Analysis

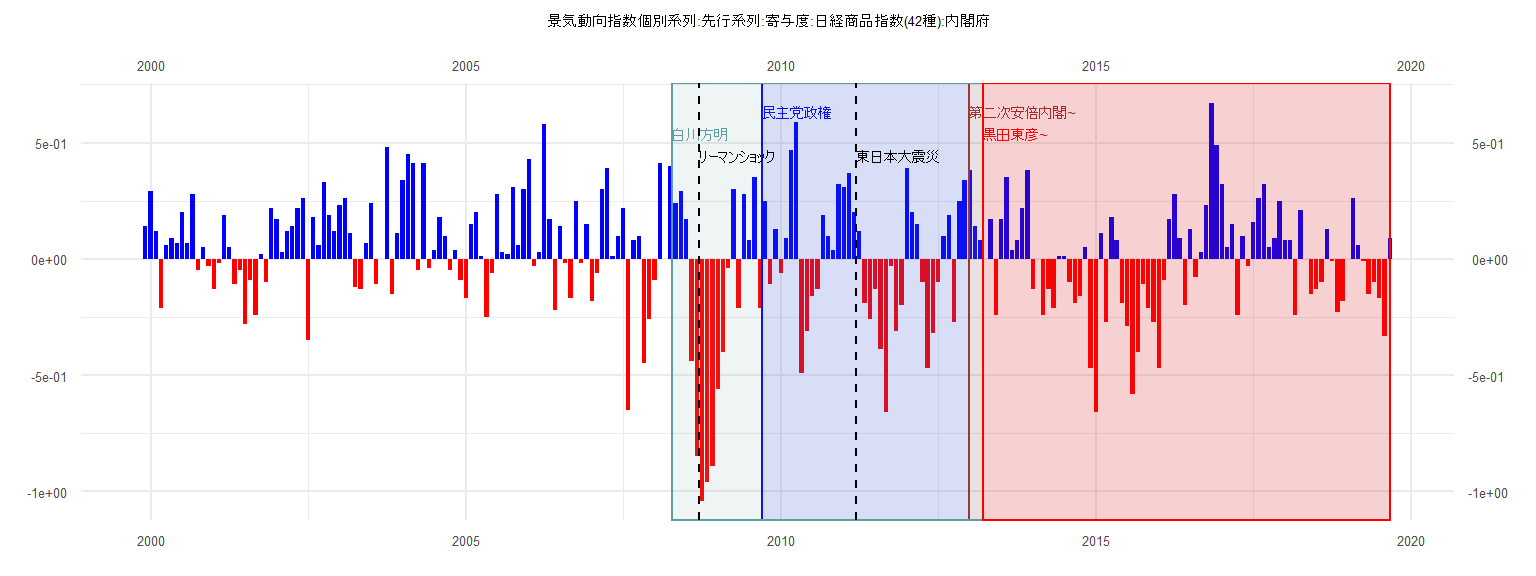

[1] "景気動向指数個別系列:先行系列:寄与度:日経商品指数(42種):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 0.14

2000 0.29 0.12 -0.21 0.06 0.09 0.07 0.20 0.07 0.28 -0.05 0.05 -0.03

2001 -0.13 -0.02 0.19 0.05 -0.11 -0.05 -0.28 -0.09 -0.24 0.02 -0.10 0.22

2002 0.17 0.03 0.12 0.14 0.22 0.26 -0.35 0.18 0.06 0.33 0.19 0.12

2003 0.23 0.26 0.11 -0.12 -0.13 0.07 0.24 -0.11 0.00 0.48 -0.15 0.11

2004 0.34 0.45 0.41 -0.05 0.41 -0.04 0.04 0.18 0.10 -0.05 0.04 -0.09

2005 -0.17 0.15 0.20 0.01 -0.25 -0.06 0.28 0.03 0.02 0.31 0.06 0.30

2006 0.43 -0.03 0.03 0.58 0.17 -0.22 0.14 -0.02 -0.17 0.25 -0.02 0.15

2007 -0.18 -0.06 0.30 0.39 0.01 0.10 0.22 -0.65 0.08 0.10 -0.45 -0.26

2008 -0.09 0.41 0.00 0.40 0.24 0.29 0.17 -0.44 -0.85 -1.04 -0.96 -0.89

2009 -0.56 -0.40 -0.04 0.30 -0.21 0.28 0.08 0.35 -0.21 0.25 -0.11 0.13

2010 -0.06 0.09 0.47 0.59 -0.49 -0.31 -0.16 -0.13 0.19 0.10 0.04 0.32

2011 0.31 0.37 0.20 0.12 -0.19 -0.26 -0.13 -0.39 -0.66 -0.03 -0.31 -0.20

2012 0.39 0.20 0.15 -0.10 -0.47 -0.32 -0.10 0.10 0.19 -0.27 0.25 0.34

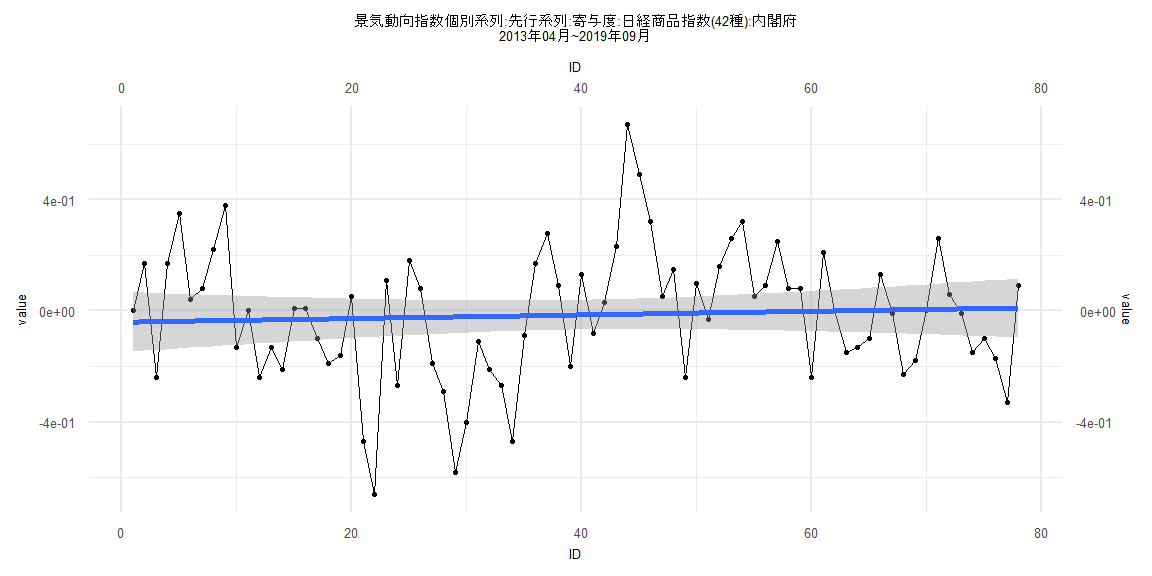

2013 0.38 0.14 0.08 0.00 0.17 -0.24 0.17 0.35 0.04 0.08 0.22 0.38

2014 -0.13 0.00 -0.24 -0.13 -0.21 0.01 0.01 -0.10 -0.19 -0.16 0.05 -0.47

2015 -0.66 0.11 -0.27 0.18 0.08 -0.19 -0.29 -0.58 -0.40 -0.11 -0.21 -0.27

2016 -0.47 -0.09 0.17 0.28 0.09 -0.20 0.13 -0.08 0.03 0.23 0.67 0.49

2017 0.32 0.05 0.15 -0.24 0.10 -0.03 0.16 0.26 0.32 0.05 0.09 0.25

2018 0.08 0.08 -0.24 0.21 0.00 -0.15 -0.13 -0.10 0.13 -0.01 -0.23 -0.18

2019 0.00 0.26 0.06 -0.01 -0.15 -0.10 -0.17 -0.33 0.09

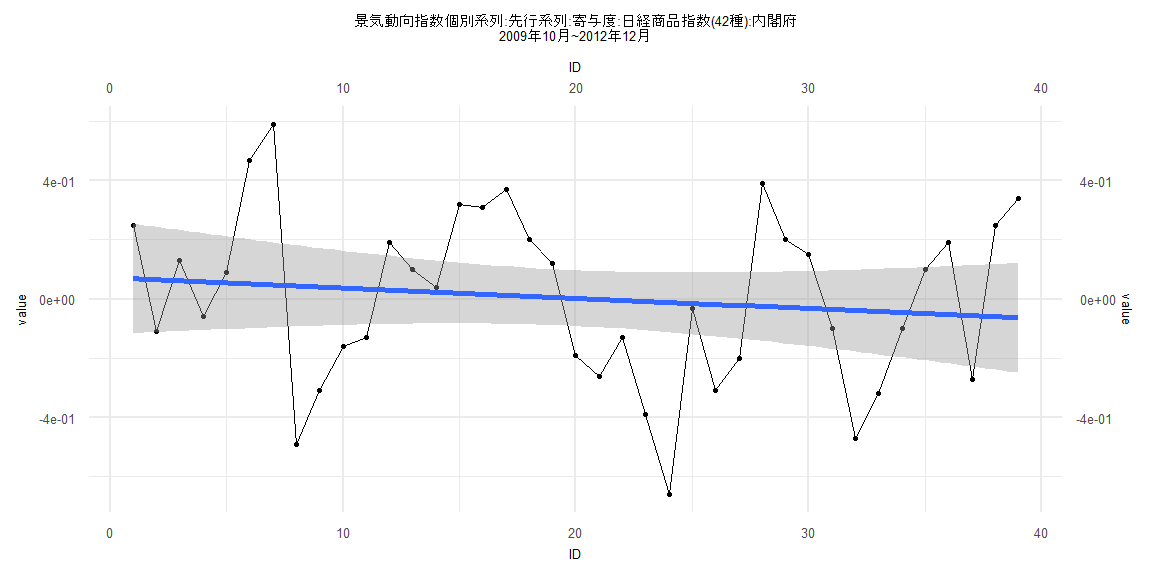

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.64889 -0.19523 0.01629 0.20937 0.54192

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.072456 0.094945 0.763 0.450

ID -0.003482 0.004137 -0.842 0.405

Residual standard error: 0.2908 on 37 degrees of freedom

Multiple R-squared: 0.01878, Adjusted R-squared: -0.007737

F-statistic: 0.7083 on 1 and 37 DF, p-value: 0.4054

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.2148, p-value = 0.00292

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0097755, df = 1, p-value = 0.9212

Box-Ljung test

data: lm_residuals

X-squared = 5.4954, df = 1, p-value = 0.01907

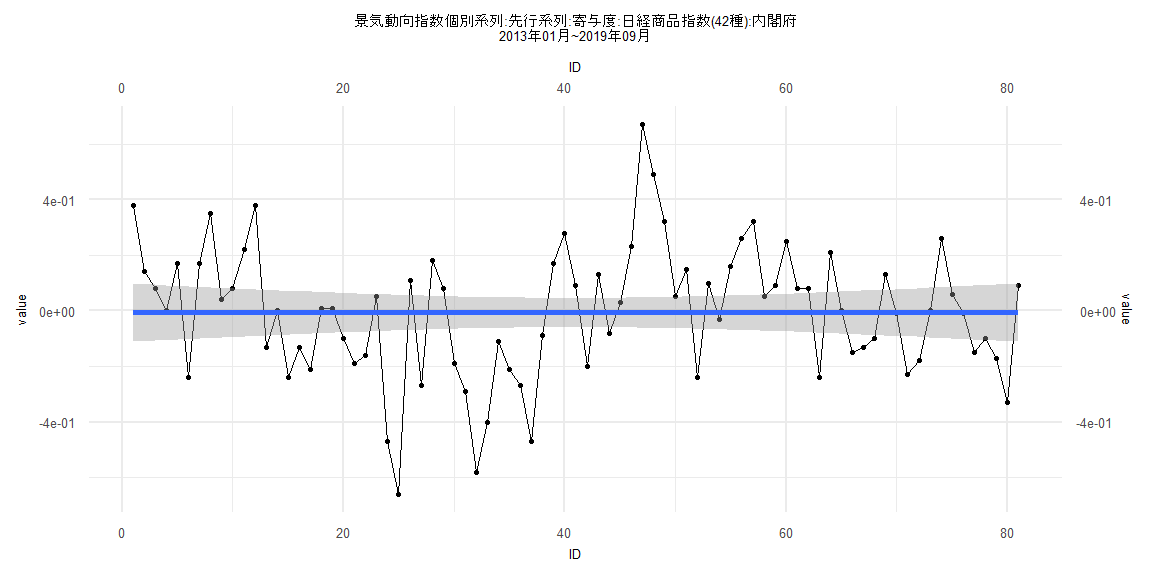

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.65296 -0.16338 0.01708 0.14721 0.67687

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.007228395 0.053366013 -0.135 0.893

ID 0.000007678 0.001130680 0.007 0.995

Residual standard error: 0.2379 on 79 degrees of freedom

Multiple R-squared: 5.838e-07, Adjusted R-squared: -0.01266

F-statistic: 4.612e-05 on 1 and 79 DF, p-value: 0.9946

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17284, p-value = 0.1783

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0932, p-value = 0.000004238

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.0238, df = 1, p-value = 0.3116

Box-Ljung test

data: lm_residuals

X-squared = 15.947, df = 1, p-value = 0.00006513

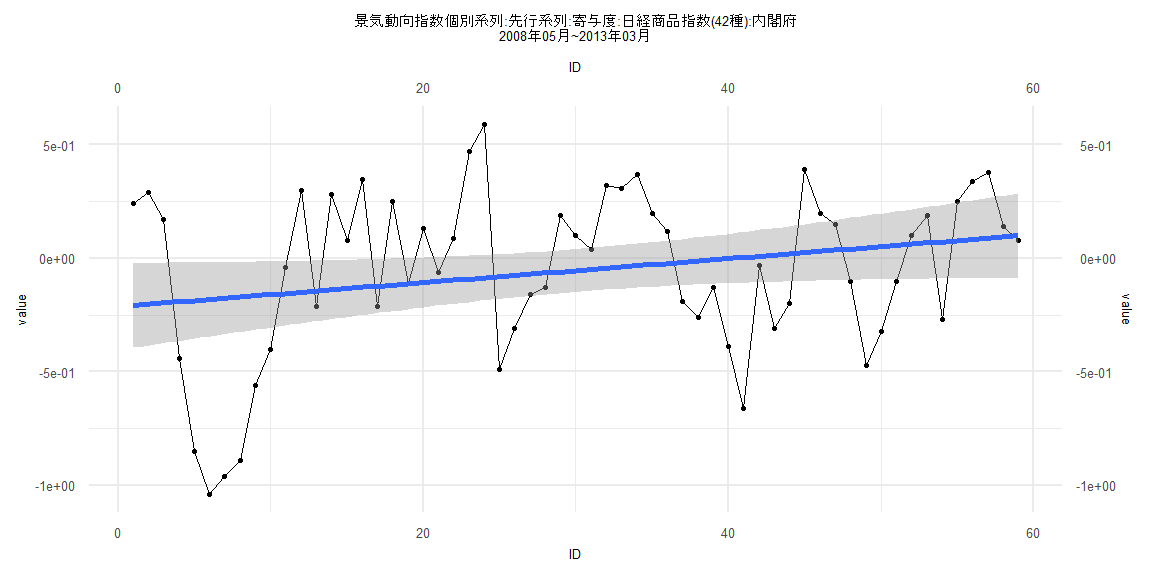

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.85909 -0.23759 0.04153 0.25275 0.67565

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.212665 0.095351 -2.230 0.0297 *

ID 0.005292 0.002764 1.915 0.0606 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3616 on 57 degrees of freedom

Multiple R-squared: 0.06043, Adjusted R-squared: 0.04394

F-statistic: 3.666 on 1 and 57 DF, p-value: 0.06056

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.13559, p-value = 0.6544

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.80362, p-value = 0.00000006211

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 9.7424, df = 1, p-value = 0.001801

Box-Ljung test

data: lm_residuals

X-squared = 21.216, df = 1, p-value = 0.000004102

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.63372 -0.16551 0.03671 0.14232 0.68194

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.040626 0.054207 -0.749 0.456

ID 0.000652 0.001192 0.547 0.586

Residual standard error: 0.2371 on 76 degrees of freedom

Multiple R-squared: 0.00392, Adjusted R-squared: -0.009187

F-statistic: 0.2991 on 1 and 76 DF, p-value: 0.5861

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.1286, p-value = 0.00001402

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.0184, df = 1, p-value = 0.3129

Box-Ljung test

data: lm_residuals

X-squared = 15.317, df = 1, p-value = 0.0000909