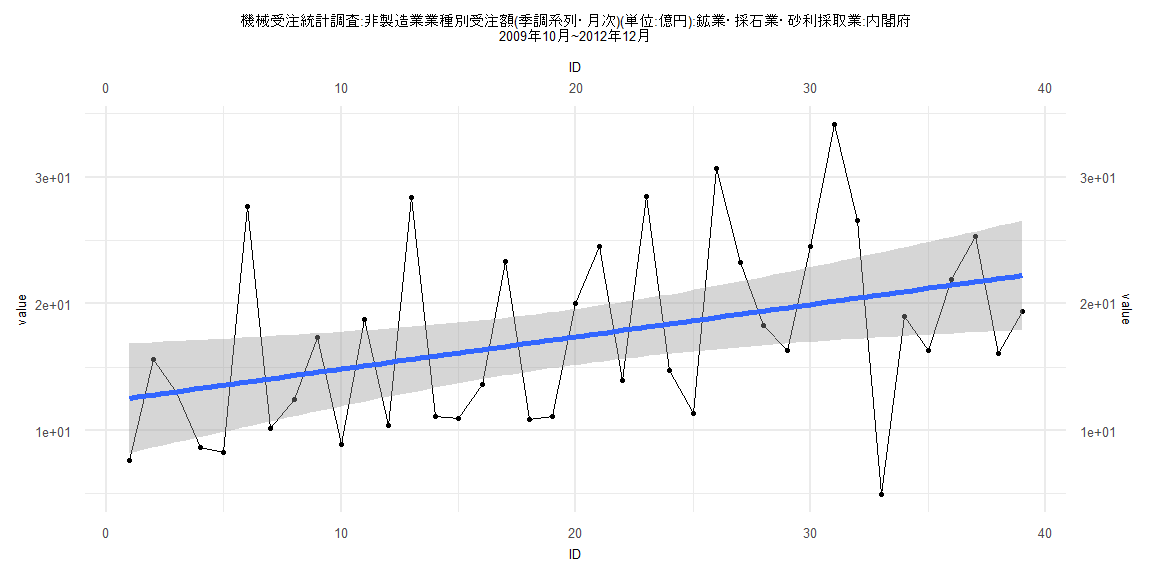

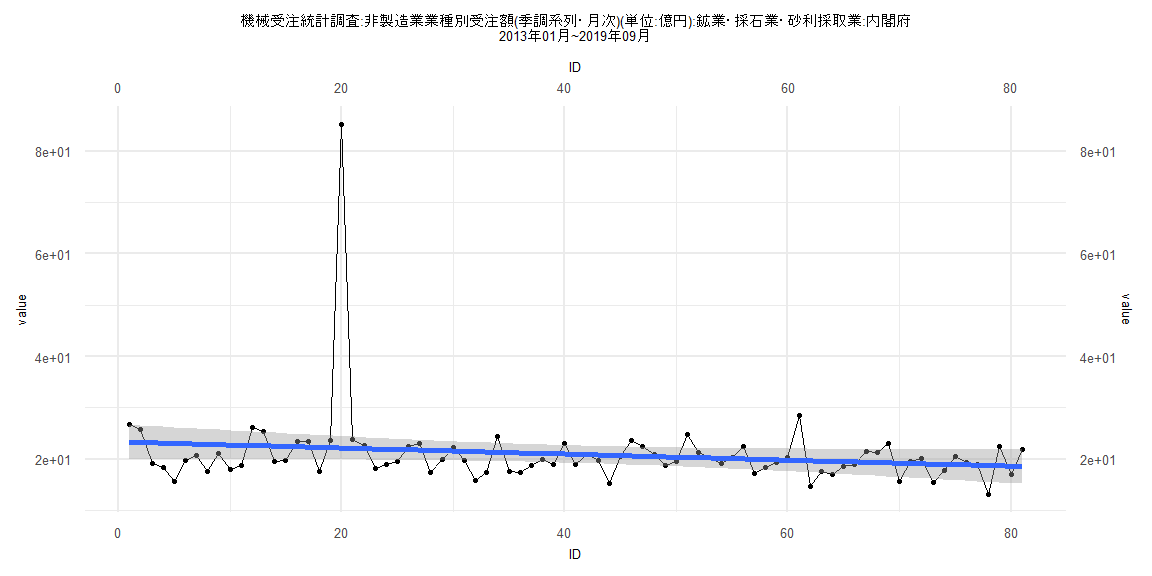

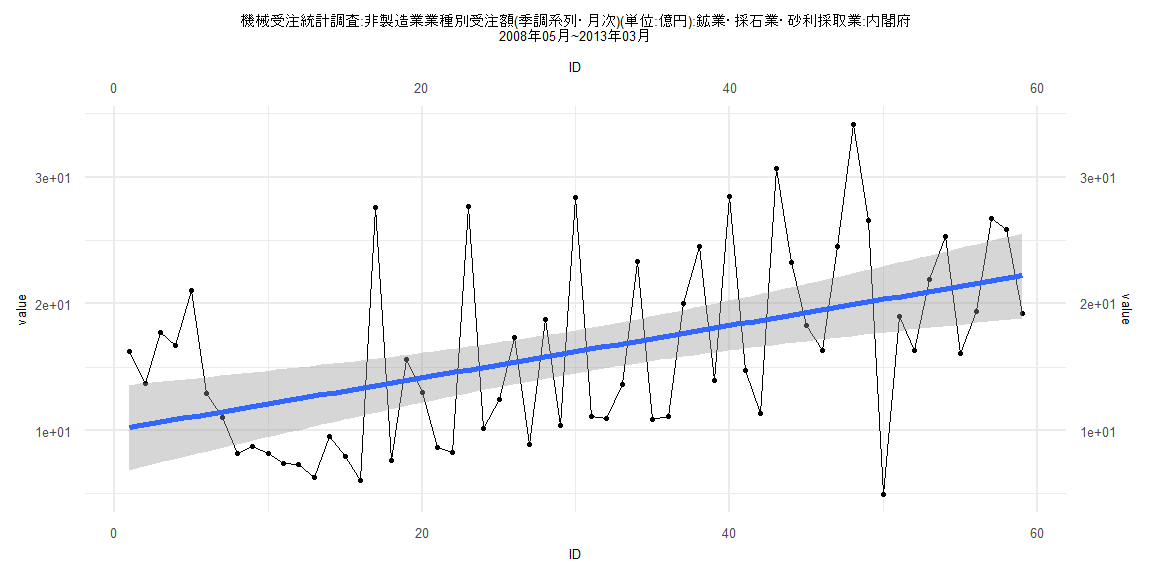

Analysis

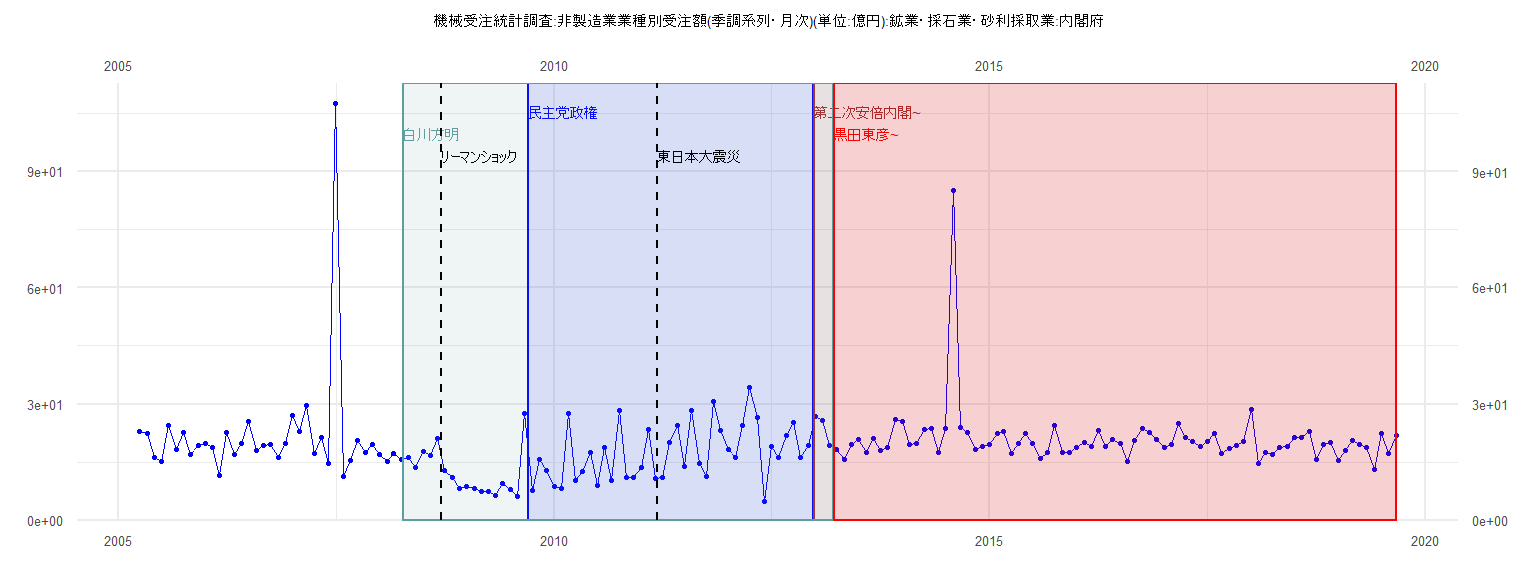

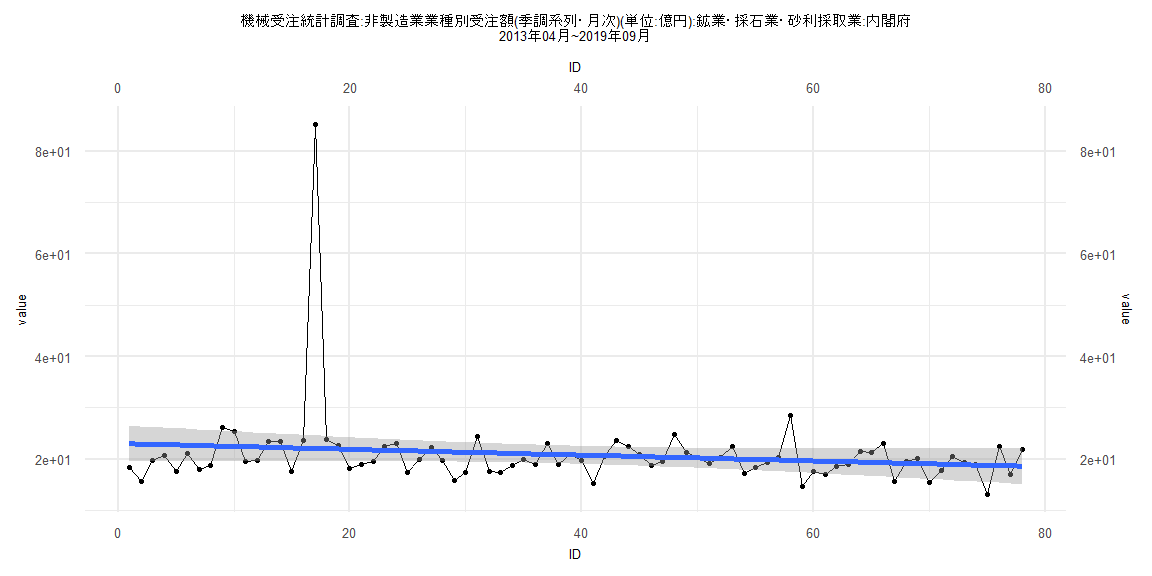

[1] "機械受注統計調査:非製造業業種別受注額(季調系列・月次)(単位:億円):鉱業・採石業・砂利採取業:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 23.03 22.31 16.32 15.09 24.57 18.20 22.53 16.98 19.26

2006 19.85 18.85 11.65 22.60 16.91 19.94 25.60 17.98 19.24 19.46 16.24 19.76

2007 26.92 23.00 29.72 17.34 21.29 14.77 107.53 11.23 15.44 20.64 17.48 19.63

2008 17.08 15.15 17.15 15.74 16.24 13.73 17.72 16.68 21.04 12.91 11.04 8.20

2009 8.71 8.21 7.40 7.31 6.33 9.57 7.96 6.08 27.61 7.67 15.60 12.97

2010 8.65 8.27 27.64 10.18 12.48 17.38 8.93 18.73 10.39 28.40 11.12 10.95

2011 13.64 23.33 10.87 11.14 20.03 24.54 13.91 28.44 14.77 11.38 30.65 23.23

2012 18.30 16.31 24.54 34.14 26.60 4.96 18.96 16.29 21.92 25.32 16.11 19.42

2013 26.72 25.87 19.26 18.35 15.76 19.68 20.78 17.59 21.23 18.12 18.89 26.12

2014 25.51 19.57 19.78 23.45 23.56 17.60 23.74 85.16 23.86 22.74 18.18 19.00

2015 19.66 22.44 23.02 17.35 19.93 22.35 19.85 15.93 17.53 24.49 17.57 17.53

2016 18.76 20.05 19.06 23.15 18.96 20.93 19.80 15.23 20.59 23.69 22.59 20.96

2017 18.77 19.50 24.90 21.38 20.34 19.15 20.38 22.48 17.17 18.49 19.35 20.31

2018 28.62 14.73 17.61 17.08 18.67 19.09 21.48 21.31 23.00 15.72 19.49 20.07

2019 15.42 17.89 20.52 19.48 18.90 13.17 22.42 17.14 21.93

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-15.743 -4.899 -1.998 3.846 13.947

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 12.28957 2.21531 5.548 0.00000257 ***

ID 0.25496 0.09653 2.641 0.012 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.785 on 37 degrees of freedom

Multiple R-squared: 0.1586, Adjusted R-squared: 0.1359

F-statistic: 6.976 on 1 and 37 DF, p-value: 0.01203

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3571, p-value = 0.8319

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.35636, df = 1, p-value = 0.5505

Box-Ljung test

data: lm_residuals

X-squared = 1.4849, df = 1, p-value = 0.223

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-7.326 -2.965 -0.931 1.232 62.959

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 23.38134 1.72973 13.52 <0.0000000000000002 ***

ID -0.05901 0.03665 -1.61 0.111

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.712 on 79 degrees of freedom

Multiple R-squared: 0.03178, Adjusted R-squared: 0.01952

F-statistic: 2.593 on 1 and 79 DF, p-value: 0.1113

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.33333, p-value = 0.0002198

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.8627, p-value = 0.2308

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.88401, df = 1, p-value = 0.3471

Box-Ljung test

data: lm_residuals

X-squared = 0.36898, df = 1, p-value = 0.5436

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-15.382 -5.177 -2.160 4.485 14.210

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 10.02709 1.71715 5.839 0.000000263 ***

ID 0.20630 0.04978 4.144 0.000114 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.511 on 57 degrees of freedom

Multiple R-squared: 0.2316, Adjusted R-squared: 0.2181

F-statistic: 17.18 on 1 and 57 DF, p-value: 0.0001143

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.30508, p-value = 0.00792

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.1174, p-value = 0.6245

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.17374, df = 1, p-value = 0.6768

Box-Ljung test

data: lm_residuals

X-squared = 0.28673, df = 1, p-value = 0.5923

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-7.214 -2.884 -0.970 1.225 63.037

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 23.08720 1.79123 12.89 <0.0000000000000002 ***

ID -0.05672 0.03940 -1.44 0.154

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.834 on 76 degrees of freedom

Multiple R-squared: 0.02655, Adjusted R-squared: 0.01374

F-statistic: 2.073 on 1 and 76 DF, p-value: 0.1541

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.24359, p-value = 0.01923

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.8668, p-value = 0.2392

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.0764, df = 1, p-value = 0.2995

Box-Ljung test

data: lm_residuals

X-squared = 0.32273, df = 1, p-value = 0.57