Analysis

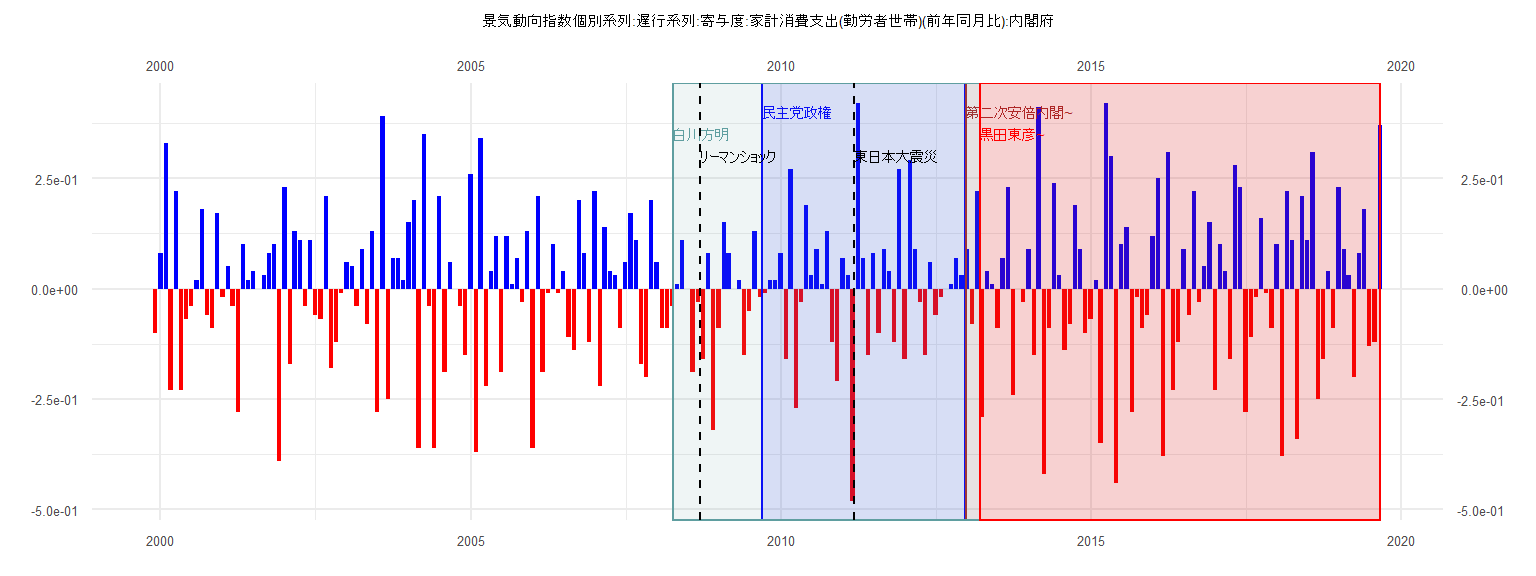

[1] "景気動向指数個別系列:遅行系列:寄与度:家計消費支出(勤労者世帯)(前年同月比):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.10

2000 0.08 0.33 -0.23 0.22 -0.23 -0.07 -0.04 0.02 0.18 -0.06 -0.09 0.17

2001 -0.02 0.05 -0.04 -0.28 0.10 0.02 0.04 0.00 0.03 0.08 0.10 -0.39

2002 0.23 -0.17 0.13 0.11 -0.04 0.11 -0.06 -0.07 0.21 -0.18 -0.12 -0.01

2003 0.06 0.05 -0.04 0.09 -0.08 0.13 -0.28 0.39 -0.25 0.07 0.07 0.02

2004 0.15 0.20 -0.36 0.35 -0.04 -0.36 0.21 -0.19 0.06 0.00 -0.04 -0.15

2005 0.26 -0.37 0.34 -0.22 0.04 0.12 -0.19 0.12 0.01 0.07 -0.03 0.13

2006 -0.36 0.21 -0.19 -0.01 0.10 -0.01 0.04 -0.11 -0.14 0.20 0.08 -0.12

2007 0.22 -0.22 0.14 0.04 0.03 -0.09 0.06 0.17 0.11 -0.17 -0.20 0.20

2008 0.06 -0.09 -0.09 -0.04 0.01 0.11 0.00 -0.19 -0.03 -0.16 0.08 -0.32

2009 -0.09 0.15 0.08 0.00 0.02 -0.15 -0.05 0.13 -0.02 -0.01 0.02 0.02

2010 0.08 -0.16 0.27 -0.27 -0.03 0.19 0.03 0.09 0.01 0.13 -0.12 -0.21

2011 0.07 0.03 -0.48 0.42 0.07 -0.15 0.08 -0.10 0.09 0.04 -0.12 0.27

2012 -0.16 0.29 0.09 -0.03 -0.15 0.06 -0.06 -0.02 0.00 0.01 0.07 0.03

2013 0.09 -0.08 0.22 -0.29 0.04 0.01 -0.09 0.07 0.23 -0.24 0.00 -0.03

2014 0.09 -0.15 0.41 -0.42 -0.09 0.24 0.03 -0.14 -0.08 0.19 0.09 -0.10

2015 -0.07 0.02 -0.35 0.42 0.30 -0.44 0.10 0.14 -0.28 -0.02 -0.09 -0.06

2016 0.12 0.25 -0.38 0.31 -0.23 -0.12 0.09 -0.06 0.22 -0.03 0.05 0.15

2017 -0.23 0.10 0.04 -0.16 0.28 0.23 -0.28 -0.11 -0.02 0.16 -0.01 -0.09

2018 0.10 -0.38 0.22 0.11 -0.34 0.21 0.11 0.31 -0.25 -0.16 0.04 -0.09

2019 0.23 0.09 0.03 -0.20 0.08 0.18 -0.13 -0.12 0.37

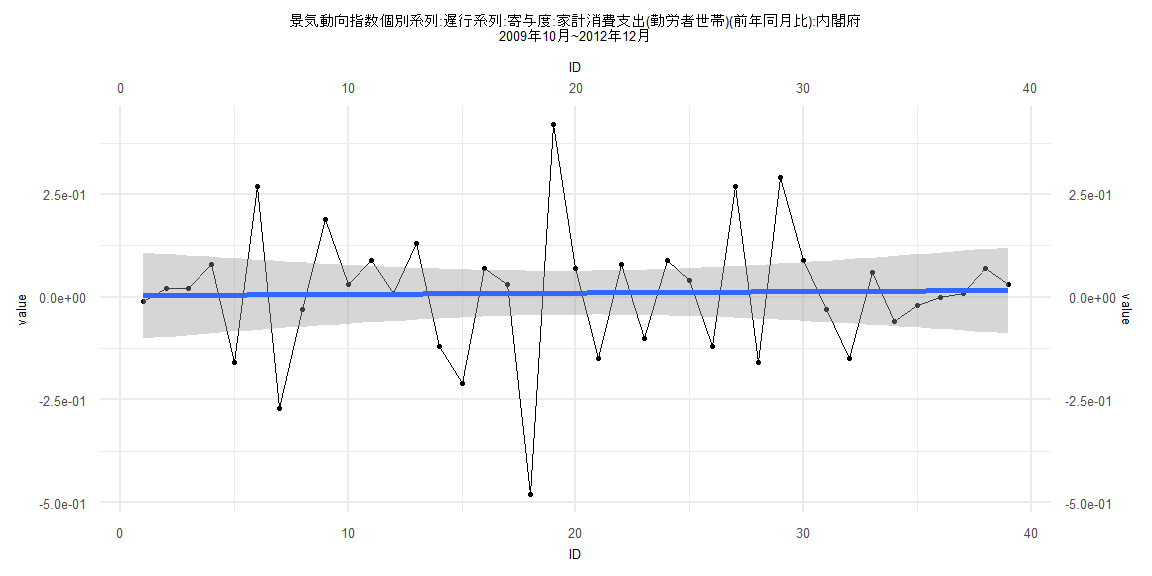

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.48934 -0.09280 0.01561 0.07231 0.41033

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.003401 0.053782 0.063 0.950

ID 0.000330 0.002344 0.141 0.889

Residual standard error: 0.1647 on 37 degrees of freedom

Multiple R-squared: 0.0005355, Adjusted R-squared: -0.02648

F-statistic: 0.01982 on 1 and 37 DF, p-value: 0.8888

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.8986, p-value = 0.9976

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.30657, df = 1, p-value = 0.5798

Box-Ljung test

data: lm_residuals

X-squared = 8.5013, df = 1, p-value = 0.003549

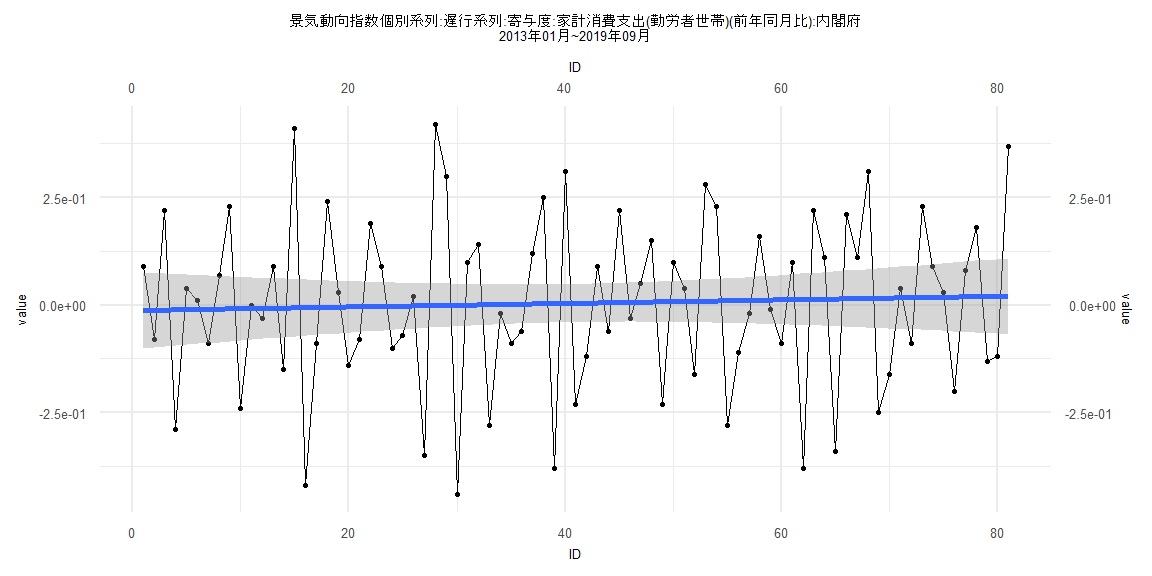

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43989 -0.12486 0.02005 0.13928 0.42094

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0125370 0.0451422 -0.278 0.782

ID 0.0004142 0.0009564 0.433 0.666

Residual standard error: 0.2013 on 79 degrees of freedom

Multiple R-squared: 0.002368, Adjusted R-squared: -0.01026

F-statistic: 0.1875 on 1 and 79 DF, p-value: 0.6662

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.7012, p-value = 0.9992

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.014097, df = 1, p-value = 0.9055

Box-Ljung test

data: lm_residuals

X-squared = 11.584, df = 1, p-value = 0.000665

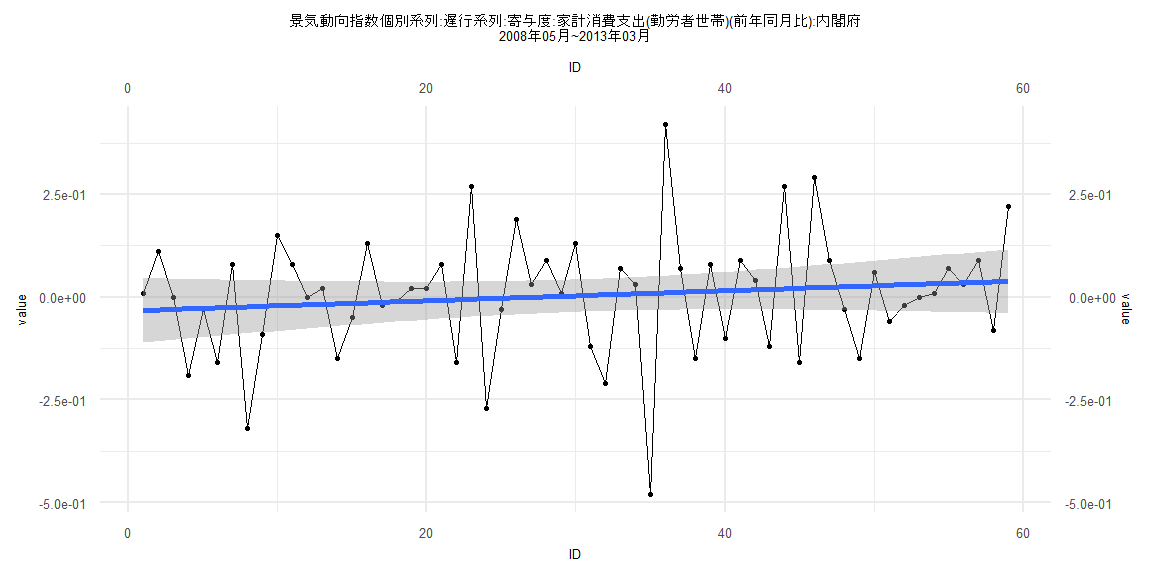

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.48933 -0.10216 0.02189 0.06967 0.40945

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.033442 0.039955 -0.837 0.406

ID 0.001222 0.001158 1.055 0.296

Residual standard error: 0.1515 on 57 degrees of freedom

Multiple R-squared: 0.01916, Adjusted R-squared: 0.00195

F-statistic: 1.113 on 1 and 57 DF, p-value: 0.2958

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.7258, p-value = 0.9971

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.050214, df = 1, p-value = 0.8227

Box-Ljung test

data: lm_residuals

X-squared = 8.7798, df = 1, p-value = 0.003046

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43314 -0.12506 0.01936 0.13896 0.42823

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0252914 0.0463848 -0.545 0.587

ID 0.0006825 0.0010202 0.669 0.506

Residual standard error: 0.2029 on 76 degrees of freedom

Multiple R-squared: 0.005854, Adjusted R-squared: -0.007227

F-statistic: 0.4475 on 1 and 76 DF, p-value: 0.5055

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.81

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.6423, p-value = 0.9975

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.1109, df = 1, p-value = 0.7391

Box-Ljung test

data: lm_residuals

X-squared = 9.9915, df = 1, p-value = 0.001573