Analysis

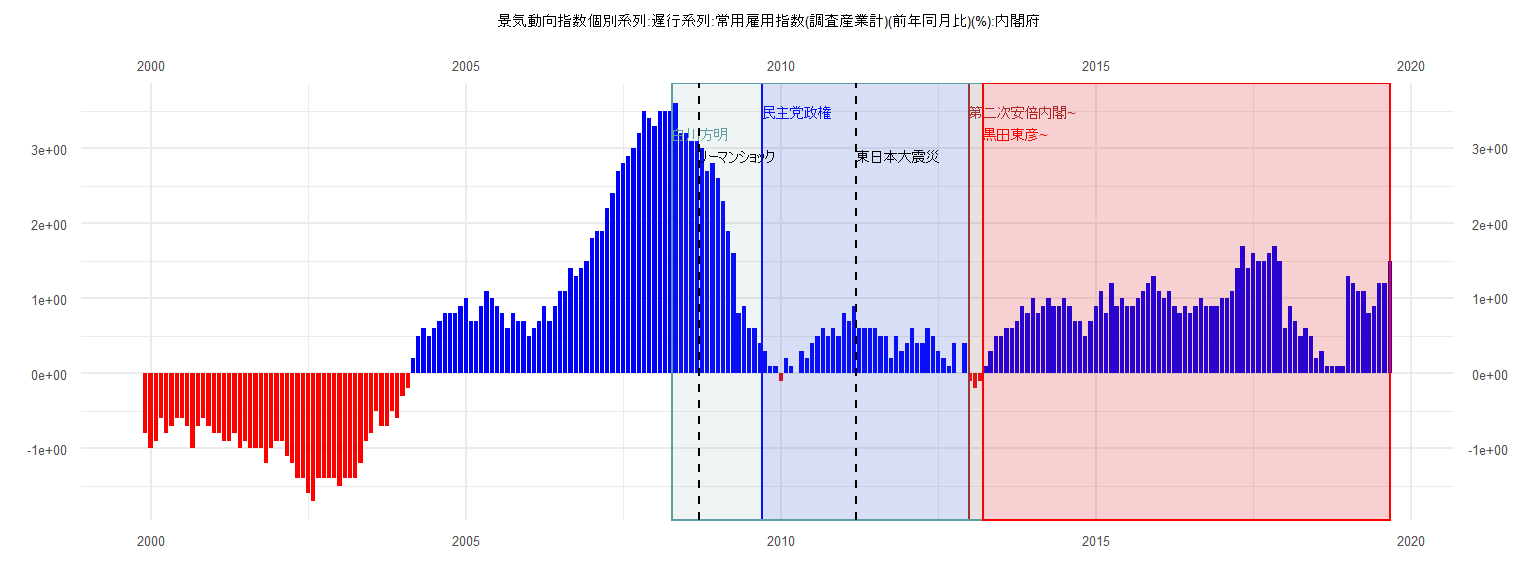

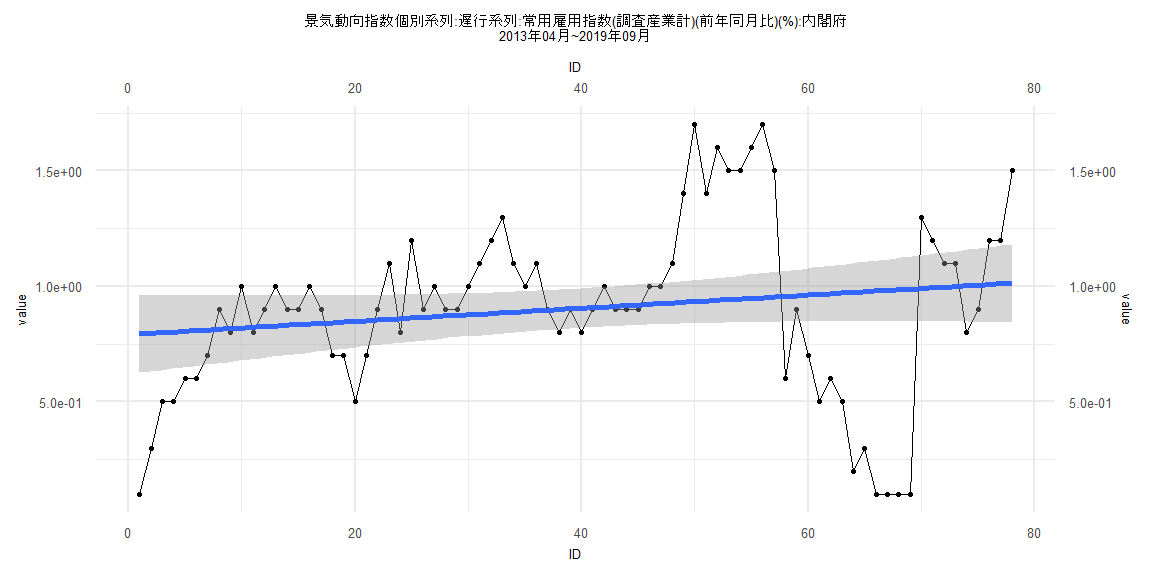

[1] "景気動向指数個別系列:遅行系列:常用雇用指数(調査産業計)(前年同月比)(%):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 -0.8

2000 -1.0 -0.9 -0.6 -0.8 -0.7 -0.6 -0.6 -0.7 -1.0 -0.7 -0.6 -0.7

2001 -0.8 -0.8 -0.9 -0.9 -0.8 -1.0 -0.9 -1.0 -1.0 -1.0 -1.2 -1.0

2002 -0.9 -0.9 -1.1 -1.2 -1.4 -1.4 -1.6 -1.7 -1.4 -1.4 -1.4 -1.4

2003 -1.5 -1.4 -1.4 -1.4 -1.2 -0.9 -0.8 -0.5 -0.7 -0.7 -0.5 -0.6

2004 -0.3 -0.2 0.2 0.5 0.6 0.5 0.6 0.7 0.8 0.8 0.8 0.9

2005 1.0 0.7 0.7 0.9 1.1 1.0 0.9 0.8 0.6 0.8 0.7 0.7

2006 0.5 0.6 0.7 0.9 0.7 0.9 1.1 1.1 1.4 1.3 1.4 1.5

2007 1.8 1.9 1.9 2.2 2.4 2.7 2.8 2.9 3.0 3.2 3.5 3.4

2008 3.3 3.5 3.5 3.5 3.6 3.2 3.2 3.1 3.1 3.0 2.7 2.8

2009 2.6 2.3 1.9 1.6 0.8 0.9 0.6 0.6 0.4 0.3 0.1 0.1

2010 -0.1 0.2 0.1 0.0 0.3 0.2 0.4 0.5 0.6 0.5 0.6 0.5

2011 0.8 0.7 0.9 0.6 0.6 0.6 0.6 0.5 0.5 0.2 0.5 0.3

2012 0.4 0.6 0.4 0.4 0.6 0.5 0.3 0.2 0.1 0.4 0.0 0.4

2013 -0.1 -0.2 -0.1 0.1 0.3 0.5 0.5 0.6 0.6 0.7 0.9 0.8

2014 1.0 0.8 0.9 1.0 0.9 0.9 1.0 0.9 0.7 0.7 0.5 0.7

2015 0.9 1.1 0.8 1.2 0.9 1.0 0.9 0.9 1.0 1.1 1.2 1.3

2016 1.1 1.0 1.1 0.9 0.8 0.9 0.8 0.9 1.0 0.9 0.9 0.9

2017 1.0 1.0 1.1 1.4 1.7 1.4 1.6 1.5 1.5 1.6 1.7 1.5

2018 0.6 0.9 0.7 0.5 0.6 0.5 0.2 0.3 0.1 0.1 0.1 0.1

2019 1.3 1.2 1.1 1.1 0.8 0.9 1.2 1.2 1.5

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.45645 -0.15040 -0.02224 0.16921 0.51197

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.326451 0.075173 4.343 0.000105 ***

ID 0.003421 0.003276 1.044 0.303075

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2302 on 37 degrees of freedom

Multiple R-squared: 0.02864, Adjusted R-squared: 0.002383

F-statistic: 1.091 on 1 and 37 DF, p-value: 0.3031

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.73924, p-value = 0.000001452

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.33666, df = 1, p-value = 0.5618

Box-Ljung test

data: lm_residuals

X-squared = 16.661, df = 1, p-value = 0.00004469

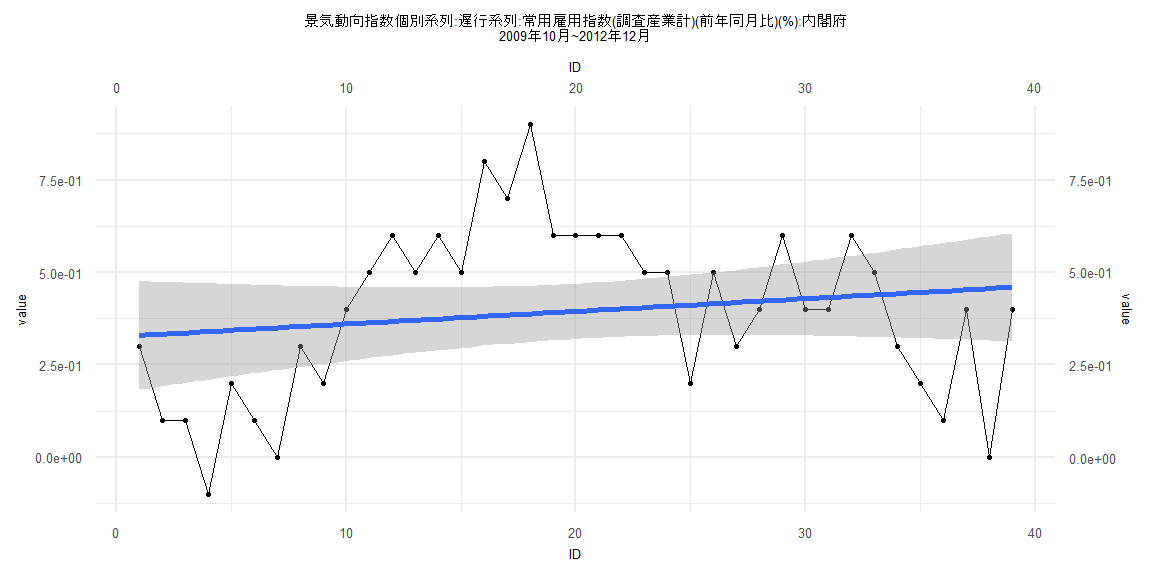

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.92911 -0.16079 0.08209 0.24513 0.77121

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.648951 0.091157 7.119 0.000000000442 ***

ID 0.005280 0.001931 2.734 0.00772 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4064 on 79 degrees of freedom

Multiple R-squared: 0.08643, Adjusted R-squared: 0.07486

F-statistic: 7.474 on 1 and 79 DF, p-value: 0.007724

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.22222, p-value = 0.03633

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.33454, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 4.3968, df = 1, p-value = 0.03601

Box-Ljung test

data: lm_residuals

X-squared = 54.332, df = 1, p-value = 0.0000000000001693

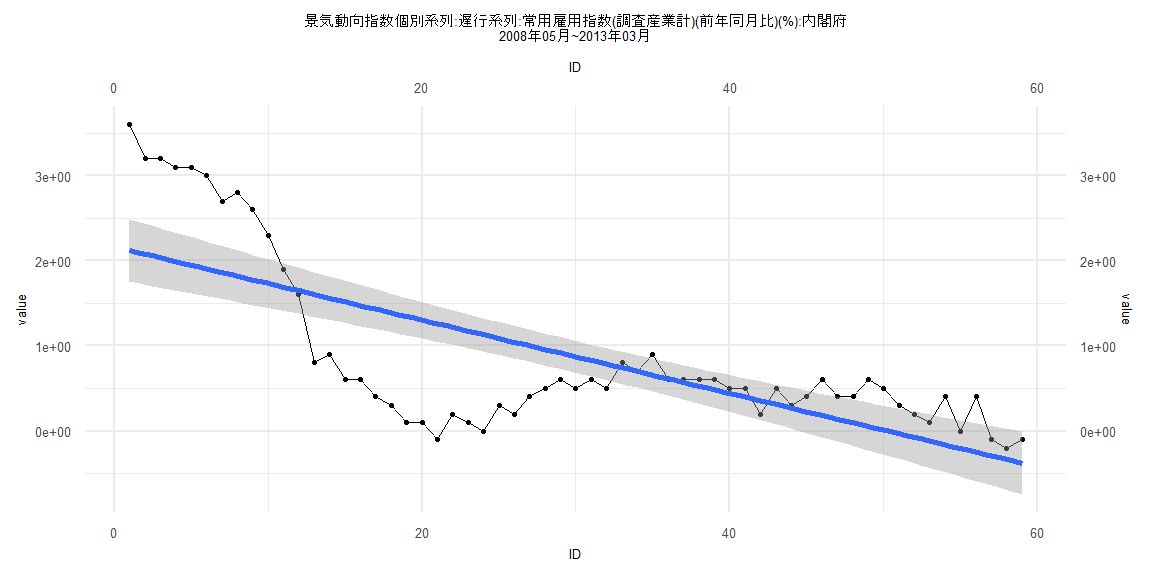

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.3587 -0.5288 0.1025 0.3755 1.4800

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.163063 0.188085 11.500 < 0.0000000000000002 ***

ID -0.043063 0.005452 -7.898 0.000000000102 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.7132 on 57 degrees of freedom

Multiple R-squared: 0.5225, Adjusted R-squared: 0.5142

F-statistic: 62.38 on 1 and 57 DF, p-value: 0.0000000001015

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.10206, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 28.248, df = 1, p-value = 0.0000001068

Box-Ljung test

data: lm_residuals

X-squared = 51.37, df = 1, p-value = 0.0000000000007649

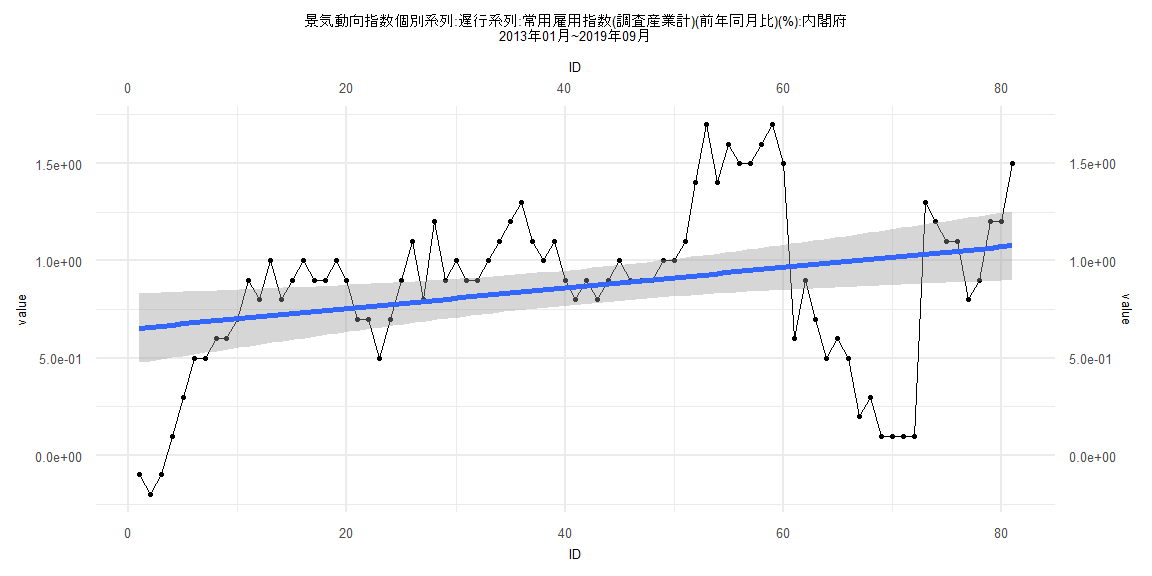

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.88774 -0.14981 0.04024 0.19164 0.76629

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.791508 0.086390 9.162 0.0000000000000654 ***

ID 0.002844 0.001900 1.497 0.139

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3778 on 76 degrees of freedom

Multiple R-squared: 0.02863, Adjusted R-squared: 0.01585

F-statistic: 2.24 on 1 and 76 DF, p-value: 0.1386

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.81

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.39752, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 11.84, df = 1, p-value = 0.0005796

Box-Ljung test

data: lm_residuals

X-squared = 47.812, df = 1, p-value = 0.000000000004691