Analysis

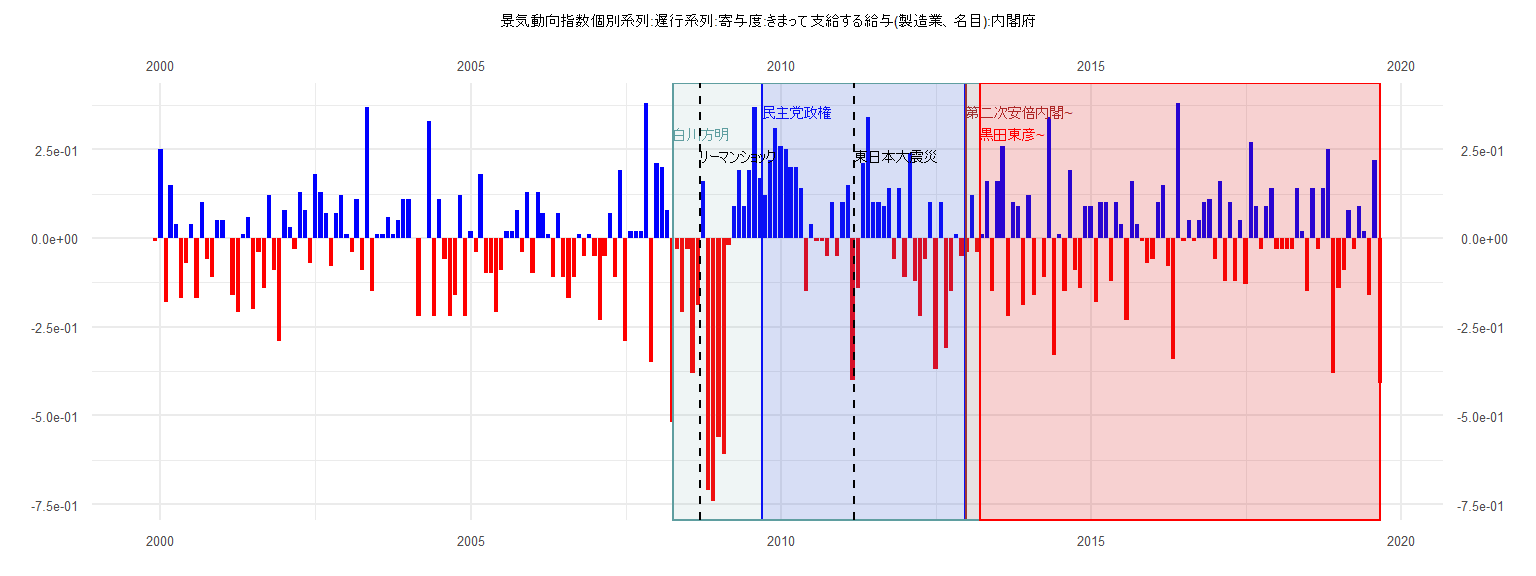

[1] "景気動向指数個別系列:遅行系列:寄与度:きまって支給する給与(製造業、名目):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.01

2000 0.25 -0.18 0.15 0.04 -0.17 -0.07 0.04 -0.17 0.10 -0.06 -0.11 0.05

2001 0.05 0.00 -0.16 -0.21 0.01 0.06 -0.20 -0.04 -0.14 0.12 -0.09 -0.29

2002 0.08 0.03 -0.03 0.13 0.08 -0.07 0.18 0.13 0.07 -0.08 0.07 0.12

2003 0.01 -0.04 0.11 -0.09 0.37 -0.15 0.01 0.01 0.06 0.01 0.05 0.11

2004 0.11 0.00 -0.22 0.00 0.33 -0.22 0.11 -0.06 -0.22 -0.16 0.12 -0.22

2005 0.02 -0.04 0.18 -0.10 -0.10 -0.21 -0.09 0.02 0.02 0.08 -0.04 0.13

2006 -0.10 0.13 0.07 0.01 -0.11 0.07 -0.11 -0.17 -0.11 0.01 -0.05 0.01

2007 -0.05 -0.23 -0.05 0.07 -0.11 0.19 -0.29 0.02 0.02 0.02 0.38 -0.35

2008 0.21 0.20 0.08 -0.52 -0.03 -0.21 -0.03 -0.38 -0.19 0.16 -0.71 -0.74

2009 -0.56 -0.61 -0.02 0.09 0.19 0.09 0.19 0.37 0.17 0.12 0.22 0.31

2010 0.26 0.25 0.20 0.20 0.14 -0.15 0.04 -0.01 -0.01 -0.05 0.10 -0.05

2011 0.10 0.15 -0.40 -0.14 0.21 0.34 0.10 0.10 0.09 0.14 -0.06 0.14

2012 -0.11 0.24 -0.12 -0.22 -0.06 0.10 -0.37 0.10 -0.31 -0.15 0.01 -0.05

2013 -0.04 0.12 -0.04 0.01 0.16 -0.15 0.16 0.26 -0.22 0.10 0.09 -0.19

2014 0.12 -0.16 0.00 -0.11 0.34 -0.33 0.01 -0.15 0.19 -0.09 -0.14 0.09

2015 0.09 -0.18 0.10 0.10 -0.12 0.10 0.04 -0.23 0.16 0.04 -0.01 -0.07

2016 -0.06 0.10 0.15 -0.08 -0.34 0.38 -0.01 0.05 -0.01 0.05 0.10 0.11

2017 -0.06 0.16 -0.12 0.10 -0.12 0.05 -0.13 0.27 0.09 -0.03 0.09 0.14

2018 -0.03 -0.03 -0.03 -0.03 0.14 0.02 -0.15 0.14 -0.03 0.14 0.25 -0.38

2019 -0.14 -0.09 0.08 -0.03 0.09 0.02 -0.16 0.22 -0.41

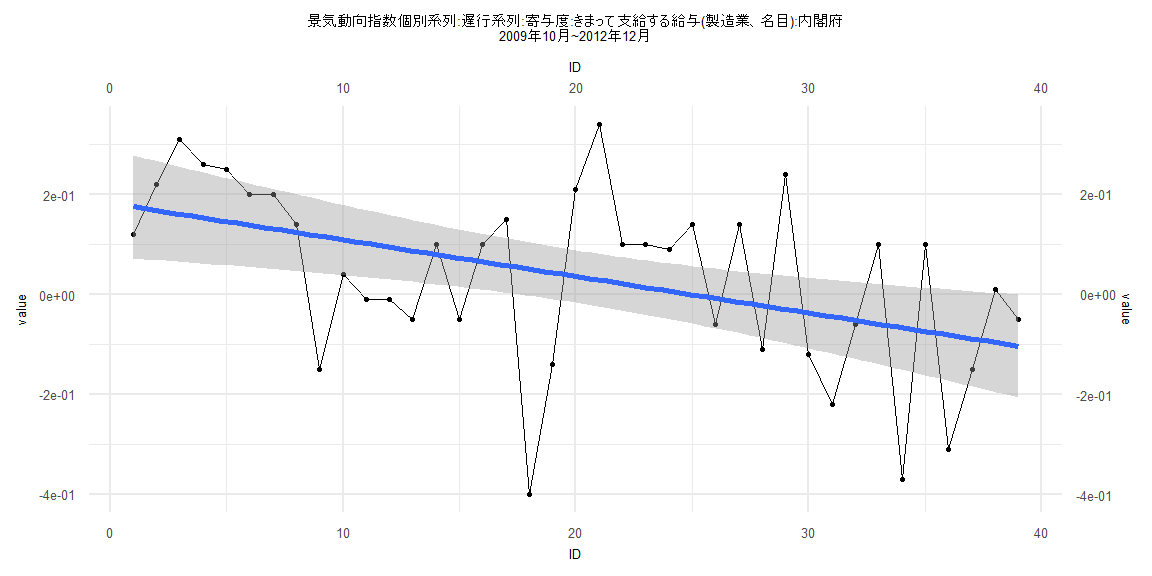

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.4506 -0.0959 0.0348 0.1051 0.3114

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.182416 0.052852 3.451 0.00141 **

ID -0.007326 0.002303 -3.181 0.00297 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1619 on 37 degrees of freedom

Multiple R-squared: 0.2148, Adjusted R-squared: 0.1935

F-statistic: 10.12 on 1 and 37 DF, p-value: 0.002967

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.9711, p-value = 0.3961

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.64756, df = 1, p-value = 0.421

Box-Ljung test

data: lm_residuals

X-squared = 0.0054741, df = 1, p-value = 0.941

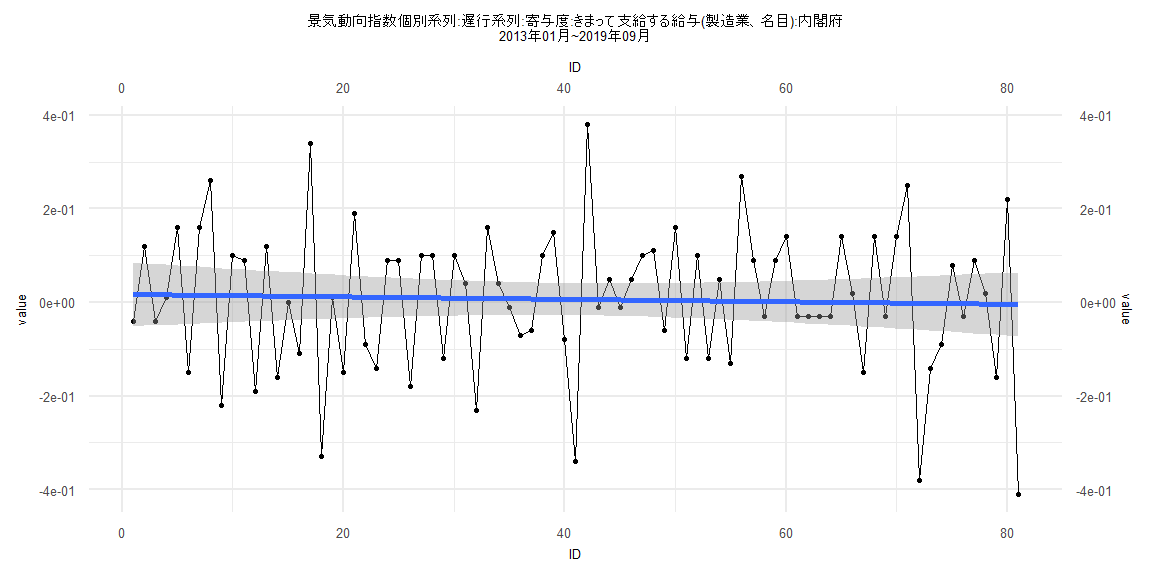

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.40594 -0.10140 -0.00218 0.09515 0.37384

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0171605 0.0348157 0.493 0.623

ID -0.0002620 0.0007376 -0.355 0.723

Residual standard error: 0.1552 on 79 degrees of freedom

Multiple R-squared: 0.001594, Adjusted R-squared: -0.01104

F-statistic: 0.1261 on 1 and 79 DF, p-value: 0.7234

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.074074, p-value = 0.9806

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.7094, p-value = 0.9993

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.21466, df = 1, p-value = 0.6431

Box-Ljung test

data: lm_residuals

X-squared = 13.368, df = 1, p-value = 0.000256

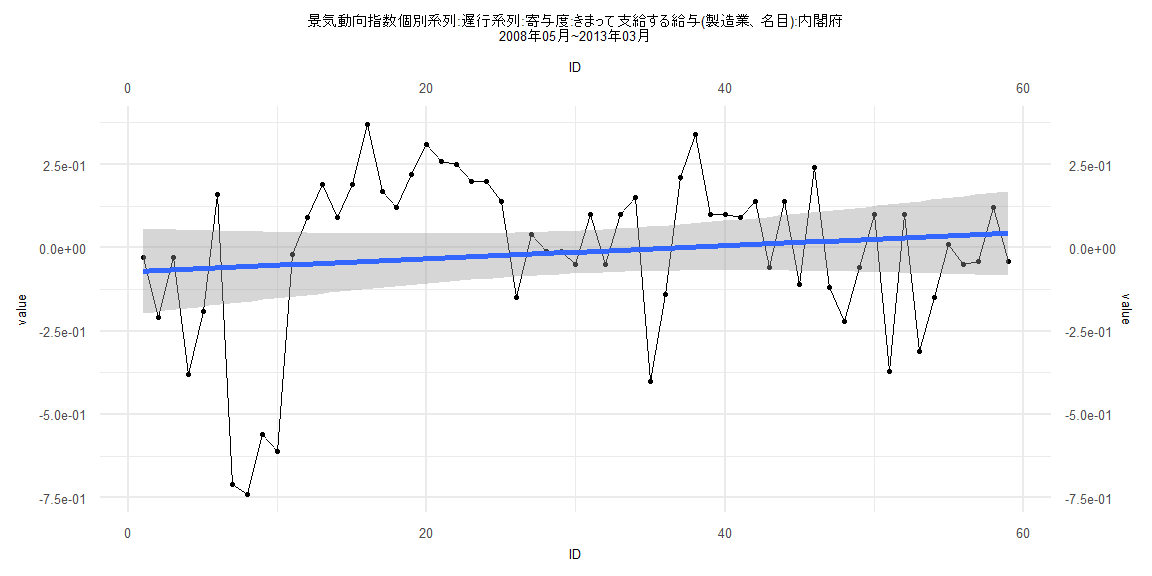

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.68371 -0.12699 0.05909 0.15986 0.41063

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.071958 0.065074 -1.106 0.273

ID 0.001958 0.001886 1.038 0.304

Residual standard error: 0.2468 on 57 degrees of freedom

Multiple R-squared: 0.01855, Adjusted R-squared: 0.00133

F-statistic: 1.077 on 1 and 57 DF, p-value: 0.3037

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0277, p-value = 0.0000164

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.9927, df = 1, p-value = 0.008184

Box-Ljung test

data: lm_residuals

X-squared = 14.592, df = 1, p-value = 0.0001335

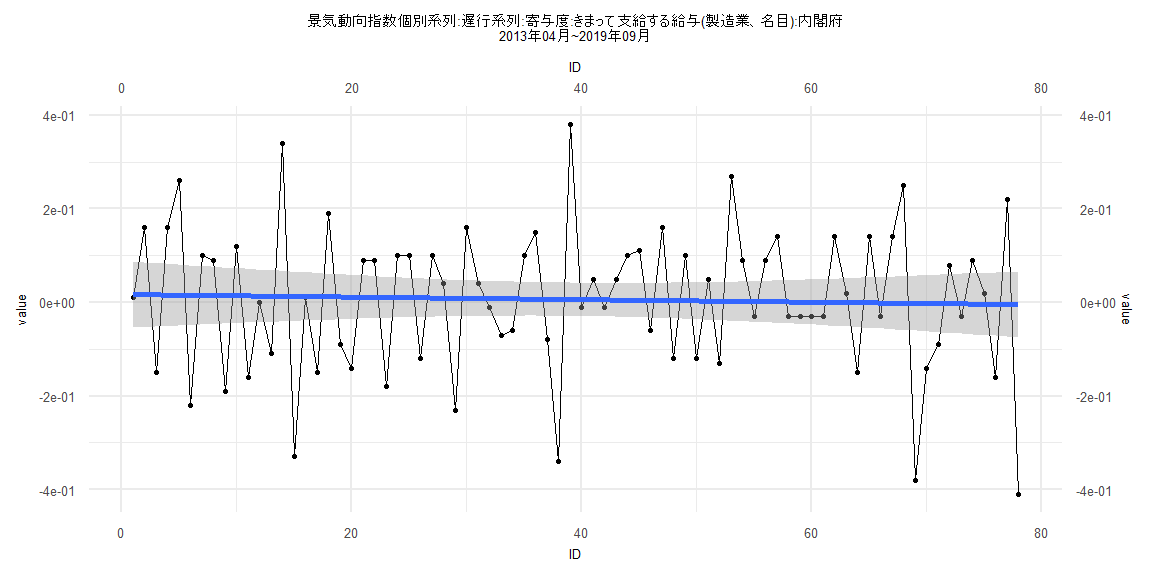

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.40568 -0.11791 0.00885 0.09461 0.37371

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.0169031 0.0360224 0.469 0.640

ID -0.0002721 0.0007923 -0.343 0.732

Residual standard error: 0.1575 on 76 degrees of freedom

Multiple R-squared: 0.00155, Adjusted R-squared: -0.01159

F-statistic: 0.118 on 1 and 76 DF, p-value: 0.7322

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16667, p-value = 0.2297

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.7055, p-value = 0.9991

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.030659, df = 1, p-value = 0.861

Box-Ljung test

data: lm_residuals

X-squared = 12.732, df = 1, p-value = 0.0003595