Analysis

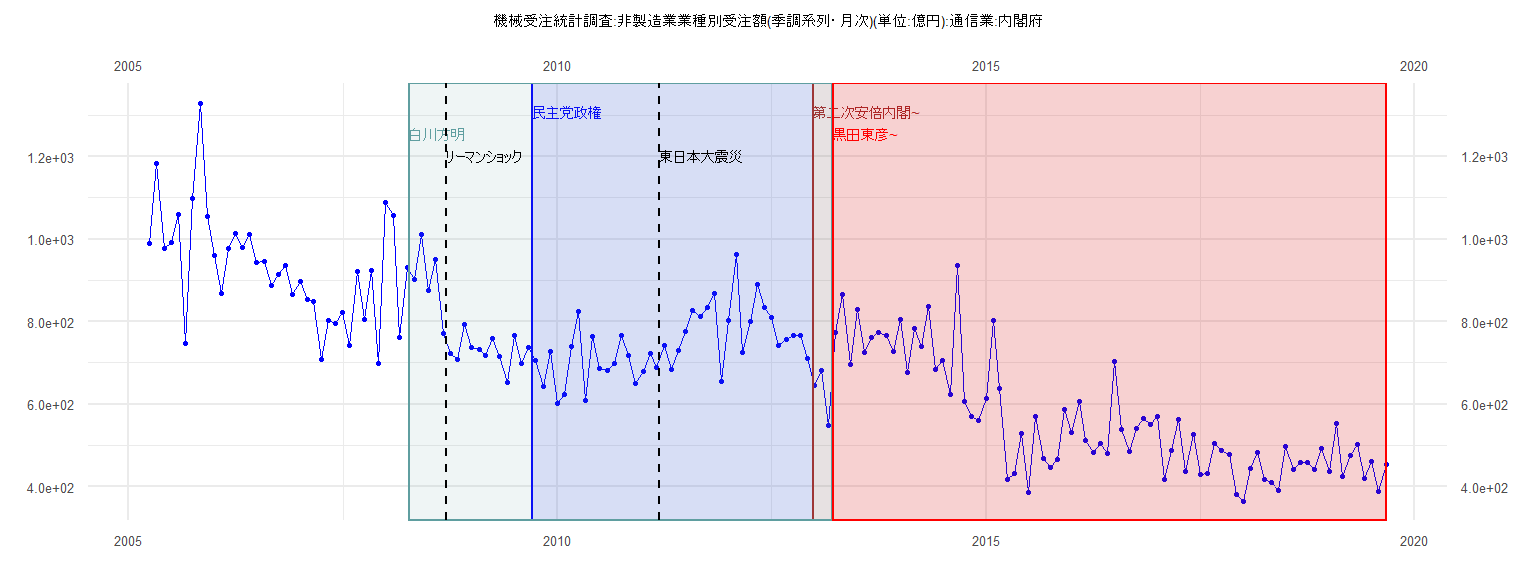

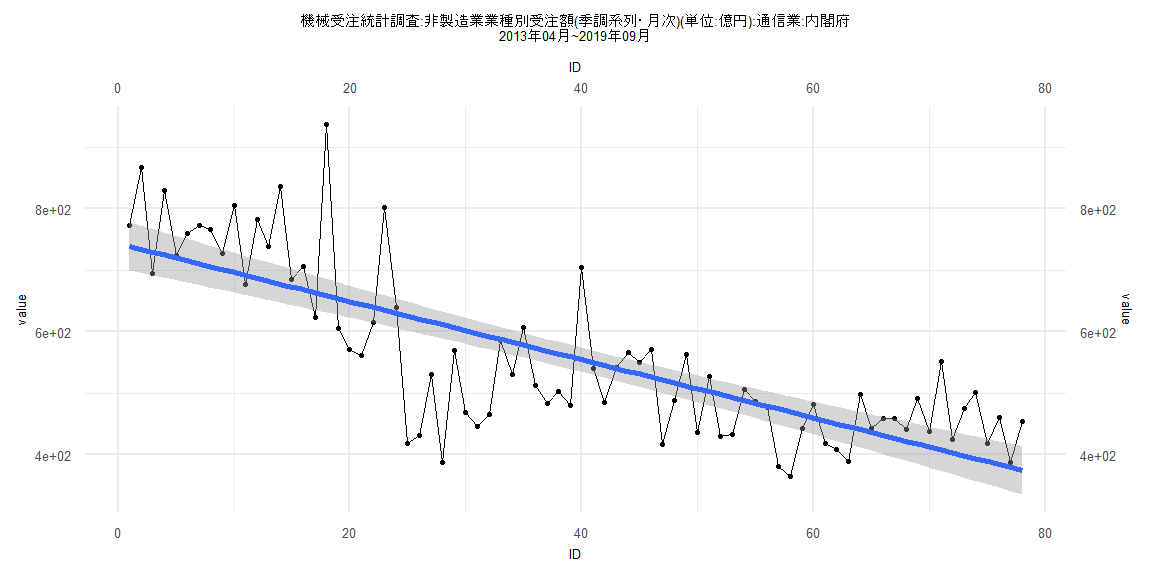

[1] "機械受注統計調査:非製造業業種別受注額(季調系列・月次)(単位:億円):通信業:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 988.60 1183.32 977.90 991.34 1059.05 745.73 1099.21 1328.42 1053.74

2006 961.17 868.10 976.75 1014.00 979.35 1011.06 943.29 944.72 886.65 913.54 935.95 865.43

2007 897.14 852.85 848.23 707.88 802.33 796.37 822.10 741.43 920.34 805.43 924.48 699.55

2008 1087.44 1057.61 761.15 931.20 901.77 1010.89 876.41 950.57 772.09 722.19 707.06 792.75

2009 737.47 731.95 717.91 758.59 715.78 652.51 765.26 697.34 736.63 705.95 643.50 726.90

2010 601.84 623.02 739.82 823.78 609.57 764.14 686.62 681.19 699.50 767.09 716.87 650.91

2011 678.21 722.08 688.57 741.14 683.94 729.94 775.09 827.62 812.74 833.83 869.08 653.70

2012 801.71 962.91 726.09 800.73 888.73 834.70 808.96 740.94 756.33 765.27 767.37 711.04

2013 645.51 680.84 549.01 773.20 866.86 695.48 829.73 724.05 760.51 772.55 765.72 727.37

2014 805.90 676.52 783.42 739.42 836.13 685.08 705.68 623.66 937.10 605.30 570.84 561.10

2015 614.51 801.90 638.90 417.91 431.59 529.84 386.68 569.09 468.77 446.20 466.25 585.79

2016 530.56 606.81 512.02 483.84 503.67 480.76 704.21 539.67 485.53 541.37 565.59 549.76

2017 570.71 416.88 488.16 563.46 436.49 527.40 430.28 432.91 505.49 487.05 477.66 380.22

2018 365.05 442.77 481.77 417.63 408.90 389.85 498.05 442.23 459.56 458.70 440.91 491.78

2019 437.40 551.88 425.38 475.07 501.81 418.58 460.43 388.03 453.77

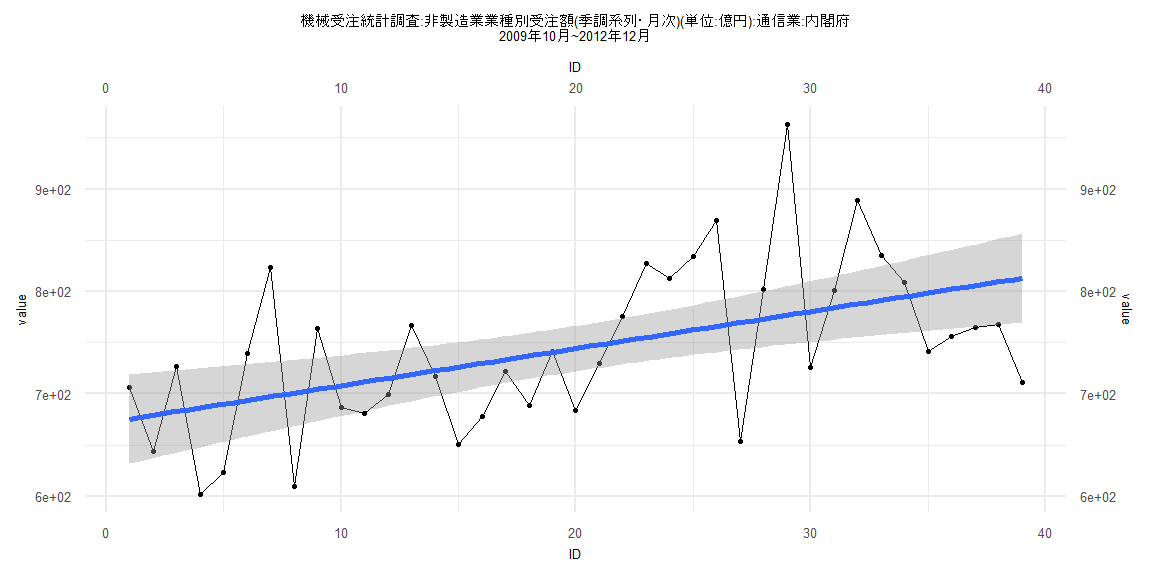

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-115.78 -49.89 -11.20 45.32 186.20

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 671.7495 22.3047 30.117 < 0.0000000000000002 ***

ID 3.6195 0.9719 3.724 0.000651 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 68.31 on 37 degrees of freedom

Multiple R-squared: 0.2726, Adjusted R-squared: 0.253

F-statistic: 13.87 on 1 and 37 DF, p-value: 0.000651

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.9097, p-value = 0.3238

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.61803, df = 1, p-value = 0.4318

Box-Ljung test

data: lm_residuals

X-squared = 0.0064651, df = 1, p-value = 0.9359

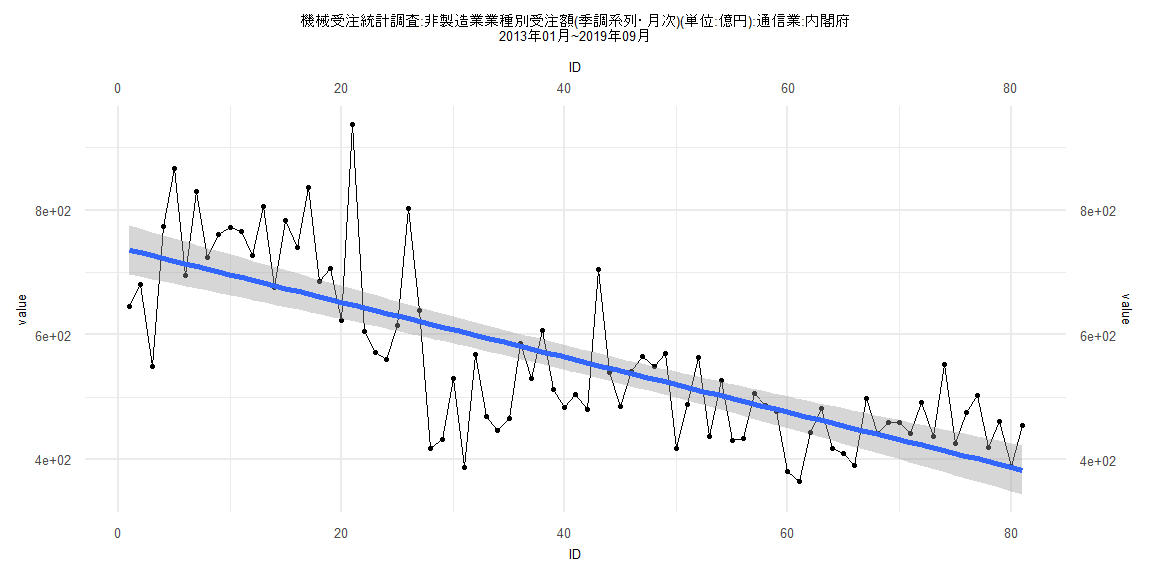

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-216.766 -56.201 4.047 50.733 289.572

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 740.1000 20.0372 36.94 <0.0000000000000002 ***

ID -4.4082 0.4245 -10.38 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 89.33 on 79 degrees of freedom

Multiple R-squared: 0.5771, Adjusted R-squared: 0.5718

F-statistic: 107.8 on 1 and 79 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11111, p-value = 0.7027

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4239, p-value = 0.002759

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 5.6833, df = 1, p-value = 0.01713

Box-Ljung test

data: lm_residuals

X-squared = 6.4772, df = 1, p-value = 0.01093

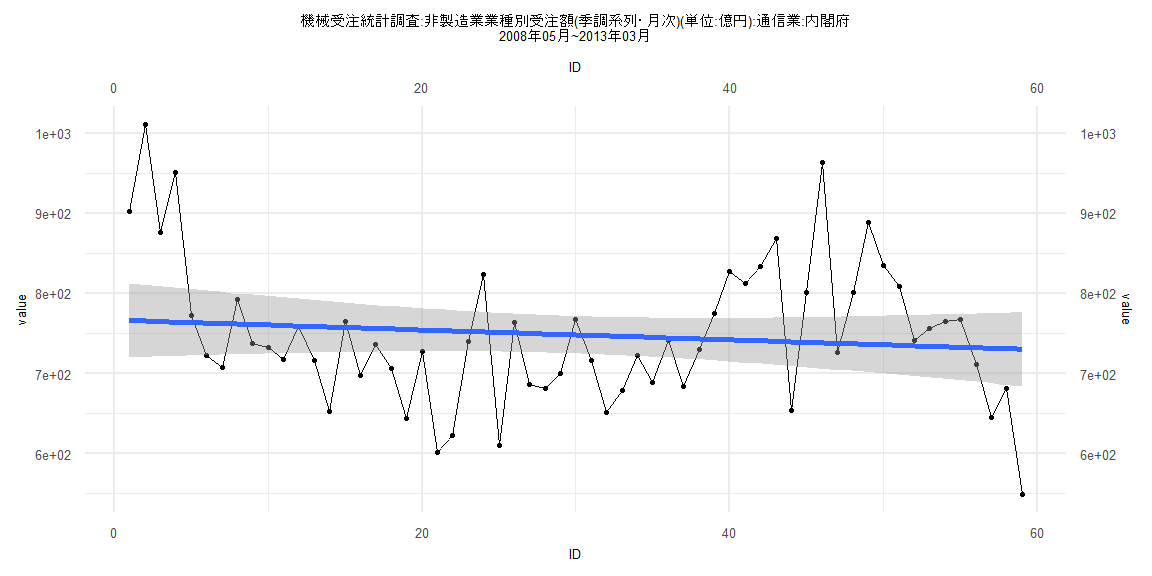

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-181.27 -55.95 -13.32 48.70 245.38

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 766.7446 23.5822 32.514 <0.0000000000000002 ***

ID -0.6181 0.6836 -0.904 0.37

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 89.42 on 57 degrees of freedom

Multiple R-squared: 0.01414, Adjusted R-squared: -0.003158

F-statistic: 0.8174 on 1 and 57 DF, p-value: 0.3697

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11864, p-value = 0.8052

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0088, p-value = 0.00001101

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.37727, df = 1, p-value = 0.5391

Box-Ljung test

data: lm_residuals

X-squared = 11.98, df = 1, p-value = 0.0005378

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-224.57 -58.55 7.36 45.02 278.52

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 743.7570 20.0210 37.15 <0.0000000000000002 ***

ID -4.7322 0.4403 -10.75 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 87.56 on 76 degrees of freedom

Multiple R-squared: 0.6031, Adjusted R-squared: 0.5979

F-statistic: 115.5 on 1 and 76 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.81

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4204, p-value = 0.003027

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 3.5411, df = 1, p-value = 0.05986

Box-Ljung test

data: lm_residuals

X-squared = 6.5095, df = 1, p-value = 0.01073