Analysis

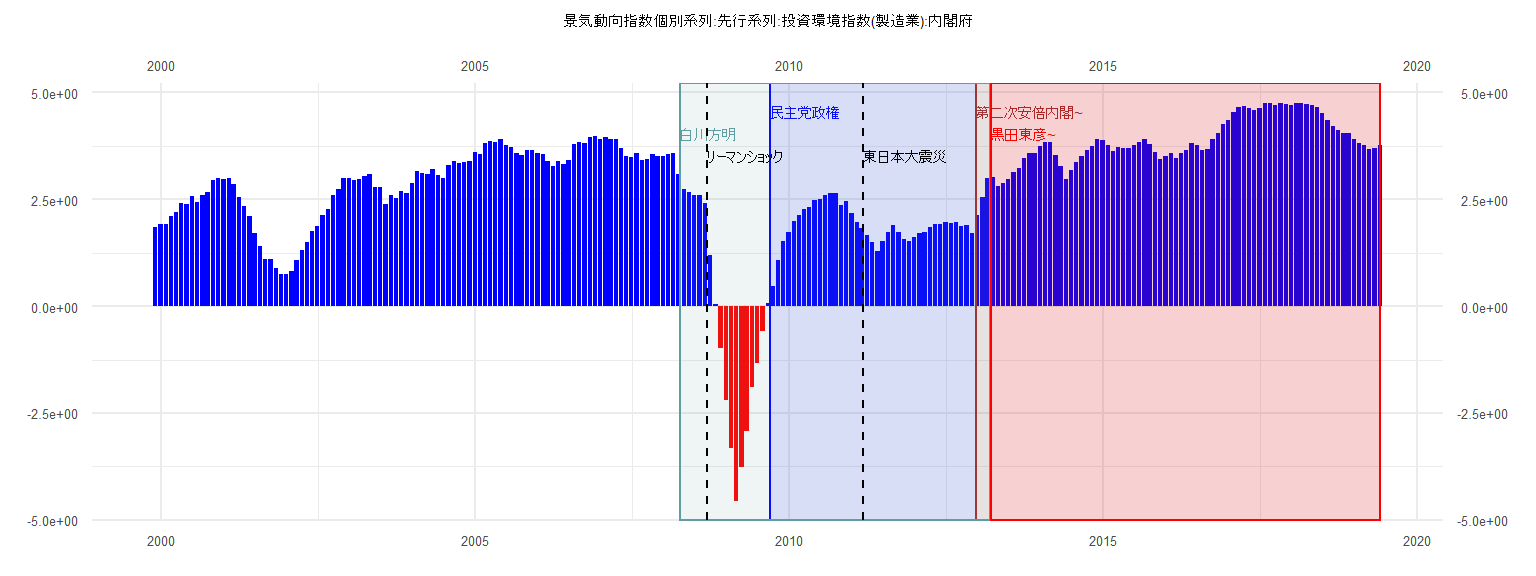

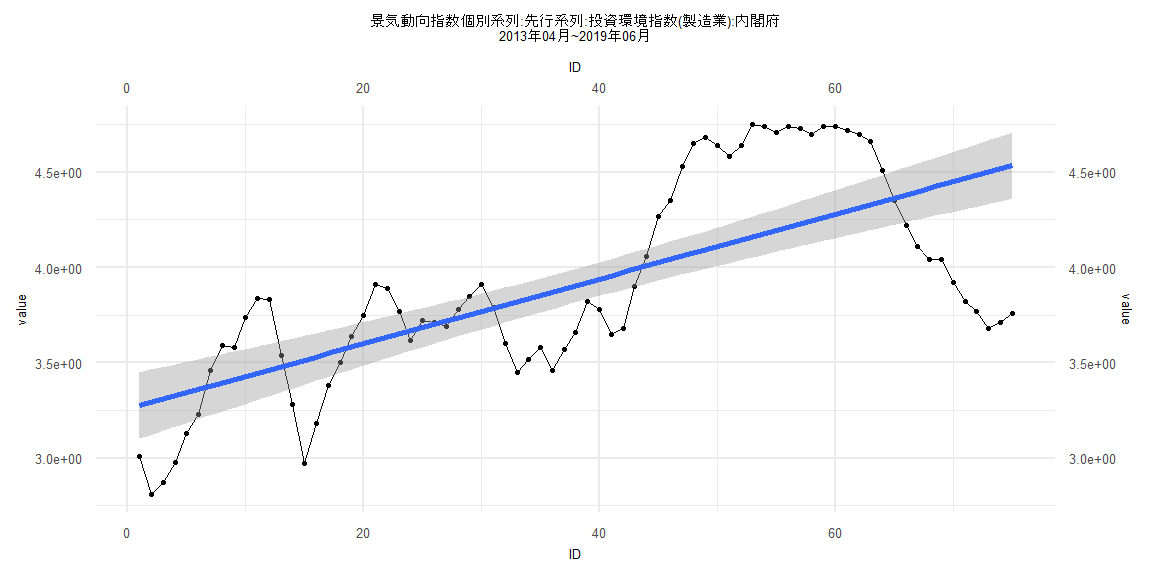

[1] "景気動向指数個別系列:先行系列:投資環境指数(製造業):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 1.86

2000 1.92 1.92 2.11 2.21 2.40 2.39 2.57 2.44 2.59 2.67 2.94 3.00

2001 2.98 3.00 2.86 2.55 2.34 2.10 1.72 1.41 1.10 1.09 0.90 0.76

2002 0.76 0.83 1.08 1.31 1.49 1.75 1.87 2.14 2.27 2.61 2.75 2.99

2003 3.00 2.96 2.97 3.05 3.10 2.79 2.79 2.38 2.60 2.53 2.70 2.65

2004 2.88 3.15 3.11 3.10 3.21 3.07 3.00 3.30 3.39 3.34 3.38 3.39

2005 3.61 3.56 3.81 3.86 3.83 3.90 3.76 3.72 3.57 3.53 3.65 3.65

2006 3.57 3.56 3.40 3.27 3.39 3.33 3.42 3.80 3.83 3.82 3.95 3.97

2007 3.92 3.95 3.90 3.90 3.70 3.52 3.49 3.59 3.42 3.45 3.56 3.50

2008 3.51 3.55 3.59 3.09 2.73 2.66 2.61 2.61 2.41 1.19 0.04 -0.99

2009 -2.19 -3.32 -4.55 -3.77 -2.92 -1.89 -1.33 -0.58 0.08 0.46 1.08 1.53

2010 1.74 2.00 2.14 2.28 2.31 2.49 2.51 2.59 2.64 2.65 2.37 2.45

2011 2.17 1.97 1.82 1.66 1.50 1.30 1.52 1.73 1.90 1.73 1.57 1.53

2012 1.61 1.70 1.74 1.84 1.91 1.92 1.96 1.94 1.96 1.88 1.89 1.72

2013 2.14 2.55 2.99 3.01 2.81 2.87 2.98 3.13 3.23 3.46 3.59 3.58

2014 3.74 3.84 3.83 3.54 3.28 2.97 3.18 3.38 3.50 3.64 3.75 3.91

2015 3.89 3.77 3.62 3.72 3.71 3.69 3.78 3.85 3.91 3.79 3.60 3.45

2016 3.52 3.58 3.46 3.57 3.66 3.82 3.78 3.65 3.68 3.90 4.06 4.27

2017 4.35 4.53 4.65 4.68 4.64 4.58 4.64 4.75 4.74 4.71 4.74 4.73

2018 4.70 4.74 4.74 4.72 4.70 4.66 4.51 4.35 4.22 4.11 4.04 4.04

2019 3.92 3.82 3.77 3.68 3.71 3.76

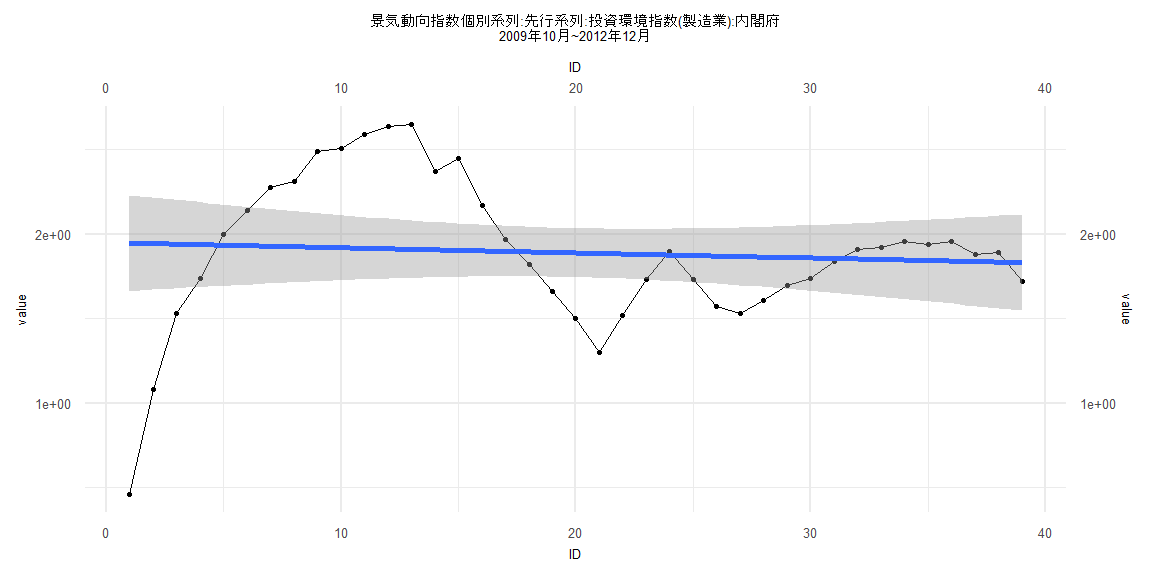

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.48773 -0.21583 0.04165 0.23765 0.73873

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.950769 0.145768 13.383 0.000000000000000942 ***

ID -0.003038 0.006352 -0.478 0.635

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4464 on 37 degrees of freedom

Multiple R-squared: 0.006147, Adjusted R-squared: -0.02071

F-statistic: 0.2288 on 1 and 37 DF, p-value: 0.6352

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25641, p-value = 0.1547

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.18332, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 9.5451, df = 1, p-value = 0.002005

Box-Ljung test

data: lm_residuals

X-squared = 24.14, df = 1, p-value = 0.000000896

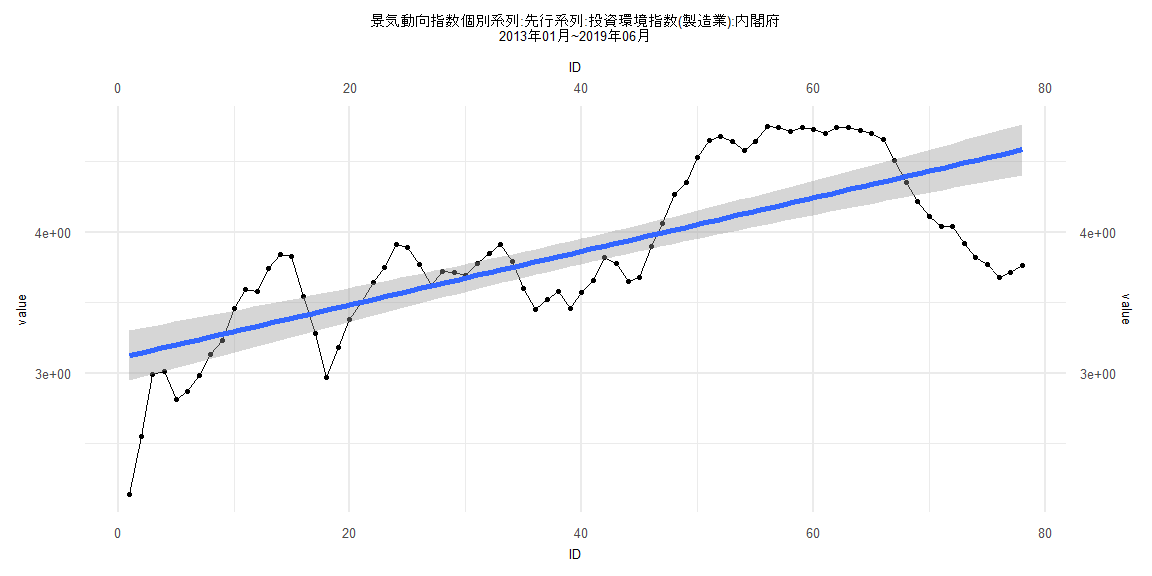

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.98332 -0.28288 0.02888 0.34206 0.58965

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.104362 0.091621 33.883 < 0.0000000000000002 ***

ID 0.018961 0.002015 9.409 0.000000000000022 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4007 on 76 degrees of freedom

Multiple R-squared: 0.5381, Adjusted R-squared: 0.532

F-statistic: 88.54 on 1 and 76 DF, p-value: 0.00000000000002202

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.089744, p-value = 0.9147

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.1206, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 10.082, df = 1, p-value = 0.001497

Box-Ljung test

data: lm_residuals

X-squared = 61.664, df = 1, p-value = 0.000000000000004108

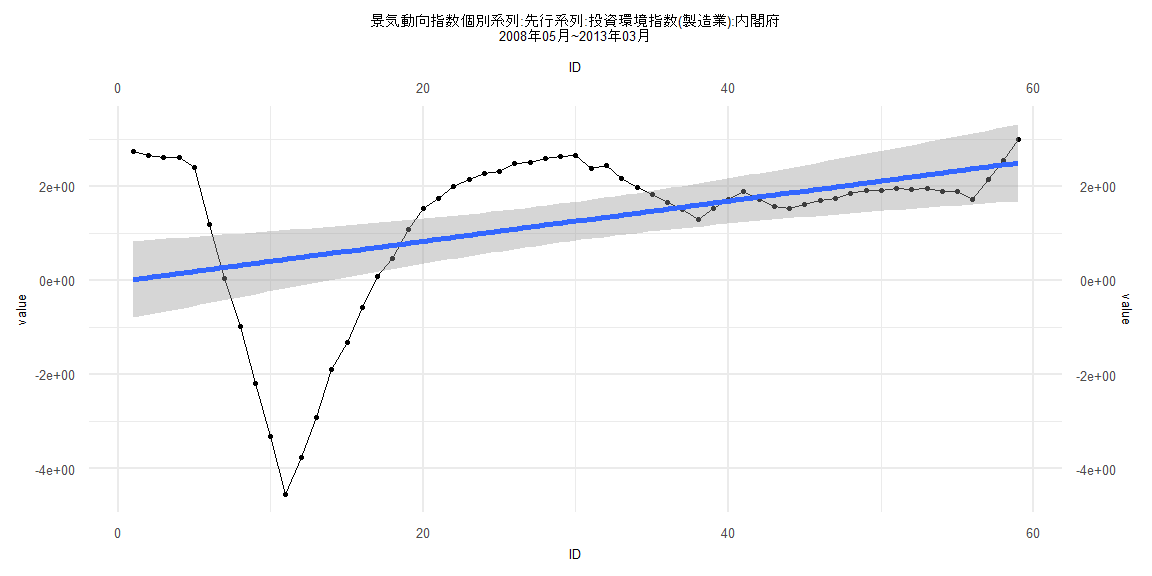

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-4.9961 -0.2933 -0.0562 1.0771 2.7109

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.02359 0.41859 -0.056 0.95525

ID 0.04270 0.01213 3.519 0.00086 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.587 on 57 degrees of freedom

Multiple R-squared: 0.1784, Adjusted R-squared: 0.164

F-statistic: 12.38 on 1 and 57 DF, p-value: 0.0008598

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25424, p-value = 0.04374

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.097231, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 17.43, df = 1, p-value = 0.0000298

Box-Ljung test

data: lm_residuals

X-squared = 53.087, df = 1, p-value = 0.0000000000003192

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.82007 -0.29057 0.00893 0.32043 0.58993

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.25907 0.08922 36.527 < 0.0000000000000002 ***

ID 0.01700 0.00204 8.333 0.00000000000333 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3825 on 73 degrees of freedom

Multiple R-squared: 0.4875, Adjusted R-squared: 0.4805

F-statistic: 69.44 on 1 and 73 DF, p-value: 0.000000000003335

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14667, p-value = 0.3974

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.10667, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 22.822, df = 1, p-value = 0.000001777

Box-Ljung test

data: lm_residuals

X-squared = 65.38, df = 1, p-value = 0.0000000000000006661