Analysis

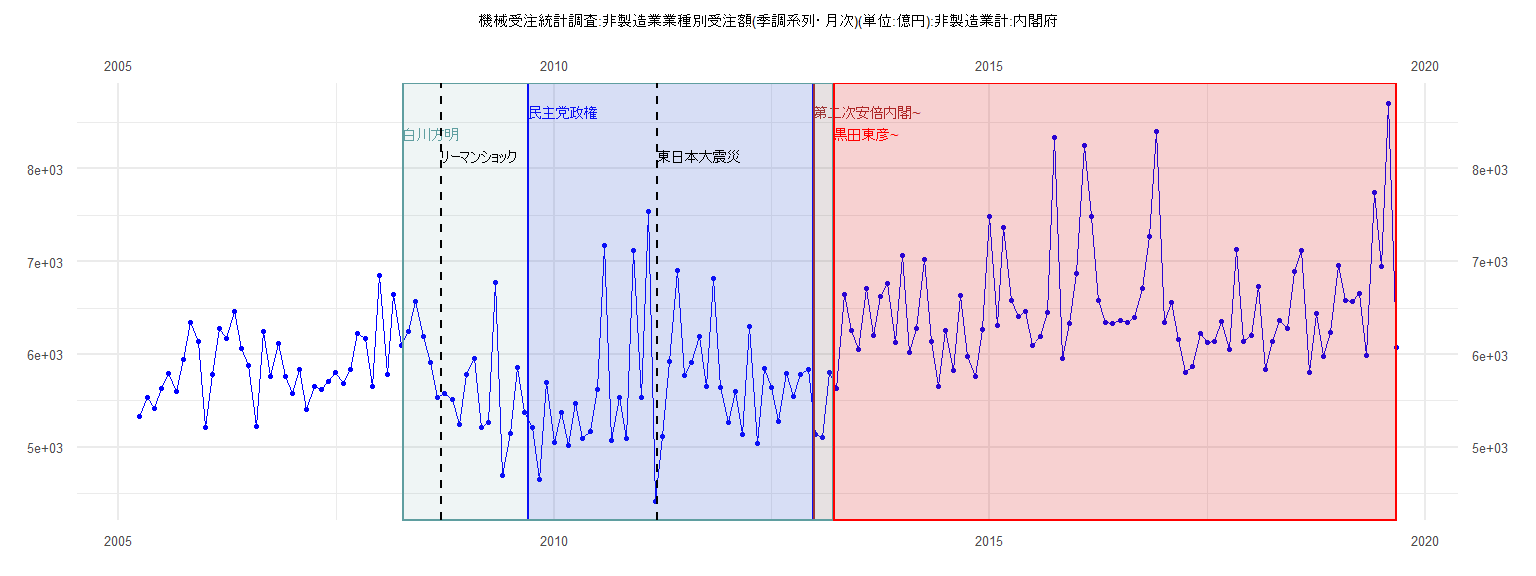

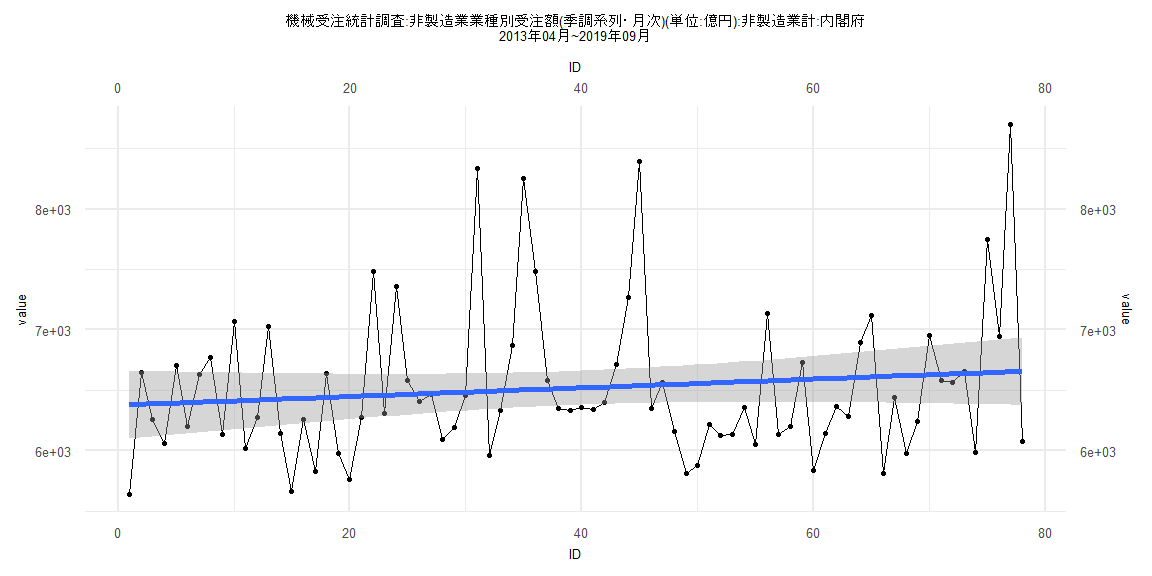

[1] "機械受注統計調査:非製造業業種別受注額(季調系列・月次)(単位:億円):非製造業計:内閣府"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 5327.76 5535.57 5414.58 5634.51 5790.08 5600.52 5943.71 6346.58 6134.67

2006 5216.78 5782.56 6278.53 6172.31 6467.47 6063.45 5879.07 5229.18 6242.86 5766.81 6118.49 5757.73

2007 5584.58 5842.40 5403.22 5659.98 5619.00 5713.97 5802.86 5689.73 5833.71 6225.29 6169.76 5657.40

2008 6846.15 5779.66 6644.24 6095.10 6244.68 6570.00 6191.89 5914.74 5540.48 5581.77 5517.68 5244.67

2009 5788.58 5960.48 5210.14 5265.36 6776.93 4695.46 5147.41 5859.78 5370.51 5214.29 4650.72 5702.66

2010 5046.89 5379.74 5020.62 5472.37 5090.32 5168.68 5618.36 7177.86 5076.59 5539.67 5100.09 7124.23

2011 5535.40 7538.01 4421.84 5113.79 5923.28 6908.28 5768.63 5909.58 6194.32 5651.91 6818.91 5639.85

2012 5264.95 5596.04 5135.81 6305.42 5043.21 5846.05 5644.99 5283.17 5800.40 5542.79 5782.20 5835.71

2013 5141.77 5101.99 5807.53 5637.93 6650.56 6262.42 6058.84 6706.06 6198.88 6627.68 6769.34 6133.09

2014 7066.60 6018.50 6277.25 7024.81 6144.69 5660.10 6261.60 5828.12 6638.26 5979.50 5763.25 6272.74

2015 7484.71 6306.64 7362.37 6578.21 6405.50 6463.35 6095.91 6190.50 6456.35 8338.40 5956.48 6329.37

2016 6869.53 8251.55 7484.19 6583.97 6345.97 6334.27 6361.93 6343.46 6396.76 6711.46 7267.72 8396.38

2017 6348.36 6561.56 6155.95 5809.83 5875.18 6220.79 6127.33 6136.16 6355.93 6050.87 7133.16 6134.76

2018 6202.90 6730.19 5837.81 6139.72 6363.94 6283.06 6897.44 7119.88 5808.65 6441.15 5979.02 6240.41

2019 6952.75 6584.73 6568.63 6653.09 5985.60 7749.11 6945.82 8701.39 6079.37

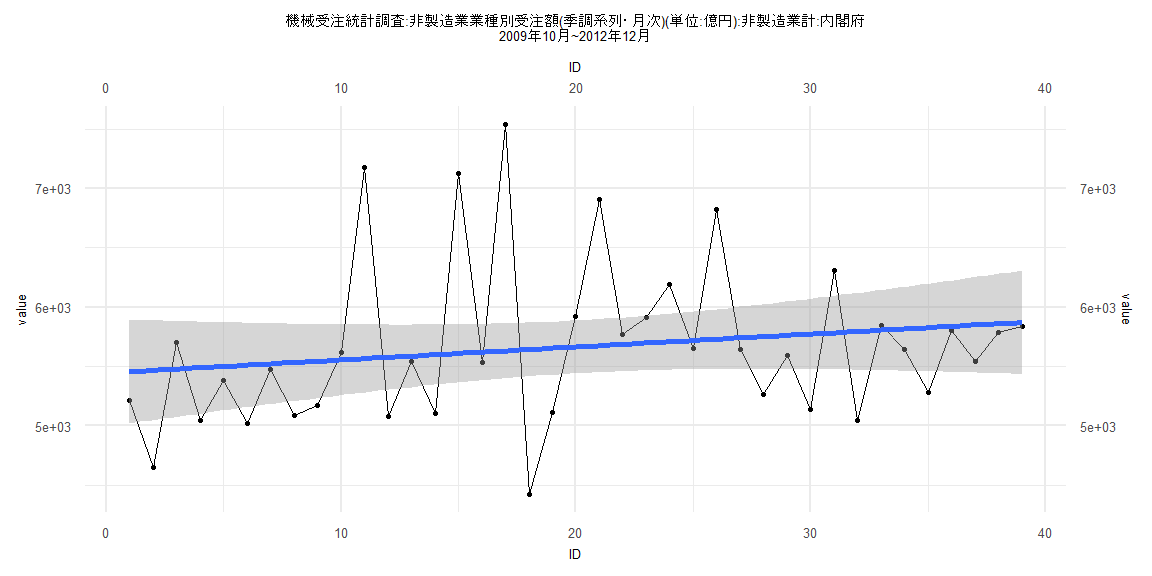

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1220.11 -464.31 -84.71 148.02 1906.98

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5445.416 223.941 24.316 <0.0000000000000002 ***

ID 10.918 9.758 1.119 0.27

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 685.9 on 37 degrees of freedom

Multiple R-squared: 0.03273, Adjusted R-squared: 0.006587

F-statistic: 1.252 on 1 and 37 DF, p-value: 0.2704

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.38462, p-value = 0.00581

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.3801, p-value = 0.8499

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.63329, df = 1, p-value = 0.4262

Box-Ljung test

data: lm_residuals

X-squared = 1.5474, df = 1, p-value = 0.2135

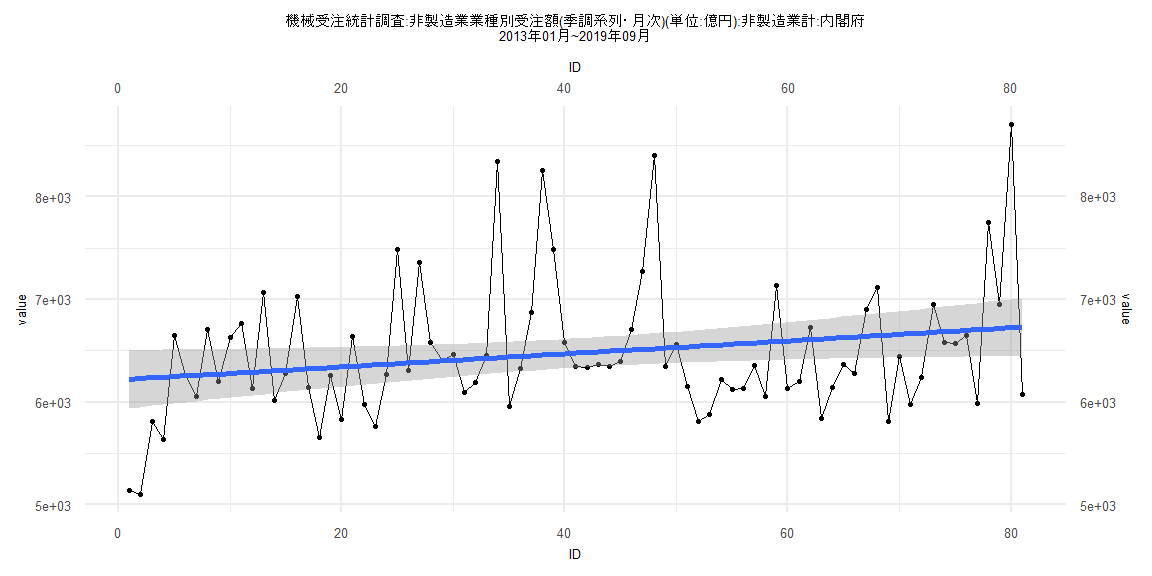

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1127.1 -427.9 -121.8 257.6 1979.3

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6216.460 144.368 43.060 <0.0000000000000002 ***

ID 6.320 3.059 2.066 0.0421 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 643.6 on 79 degrees of freedom

Multiple R-squared: 0.05127, Adjusted R-squared: 0.03926

F-statistic: 4.269 on 1 and 79 DF, p-value: 0.0421

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12346, p-value = 0.5705

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.648, p-value = 0.04288

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.34611, df = 1, p-value = 0.5563

Box-Ljung test

data: lm_residuals

X-squared = 1.9346, df = 1, p-value = 0.1643

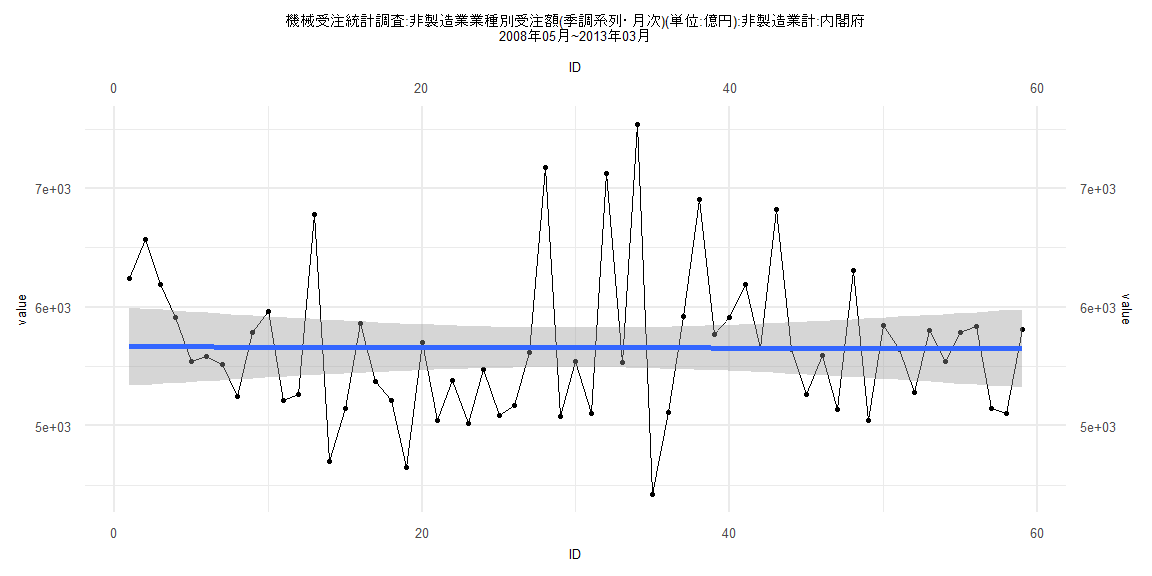

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1234.81 -471.55 -82.46 224.08 1881.10

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5665.7949 168.8091 33.563 <0.0000000000000002 ***

ID -0.2613 4.8935 -0.053 0.958

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 640.1 on 57 degrees of freedom

Multiple R-squared: 5e-05, Adjusted R-squared: -0.01749

F-statistic: 0.00285 on 1 and 57 DF, p-value: 0.9576

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.18644, p-value = 0.2582

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 2.2028, p-value = 0.7416

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.048223, df = 1, p-value = 0.8262

Box-Ljung test

data: lm_residuals

X-squared = 0.73849, df = 1, p-value = 0.3901

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-805.7 -391.3 -166.8 256.6 2047.4

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6376.518 142.998 44.592 <0.0000000000000002 ***

ID 3.603 3.145 1.146 0.256

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 625.4 on 76 degrees of freedom

Multiple R-squared: 0.01698, Adjusted R-squared: 0.004041

F-statistic: 1.312 on 1 and 76 DF, p-value: 0.2555

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.1624

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.7969, p-value = 0.1538

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.0731, df = 1, p-value = 0.3002

Box-Ljung test

data: lm_residuals

X-squared = 0.60859, df = 1, p-value = 0.4353