Analysis

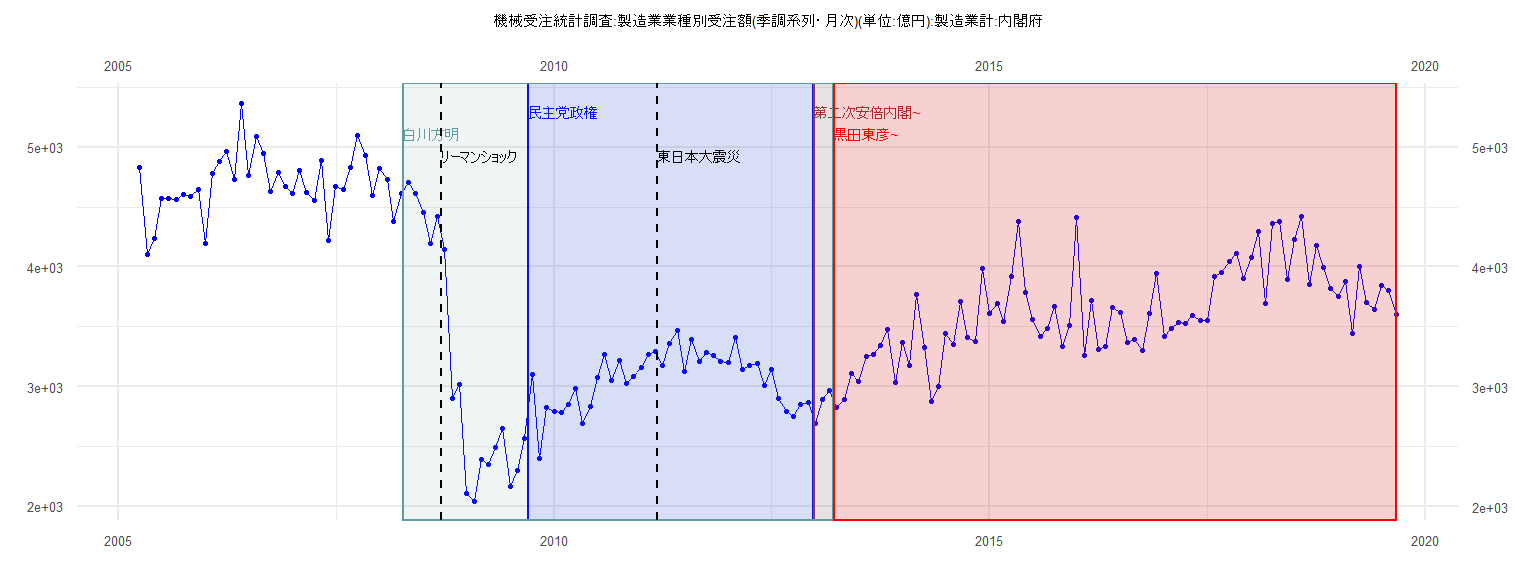

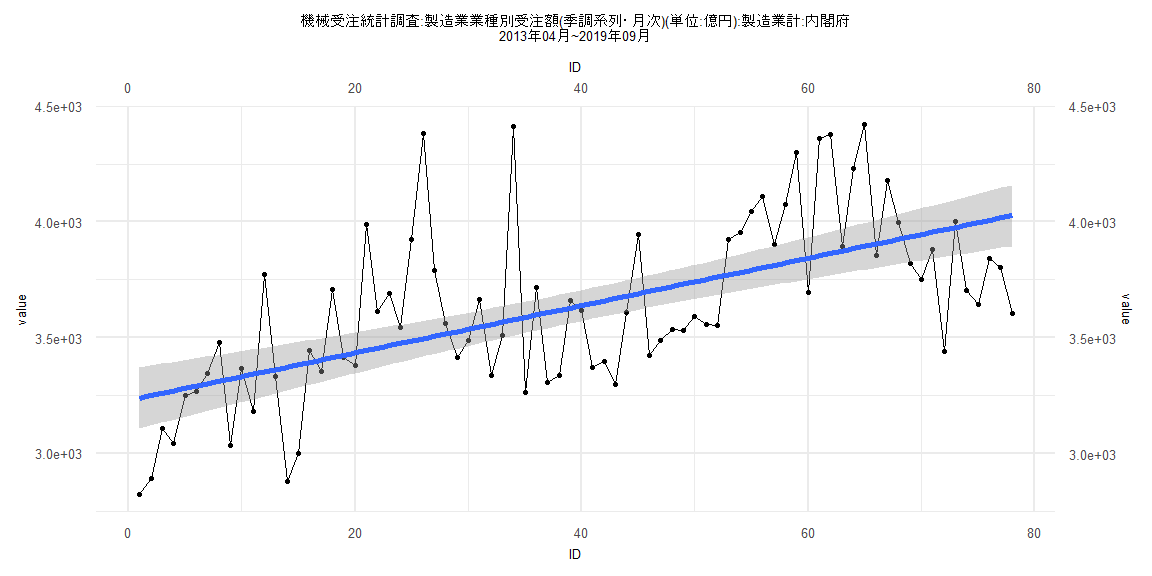

[1] "機械受注統計調査:製造業業種別受注額(季調系列・月次)(単位:億円):製造業計:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 4827.59 4105.29 4239.97 4572.19 4568.84 4563.79 4606.54 4591.43 4646.57

2006 4198.65 4780.75 4881.66 4965.91 4733.10 5364.14 4762.07 5087.51 4944.06 4627.67 4791.50 4673.72

2007 4616.36 4803.53 4623.63 4553.97 4884.60 4219.32 4673.76 4650.19 4832.95 5100.21 4934.39 4592.47

2008 4817.52 4730.37 4377.54 4616.27 4708.66 4609.55 4455.45 4193.51 4417.91 4144.04 2904.49 3014.63

2009 2109.63 2044.04 2387.98 2353.37 2490.26 2650.51 2168.70 2302.45 2568.79 3104.50 2403.28 2823.39

2010 2792.97 2785.22 2849.56 2980.18 2693.84 2834.92 3075.93 3272.20 3050.08 3214.53 3022.25 3085.63

2011 3157.92 3272.26 3290.97 3177.46 3360.80 3468.92 3125.72 3395.22 3207.43 3284.97 3257.13 3212.57

2012 3202.52 3410.16 3138.68 3175.36 3196.85 3005.95 3146.95 2897.91 2794.56 2751.01 2853.34 2864.80

2013 2694.62 2890.38 2964.18 2822.48 2891.48 3107.48 3043.65 3252.08 3268.97 3344.34 3477.77 3034.37

2014 3367.94 3180.30 3772.38 3330.39 2877.68 3001.27 3442.61 3355.39 3707.40 3412.70 3379.67 3989.73

2015 3612.35 3689.95 3543.67 3922.51 4381.48 3789.75 3559.53 3415.32 3488.93 3665.28 3337.79 3507.22

2016 4413.00 3261.08 3715.76 3306.99 3335.68 3660.62 3615.94 3369.74 3396.42 3297.90 3609.49 3947.24

2017 3421.81 3485.81 3534.42 3530.80 3591.64 3554.85 3553.00 3922.26 3953.95 4043.29 4111.17 3904.69

2018 4074.66 4299.41 3695.50 4361.04 4379.89 3893.85 4231.11 4420.94 3854.53 4181.08 3996.80 3821.43

2019 3749.60 3880.73 3439.91 4000.99 3705.95 3643.90 3841.10 3801.85 3603.81

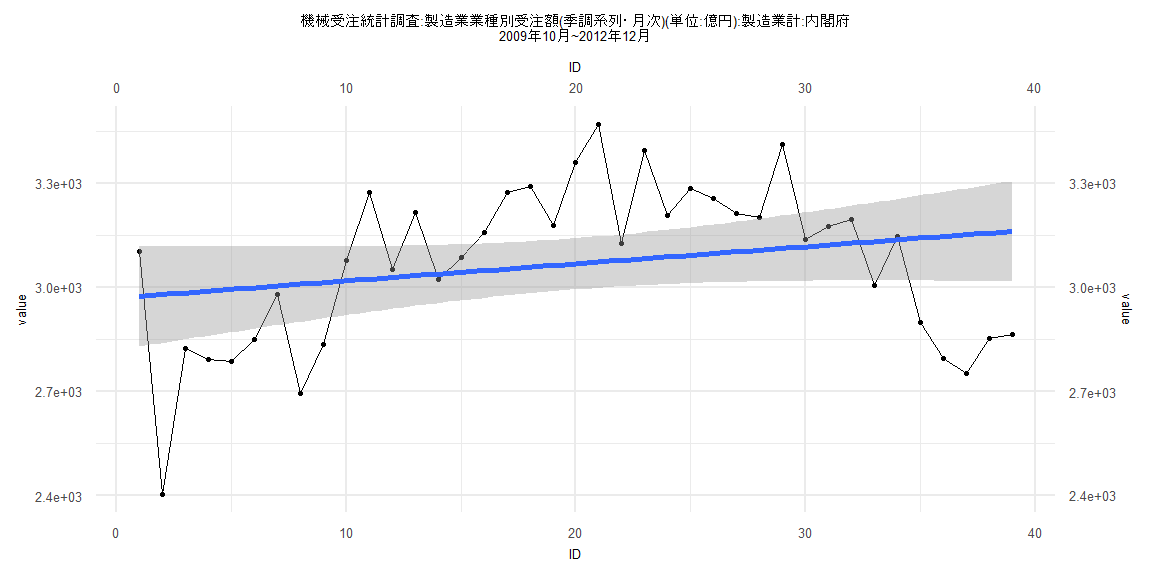

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-575.74 -169.56 48.23 145.18 396.36

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2969.177 74.304 39.960 <0.0000000000000002 ***

ID 4.923 3.238 1.521 0.137

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 227.6 on 37 degrees of freedom

Multiple R-squared: 0.05881, Adjusted R-squared: 0.03338

F-statistic: 2.312 on 1 and 37 DF, p-value: 0.1369

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.82516, p-value = 0.000009001

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.000036185, df = 1, p-value = 0.9952

Box-Ljung test

data: lm_residuals

X-squared = 13.199, df = 1, p-value = 0.0002801

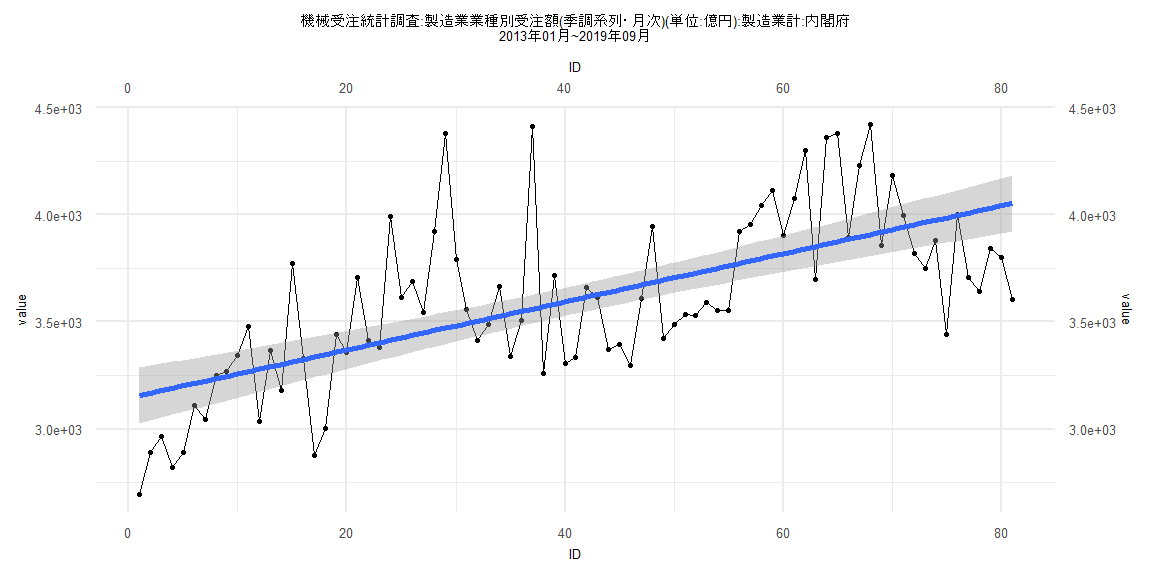

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-545.77 -213.64 -22.54 170.24 911.95

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3144.133 66.996 46.930 < 0.0000000000000002 ***

ID 11.221 1.419 7.905 0.0000000000134 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 298.7 on 79 degrees of freedom

Multiple R-squared: 0.4416, Adjusted R-squared: 0.4346

F-statistic: 62.49 on 1 and 79 DF, p-value: 0.00000000001335

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.2843, p-value = 0.0002687

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.016672, df = 1, p-value = 0.8973

Box-Ljung test

data: lm_residuals

X-squared = 9.0678, df = 1, p-value = 0.002602

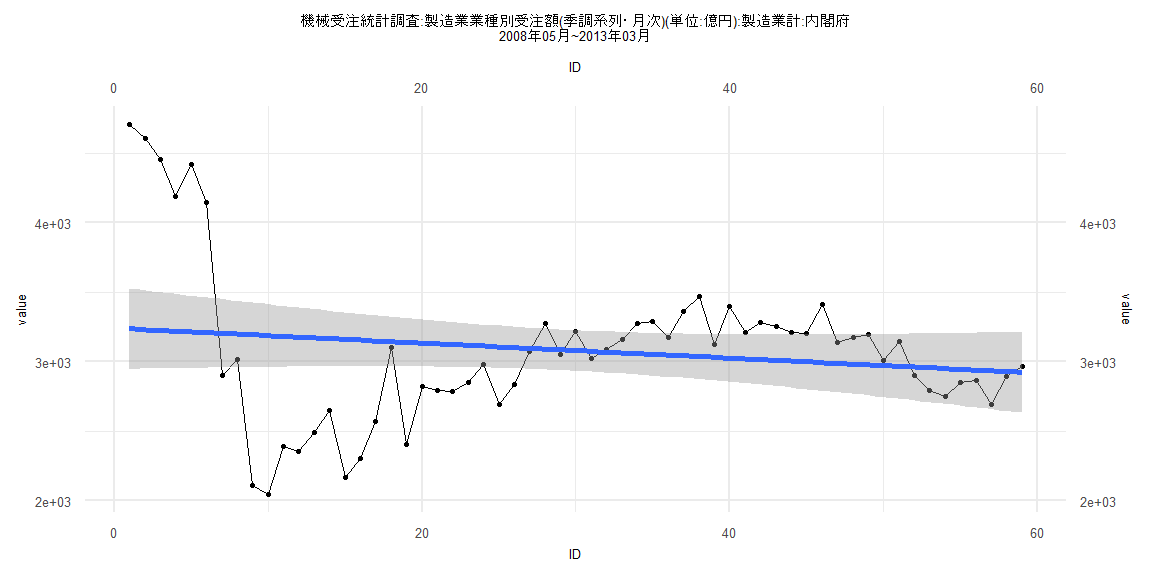

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1143.77 -283.80 -20.11 211.15 1472.27

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3241.792 148.498 21.831 <0.0000000000000002 ***

ID -5.398 4.305 -1.254 0.215

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 563.1 on 57 degrees of freedom

Multiple R-squared: 0.02685, Adjusted R-squared: 0.009774

F-statistic: 1.572 on 1 and 57 DF, p-value: 0.215

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.27692, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 28.181, df = 1, p-value = 0.0000001105

Box-Ljung test

data: lm_residuals

X-squared = 39.864, df = 1, p-value = 0.0000000002722

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-526.1 -213.6 -39.2 165.0 886.5

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3228.687 67.709 47.685 < 0.0000000000000002 ***

ID 10.241 1.489 6.877 0.0000000015 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 296.1 on 76 degrees of freedom

Multiple R-squared: 0.3836, Adjusted R-squared: 0.3754

F-statistic: 47.29 on 1 and 76 DF, p-value: 0.000000001498

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11538, p-value = 0.6802

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.349, p-value = 0.001013

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.010758, df = 1, p-value = 0.9174

Box-Ljung test

data: lm_residuals

X-squared = 7.2457, df = 1, p-value = 0.007107