Analysis

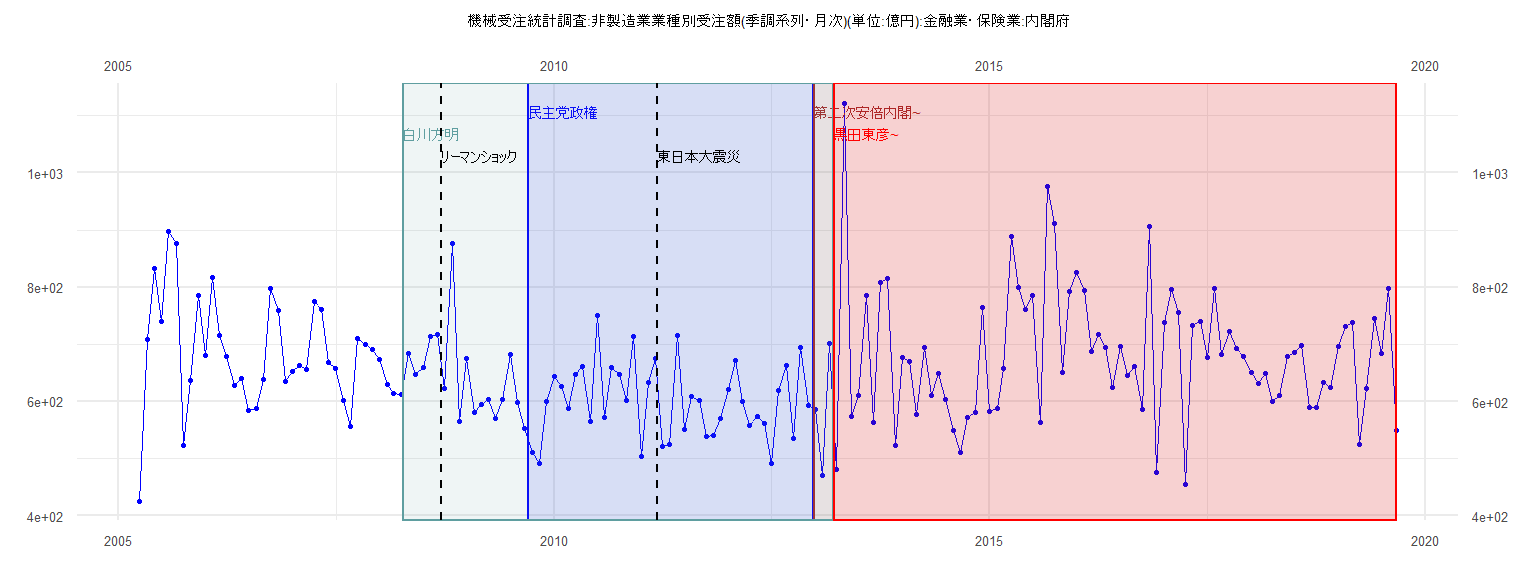

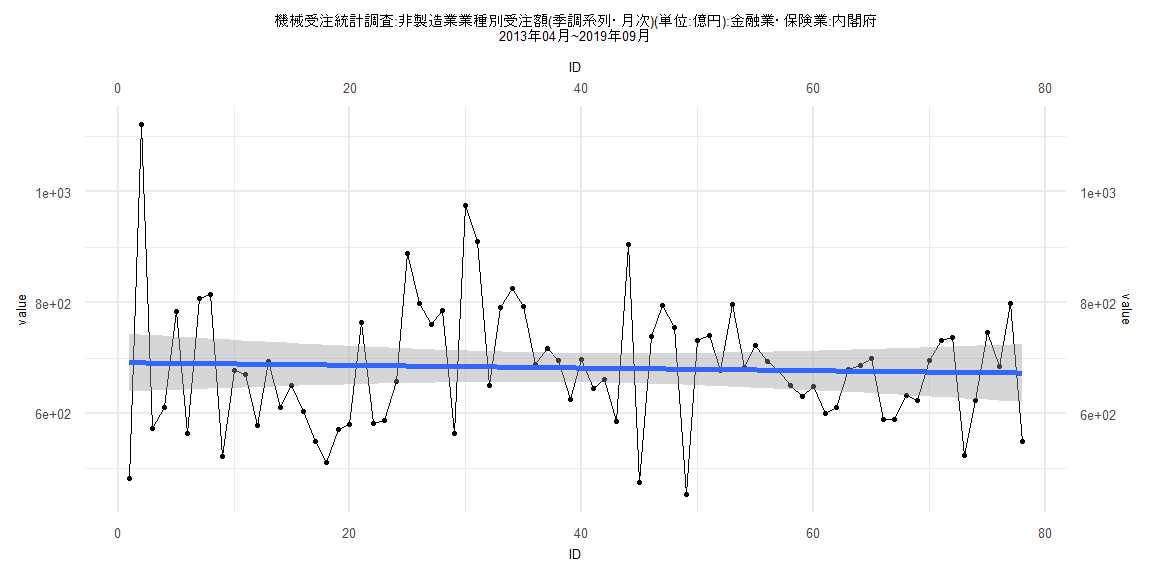

[1] "機械受注統計調査:非製造業業種別受注額(季調系列・月次)(単位:億円):金融業・保険業:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 425.52 707.73 832.09 740.57 897.73 876.85 522.44 636.85 785.41

2006 681.25 817.40 715.10 679.08 627.99 640.96 584.09 587.41 638.16 798.56 759.74 634.42

2007 651.51 662.90 656.18 774.44 761.37 668.35 658.29 601.48 556.22 710.95 700.04 690.47

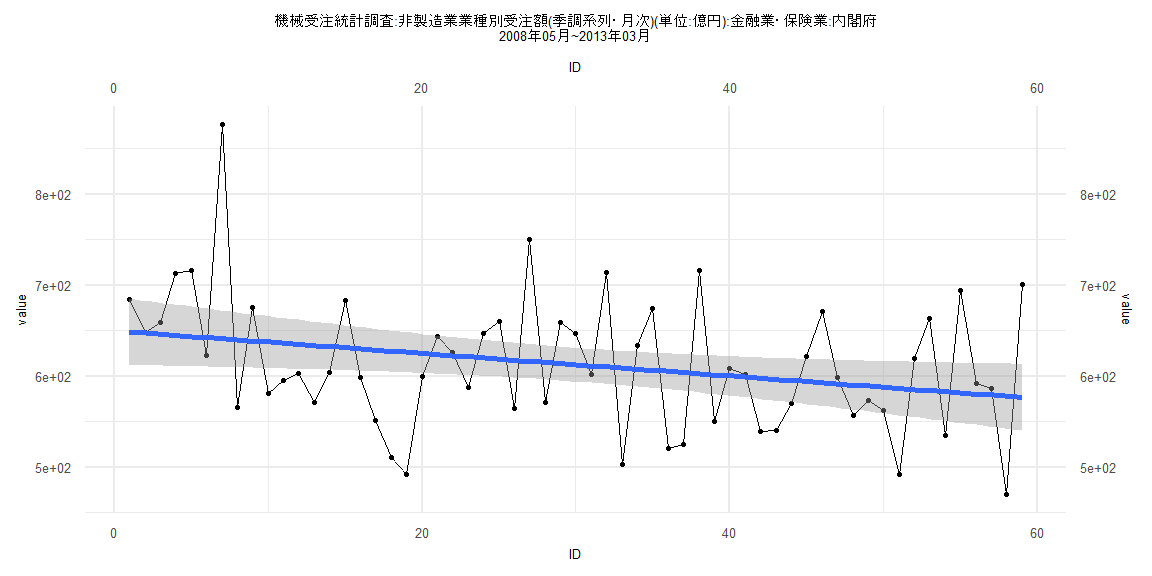

2008 672.51 629.98 614.06 611.82 684.06 647.99 659.56 712.78 716.57 622.74 876.40 565.62

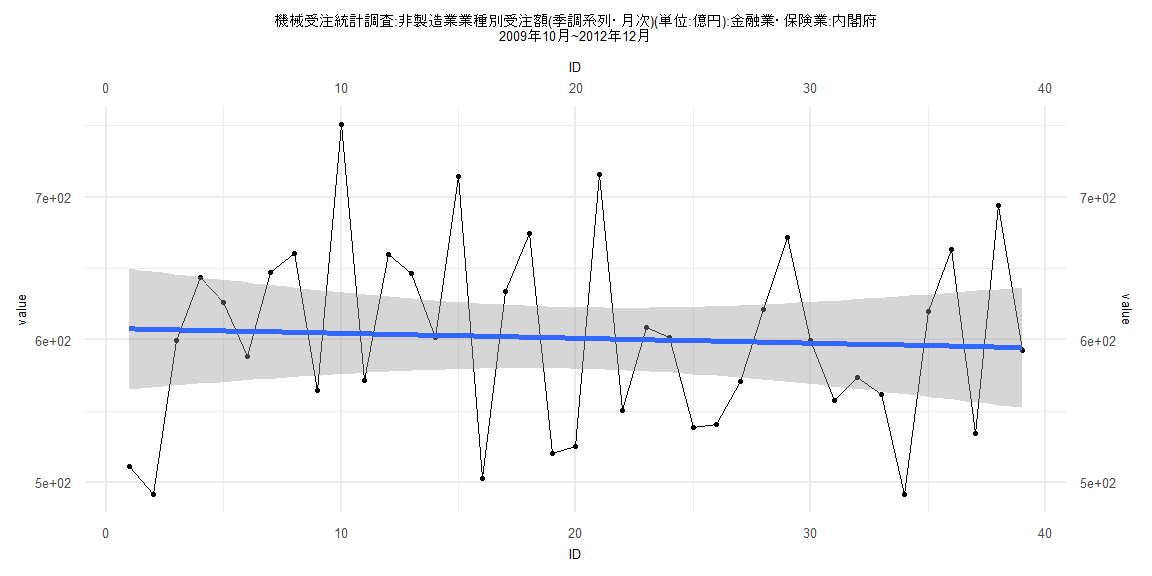

2009 674.97 580.87 594.81 602.81 570.86 604.10 682.93 598.55 551.81 511.17 491.63 599.44

2010 643.70 626.07 587.99 647.40 660.61 564.36 750.74 571.64 659.42 646.49 601.77 714.11

2011 502.79 633.68 674.41 520.57 525.24 716.10 550.44 608.57 601.63 538.85 540.86 570.40

2012 621.40 671.38 599.13 557.14 573.58 561.97 491.79 619.92 663.28 534.59 694.30 592.59

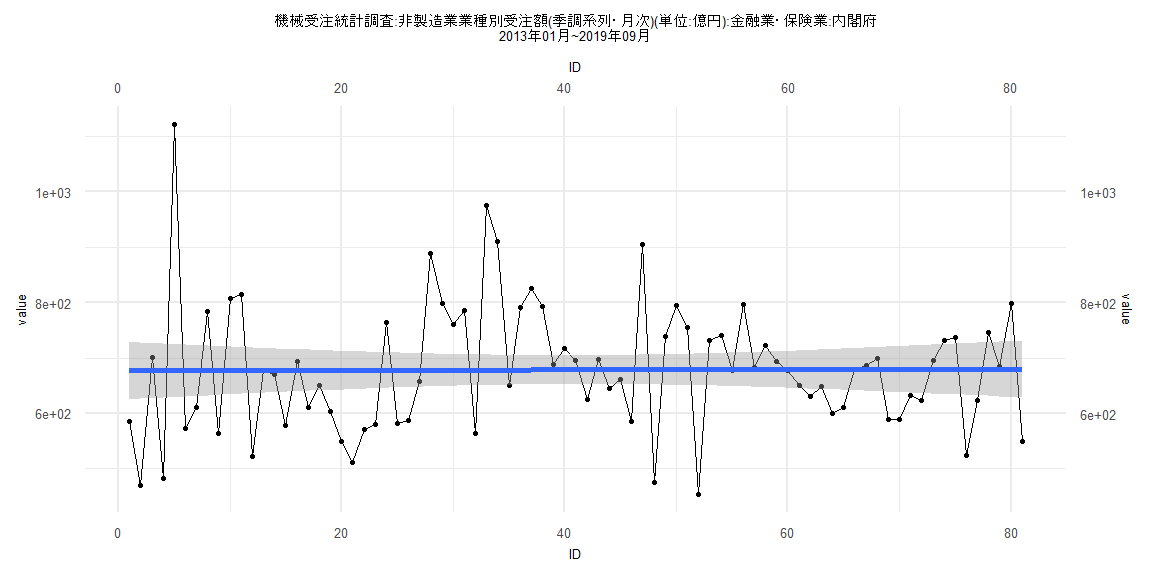

2013 586.10 470.23 700.54 481.62 1121.53 573.26 610.41 784.59 563.70 807.60 815.13 522.96

2014 676.68 670.69 577.70 693.74 610.82 649.61 603.58 549.25 510.92 571.49 580.80 764.78

2015 582.35 587.90 657.53 888.04 799.21 760.70 786.24 563.57 976.24 911.13 649.77 792.10

2016 825.30 793.73 687.52 717.48 695.10 624.44 696.57 645.10 661.06 585.40 905.57 476.09

2017 738.92 795.63 755.02 453.65 732.10 739.86 676.90 797.31 682.37 722.21 693.24 678.28

2018 650.03 631.19 649.15 600.54 610.35 678.68 685.85 698.30 588.78 589.05 632.74 623.66

2019 696.25 730.85 737.57 523.77 623.30 745.41 684.31 798.55 549.45

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-115.608 -45.201 -1.346 42.455 146.250

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 607.9252 21.6181 28.121 <0.0000000000000002 ***

ID -0.3435 0.9420 -0.365 0.717

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 66.21 on 37 degrees of freedom

Multiple R-squared: 0.003581, Adjusted R-squared: -0.02335

F-statistic: 0.133 on 1 and 37 DF, p-value: 0.7174

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.076923, p-value = 0.9999

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.2531, p-value = 0.7351

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.66783, df = 1, p-value = 0.4138

Box-Ljung test

data: lm_residuals

X-squared = 1.0139, df = 1, p-value = 0.314

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-225.31 -89.99 -1.01 60.82 444.50

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 676.82098 26.35587 25.680 <0.0000000000000002 ***

ID 0.04114 0.55841 0.074 0.941

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 117.5 on 79 degrees of freedom

Multiple R-squared: 6.872e-05, Adjusted R-squared: -0.01259

F-statistic: 0.005429 on 1 and 79 DF, p-value: 0.9414

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.08642, p-value = 0.9254

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.1435, p-value = 0.7033

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.6459, df = 1, p-value = 0.0175

Box-Ljung test

data: lm_residuals

X-squared = 0.58413, df = 1, p-value = 0.4447

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-134.632 -49.679 0.669 35.910 235.273

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 649.7988 18.7359 34.682 <0.0000000000000002 ***

ID -1.2388 0.5431 -2.281 0.0263 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 71.04 on 57 degrees of freedom

Multiple R-squared: 0.08364, Adjusted R-squared: 0.06756

F-statistic: 5.202 on 1 and 57 DF, p-value: 0.02631

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.2468, p-value = 0.7939

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.19822, df = 1, p-value = 0.6562

Box-Ljung test

data: lm_residuals

X-squared = 1.4384, df = 1, p-value = 0.2304

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-226.13 -83.21 -0.86 69.79 430.37

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 691.6489 26.6849 25.919 <0.0000000000000002 ***

ID -0.2422 0.5869 -0.413 0.681

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 116.7 on 76 degrees of freedom

Multiple R-squared: 0.002236, Adjusted R-squared: -0.01089

F-statistic: 0.1703 on 1 and 76 DF, p-value: 0.681

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11538, p-value = 0.6802

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.1483, p-value = 0.7056

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.5983, df = 1, p-value = 0.01021

Box-Ljung test

data: lm_residuals

X-squared = 0.85543, df = 1, p-value = 0.355