Analysis

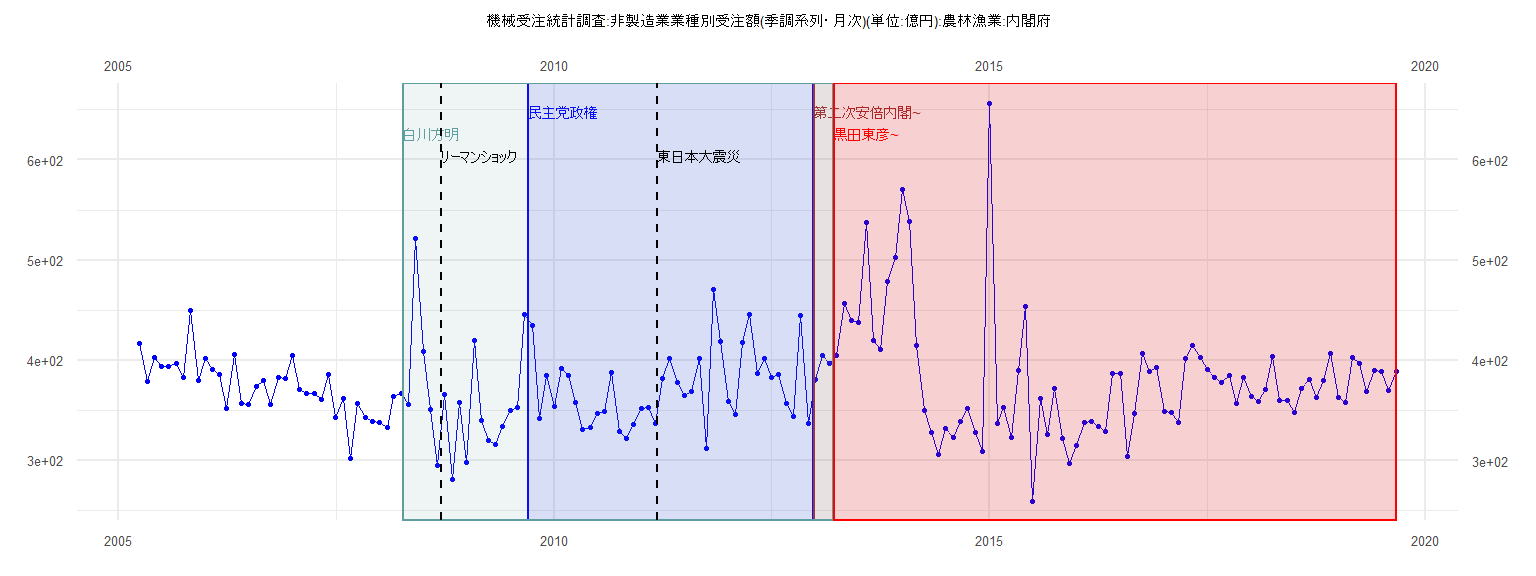

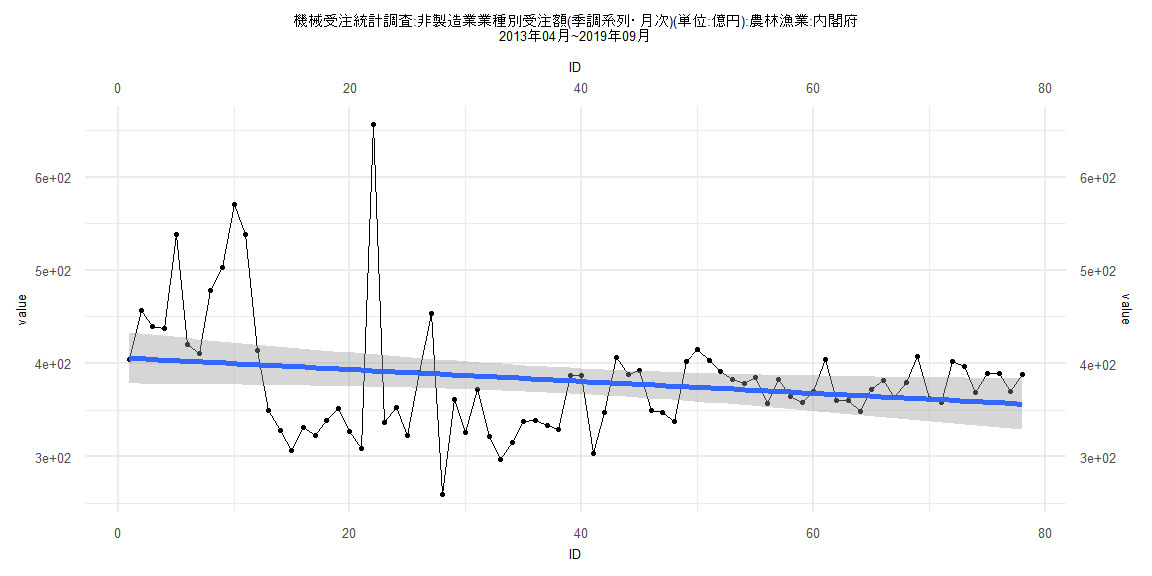

[1] "機械受注統計調査:非製造業業種別受注額(季調系列・月次)(単位:億円):農林漁業:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 416.57 378.78 402.96 394.22 393.45 396.47 382.73 449.87 379.98

2006 401.33 391.01 386.32 351.92 405.70 356.55 355.62 373.67 380.27 355.77 382.50 382.33

2007 404.89 370.57 366.65 366.56 360.79 385.50 343.33 361.45 301.50 357.06 342.51 338.89

2008 337.95 332.60 363.49 366.39 355.54 522.02 408.43 350.68 294.73 366.31 281.06 357.72

2009 297.83 420.25 339.54 320.06 316.38 333.64 349.42 353.27 445.54 435.04 341.49 384.86

2010 353.84 392.23 385.29 357.83 331.19 332.73 346.62 349.22 387.51 329.00 321.72 336.37

2011 351.83 352.65 336.75 381.62 401.72 377.76 364.42 368.37 401.78 312.17 471.16 419.00

2012 358.87 346.03 417.55 446.12 387.11 401.49 382.74 385.82 357.20 343.72 444.55 337.04

2013 380.70 404.38 396.56 404.64 456.45 439.49 437.26 537.91 420.19 410.96 478.36 502.76

2014 570.90 538.32 414.30 349.96 328.30 306.15 331.75 322.80 339.04 352.22 327.52 308.85

2015 656.26 336.53 352.74 322.79 389.83 453.51 259.52 361.68 325.53 371.69 321.97 297.06

2016 314.92 337.47 339.35 333.81 329.42 387.29 386.98 303.94 347.14 406.74 388.50 392.91

2017 349.40 347.85 337.86 402.30 414.85 403.21 390.92 382.37 378.23 384.99 357.01 382.51

2018 364.12 358.60 370.37 404.25 359.94 359.82 348.36 371.72 381.33 363.21 379.81 407.14

2019 362.62 357.67 402.33 396.97 369.30 389.46 388.81 369.53 388.61

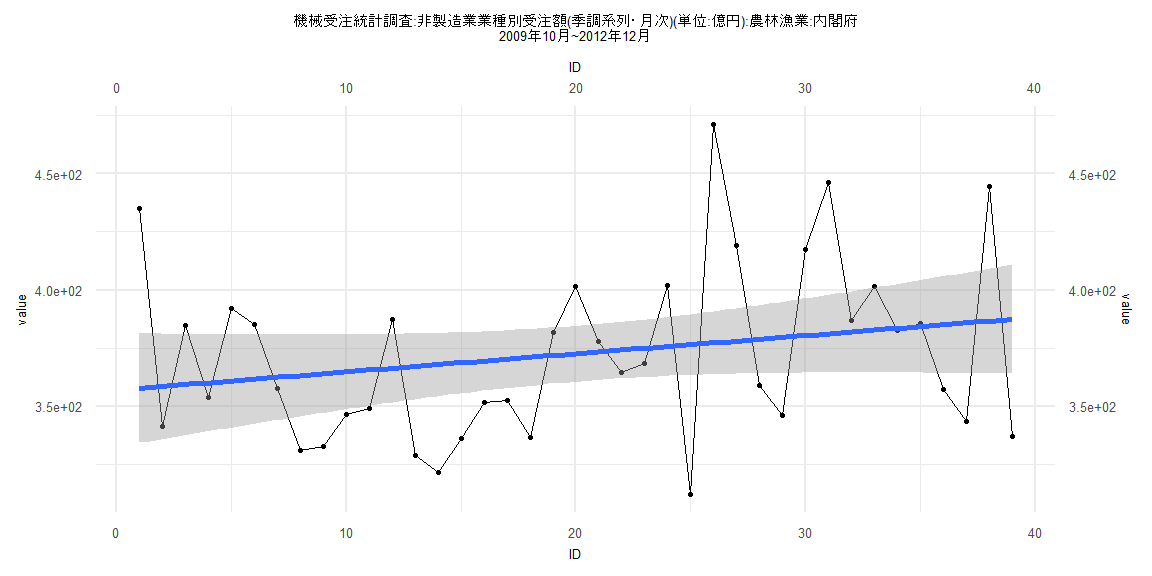

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-64.360 -29.613 -6.293 24.551 93.849

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 357.0102 12.0453 29.639 <0.0000000000000002 ***

ID 0.7808 0.5249 1.488 0.145

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 36.89 on 37 degrees of freedom

Multiple R-squared: 0.05643, Adjusted R-squared: 0.03093

F-statistic: 2.213 on 1 and 37 DF, p-value: 0.1453

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.9348, p-value = 0.3528

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.62407, df = 1, p-value = 0.4295

Box-Ljung test

data: lm_residuals

X-squared = 0.11341, df = 1, p-value = 0.7363

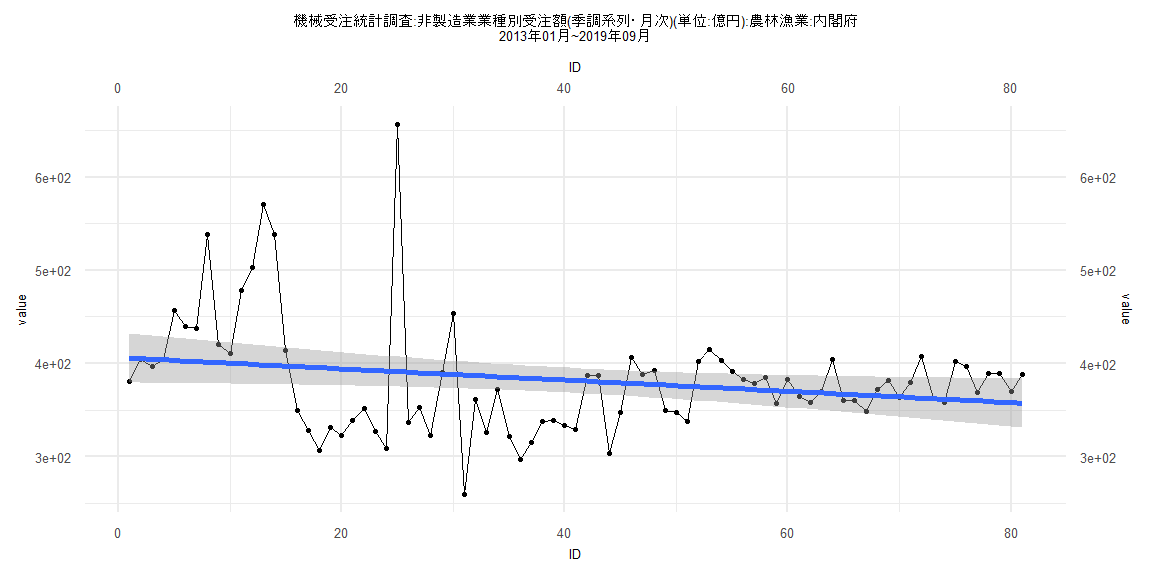

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-128.026 -40.753 0.814 27.416 265.096

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 406.2383 13.5164 30.055 <0.0000000000000002 ***

ID -0.6030 0.2864 -2.106 0.0384 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 60.26 on 79 degrees of freedom

Multiple R-squared: 0.05314, Adjusted R-squared: 0.04115

F-statistic: 4.433 on 1 and 79 DF, p-value: 0.03842

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12346, p-value = 0.5705

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.3427, p-value = 0.0007593

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 6.2375, df = 1, p-value = 0.01251

Box-Ljung test

data: lm_residuals

X-squared = 8.9242, df = 1, p-value = 0.002814

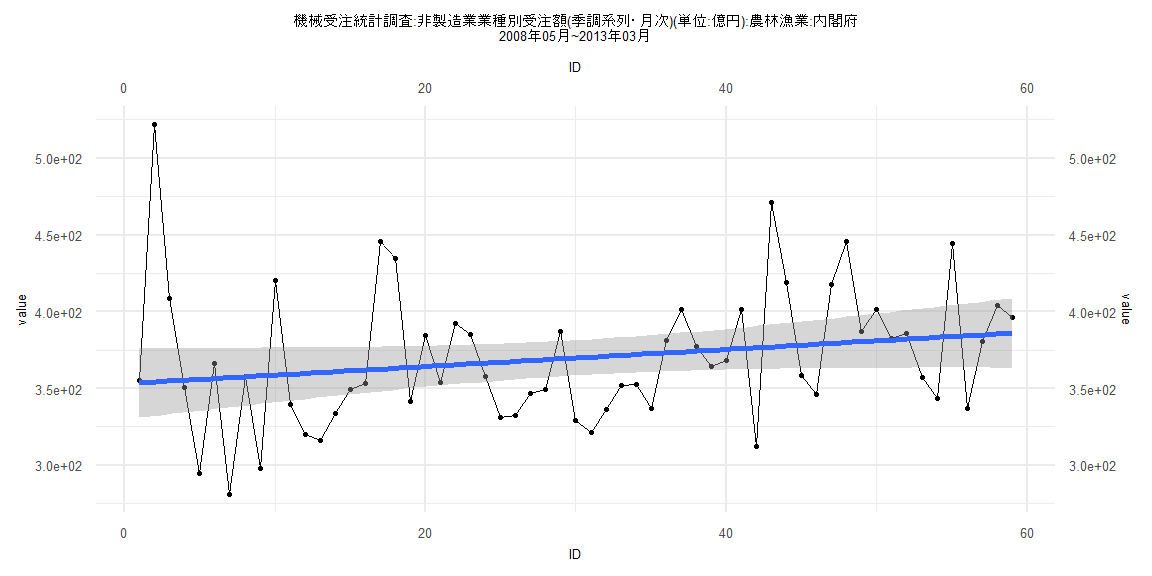

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-76.040 -30.105 -7.153 19.821 167.711

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 353.1925 11.6365 30.352 <0.0000000000000002 ***

ID 0.5583 0.3373 1.655 0.103

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 44.12 on 57 degrees of freedom

Multiple R-squared: 0.04585, Adjusted R-squared: 0.02911

F-statistic: 2.739 on 1 and 57 DF, p-value: 0.1034

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.084746, p-value = 0.9854

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.8001, p-value = 0.1812

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 3.4049, df = 1, p-value = 0.065

Box-Ljung test

data: lm_residuals

X-squared = 0.61358, df = 1, p-value = 0.4334

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-128.854 -43.415 1.715 27.778 264.060

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 406.2290 14.0298 28.955 <0.0000000000000002 ***

ID -0.6377 0.3086 -2.067 0.0422 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 61.36 on 76 degrees of freedom

Multiple R-squared: 0.0532, Adjusted R-squared: 0.04074

F-statistic: 4.27 on 1 and 76 DF, p-value: 0.04219

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.19231, p-value = 0.1118

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.3437, p-value = 0.0009289

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.9404, df = 1, p-value = 0.004834

Box-Ljung test

data: lm_residuals

X-squared = 8.631, df = 1, p-value = 0.003305