Analysis

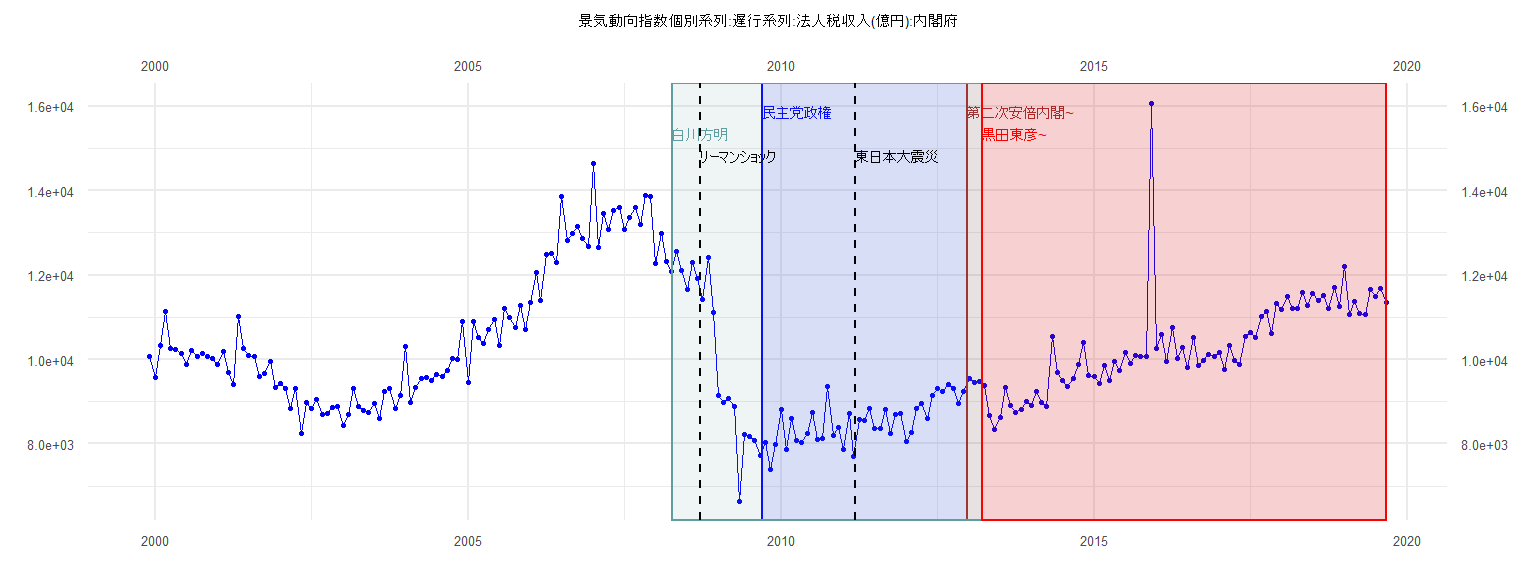

[1] "景気動向指数個別系列:遅行系列:法人税収入(億円):内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 10062

2000 9565 10333 11141 10251 10238 10133 9884 10215 10078 10149 10062 10029

2001 9886 10194 9683 9410 11008 10264 10091 10080 9597 9664 9948 9336

2002 9438 9314 8840 9309 8247 8970 8838 9042 8703 8718 8862 8886

2003 8439 8697 9314 8879 8800 8746 8959 8600 9245 9303 8845 9138

2004 10315 8981 9342 9538 9579 9502 9633 9586 9733 10024 10000 10900

2005 9444 10897 10513 10369 10712 10953 10334 11208 11006 10763 11270 10717

2006 11354 12065 11407 12497 12508 12290 13859 12819 12979 13164 12869 12681

2007 14650 12645 13452 13085 13525 13609 13093 13363 13596 13199 13883 13869

2008 12272 12992 12312 12078 12549 12106 11657 12300 11915 11419 12414 11123

2009 9156 8970 9070 8876 6644 8221 8176 8089 7730 8033 7394 7987

2010 8803 7867 8600 8075 8032 8238 8740 8108 8138 9350 8191 8380

2011 7877 8713 7711 8576 8542 8830 8361 8367 8816 8239 8700 8715

2012 8062 8270 8850 8967 8610 9150 9301 9232 9404 9312 8962 9247

2013 9559 9458 9482 9378 8671 8332 8621 9347 8913 8737 8826 9009

2014 8913 9231 8979 8895 10549 9689 9514 9371 9550 9881 10405 9609

2015 9598 9426 9869 9496 9952 9737 10168 9901 10086 10067 10074 16068

2016 10264 10590 9959 10755 10024 10289 9817 10513 9858 9982 10108 10081

2017 10157 9768 10340 9970 9880 10547 10641 10527 11010 11135 10626 11329

2018 11175 11499 11200 11208 11595 11288 11564 11390 11508 11214 11696 11260

2019 12215 11060 11372 11096 11065 11656 11492 11677 11345

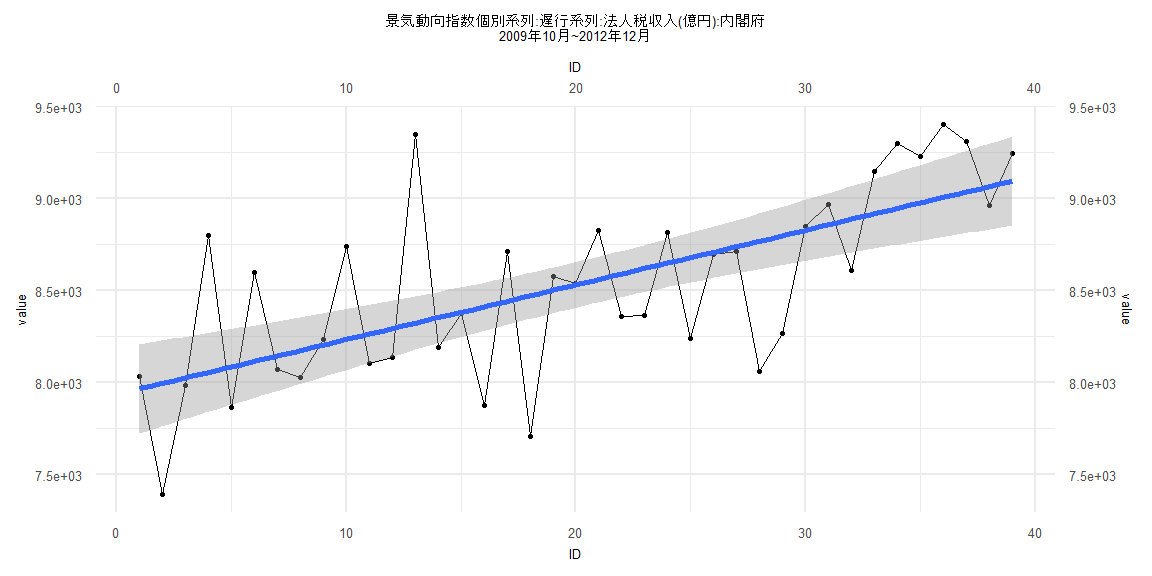

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-761.63 -191.08 -3.49 242.98 1025.93

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 7937.816 124.252 63.885 < 0.0000000000000002 ***

ID 29.712 5.414 5.488 0.0000031 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 380.5 on 37 degrees of freedom

Multiple R-squared: 0.4487, Adjusted R-squared: 0.4338

F-statistic: 30.12 on 1 and 37 DF, p-value: 0.000003102

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.2181, p-value = 0.6974

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.1244, df = 1, p-value = 0.289

Box-Ljung test

data: lm_residuals

X-squared = 0.52364, df = 1, p-value = 0.4693

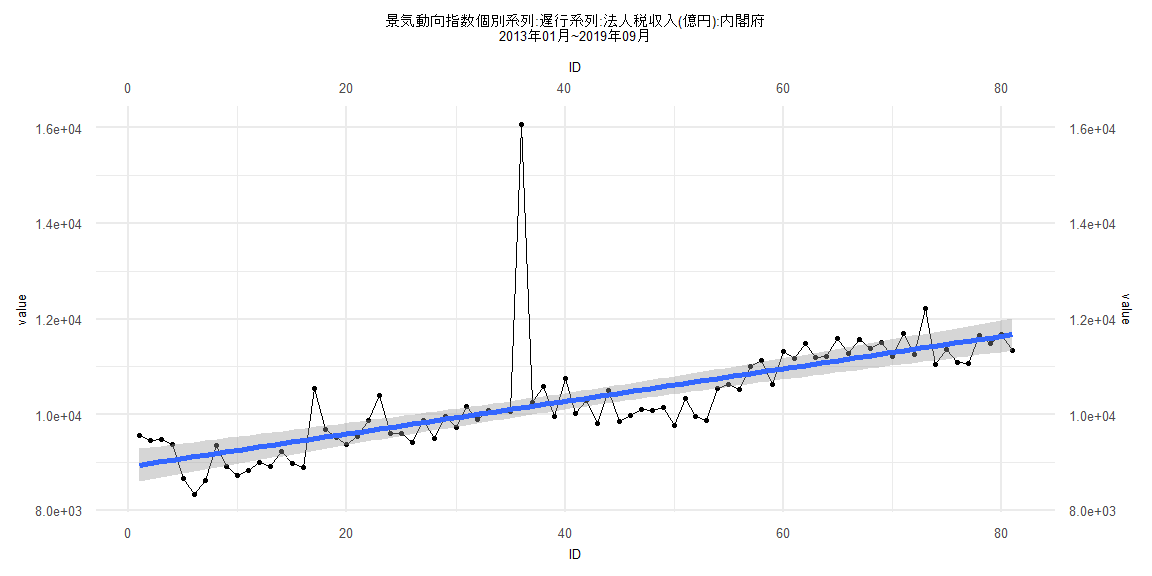

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-848.6 -372.8 -96.6 162.8 5928.4

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8912.791 173.913 51.249 < 0.0000000000000002 ***

ID 34.077 3.685 9.248 0.0000000000000319 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 775.4 on 79 degrees of freedom

Multiple R-squared: 0.5198, Adjusted R-squared: 0.5138

F-statistic: 85.53 on 1 and 79 DF, p-value: 0.0000000000000319

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.24691, p-value = 0.01405

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.8066, p-value = 0.1608

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.080485, df = 1, p-value = 0.7766

Box-Ljung test

data: lm_residuals

X-squared = 0.70574, df = 1, p-value = 0.4009

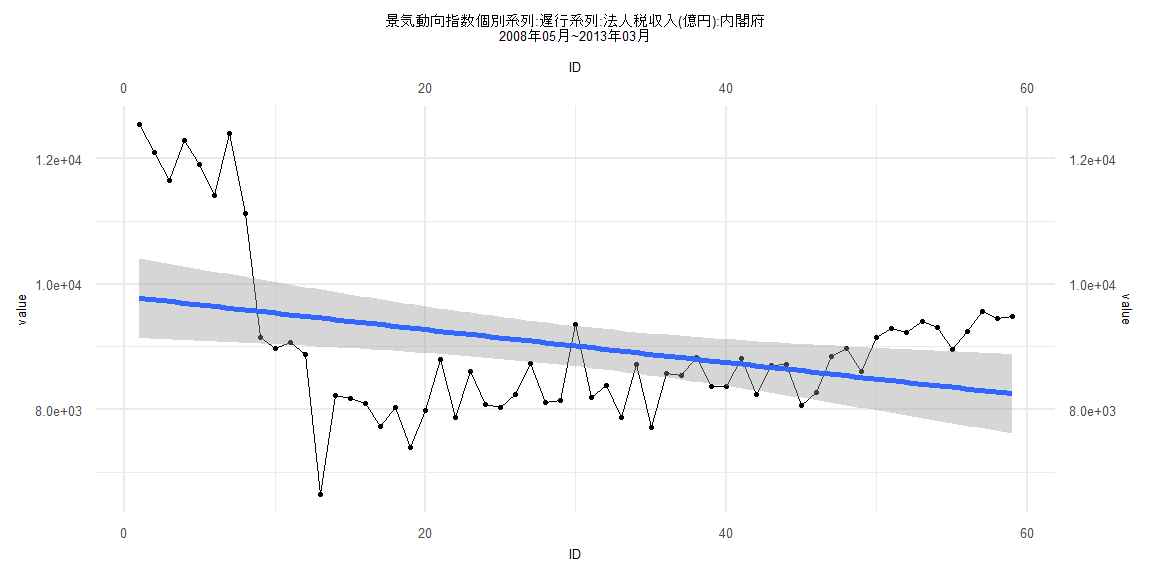

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-2814.7 -889.0 -320.2 821.1 2797.4

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 9800.793 326.158 30.049 < 0.0000000000000002 ***

ID -26.318 9.455 -2.784 0.00728 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1237 on 57 degrees of freedom

Multiple R-squared: 0.1197, Adjusted R-squared: 0.1042

F-statistic: 7.748 on 1 and 57 DF, p-value: 0.007282

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16949, p-value = 0.3674

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.31454, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 20.313, df = 1, p-value = 0.000006577

Box-Ljung test

data: lm_residuals

X-squared = 38.712, df = 1, p-value = 0.0000000004912

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-840.7 -360.3 -100.8 148.5 5958.8

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8931.965 178.933 49.918 < 0.0000000000000002 ***

ID 35.675 3.936 9.065 0.0000000000001 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 782.6 on 76 degrees of freedom

Multiple R-squared: 0.5195, Adjusted R-squared: 0.5132

F-statistic: 82.17 on 1 and 76 DF, p-value: 0.0000000000001003

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.26923, p-value = 0.006781

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.8428, p-value = 0.2073

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.10526, df = 1, p-value = 0.7456

Box-Ljung test

data: lm_residuals

X-squared = 0.45994, df = 1, p-value = 0.4977