Analysis

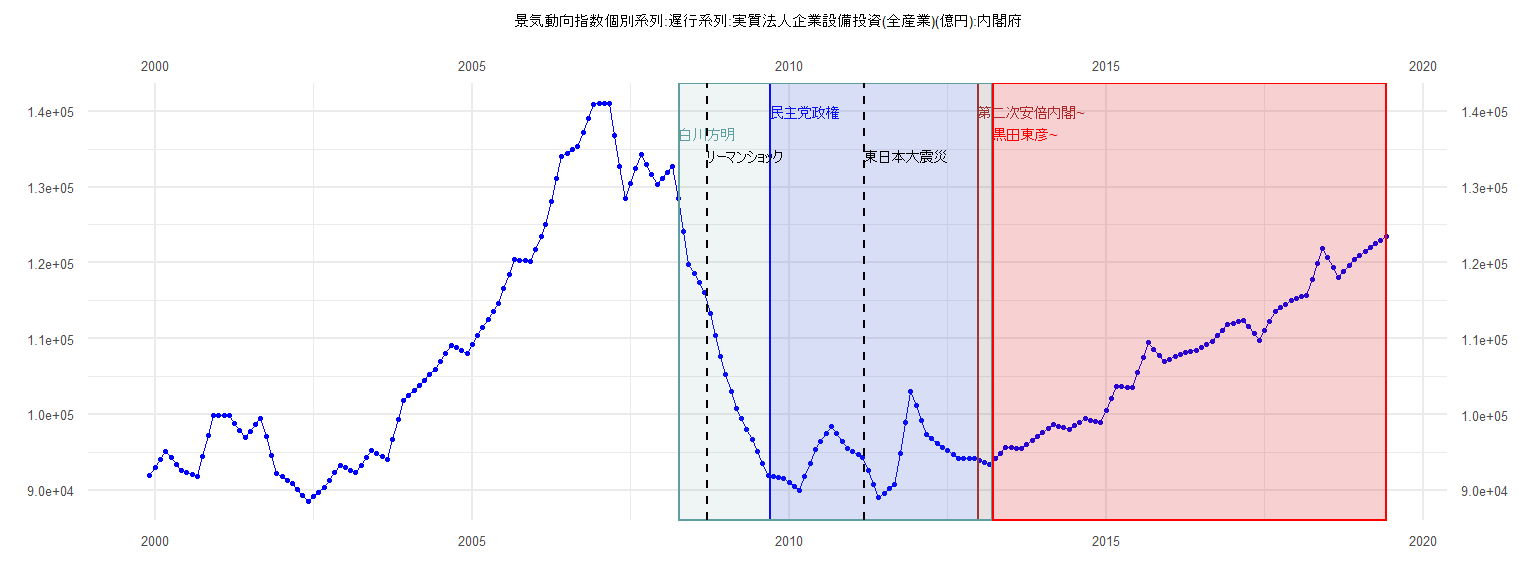

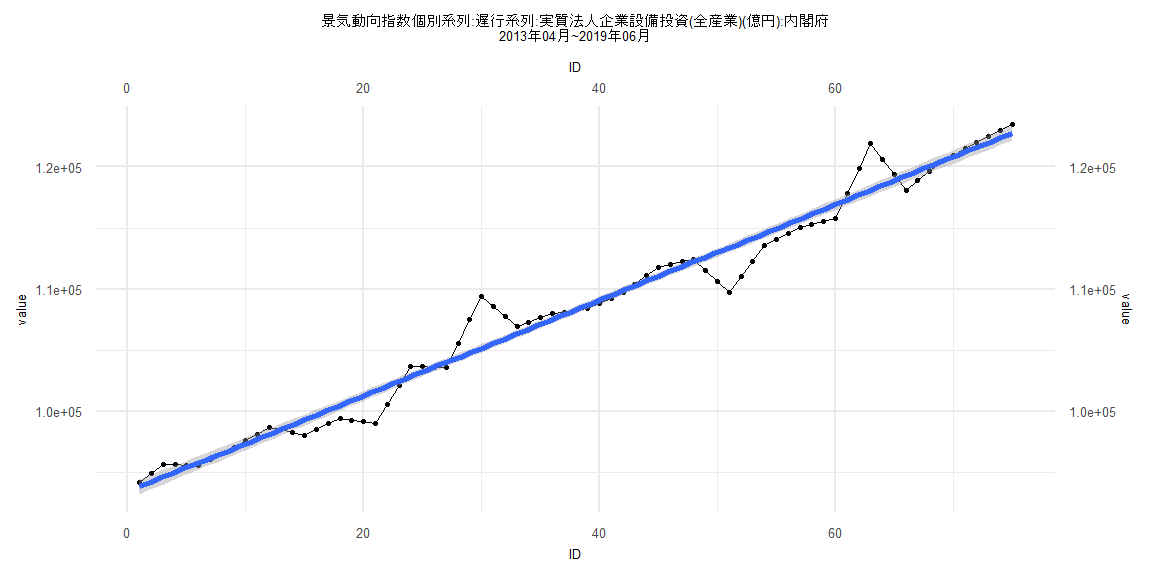

[1] "景気動向指数個別系列:遅行系列:実質法人企業設備投資(全産業)(億円):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 92001

2000 93043 94084 95126 94264 93402 92540 92299 92057 91816 94501 97185 99870

2001 99846 99821 99797 98833 97869 96905 97771 98637 99503 97072 94641 92210

2002 91771 91331 90892 90119 89345 88572 89154 89735 90317 91299 92282 93264

2003 92945 92625 92306 93302 94297 95293 94898 94503 94108 96697 99286 101875

2004 102516 103157 103798 104526 105254 105982 107030 108078 109126 108764 108402 108040

2005 109197 110355 111512 112547 113582 114617 116555 118494 120432 120342 120253 120163

2006 121814 123465 125116 128097 131079 134060 134483 134905 135328 137196 139065 140933

2007 140959 140985 141011 136851 132690 128530 130457 132383 134310 133004 131699 130393

2008 131180 131966 132753 128430 124107 119784 118572 117360 116148 113292 110435 107579

2009 105304 103030 100755 99408 98060 96713 95139 93565 91991 91825 91658 91492

2010 90982 90471 89961 91775 93588 95402 96412 97422 98432 97447 96462 95477

2011 95099 94721 94343 92581 90819 89057 89616 90175 90734 94830 98926 103022

2012 101141 99260 97379 96804 96230 95655 95177 94699 94221 94209 94198 94186

2013 93909 93632 93355 94122 94889 95656 95611 95566 95521 96022 96523 97024

2014 97571 98118 98665 98455 98246 98036 98496 98955 99415 99263 99110 98958

2015 100530 102101 103673 103632 103591 103550 105508 107466 109424 108600 107775 106951

2016 107290 107630 107969 108114 108260 108405 108829 109254 109678 110386 111095 111803

2017 112018 112232 112447 111539 110632 109724 111009 112294 113579 114062 114544 115027

2018 115266 115504 115743 117804 119866 121927 120650 119373 118096 118868 119640 120412

2019 120948 121484 122020 122505 122990 123475

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-5549.5 -1962.7 -162.7 1928.8 7836.2

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 92578.84 1017.83 90.957 <0.0000000000000002 ***

ID 96.56 44.35 2.177 0.0359 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3117 on 37 degrees of freedom

Multiple R-squared: 0.1136, Adjusted R-squared: 0.08959

F-statistic: 4.74 on 1 and 37 DF, p-value: 0.03593

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.24998, p-value = 0.000000000000001947

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.37913, df = 1, p-value = 0.5381

Box-Ljung test

data: lm_residuals

X-squared = 31.669, df = 1, p-value = 0.00000001829

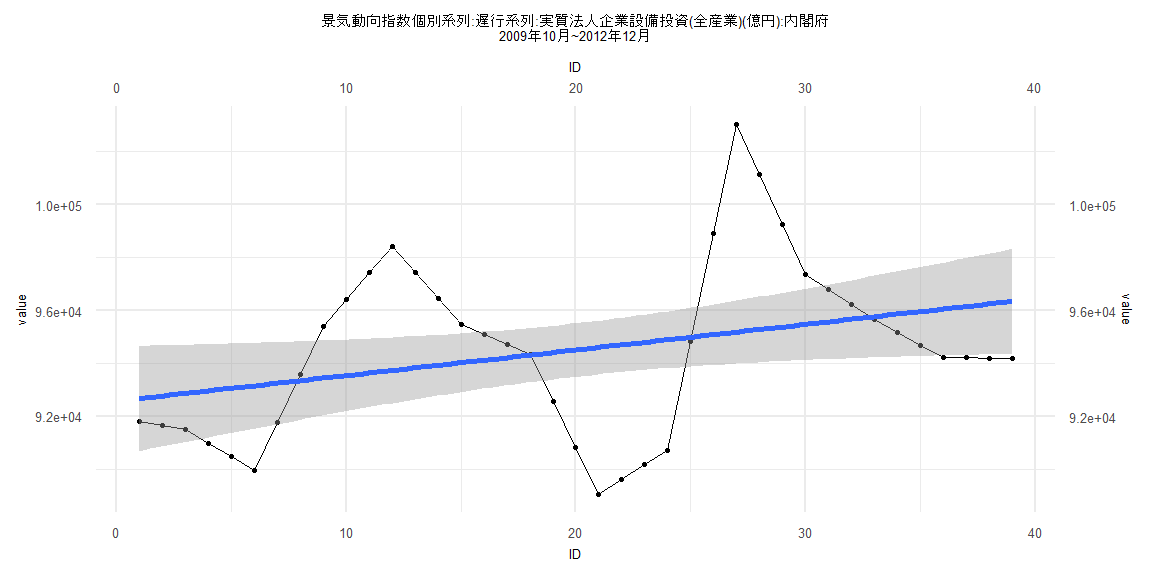

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-3652.4 -773.6 76.9 541.5 4236.8

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 92318.453 305.622 302.07 <0.0000000000000002 ***

ID 389.961 6.722 58.01 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1337 on 76 degrees of freedom

Multiple R-squared: 0.9779, Adjusted R-squared: 0.9776

F-statistic: 3366 on 1 and 76 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.21795, p-value = 0.04892

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.33803, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.72727, df = 1, p-value = 0.3938

Box-Ljung test

data: lm_residuals

X-squared = 54.978, df = 1, p-value = 0.0000000000001219

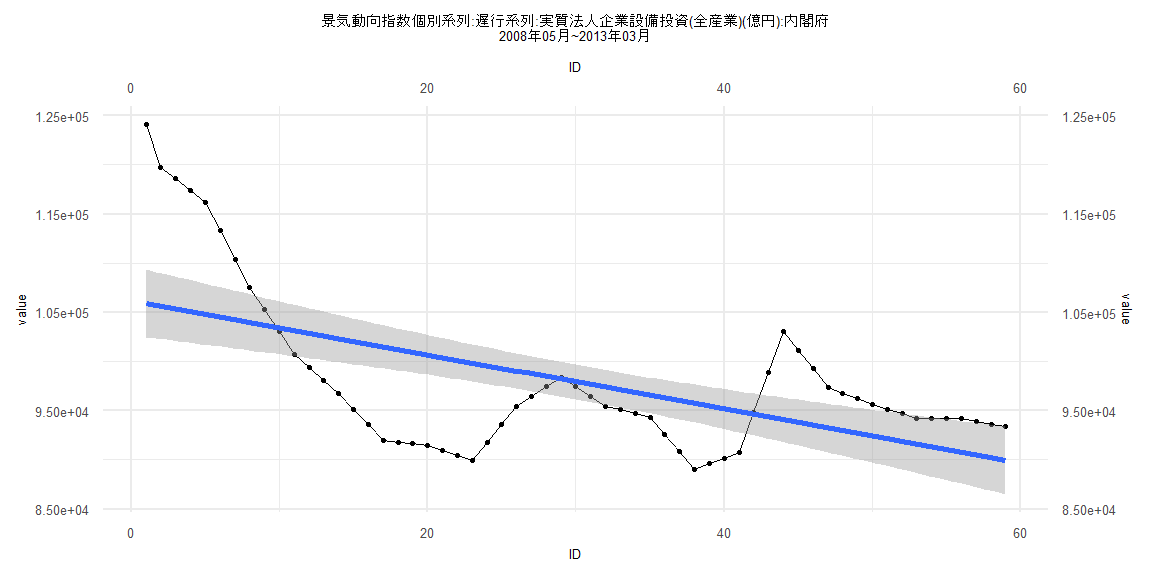

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-9900.9 -5093.0 -485.6 3476.4 18181.9

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 106200.71 1765.90 60.140 < 0.0000000000000002 ***

ID -275.60 51.19 -5.384 0.00000143 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6696 on 57 degrees of freedom

Multiple R-squared: 0.3371, Adjusted R-squared: 0.3255

F-statistic: 28.99 on 1 and 57 DF, p-value: 0.000001432

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.18644, p-value = 0.2582

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.060126, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 17.743, df = 1, p-value = 0.00002528

Box-Ljung test

data: lm_residuals

X-squared = 50.595, df = 1, p-value = 0.000000000001135

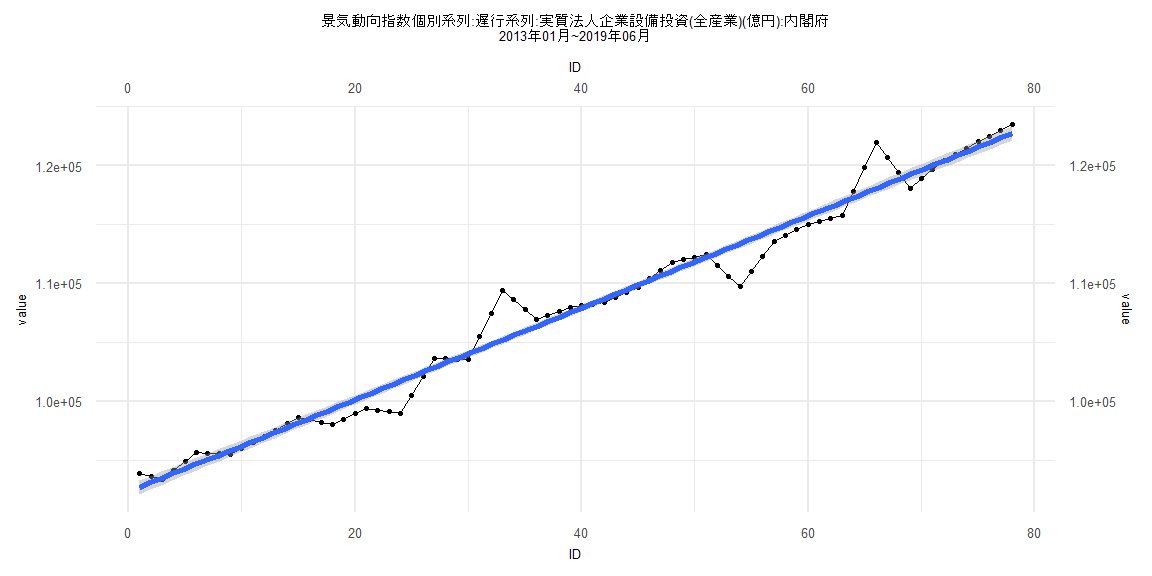

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-3654.6 -824.3 100.0 542.7 4272.7

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 93398.053 315.911 295.65 <0.0000000000000002 ***

ID 391.775 7.223 54.24 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1354 on 73 degrees of freedom

Multiple R-squared: 0.9758, Adjusted R-squared: 0.9755

F-statistic: 2942 on 1 and 73 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17333, p-value = 0.2107

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.3351, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.44422, df = 1, p-value = 0.5051

Box-Ljung test

data: lm_residuals

X-squared = 53.794, df = 1, p-value = 0.0000000000002227