Analysis

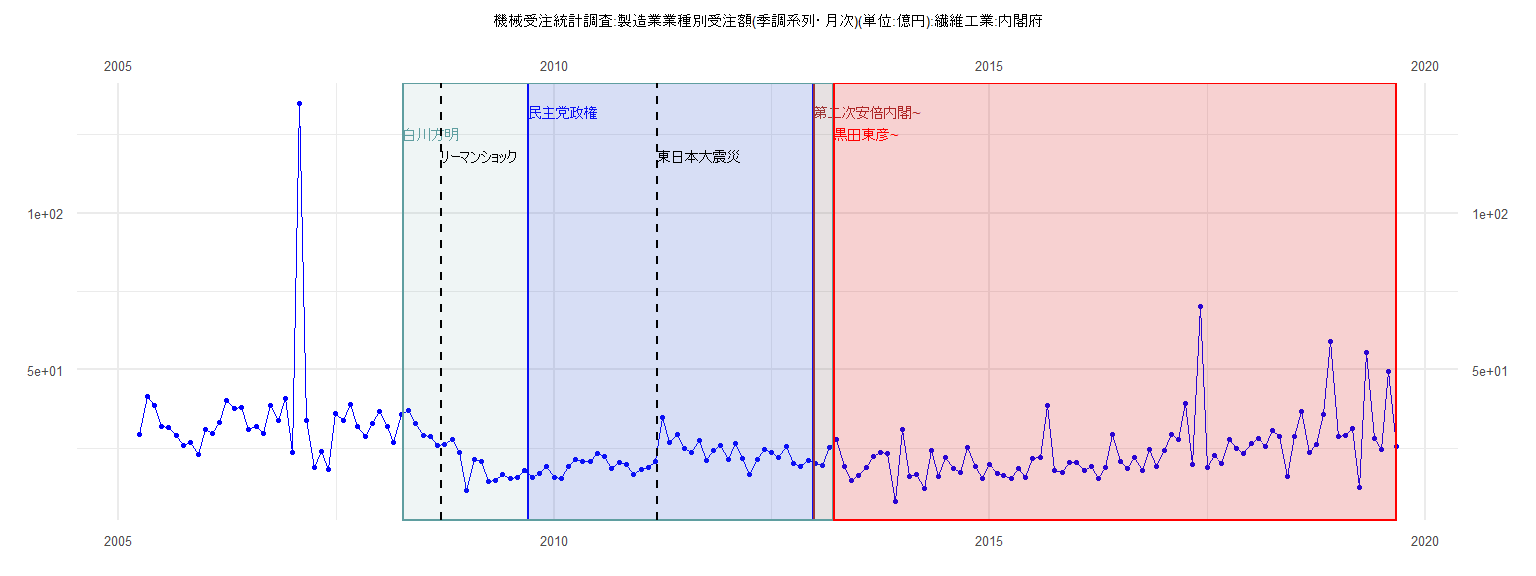

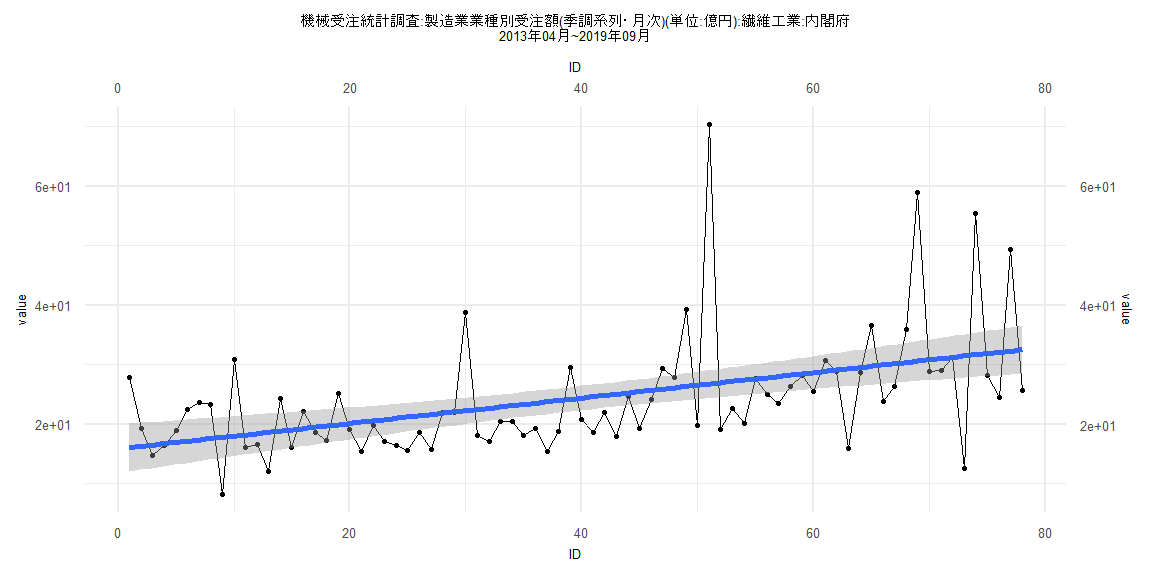

[1] "機械受注統計調査:製造業業種別受注額(季調系列・月次)(単位:億円):繊維工業:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 29.52 41.43 38.67 31.90 31.69 29.08 26.03 26.91 23.15

2006 31.17 29.89 33.25 40.24 37.63 38.17 30.92 31.95 29.90 38.83 34.06 40.95

2007 23.55 134.91 33.92 18.84 24.18 18.26 36.12 33.98 39.11 31.87 28.65 32.86

2008 36.93 31.84 26.79 35.87 37.23 32.84 29.25 28.87 26.05 26.21 27.69 23.58

2009 11.75 21.34 20.89 14.39 14.86 16.60 15.51 15.64 17.92 15.80 17.15 19.32

2010 15.77 15.37 19.31 21.40 20.78 20.78 23.52 22.38 18.72 20.36 19.81 16.69

2011 18.24 18.88 20.72 34.87 26.86 29.50 25.08 23.60 27.37 21.24 24.39 25.99

2012 21.41 26.57 21.74 16.84 21.41 24.69 23.82 22.14 25.50 20.11 19.32 21.24

2013 20.04 19.66 25.16 27.87 19.23 14.84 16.46 19.02 22.50 23.68 23.32 8.23

2014 30.93 16.09 16.62 12.15 24.34 16.08 22.22 18.57 17.27 25.19 19.12 15.48

2015 19.88 17.09 16.45 15.54 18.62 15.86 21.94 22.05 38.76 18.08 17.18 20.45

2016 20.43 18.09 19.37 15.50 18.77 29.57 20.85 18.64 22.07 17.95 24.76 19.26

2017 24.25 29.31 27.87 39.26 19.78 70.38 19.08 22.74 20.12 27.77 24.94 23.53

2018 26.44 28.17 25.57 30.69 28.92 15.94 28.66 36.62 23.85 26.33 35.89 58.99

2019 28.82 29.04 31.21 12.66 55.48 28.18 24.53 49.41 25.67

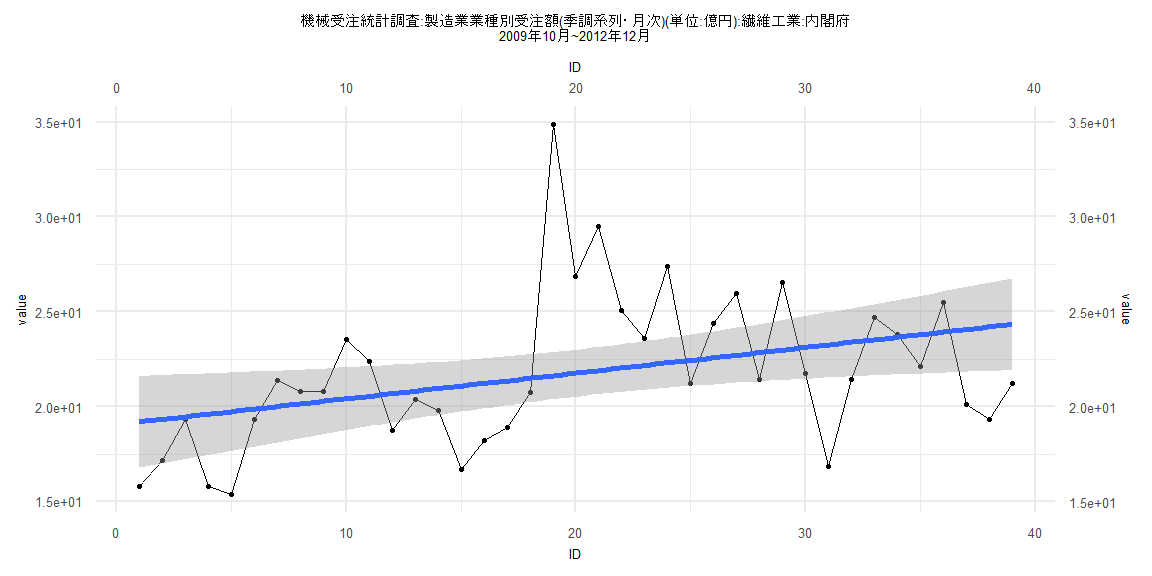

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-6.4094 -2.3258 -0.5573 1.6956 13.2440

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 19.05557 1.24192 15.34 <0.0000000000000002 ***

ID 0.13529 0.05412 2.50 0.017 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.804 on 37 degrees of freedom

Multiple R-squared: 0.1445, Adjusted R-squared: 0.1214

F-statistic: 6.25 on 1 and 37 DF, p-value: 0.01698

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.23077, p-value = 0.2523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.1435, p-value = 0.00128

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.075198, df = 1, p-value = 0.7839

Box-Ljung test

data: lm_residuals

X-squared = 7.0248, df = 1, p-value = 0.008039

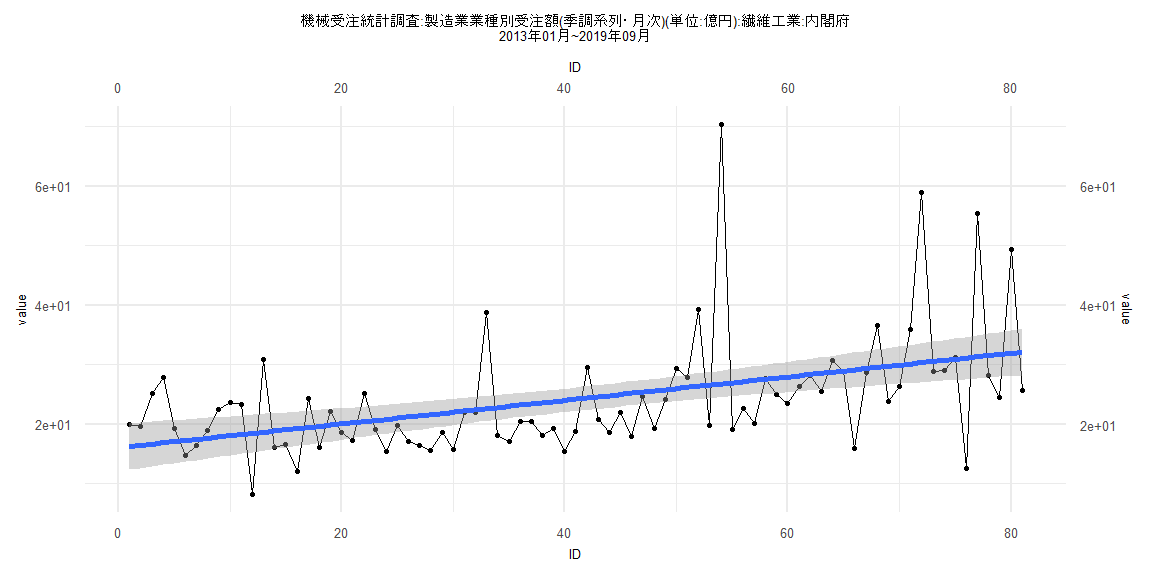

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-18.484 -4.992 -1.734 2.362 43.592

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 16.09540 2.00372 8.033 0.00000000000753 ***

ID 0.19801 0.04245 4.664 0.00001241889138 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 8.933 on 79 degrees of freedom

Multiple R-squared: 0.2159, Adjusted R-squared: 0.206

F-statistic: 21.76 on 1 and 79 DF, p-value: 0.00001242

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.22222, p-value = 0.03633

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3427, p-value = 0.9256

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 3.0305, df = 1, p-value = 0.08172

Box-Ljung test

data: lm_residuals

X-squared = 2.5963, df = 1, p-value = 0.1071

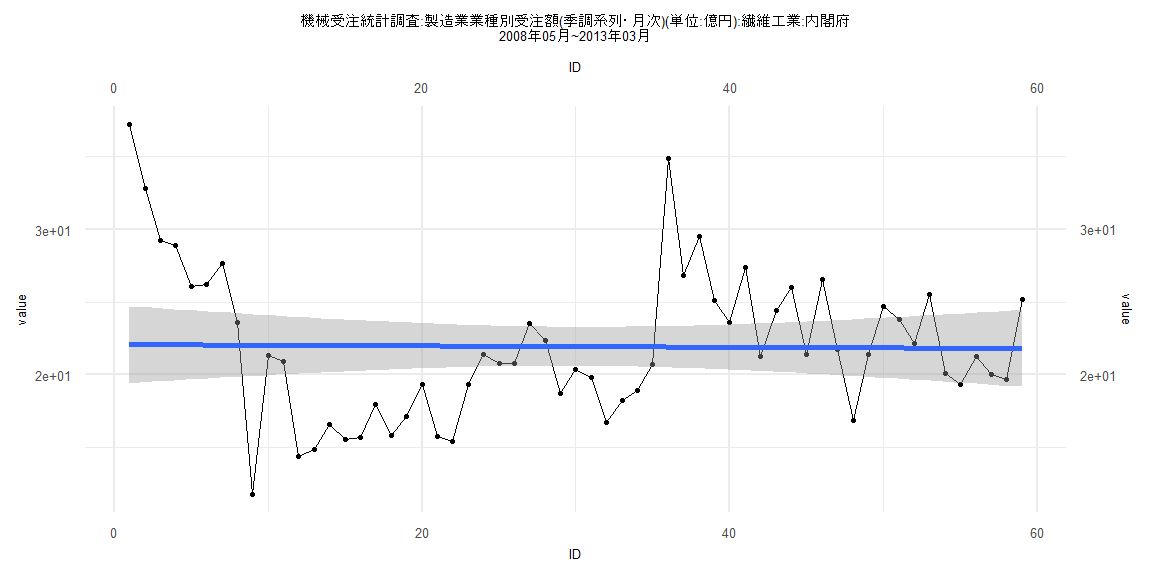

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-10.2801 -3.1283 -0.6408 3.2709 15.1637

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 22.070812 1.356851 16.266 <0.0000000000000002 ***

ID -0.004524 0.039333 -0.115 0.909

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.145 on 57 degrees of freedom

Multiple R-squared: 0.0002321, Adjusted R-squared: -0.01731

F-statistic: 0.01323 on 1 and 57 DF, p-value: 0.9088

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16949, p-value = 0.3674

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.65777, p-value = 0.0000000004473

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 10.247, df = 1, p-value = 0.001369

Box-Ljung test

data: lm_residuals

X-squared = 21.687, df = 1, p-value = 0.00000321

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-18.811 -4.799 -2.007 2.004 43.609

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 15.87440 2.06454 7.689 0.0000000000433 ***

ID 0.21365 0.04541 4.705 0.0000111446133 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 9.029 on 76 degrees of freedom

Multiple R-squared: 0.2256, Adjusted R-squared: 0.2154

F-statistic: 22.14 on 1 and 76 DF, p-value: 0.00001114

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.07495

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3782, p-value = 0.9423

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.7805, df = 1, p-value = 0.09542

Box-Ljung test

data: lm_residuals

X-squared = 3.3761, df = 1, p-value = 0.06615