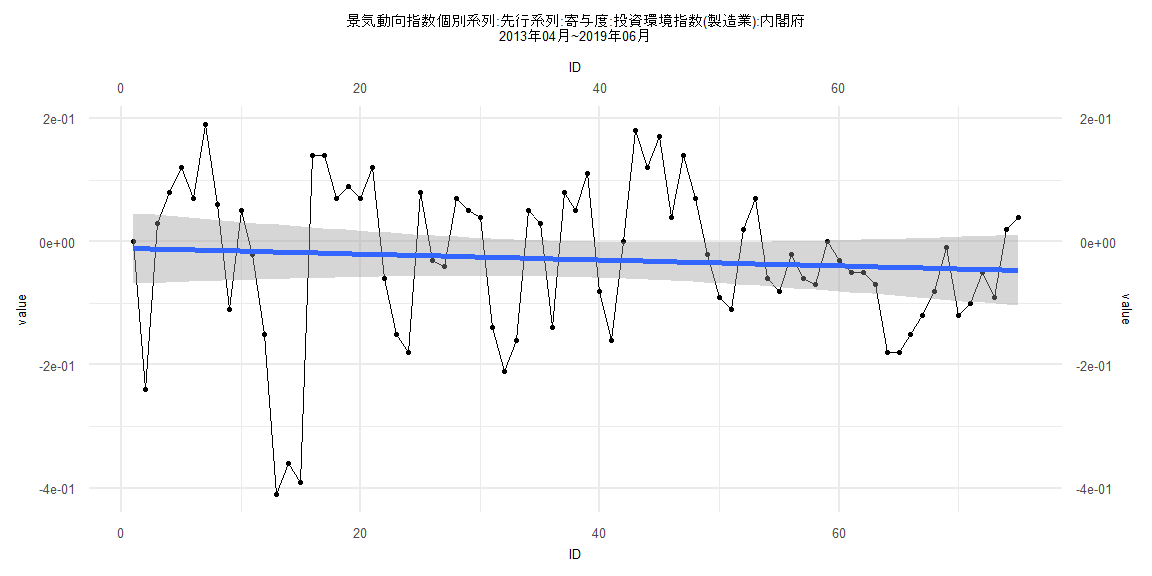

[1] "景気動向指数個別系列:先行系列:寄与度:投資環境指数(製造業):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.17

2000 0.01 -0.05 0.14 0.05 0.14 -0.05 0.13 -0.17 0.10 0.03 0.22 0.01

2001 -0.07 -0.04 -0.18 -0.33 -0.23 -0.25 -0.36 -0.29 -0.28 -0.01 -0.16 -0.12

2002 0.01 0.07 0.22 0.20 0.16 0.23 0.10 0.24 0.10 0.29 0.10 0.19

2003 -0.02 -0.07 -0.03 0.04 0.01 -0.32 -0.03 -0.41 0.19 -0.09 0.13 -0.09

2004 0.18 0.22 -0.08 -0.04 0.08 -0.18 -0.10 0.27 0.06 -0.08 0.01 -0.02

2005 0.20 -0.08 0.23 0.02 -0.06 0.05 -0.17 -0.06 -0.17 -0.06 0.12 -0.01

2006 -0.10 -0.02 -0.18 -0.15 0.11 -0.09 0.07 0.36 -0.02 -0.06 0.09 -0.04

2007 -0.11 -0.02 -0.11 -0.05 -0.26 -0.23 -0.06 0.08 -0.20 0.02 0.10 -0.07

2008 0.00 0.03 0.03 -0.36 -0.36 -0.07 -0.05 -0.01 -0.19 -0.83 -0.77 -0.71

2009 -0.87 -0.42 -0.24 0.66 0.64 0.74 0.51 0.64 0.61 0.36 0.37 0.42

2010 0.20 0.24 0.14 0.14 0.03 0.17 0.01 0.07 0.04 0.00 -0.28 0.07

2011 -0.28 -0.20 -0.15 -0.15 -0.15 -0.19 0.22 0.22 0.17 -0.16 -0.14 -0.03

2012 0.09 0.10 0.05 0.11 0.07 0.01 0.04 -0.02 0.02 -0.08 0.01 -0.16

2013 0.40 0.40 0.43 0.00 -0.24 0.03 0.08 0.12 0.07 0.19 0.06 -0.11

2014 0.05 -0.02 -0.15 -0.41 -0.36 -0.39 0.14 0.14 0.07 0.09 0.07 0.12

2015 -0.06 -0.15 -0.18 0.08 -0.03 -0.04 0.07 0.05 0.04 -0.14 -0.21 -0.16

2016 0.05 0.03 -0.14 0.08 0.05 0.11 -0.08 -0.16 0.00 0.18 0.12 0.17

2017 0.04 0.14 0.07 -0.02 -0.09 -0.11 0.02 0.07 -0.06 -0.08 -0.02 -0.06

2018 -0.07 0.00 -0.03 -0.05 -0.05 -0.07 -0.18 -0.18 -0.15 -0.12 -0.08 -0.01

2019 -0.12 -0.10 -0.05 -0.09 0.02 0.04

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.35255 -0.08352 0.02409 0.10656 0.27931

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.159271 0.051683 3.082 0.00387 **

ID -0.006194 0.002252 -2.751 0.00915 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1583 on 37 degrees of freedom

Multiple R-squared: 0.1698, Adjusted R-squared: 0.1473

F-statistic: 7.565 on 1 and 37 DF, p-value: 0.009154

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.9885

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.89083, p-value = 0.00003079

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.5161, df = 1, p-value = 0.1127

Box-Ljung test

data: lm_residuals

X-squared = 11.741, df = 1, p-value = 0.0006112

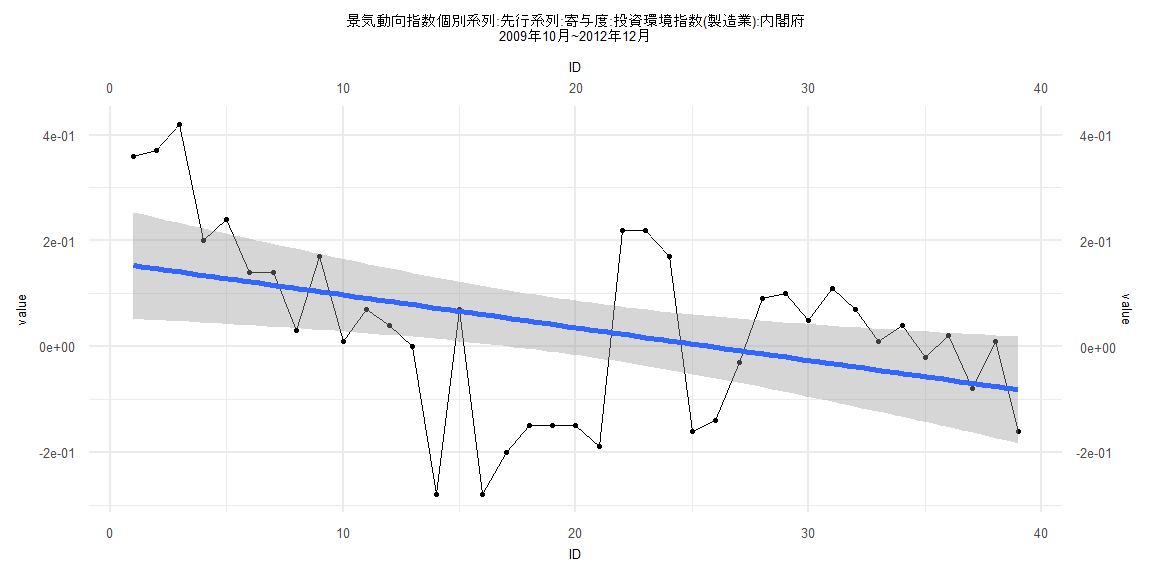

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43746 -0.05658 0.01933 0.07141 0.38075

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0542757 0.0332771 1.631 0.1070

ID -0.0016759 0.0007319 -2.290 0.0248 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1455 on 76 degrees of freedom

Multiple R-squared: 0.06454, Adjusted R-squared: 0.05223

F-statistic: 5.243 on 1 and 76 DF, p-value: 0.02481

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.83206, p-value = 0.000000002444

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 13.681, df = 1, p-value = 0.0002167

Box-Ljung test

data: lm_residuals

X-squared = 23.83, df = 1, p-value = 0.000001052

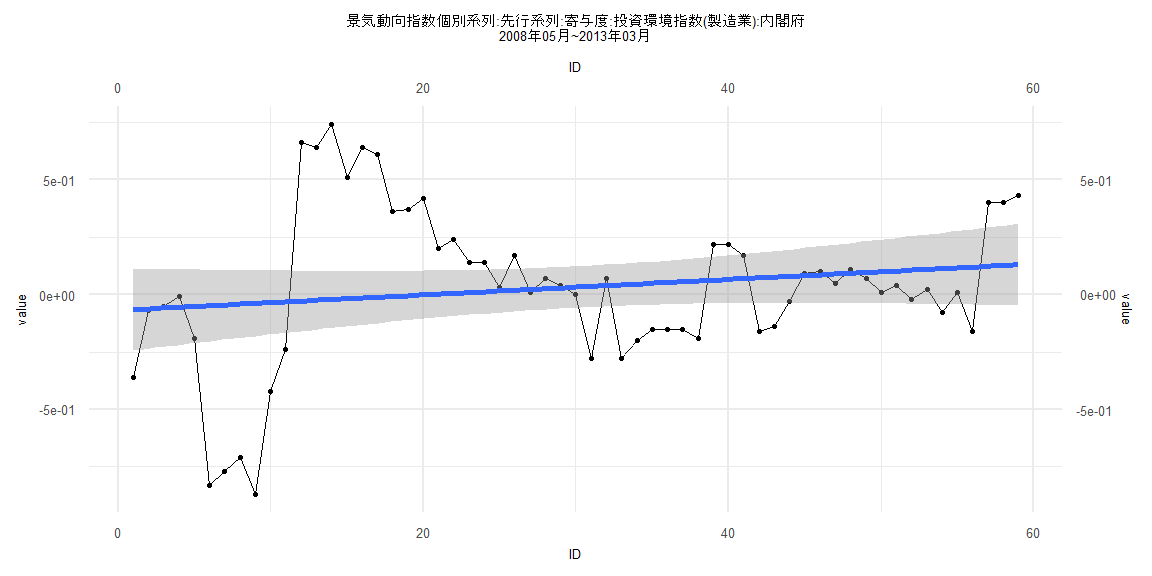

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.83130 -0.20393 -0.00772 0.15597 0.76186

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.069012 0.091091 -0.758 0.452

ID 0.003368 0.002641 1.276 0.207

Residual standard error: 0.3454 on 57 degrees of freedom

Multiple R-squared: 0.02775, Adjusted R-squared: 0.0107

F-statistic: 1.627 on 1 and 57 DF, p-value: 0.2073

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.18644, p-value = 0.2582

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.42499, p-value = 0.0000000000000041

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 14.758, df = 1, p-value = 0.0001222

Box-Ljung test

data: lm_residuals

X-squared = 37.222, df = 1, p-value = 0.000000001054

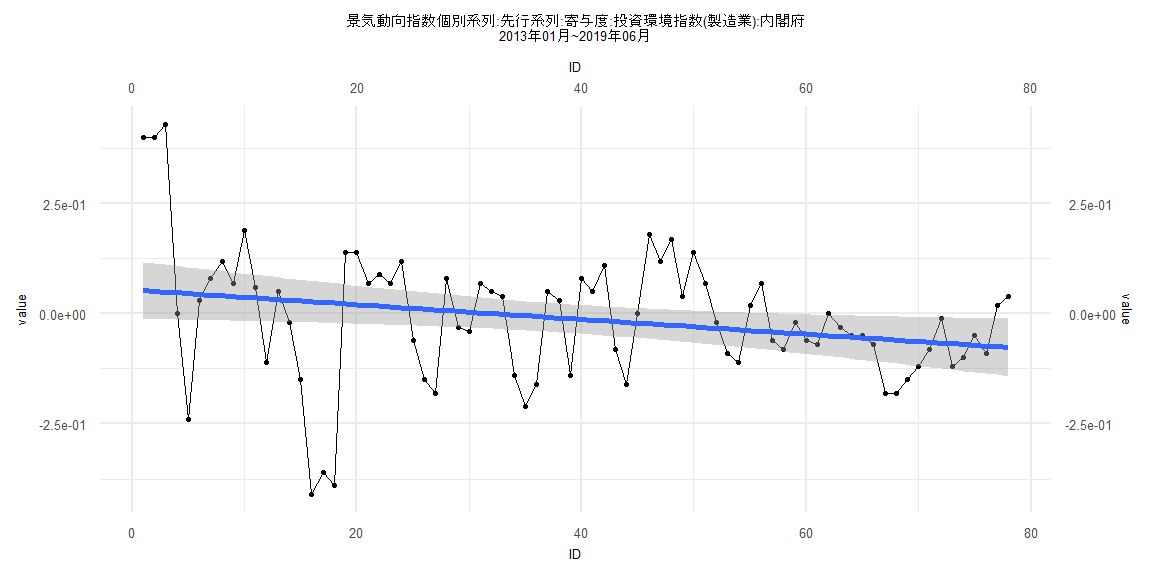

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.39324 -0.06518 0.01098 0.08789 0.21121

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0104973 0.0293626 -0.358 0.722

ID -0.0004817 0.0006714 -0.717 0.475

Residual standard error: 0.1259 on 73 degrees of freedom

Multiple R-squared: 0.007001, Adjusted R-squared: -0.006602

F-statistic: 0.5147 on 1 and 73 DF, p-value: 0.4754

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14667, p-value = 0.3974

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.99829, p-value = 0.0000007995

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 8.002, df = 1, p-value = 0.004673

Box-Ljung test

data: lm_residuals

X-squared = 19.32, df = 1, p-value = 0.00001105