Analysis

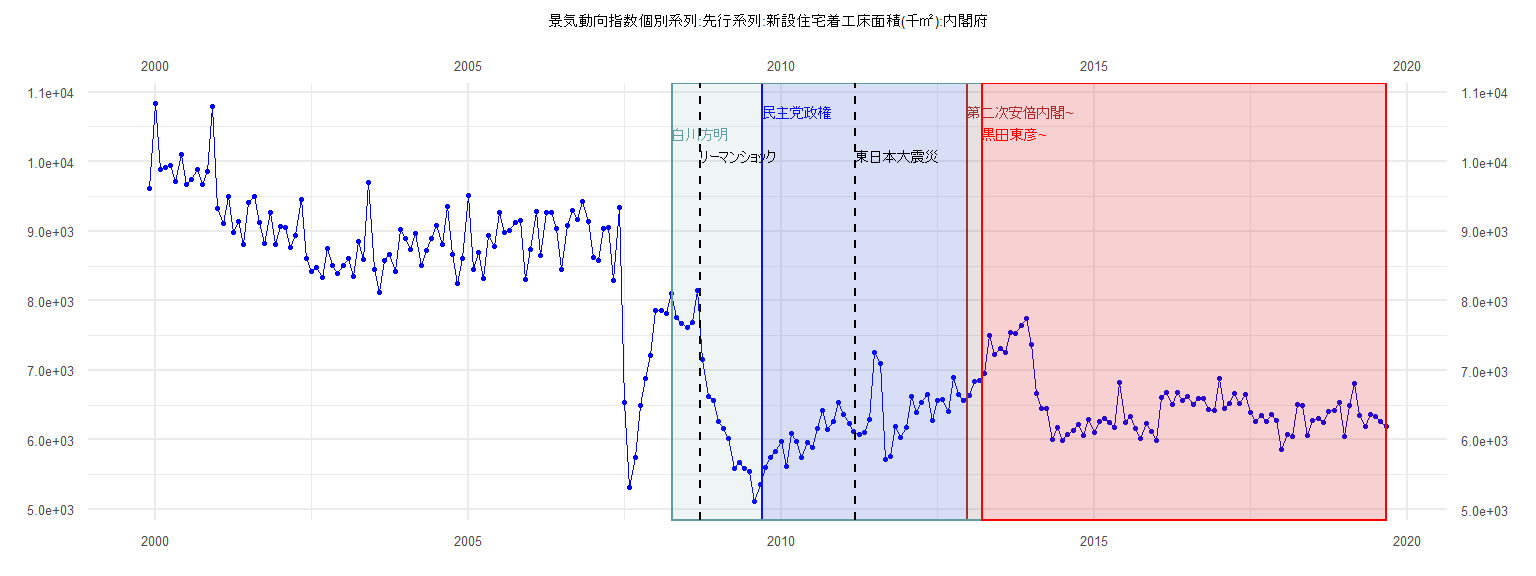

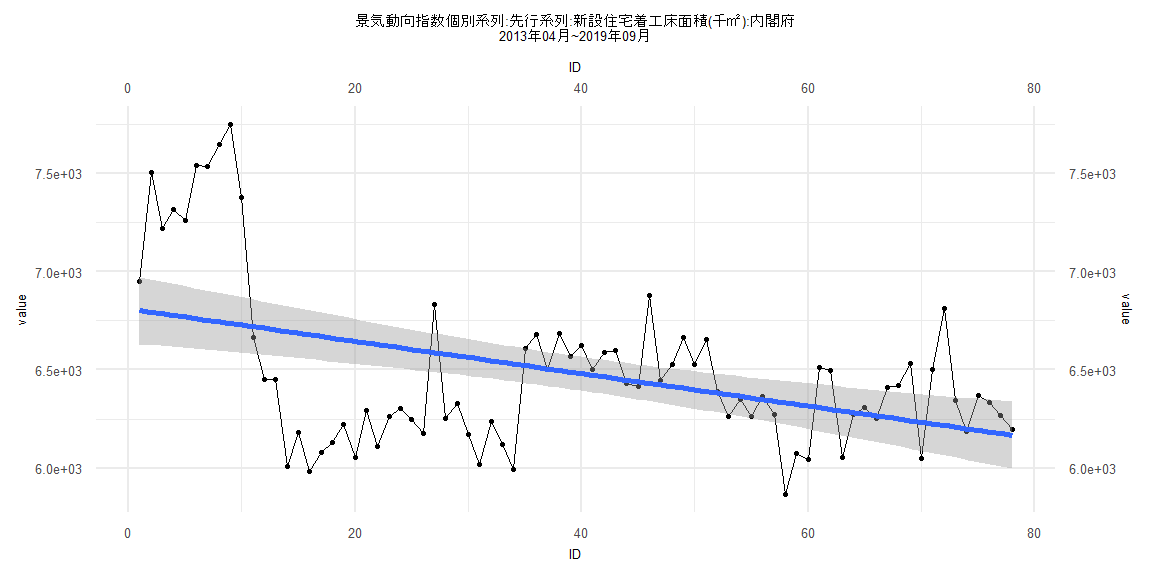

[1] "景気動向指数個別系列:先行系列:新設住宅着工床面積(千㎡):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 9615

2000 10837 9887 9924 9951 9721 10110 9674 9744 9894 9668 9864 10792

2001 9326 9115 9495 8988 9144 8817 9409 9498 9133 8824 9274 8806

2002 9070 9049 8762 8938 9464 8613 8425 8479 8342 8746 8512 8388

2003 8508 8609 8349 8850 8599 9698 8450 8114 8577 8663 8428 9025

2004 8897 8734 8961 8506 8728 8894 9084 8809 9362 8663 8249 8608

2005 9516 8451 8697 8325 8934 8780 9276 8979 9014 9133 9153 8302

2006 8734 9287 8650 9276 9273 9037 8452 9083 9295 9172 9425 9144

2007 8630 8585 9041 9050 8287 9345 6531 5313 5748 6494 6888 7213

2008 7857 7857 7813 8106 7758 7671 7619 7693 8142 7149 6628 6564

2009 6268 6161 6016 5585 5672 5584 5548 5120 5357 5605 5749 5834

2010 5977 5614 6090 5972 5746 5962 5889 6166 6419 6145 6263 6543

2011 6359 6233 6122 6073 6105 6300 7254 7102 5715 5758 6186 6036

2012 6184 6629 6389 6542 6654 6282 6569 6586 6406 6898 6652 6565

2013 6644 6836 6860 6950 7502 7222 7316 7261 7540 7535 7645 7748

2014 7376 6667 6450 6450 6008 6182 5984 6081 6133 6222 6057 6293

2015 6113 6264 6306 6248 6178 6832 6254 6330 6170 6021 6238 6123

2016 5994 6611 6680 6502 6684 6569 6622 6502 6590 6599 6432 6418

2017 6879 6446 6528 6666 6527 6653 6388 6261 6348 6263 6367 6274

2018 5867 6076 6044 6511 6495 6056 6276 6310 6255 6413 6422 6533

2019 6048 6500 6811 6345 6186 6368 6333 6268 6196

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-616.86 -167.95 7.32 130.92 965.34

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5813.490 99.685 58.319 < 0.0000000000000002 ***

ID 21.599 4.344 4.972 0.0000154 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 305.3 on 37 degrees of freedom

Multiple R-squared: 0.4006, Adjusted R-squared: 0.3844

F-statistic: 24.72 on 1 and 37 DF, p-value: 0.00001536

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4073, p-value = 0.01848

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.21036, df = 1, p-value = 0.6465

Box-Ljung test

data: lm_residuals

X-squared = 3.4779, df = 1, p-value = 0.06219

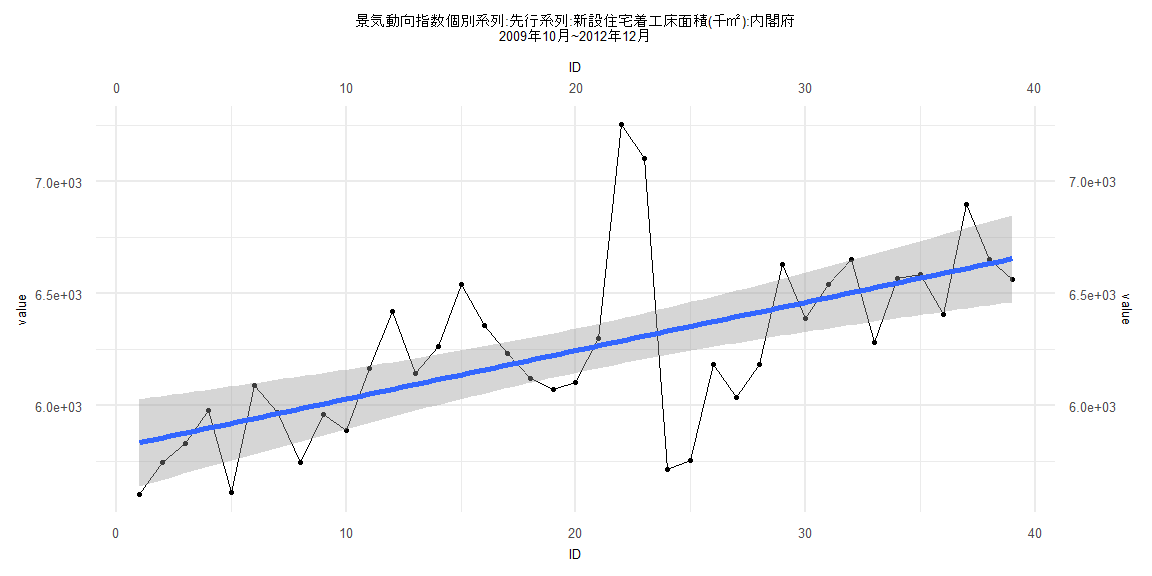

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-690.66 -272.82 17.65 170.24 1016.41

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6829.179 84.018 81.283 < 0.0000000000000002 ***

ID -8.133 1.780 -4.569 0.0000178 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 374.6 on 79 degrees of freedom

Multiple R-squared: 0.209, Adjusted R-squared: 0.199

F-statistic: 20.87 on 1 and 79 DF, p-value: 0.00001784

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.46772, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 20.687, df = 1, p-value = 0.000005409

Box-Ljung test

data: lm_residuals

X-squared = 49.142, df = 1, p-value = 0.000000000002381

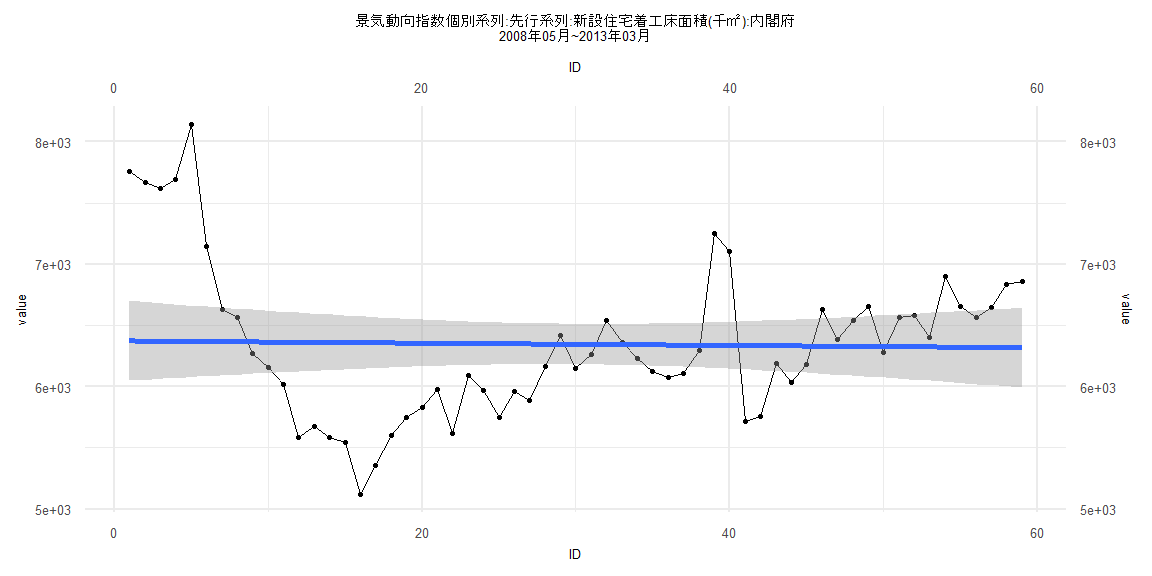

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1239.69 -384.26 -98.25 278.72 1772.01

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6374.6756 166.7512 38.229 <0.0000000000000002 ***

ID -0.9366 4.8339 -0.194 0.847

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 632.3 on 57 degrees of freedom

Multiple R-squared: 0.0006583, Adjusted R-squared: -0.01687

F-statistic: 0.03755 on 1 and 57 DF, p-value: 0.847

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.13559, p-value = 0.6544

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.30811, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 17.206, df = 1, p-value = 0.00003354

Box-Ljung test

data: lm_residuals

X-squared = 39.465, df = 1, p-value = 0.0000000003341

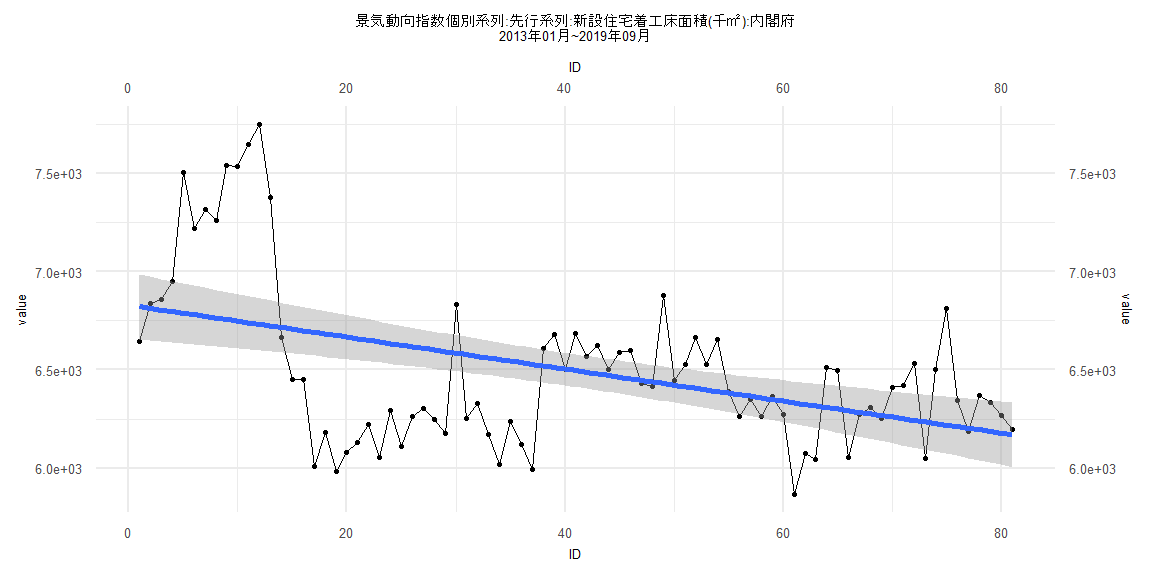

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-694.44 -297.87 12.17 174.78 1011.88

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6810.274 87.183 78.115 < 0.0000000000000002 ***

ID -8.240 1.918 -4.297 0.0000507 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 381.3 on 76 degrees of freedom

Multiple R-squared: 0.1955, Adjusted R-squared: 0.1849

F-statistic: 18.46 on 1 and 76 DF, p-value: 0.00005068

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.316

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.46463, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 26.501, df = 1, p-value = 0.0000002634

Box-Ljung test

data: lm_residuals

X-squared = 47.632, df = 1, p-value = 0.000000000005143