Analysis

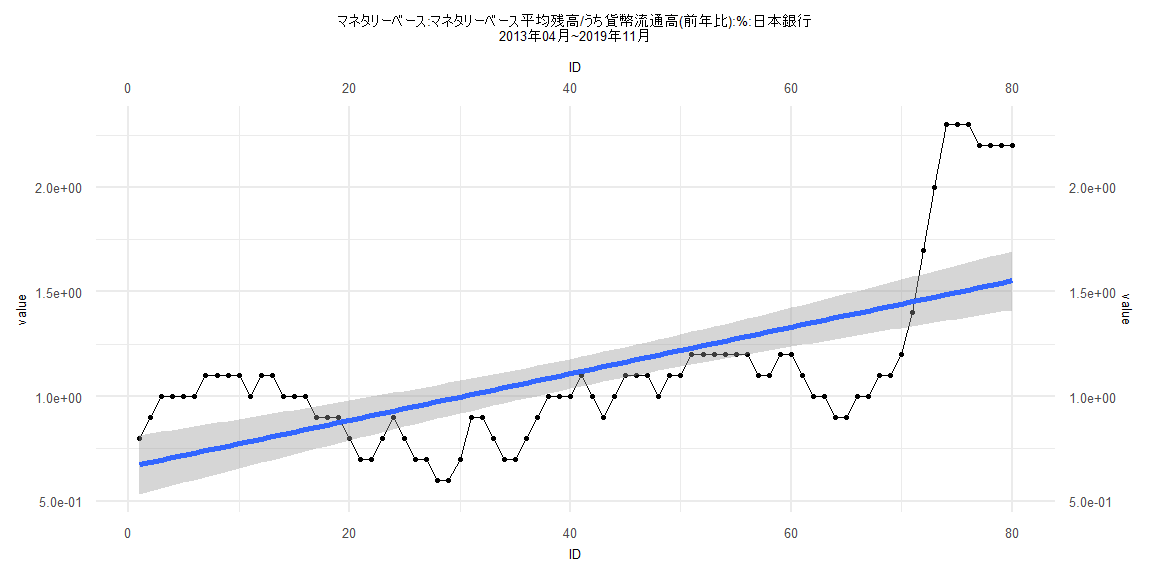

[1] "マネタリーベース:マネタリーベース平均残高/うち貨幣流通高(前年比):%:日本銀行"

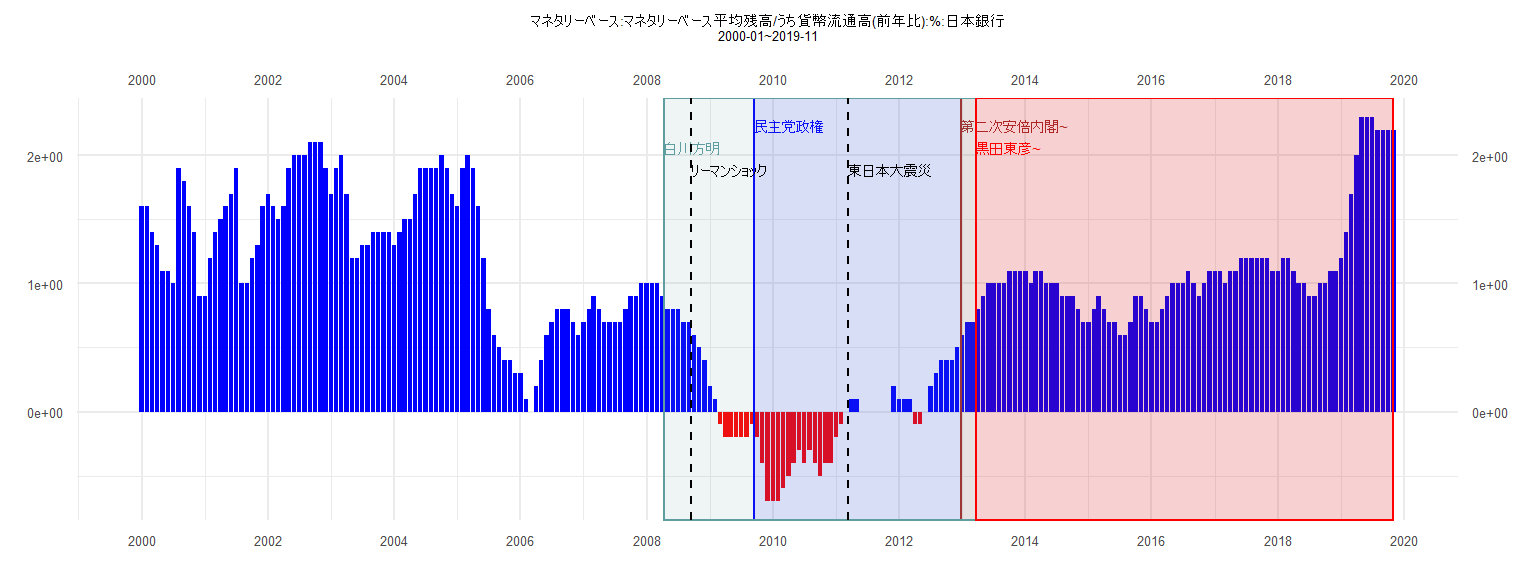

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2000 1.6 1.6 1.4 1.3 1.1 1.1 1.0 1.9 1.8 1.6 1.4 0.9

2001 0.9 1.2 1.4 1.5 1.6 1.7 1.9 1.0 1.0 1.2 1.3 1.6

2002 1.7 1.6 1.5 1.6 1.9 2.0 2.0 2.0 2.1 2.1 2.1 1.9

2003 1.7 1.9 2.0 1.7 1.2 1.2 1.3 1.3 1.4 1.4 1.4 1.4

2004 1.3 1.4 1.5 1.5 1.7 1.9 1.9 1.9 1.9 2.0 1.9 1.7

2005 1.6 1.9 2.0 1.9 1.6 1.2 0.8 0.6 0.5 0.4 0.4 0.3

2006 0.3 0.1 0.0 0.2 0.4 0.6 0.7 0.8 0.8 0.8 0.7 0.6

2007 0.7 0.8 0.9 0.8 0.7 0.7 0.7 0.7 0.8 0.9 0.9 1.0

2008 1.0 1.0 1.0 0.9 0.8 0.8 0.8 0.7 0.7 0.6 0.5 0.4

2009 0.2 0.1 -0.1 -0.2 -0.2 -0.2 -0.2 -0.2 -0.1 -0.2 -0.4 -0.7

2010 -0.7 -0.7 -0.6 -0.5 -0.4 -0.3 -0.4 -0.3 -0.4 -0.5 -0.4 -0.4

2011 -0.2 -0.1 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.2

2012 0.1 0.1 0.1 -0.1 -0.1 0.0 0.2 0.3 0.4 0.4 0.4 0.5

2013 0.6 0.7 0.7 0.8 0.9 1.0 1.0 1.0 1.0 1.1 1.1 1.1

2014 1.1 1.0 1.1 1.1 1.0 1.0 1.0 0.9 0.9 0.9 0.8 0.7

2015 0.7 0.8 0.9 0.8 0.7 0.7 0.6 0.6 0.7 0.9 0.9 0.8

2016 0.7 0.7 0.8 0.9 1.0 1.0 1.0 1.1 1.0 0.9 1.0 1.1

2017 1.1 1.1 1.0 1.1 1.1 1.2 1.2 1.2 1.2 1.2 1.2 1.1

2018 1.1 1.2 1.2 1.1 1.0 1.0 0.9 0.9 1.0 1.0 1.1 1.1

2019 1.2 1.4 1.7 2.0 2.3 2.3 2.3 2.2 2.2 2.2 2.2

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.28923 -0.10538 0.01385 0.09077 0.39769

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.623077 0.048831 -12.76 0.00000000000000405 ***

ID 0.025385 0.002128 11.93 0.00000000000003031 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1496 on 37 degrees of freedom

Multiple R-squared: 0.7937, Adjusted R-squared: 0.7881

F-statistic: 142.3 on 1 and 37 DF, p-value: 0.00000000000003031

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.55459, p-value = 0.00000000944

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.8362, df = 1, p-value = 0.1754

Box-Ljung test

data: lm_residuals

X-squared = 15.99, df = 1, p-value = 0.00006368

Call:

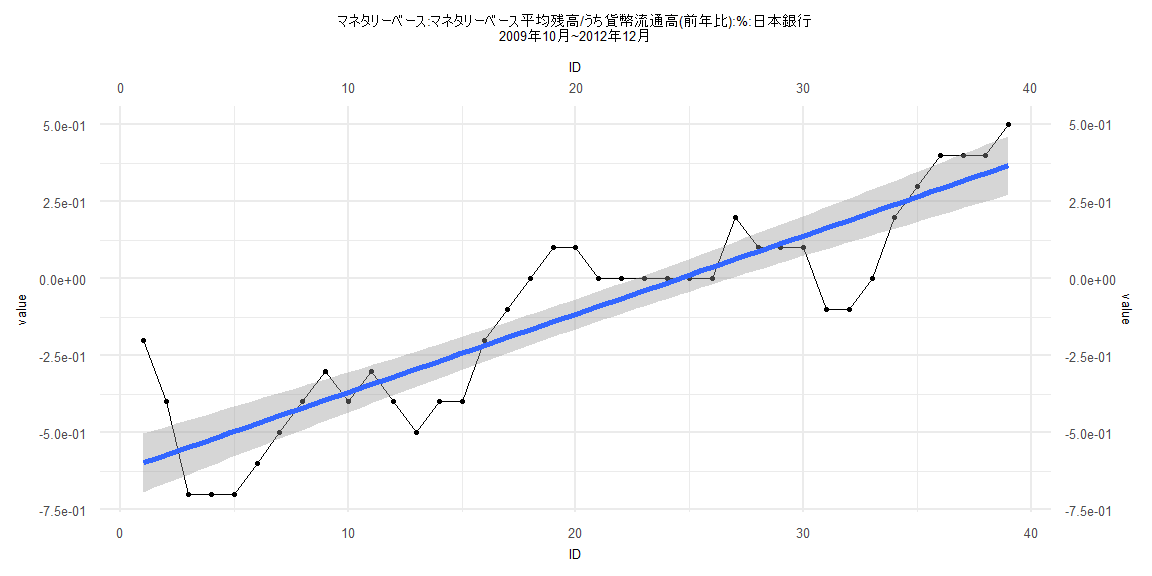

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.48639 -0.20870 -0.08642 0.19675 0.81364

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.631061 0.069538 9.075 0.0000000000000564 ***

ID 0.011108 0.001438 7.724 0.0000000000262318 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3139 on 81 degrees of freedom

Multiple R-squared: 0.4241, Adjusted R-squared: 0.417

F-statistic: 59.66 on 1 and 81 DF, p-value: 0.00000000002623

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14458, p-value = 0.3526

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.089531, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 20.531, df = 1, p-value = 0.000005868

Box-Ljung test

data: lm_residuals

X-squared = 74.237, df = 1, p-value < 0.00000000000000022

Call:

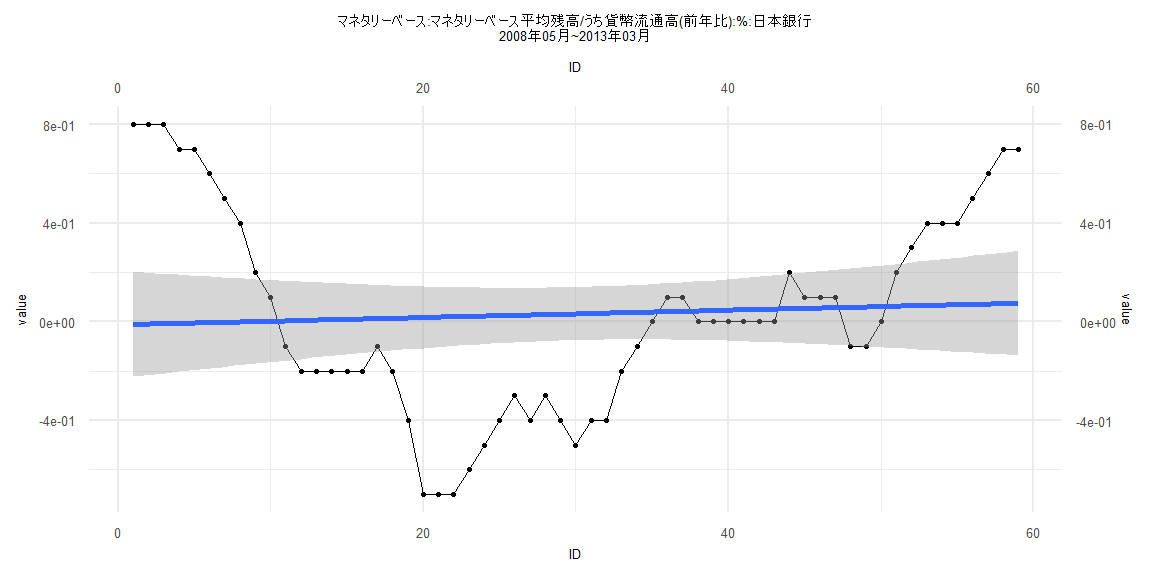

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.72033 -0.22552 -0.04853 0.28291 0.81085

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.012332 0.108854 -0.113 0.91

ID 0.001485 0.003156 0.470 0.64

Residual standard error: 0.4128 on 57 degrees of freedom

Multiple R-squared: 0.003868, Adjusted R-squared: -0.01361

F-statistic: 0.2213 on 1 and 57 DF, p-value: 0.6398

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.066977, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 9.9199, df = 1, p-value = 0.001635

Box-Ljung test

data: lm_residuals

X-squared = 51.675, df = 1, p-value = 0.0000000000006549

Call:

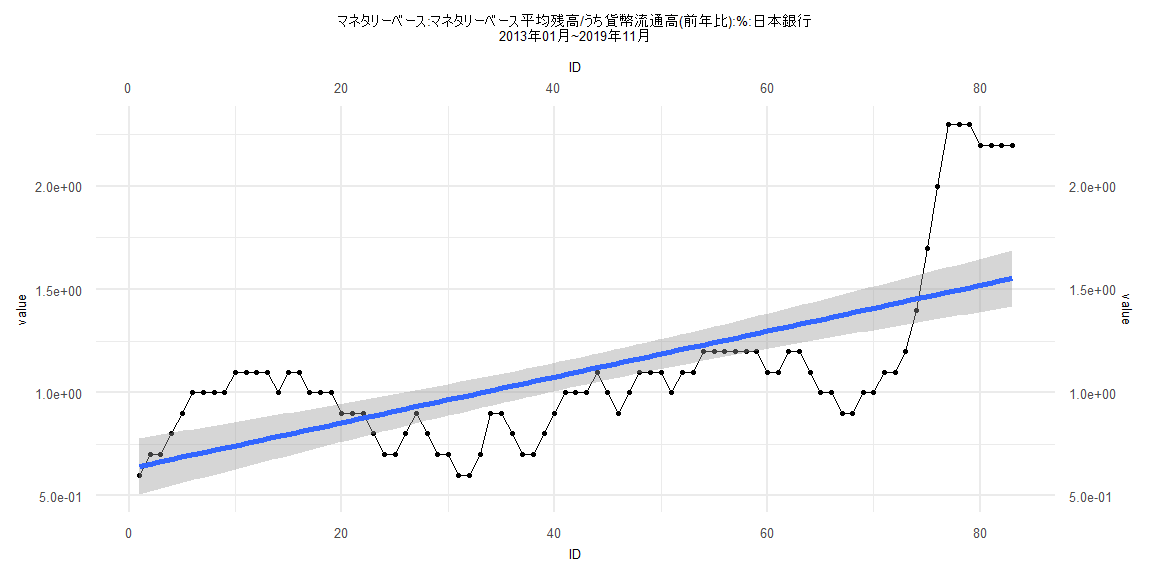

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.48680 -0.21413 -0.08604 0.21511 0.81289

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.662373 0.072179 9.177 0.000000000000049 ***

ID 0.011145 0.001548 7.199 0.000000000329150 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3198 on 78 degrees of freedom

Multiple R-squared: 0.3992, Adjusted R-squared: 0.3915

F-statistic: 51.82 on 1 and 78 DF, p-value: 0.0000000003291

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25, p-value = 0.01319

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.087589, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 18.843, df = 1, p-value = 0.00001419

Box-Ljung test

data: lm_residuals

X-squared = 71.671, df = 1, p-value < 0.00000000000000022