Analysis

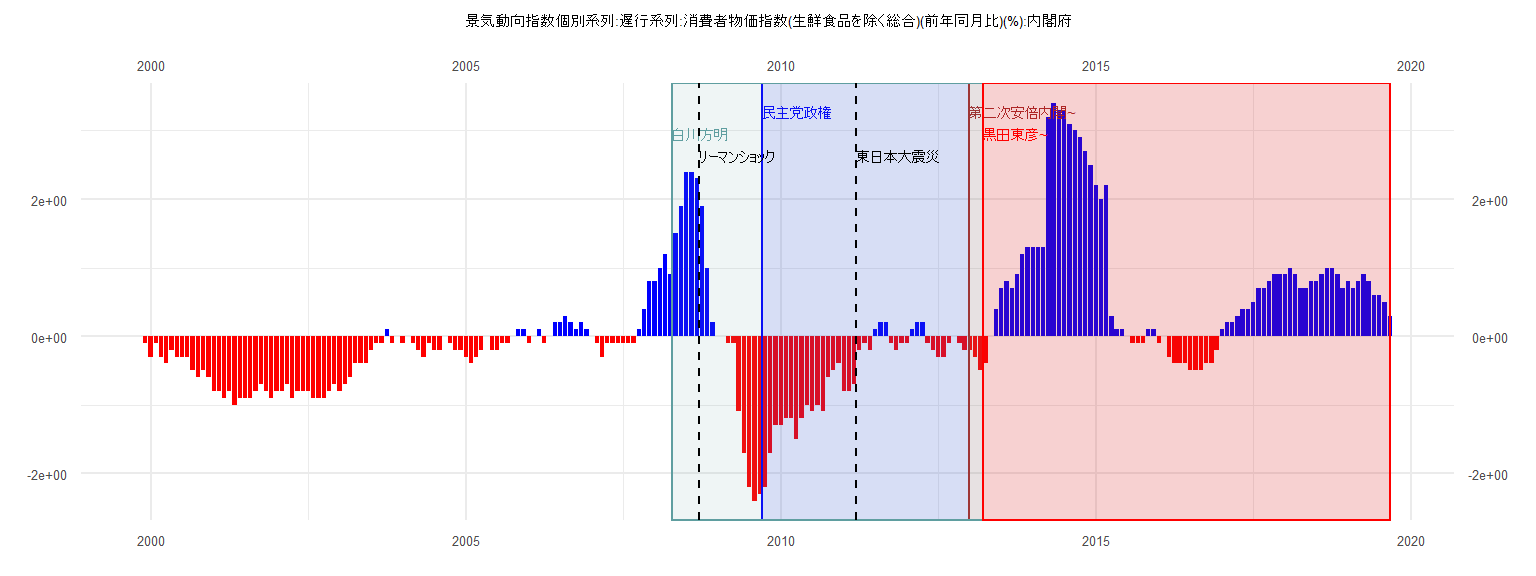

[1] "景気動向指数個別系列:遅行系列:消費者物価指数(生鮮食品を除く総合)(前年同月比)(%):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.1

2000 -0.3 -0.1 -0.3 -0.4 -0.2 -0.3 -0.3 -0.3 -0.5 -0.6 -0.5 -0.6

2001 -0.8 -0.8 -0.9 -0.8 -1.0 -0.9 -0.9 -0.9 -0.8 -0.7 -0.8 -0.9

2002 -0.8 -0.8 -0.7 -0.9 -0.8 -0.8 -0.8 -0.9 -0.9 -0.9 -0.8 -0.7

2003 -0.8 -0.7 -0.6 -0.4 -0.4 -0.4 -0.2 -0.1 -0.1 0.1 -0.1 0.0

2004 -0.1 0.0 -0.1 -0.2 -0.3 -0.1 -0.2 -0.2 0.0 -0.1 -0.2 -0.2

2005 -0.3 -0.4 -0.3 -0.2 0.0 -0.2 -0.2 -0.1 -0.1 0.0 0.1 0.1

2006 -0.1 0.0 0.1 -0.1 0.0 0.2 0.2 0.3 0.2 0.1 0.2 0.1

2007 0.0 -0.1 -0.3 -0.1 -0.1 -0.1 -0.1 -0.1 -0.1 0.1 0.4 0.8

2008 0.8 1.0 1.2 0.9 1.5 1.9 2.4 2.4 2.3 1.9 1.0 0.2

2009 0.0 0.0 -0.1 -0.1 -1.1 -1.7 -2.2 -2.4 -2.3 -2.2 -1.7 -1.3

2010 -1.3 -1.2 -1.2 -1.5 -1.2 -1.0 -1.1 -1.0 -1.1 -0.6 -0.5 -0.4

2011 -0.8 -0.8 -0.7 -0.2 -0.1 -0.2 0.1 0.2 0.2 -0.1 -0.2 -0.1

2012 -0.1 0.1 0.2 0.2 -0.1 -0.2 -0.3 -0.3 -0.1 0.0 -0.1 -0.2

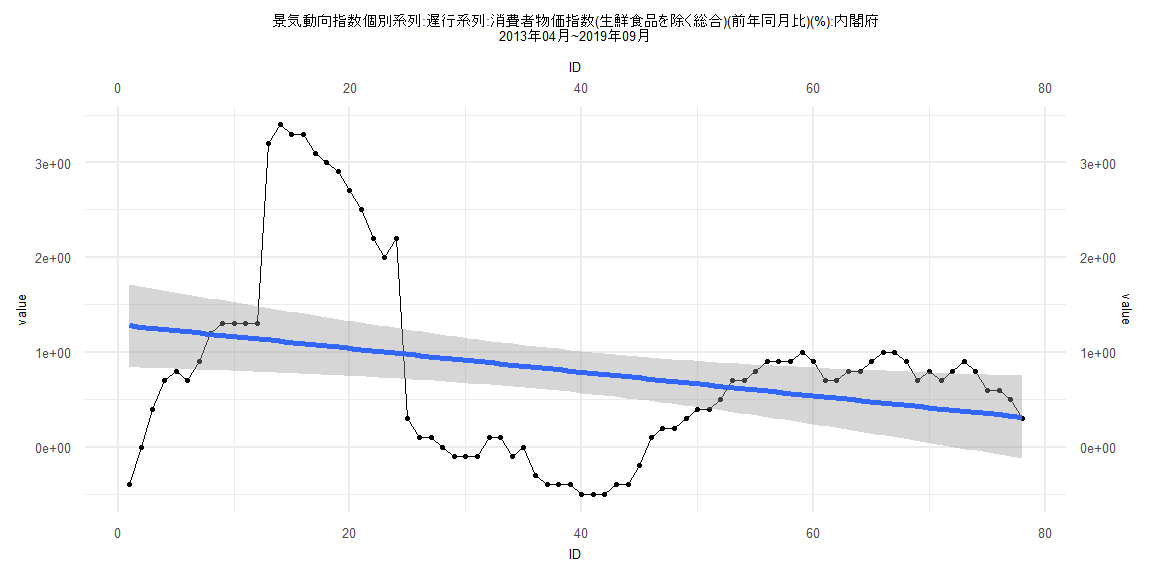

2013 -0.2 -0.3 -0.5 -0.4 0.0 0.4 0.7 0.8 0.7 0.9 1.2 1.3

2014 1.3 1.3 1.3 3.2 3.4 3.3 3.3 3.1 3.0 2.9 2.7 2.5

2015 2.2 2.0 2.2 0.3 0.1 0.1 0.0 -0.1 -0.1 -0.1 0.1 0.1

2016 -0.1 0.0 -0.3 -0.4 -0.4 -0.4 -0.5 -0.5 -0.5 -0.4 -0.4 -0.2

2017 0.1 0.2 0.2 0.3 0.4 0.4 0.5 0.7 0.7 0.8 0.9 0.9

2018 0.9 1.0 0.9 0.7 0.7 0.8 0.8 0.9 1.0 1.0 0.9 0.7

2019 0.8 0.7 0.8 0.9 0.8 0.6 0.6 0.5 0.3

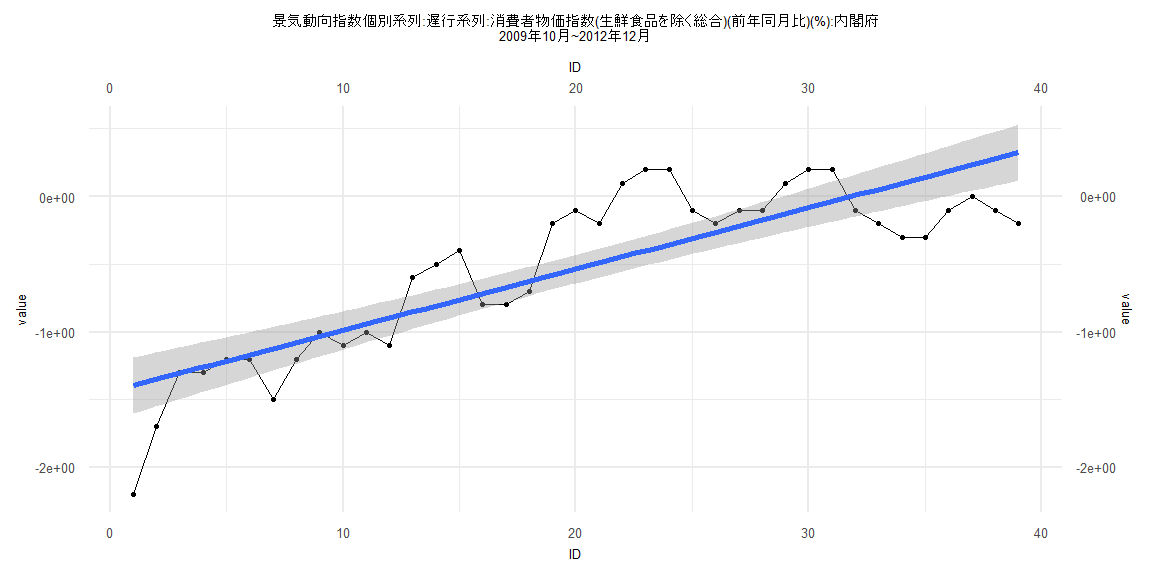

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.80333 -0.21797 -0.02985 0.24529 0.59999

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -1.441970 0.106425 -13.549 0.000000000000000643 ***

ID 0.045304 0.004637 9.769 0.000000000008637938 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3259 on 37 degrees of freedom

Multiple R-squared: 0.7206, Adjusted R-squared: 0.7131

F-statistic: 95.44 on 1 and 37 DF, p-value: 0.000000000008638

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.43675, p-value = 0.0000000001134

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.082674, df = 1, p-value = 0.7737

Box-Ljung test

data: lm_residuals

X-squared = 18.58, df = 1, p-value = 0.00001629

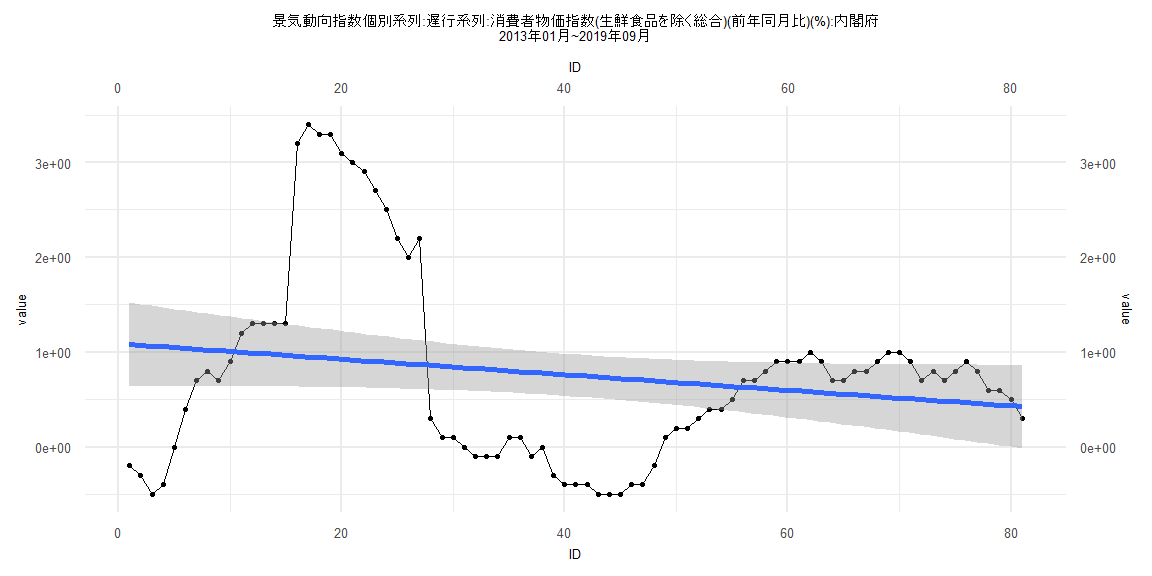

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.56452 -0.77767 0.06985 0.32722 2.45022

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.089105 0.224789 4.845 0.0000062 ***

ID -0.008196 0.004763 -1.721 0.0892 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.002 on 79 degrees of freedom

Multiple R-squared: 0.03613, Adjusted R-squared: 0.02393

F-statistic: 2.961 on 1 and 79 DF, p-value: 0.0892

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12346, p-value = 0.5705

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.11347, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 18.231, df = 1, p-value = 0.00001957

Box-Ljung test

data: lm_residuals

X-squared = 73.127, df = 1, p-value < 0.00000000000000022

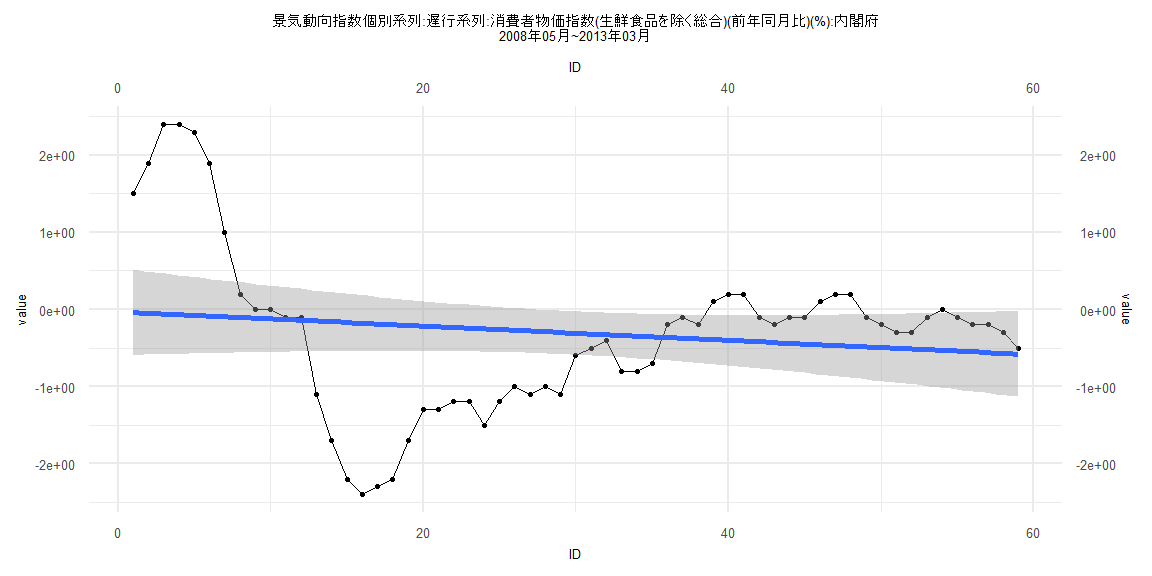

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-2.2217 -0.7648 0.1829 0.4316 2.4667

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.029515 0.283536 -0.104 0.917

ID -0.009299 0.008219 -1.131 0.263

Residual standard error: 1.075 on 57 degrees of freedom

Multiple R-squared: 0.02196, Adjusted R-squared: 0.004802

F-statistic: 1.28 on 1 and 57 DF, p-value: 0.2627

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16949, p-value = 0.3674

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.08481, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 23.199, df = 1, p-value = 0.000001461

Box-Ljung test

data: lm_residuals

X-squared = 54.78, df = 1, p-value = 0.0000000000001348

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.6765 -0.8512 0.1051 0.4054 2.2862

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.288978 0.223186 5.775 0.000000159 ***

ID -0.012509 0.004909 -2.548 0.0128 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9761 on 76 degrees of freedom

Multiple R-squared: 0.07872, Adjusted R-squared: 0.06659

F-statistic: 6.494 on 1 and 76 DF, p-value: 0.01284

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.21795, p-value = 0.04892

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.12373, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 18.53, df = 1, p-value = 0.00001673

Box-Ljung test

data: lm_residuals

X-squared = 68.402, df = 1, p-value < 0.00000000000000022