Analysis

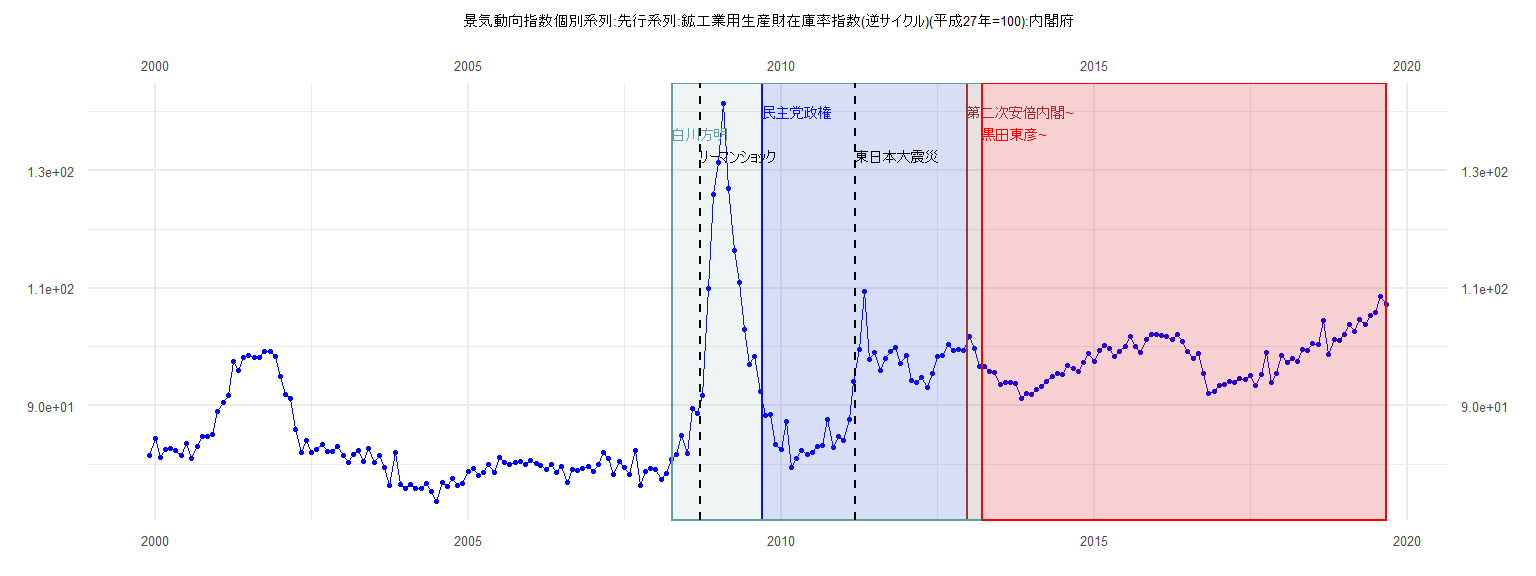

[1] "景気動向指数個別系列:先行系列:鉱工業用生産財在庫率指数(逆サイクル)(平成27年=100):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 81.5

2000 84.5 81.2 82.6 82.8 82.4 81.6 83.6 81.0 83.0 84.7 84.8 85.1

2001 89.0 90.5 91.7 97.6 96.0 98.2 98.6 98.2 98.2 99.2 99.2 98.4

2002 95.0 92.0 91.3 85.9 82.0 84.1 82.0 82.6 83.5 82.2 82.2 83.0

2003 81.5 80.3 81.8 82.4 80.5 82.8 80.4 81.5 79.5 76.5 82.1 76.7

2004 76.0 76.7 76.0 76.0 76.8 75.5 73.8 77.0 76.3 77.7 76.4 76.8

2005 78.8 79.3 78.1 78.7 80.0 78.7 81.2 80.4 80.1 80.3 80.5 80.1

2006 80.7 80.2 79.9 79.2 80.0 78.6 79.6 77.0 79.2 79.0 79.4 79.6

2007 78.8 80.0 82.0 81.0 78.3 80.5 79.5 78.3 82.4 76.5 78.8 79.3

2008 79.2 77.4 78.5 80.9 81.8 85.0 81.9 89.5 88.7 91.8 109.9 125.9

2009 131.4 141.4 126.9 116.4 111.0 103.0 97.0 98.4 92.4 88.3 88.5 83.5

2010 82.6 87.3 79.5 81.0 82.4 81.7 82.1 83.0 83.2 87.6 82.9 84.8

2011 84.1 87.6 94.2 99.5 109.5 97.8 99.0 96.0 98.0 99.3 99.9 97.2

2012 98.5 94.3 94.0 94.8 93.1 95.5 98.3 98.5 100.5 99.4 99.5 99.4

2013 101.7 99.8 96.7 96.6 95.9 95.7 93.6 94.0 93.9 93.8 91.3 92.1

2014 92.0 92.7 93.2 94.2 94.9 95.5 95.3 96.8 96.4 95.9 97.4 98.9

2015 97.6 99.4 100.3 99.7 98.4 99.3 100.0 101.8 100.0 99.0 101.3 102.2

2016 102.2 101.9 101.7 101.2 102.2 100.9 99.3 98.0 98.9 95.5 92.1 92.4

2017 93.4 93.7 94.1 94.0 94.6 94.4 95.1 93.5 95.4 99.0 93.9 95.5

2018 98.6 97.3 98.0 97.5 99.6 99.4 100.6 100.4 104.5 98.7 101.2 101.1

2019 102.1 103.9 102.6 104.6 103.8 105.3 105.8 108.6 107.2

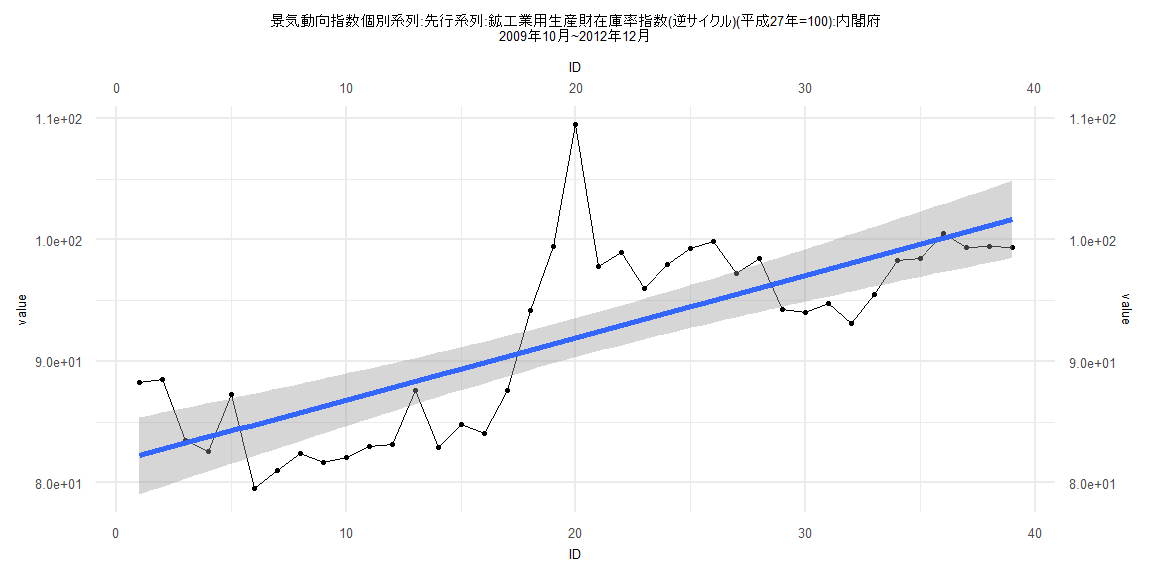

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-5.982 -3.851 -1.158 3.149 17.544

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 81.70823 1.62529 50.273 < 0.0000000000000002 ***

ID 0.51241 0.07082 7.235 0.0000000138 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.978 on 37 degrees of freedom

Multiple R-squared: 0.5859, Adjusted R-squared: 0.5747

F-statistic: 52.35 on 1 and 37 DF, p-value: 0.0000000138

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.28205, p-value = 0.08974

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.59452, p-value = 0.00000003294

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.43466, df = 1, p-value = 0.5097

Box-Ljung test

data: lm_residuals

X-squared = 19.441, df = 1, p-value = 0.00001038

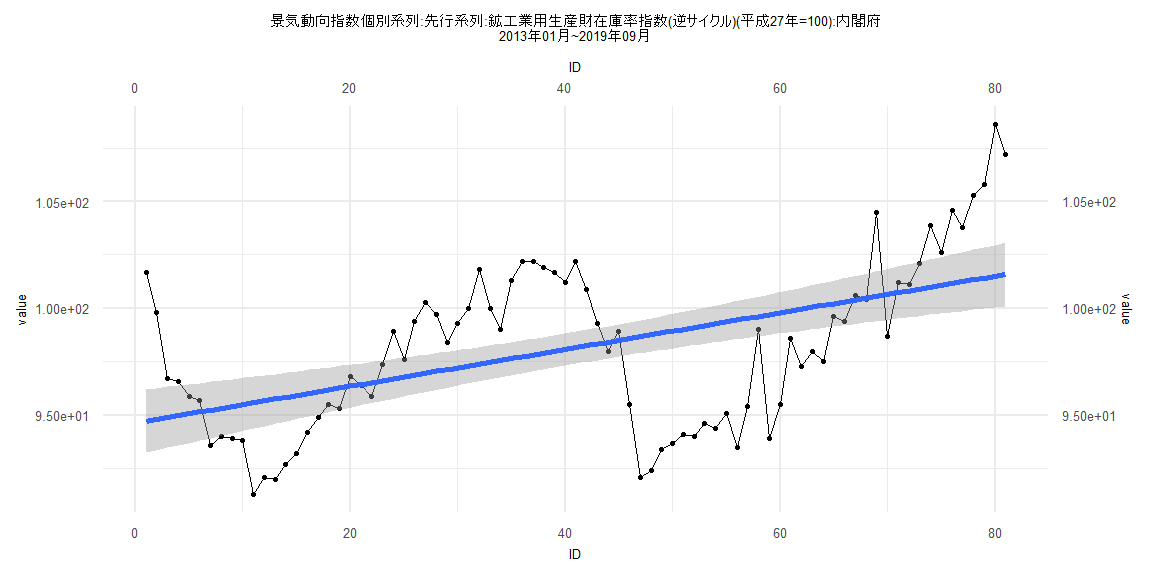

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-6.5756 -2.6352 0.2779 2.6536 7.0910

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 94.64031 0.75880 124.72 < 0.0000000000000002 ***

ID 0.08586 0.01608 5.34 0.000000868 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.383 on 79 degrees of freedom

Multiple R-squared: 0.2653, Adjusted R-squared: 0.256

F-statistic: 28.52 on 1 and 79 DF, p-value: 0.000000868

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11111, p-value = 0.7027

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.26112, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.7001, df = 1, p-value = 0.1003

Box-Ljung test

data: lm_residuals

X-squared = 57.222, df = 1, p-value = 0.00000000000003897

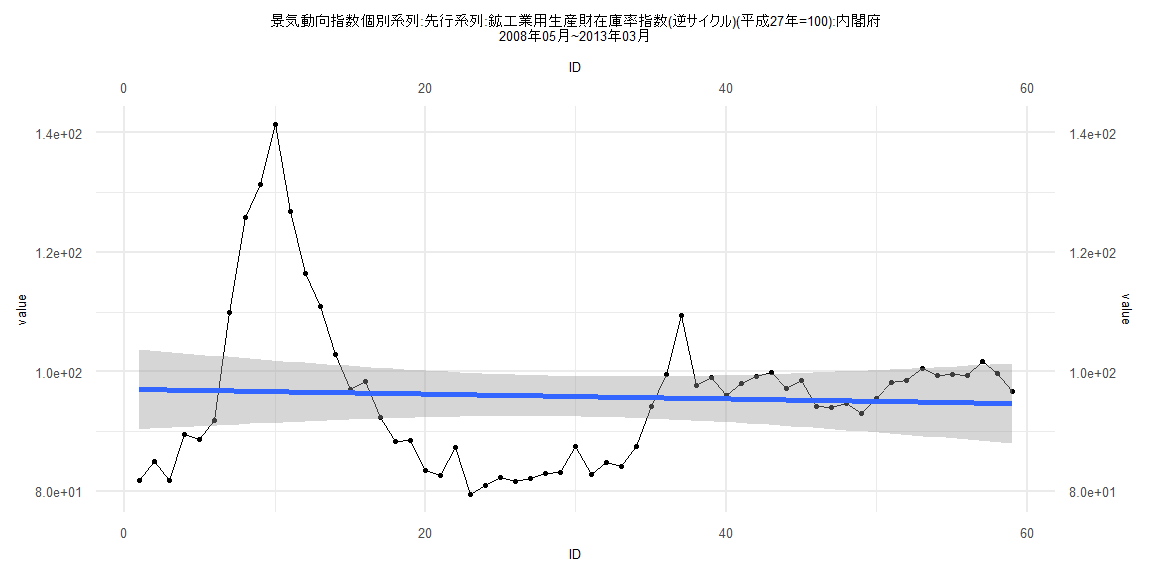

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-16.662 -9.951 0.428 4.518 44.712

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 97.09158 3.41735 28.411 <0.0000000000000002 ***

ID -0.04040 0.09906 -0.408 0.685

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 12.96 on 57 degrees of freedom

Multiple R-squared: 0.002909, Adjusted R-squared: -0.01458

F-statistic: 0.1663 on 1 and 57 DF, p-value: 0.685

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.30508, p-value = 0.00792

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.19563, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 10.811, df = 1, p-value = 0.001009

Box-Ljung test

data: lm_residuals

X-squared = 49.132, df = 1, p-value = 0.000000000002393

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-6.4632 -2.4616 0.0348 2.7876 6.7339

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 94.15937 0.74966 125.60 < 0.0000000000000002 ***

ID 0.10009 0.01649 6.07 0.0000000466 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.279 on 76 degrees of freedom

Multiple R-squared: 0.3265, Adjusted R-squared: 0.3177

F-statistic: 36.85 on 1 and 76 DF, p-value: 0.00000004663

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.546

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.27158, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.3501, df = 1, p-value = 0.01174

Box-Ljung test

data: lm_residuals

X-squared = 57.74, df = 1, p-value = 0.00000000000002998