Analysis

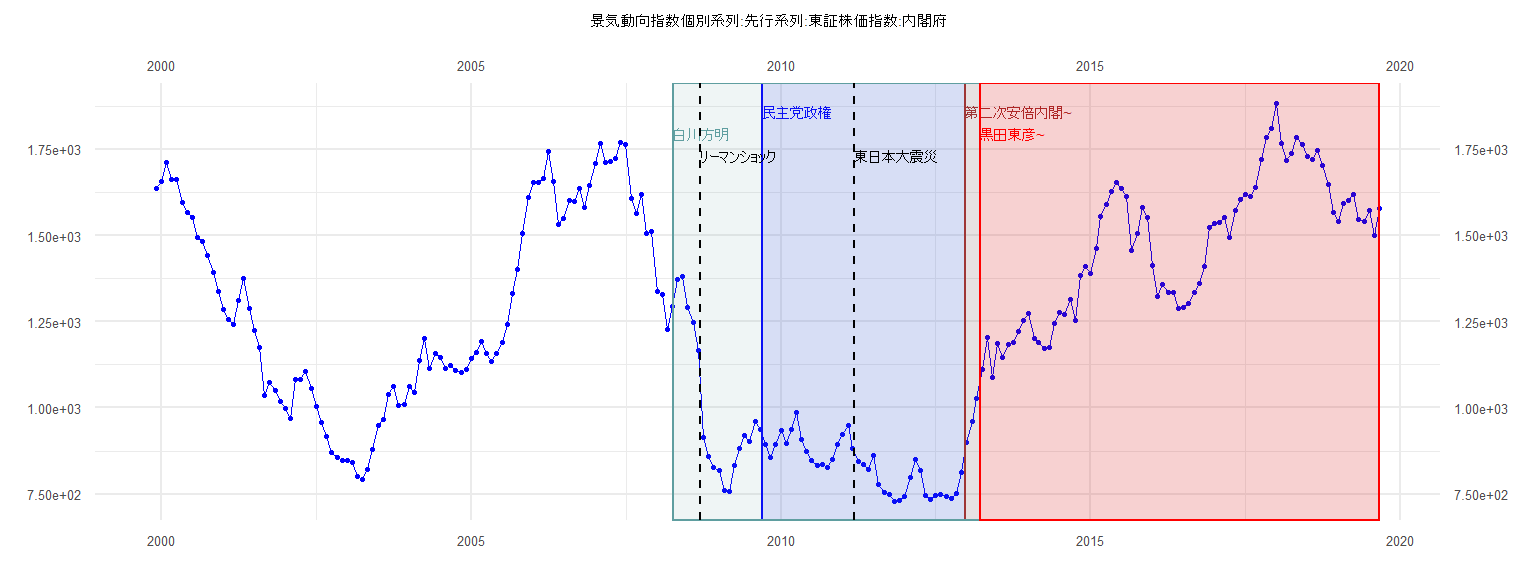

[1] "景気動向指数個別系列:先行系列:東証株価指数:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 1637.52

2000 1657.91 1711.97 1661.73 1661.89 1595.11 1566.27 1552.98 1493.44 1483.96 1443.34 1392.39 1336.78

2001 1284.67 1257.92 1240.74 1311.51 1376.04 1289.61 1224.91 1174.71 1035.73 1072.61 1050.44 1018.09

2002 999.01 970.11 1083.89 1083.27 1105.87 1056.54 1003.17 956.43 916.01 871.56 856.11 847.24

2003 847.86 841.75 802.14 791.55 820.42 879.19 949.44 965.77 1038.26 1062.92 1007.04 1010.30

2004 1061.40 1045.70 1137.66 1200.99 1113.85 1158.74 1146.49 1114.78 1122.40 1108.48 1101.78 1110.39

2005 1144.09 1159.71 1191.82 1158.22 1134.29 1159.35 1189.41 1241.61 1333.02 1400.34 1505.63 1611.10

2006 1654.17 1653.33 1665.10 1745.00 1657.22 1532.82 1549.25 1601.79 1599.36 1635.35 1580.23 1646.40

2007 1708.42 1765.50 1711.78 1714.63 1724.49 1768.46 1762.62 1606.10 1562.37 1619.67 1504.90 1510.22

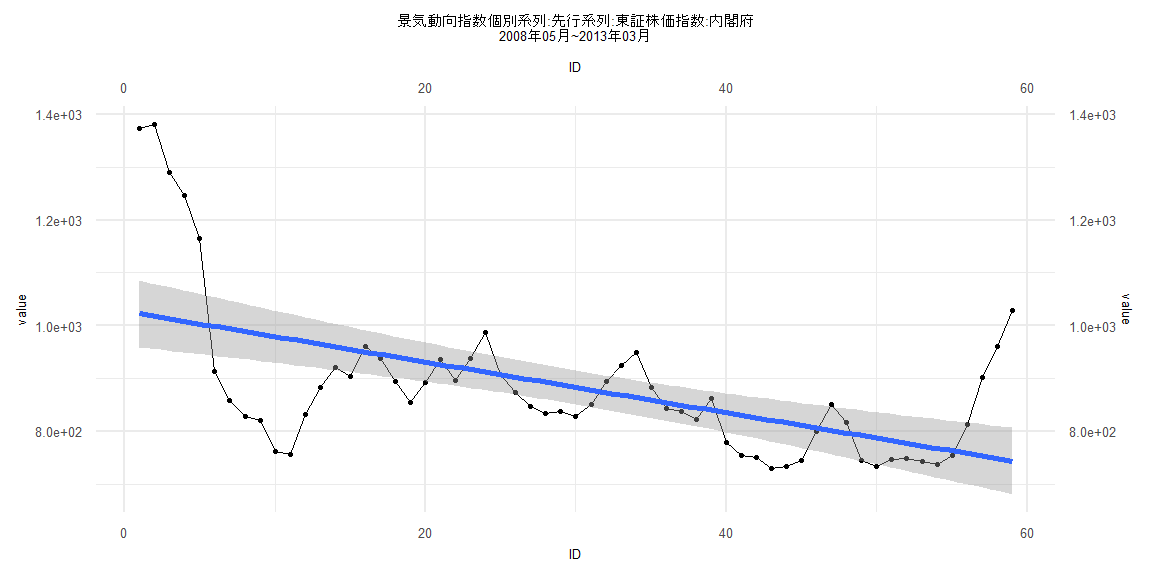

2008 1337.71 1328.42 1228.87 1294.08 1373.83 1380.74 1290.26 1247.10 1165.80 913.49 857.92 827.40

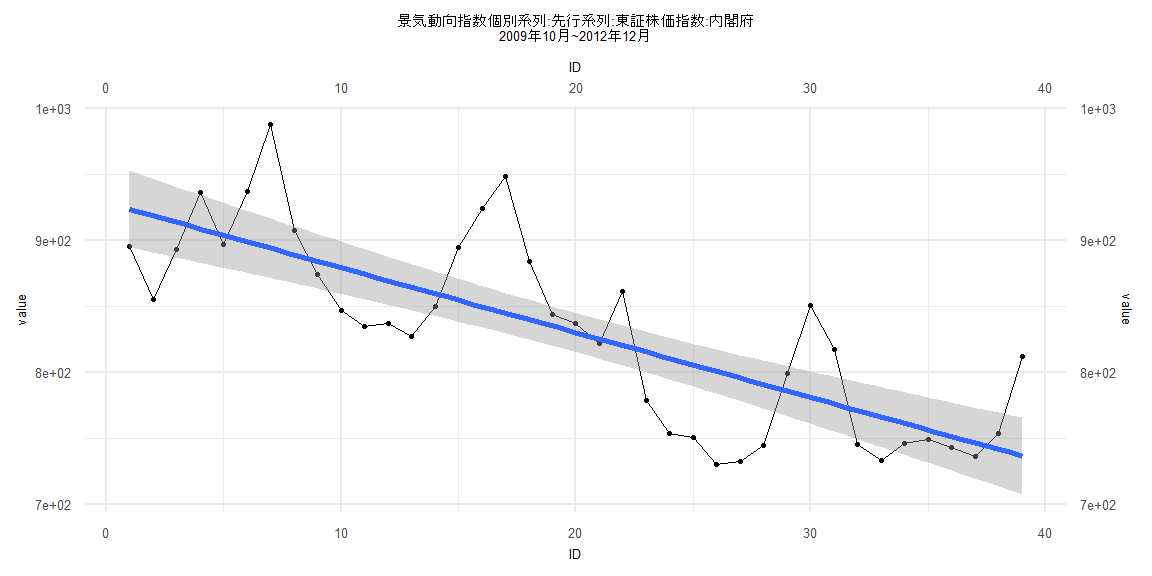

2009 819.66 762.16 756.52 832.63 882.40 921.57 903.66 961.13 937.02 895.10 855.14 892.90

2010 936.12 896.61 936.98 987.60 907.38 873.79 846.85 834.51 836.55 827.07 849.90 894.54

2011 924.36 948.61 883.59 843.89 837.02 822.06 861.29 778.73 753.81 750.34 730.12 732.53

2012 744.40 799.32 850.37 817.43 745.33 733.19 746.00 748.73 742.65 736.24 753.21 811.87

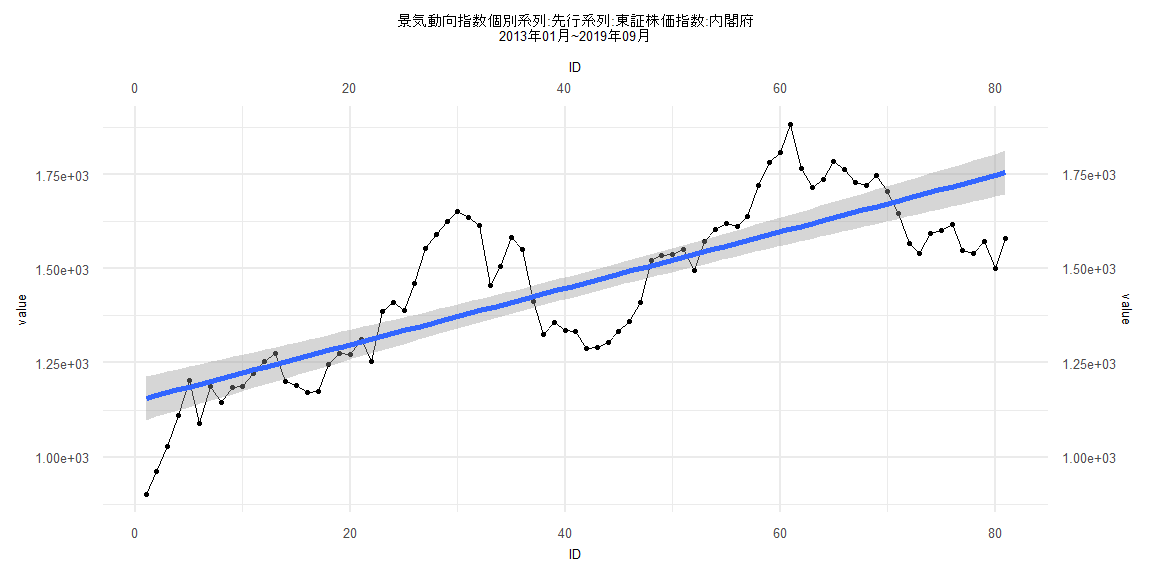

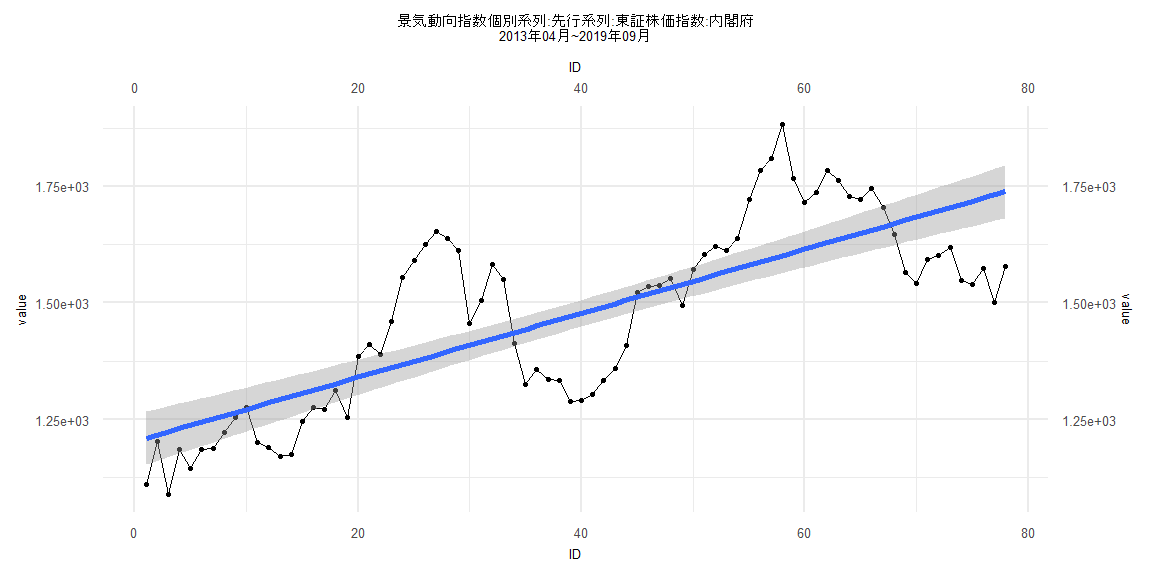

2013 901.20 961.02 1028.55 1110.41 1203.38 1089.48 1186.91 1145.42 1185.18 1188.51 1222.90 1254.45

2014 1275.17 1200.83 1190.57 1171.18 1174.62 1246.22 1275.72 1271.50 1313.29 1253.99 1385.33 1411.59

2015 1389.14 1461.08 1553.83 1590.91 1626.44 1652.72 1637.30 1613.59 1455.30 1506.15 1582.45 1551.34

2016 1412.22 1324.59 1358.30 1335.67 1334.43 1288.83 1291.30 1303.93 1334.42 1360.45 1409.47 1522.68

2017 1534.42 1537.60 1552.10 1494.81 1571.62 1603.77 1620.17 1612.95 1638.79 1721.72 1783.26 1809.61

2018 1882.57 1766.57 1716.27 1737.42 1783.96 1762.48 1729.12 1721.03 1746.41 1703.85 1646.77 1565.86

2019 1541.56 1592.61 1602.83 1618.12 1547.17 1540.08 1573.16 1501.08 1579.13

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-70.246 -32.725 -8.491 32.812 103.942

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 928.3506 14.8955 62.324 < 0.0000000000000002 ***

ID -4.9225 0.6491 -7.584 0.00000000479 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 45.62 on 37 degrees of freedom

Multiple R-squared: 0.6085, Adjusted R-squared: 0.598

F-statistic: 57.52 on 1 and 37 DF, p-value: 0.000000004794

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.23077, p-value = 0.2523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.71325, p-value = 0.0000007913

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.051813, df = 1, p-value = 0.8199

Box-Ljung test

data: lm_residuals

X-squared = 15.207, df = 1, p-value = 0.00009636

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-254.728 -103.875 -7.882 81.475 279.716

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1148.4425 29.5645 38.84 <0.0000000000000002 ***

ID 7.4854 0.6264 11.95 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 131.8 on 79 degrees of freedom

Multiple R-squared: 0.6438, Adjusted R-squared: 0.6393

F-statistic: 142.8 on 1 and 79 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.1358, p-value = 0.4462

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.19218, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.1069, df = 1, p-value = 0.2928

Box-Ljung test

data: lm_residuals

X-squared = 63.467, df = 1, p-value = 0.000000000000001665

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-217.65 -57.05 -28.31 21.46 363.33

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1027.0241 32.3765 31.721 < 0.0000000000000002 ***

ID -4.8047 0.9385 -5.119 0.00000377 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 122.8 on 57 degrees of freedom

Multiple R-squared: 0.315, Adjusted R-squared: 0.3029

F-statistic: 26.21 on 1 and 57 DF, p-value: 0.000003768

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.30508, p-value = 0.00792

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.20081, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 8.6266, df = 1, p-value = 0.003313

Box-Ljung test

data: lm_residuals

X-squared = 37.788, df = 1, p-value = 0.0000000007887

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-230.75 -97.43 -13.30 89.25 281.25

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1202.9508 29.0501 41.41 <0.0000000000000002 ***

ID 6.8685 0.6389 10.75 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 127.1 on 76 degrees of freedom

Multiple R-squared: 0.6033, Adjusted R-squared: 0.598

F-statistic: 115.6 on 1 and 76 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.089744, p-value = 0.9147

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.20525, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.6952, df = 1, p-value = 0.1006

Box-Ljung test

data: lm_residuals

X-squared = 63.181, df = 1, p-value = 0.000000000000001887