Analysis

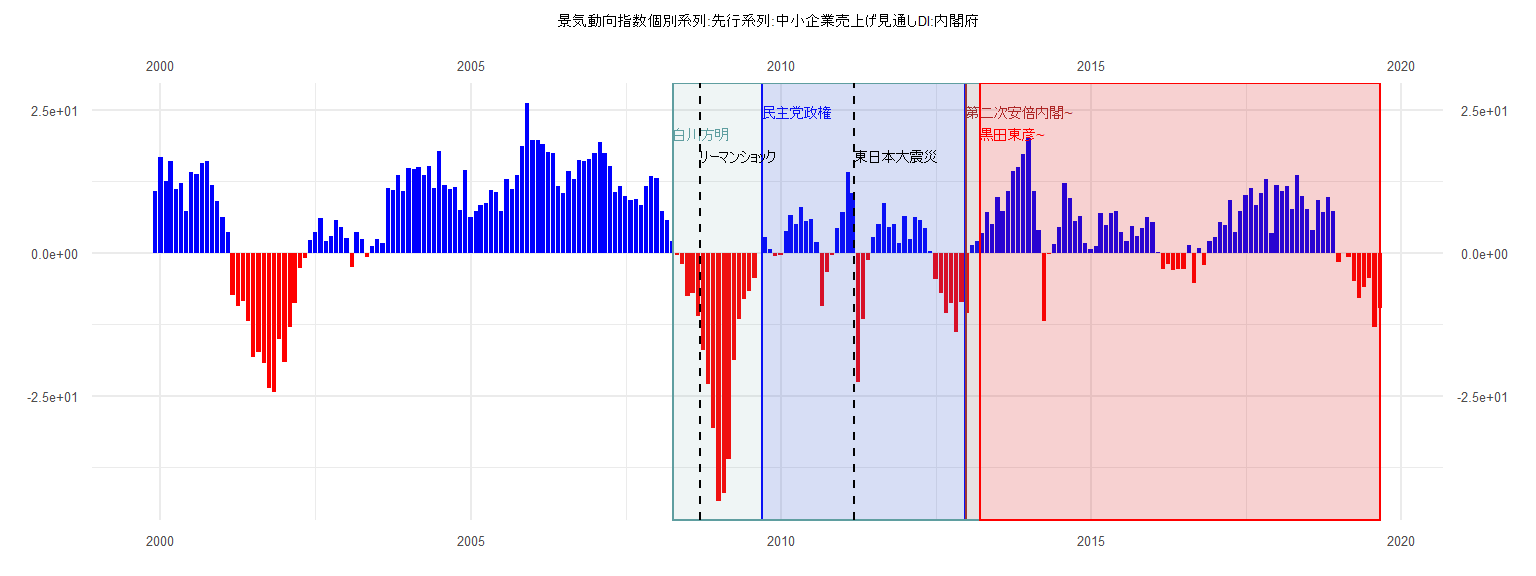

[1] "景気動向指数個別系列:先行系列:中小企業売上げ見通しDI:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 10.9

2000 16.7 12.6 16.1 11.2 12.3 7.4 14.1 13.8 15.8 16.0 11.9 9.0

2001 6.2 3.7 -7.4 -9.2 -8.4 -11.9 -18.2 -17.4 -19.2 -23.7 -24.4 -15.0

2002 -19.1 -12.9 -8.8 -2.6 -0.9 2.2 3.6 6.1 2.0 3.0 5.8 4.5

2003 2.6 -2.5 3.7 2.5 -0.8 1.2 2.4 1.7 11.3 11.0 13.6 10.9

2004 14.9 14.6 15.1 13.6 15.2 11.3 17.8 11.8 11.1 11.5 7.5 14.5

2005 6.2 7.3 8.4 8.8 11.0 10.7 7.3 12.9 11.1 13.6 18.7 26.2

2006 19.8 19.8 19.0 17.6 17.5 11.7 10.4 14.4 12.9 16.3 16.1 16.4

2007 17.4 19.4 17.5 15.2 10.6 11.7 9.9 9.2 9.5 8.4 11.7 13.4

2008 13.1 7.4 5.7 2.1 -0.3 -1.9 -7.5 -7.0 -11.1 -17.0 -22.9 -30.6

2009 -43.3 -41.9 -36.0 -18.8 -11.6 -8.1 -6.7 -4.4 0.0 2.8 0.7 -0.5

2010 -0.4 3.9 6.6 5.1 8.0 5.6 5.9 1.9 -9.3 -3.3 -0.3 4.4

2011 7.1 14.2 10.5 -22.5 -11.5 -1.3 2.7 5.1 8.8 4.6 5.1 1.7

2012 6.4 2.4 6.3 5.7 4.4 0.4 -4.6 -7.0 -10.5 -8.8 -13.8 -8.5

2013 -10.5 1.3 2.0 3.5 7.1 5.0 9.8 7.3 10.9 14.4 15.1 17.3

2014 20.1 10.8 4.0 -11.9 -0.2 1.6 4.6 12.2 9.6 5.6 6.5 1.7

2015 0.7 1.2 6.9 4.9 7.0 7.4 3.6 2.0 4.7 2.9 4.4 6.3

2016 5.4 0.1 -2.8 -1.9 -3.0 -2.9 -2.9 1.4 -5.2 0.8 -2.1 2.1

2017 2.7 5.4 4.8 9.2 3.6 7.3 10.1 11.3 8.3 10.4 12.9 3.5

2018 11.9 10.8 11.7 7.7 13.6 9.9 7.7 4.0 9.2 7.1 9.7 7.4

2019 -1.6 -0.1 -0.8 -4.9 -7.9 -6.0 -4.4 -13.0 -9.6

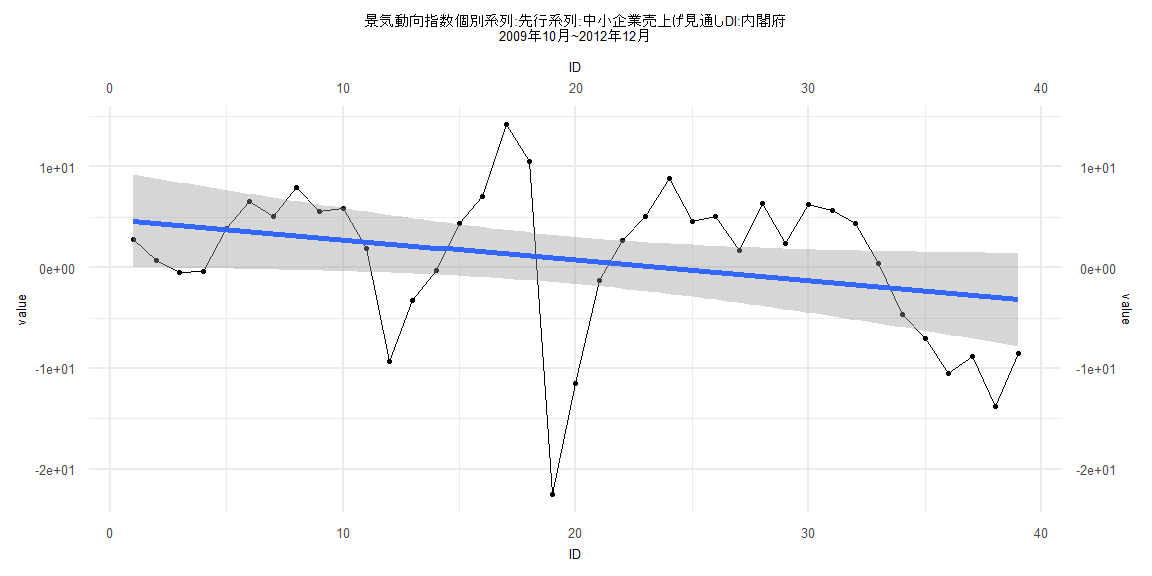

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-23.423 -4.521 2.351 4.953 12.866

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.8244 2.3631 2.042 0.0484 *

ID -0.2053 0.1030 -1.994 0.0536 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.237 on 37 degrees of freedom

Multiple R-squared: 0.09703, Adjusted R-squared: 0.07263

F-statistic: 3.976 on 1 and 37 DF, p-value: 0.05356

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.96713, p-value = 0.0001105

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.27095, df = 1, p-value = 0.6027

Box-Ljung test

data: lm_residuals

X-squared = 10.871, df = 1, p-value = 0.0009766

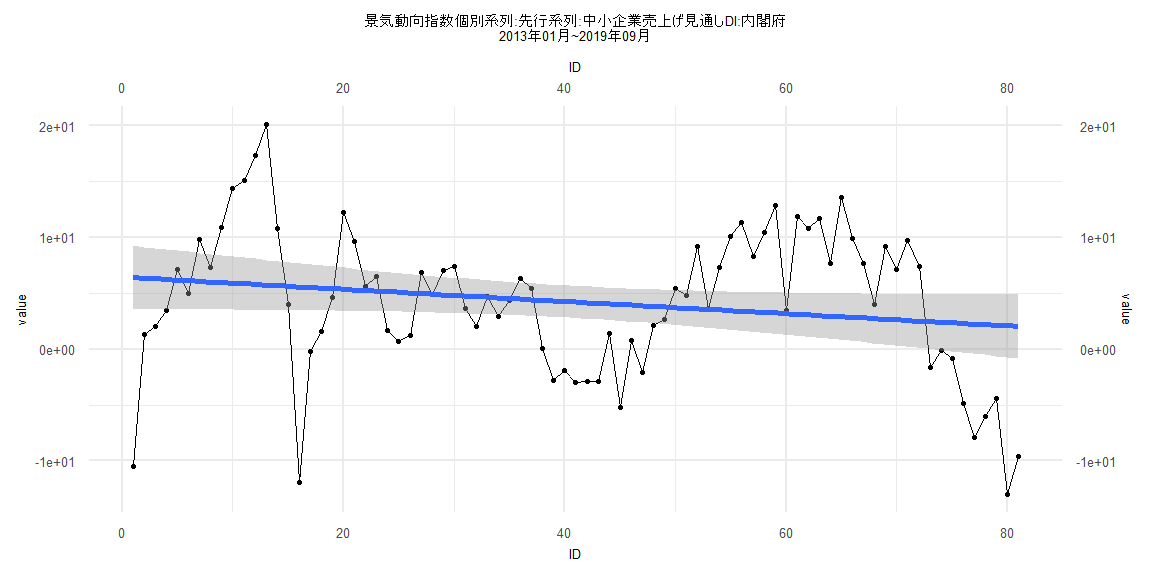

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-17.4722 -4.0577 0.0567 4.9145 14.3639

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.44645 1.46014 4.415 0.0000317 ***

ID -0.05464 0.03094 -1.766 0.0812 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.51 on 79 degrees of freedom

Multiple R-squared: 0.03799, Adjusted R-squared: 0.02581

F-statistic: 3.12 on 1 and 79 DF, p-value: 0.08122

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.50647, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.064866, df = 1, p-value = 0.799

Box-Ljung test

data: lm_residuals

X-squared = 39.316, df = 1, p-value = 0.0000000003605

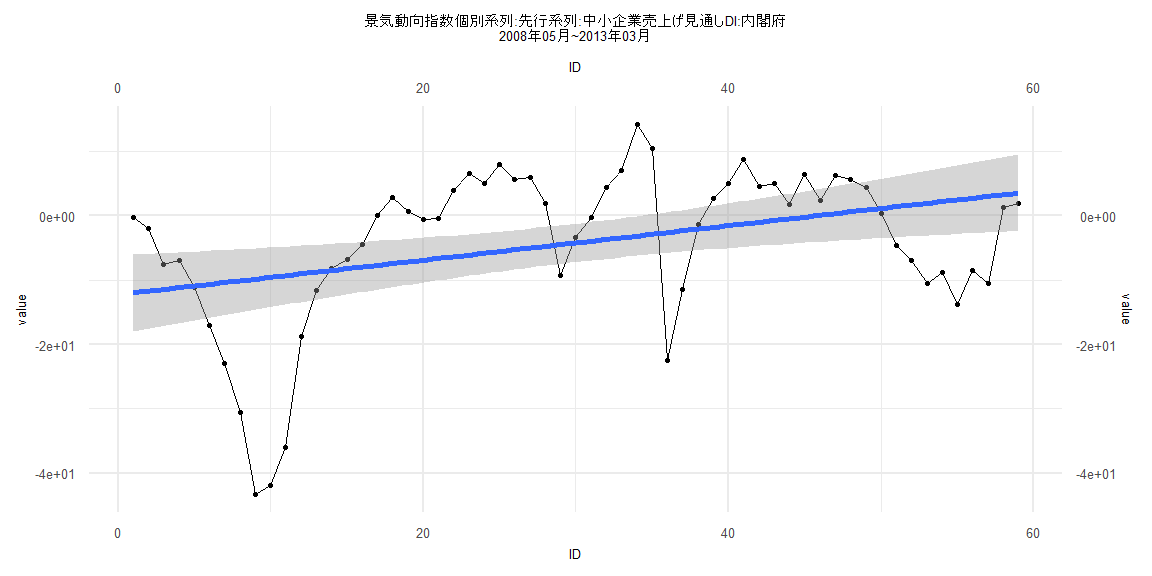

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-33.467 -6.190 3.558 7.773 17.337

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -12.2441 3.0324 -4.038 0.000163 ***

ID 0.2679 0.0879 3.047 0.003498 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 11.5 on 57 degrees of freedom

Multiple R-squared: 0.1401, Adjusted R-squared: 0.125

F-statistic: 9.285 on 1 and 57 DF, p-value: 0.003498

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.37106, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 3.8151, df = 1, p-value = 0.05079

Box-Ljung test

data: lm_residuals

X-squared = 40.237, df = 1, p-value = 0.0000000002249

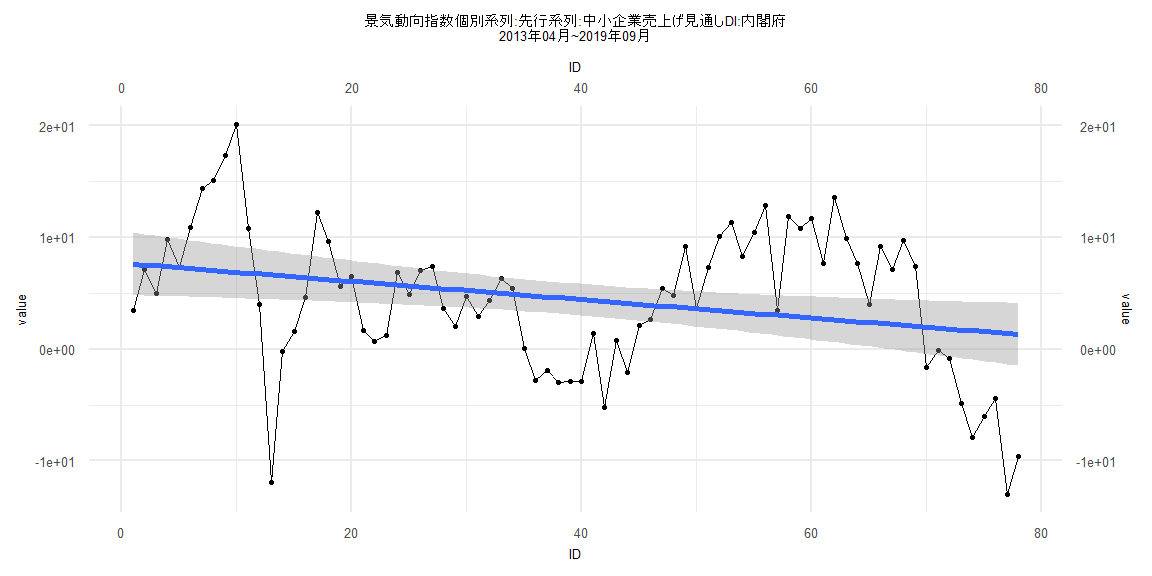

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-18.5282 -4.2327 -0.2147 5.0191 13.2264

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 7.69167 1.43198 5.371 0.000000824 ***

ID -0.08181 0.03150 -2.597 0.0113 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.263 on 76 degrees of freedom

Multiple R-squared: 0.08153, Adjusted R-squared: 0.06945

F-statistic: 6.747 on 1 and 76 DF, p-value: 0.01127

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.089744, p-value = 0.9147

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.52054, p-value = 0.0000000000000005029

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.2555, df = 1, p-value = 0.2625

Box-Ljung test

data: lm_residuals

X-squared = 41.653, df = 1, p-value = 0.000000000109