Analysis

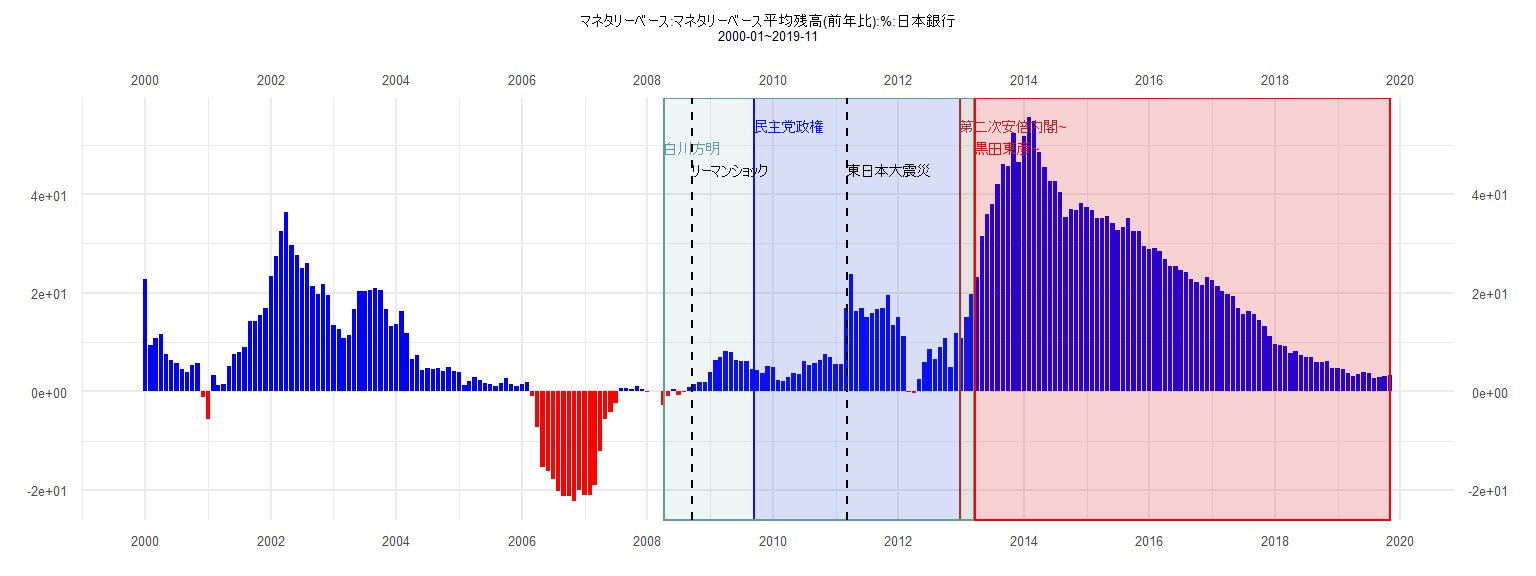

[1] "マネタリーベース:マネタリーベース平均残高(前年比):%:日本銀行"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2000 22.8 9.4 10.9 11.7 7.6 6.4 5.8 4.6 4.0 5.3 5.7 -1.1

2001 -5.6 3.4 1.2 1.4 5.1 7.6 8.0 9.0 14.2 14.3 15.5 16.9

2002 23.4 27.5 32.6 36.3 29.7 27.6 25.1 26.1 21.4 19.8 21.8 19.5

2003 13.4 12.6 10.9 11.5 16.7 20.3 20.4 20.5 20.9 20.6 16.7 13.2

2004 13.6 16.2 11.9 6.6 7.4 4.4 4.7 4.6 4.7 4.2 4.9 4.2

2005 3.9 1.2 2.0 3.0 2.2 1.7 1.5 1.1 1.7 2.8 1.5 1.0

2006 1.4 1.9 -1.0 -7.2 -15.3 -16.2 -17.8 -20.2 -21.2 -21.3 -22.3 -20.0

2007 -21.1 -21.1 -19.1 -12.2 -5.7 -4.1 -2.3 0.7 0.7 0.5 1.0 0.4

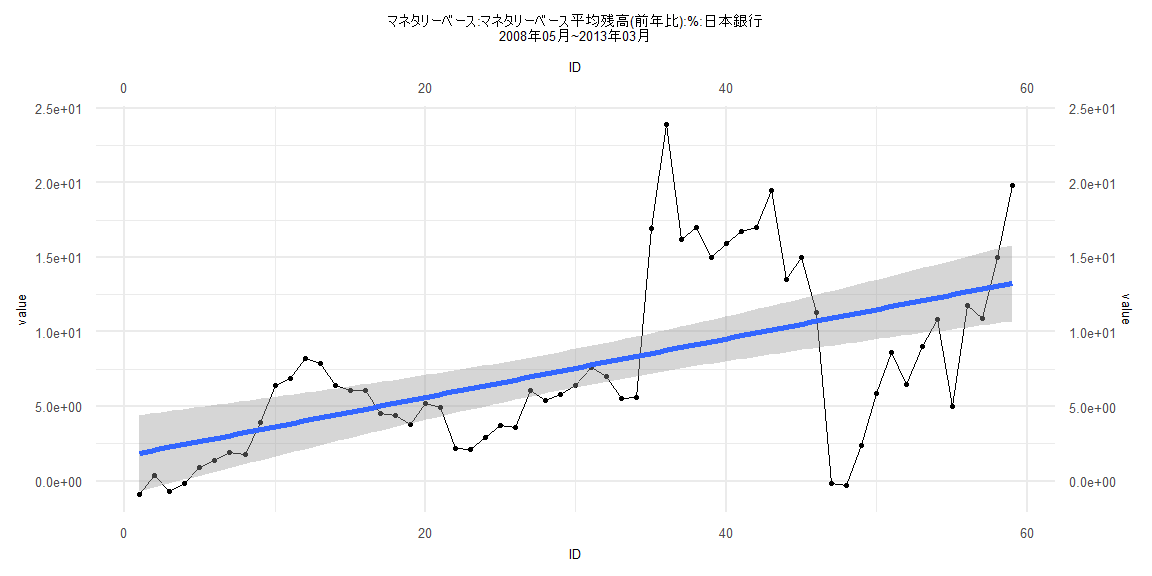

2008 -0.1 0.1 0.0 -2.8 -0.9 0.4 -0.7 -0.2 0.9 1.4 1.9 1.8

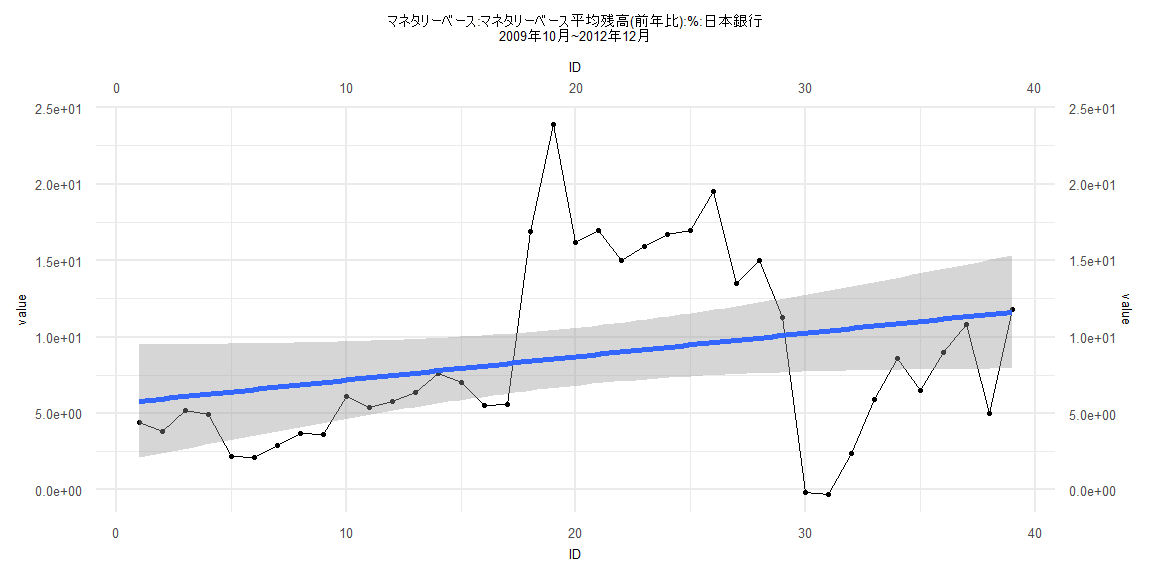

2009 3.9 6.4 6.9 8.2 7.9 6.4 6.1 6.1 4.5 4.4 3.8 5.2

2010 4.9 2.2 2.1 2.9 3.7 3.6 6.1 5.4 5.8 6.4 7.6 7.0

2011 5.5 5.6 16.9 23.9 16.2 17.0 15.0 15.9 16.7 17.0 19.5 13.5

2012 15.0 11.3 -0.2 -0.3 2.4 5.9 8.6 6.5 9.0 10.8 5.0 11.8

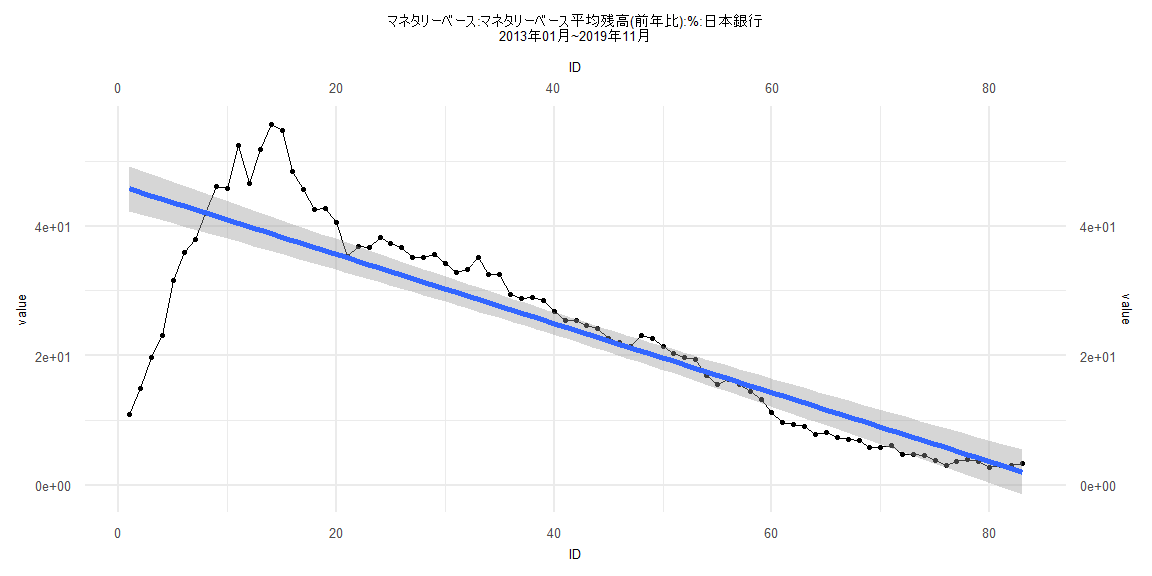

2013 10.9 15.0 19.8 23.1 31.6 36.0 38.0 42.0 46.1 45.8 52.5 46.6

2014 51.9 55.7 54.8 48.5 45.6 42.6 42.7 40.5 35.3 36.9 36.7 38.2

2015 37.4 36.7 35.2 35.2 35.6 34.2 32.8 33.3 35.1 32.5 32.5 29.5

2016 28.9 29.0 28.5 26.8 25.5 25.4 24.7 24.2 22.7 22.1 21.5 23.1

2017 22.6 21.4 20.3 19.8 19.4 17.0 15.6 16.3 15.6 14.5 13.2 11.2

2018 9.7 9.4 9.1 7.8 8.1 7.4 7.0 6.9 5.9 5.9 6.1 4.8

2019 4.7 4.6 3.8 3.1 3.6 4.0 3.7 2.8 3.0 3.1 3.3

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-10.697 -3.291 -1.350 4.390 15.346

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5.63563 1.89992 2.966 0.00526 **

ID 0.15360 0.08279 1.855 0.07152 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.819 on 37 degrees of freedom

Multiple R-squared: 0.08512, Adjusted R-squared: 0.06039

F-statistic: 3.442 on 1 and 37 DF, p-value: 0.07152

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25641, p-value = 0.1547

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.45832, p-value = 0.0000000002809

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.1261, df = 1, p-value = 0.1448

Box-Ljung test

data: lm_residuals

X-squared = 24.952, df = 1, p-value = 0.0000005877

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-34.875 -2.581 1.064 3.862 16.860

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 46.30817 1.76563 26.23 <0.0000000000000002 ***

ID -0.53347 0.03652 -14.61 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.97 on 81 degrees of freedom

Multiple R-squared: 0.7249, Adjusted R-squared: 0.7215

F-statistic: 213.4 on 1 and 81 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.25301, p-value = 0.009606

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.093015, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 17.305, df = 1, p-value = 0.00003184

Box-Ljung test

data: lm_residuals

X-squared = 60.009, df = 1, p-value = 0.000000000000009437

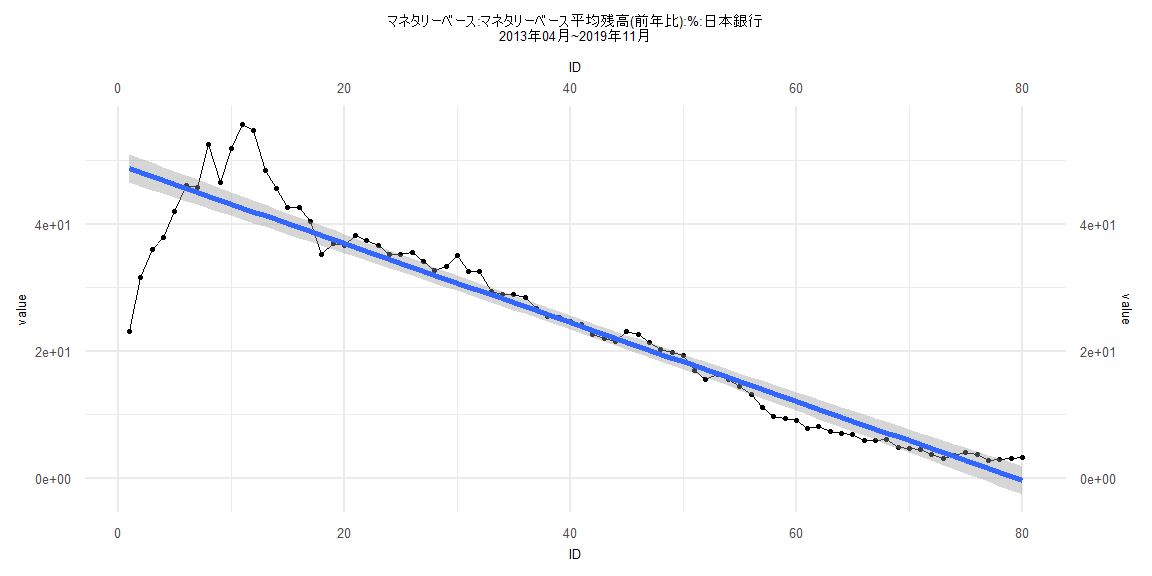

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-11.4028 -2.7572 -0.9576 2.9188 15.1561

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.66715 1.30948 1.273 0.208

ID 0.19658 0.03796 5.179 0.00000304 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.965 on 57 degrees of freedom

Multiple R-squared: 0.3199, Adjusted R-squared: 0.308

F-statistic: 26.82 on 1 and 57 DF, p-value: 0.000003038

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.22034, p-value = 0.1141

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.45027, p-value = 0.00000000000002004

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 7.4667, df = 1, p-value = 0.006285

Box-Ljung test

data: lm_residuals

X-squared = 35.554, df = 1, p-value = 0.00000000248

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-25.6681 -1.2492 0.4182 1.6740 13.1447

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 49.3893 1.1327 43.60 <0.0000000000000002 ***

ID -0.6213 0.0243 -25.57 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.018 on 78 degrees of freedom

Multiple R-squared: 0.8934, Adjusted R-squared: 0.8921

F-statistic: 653.9 on 1 and 78 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.2, p-value = 0.08141

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.21309, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 11.976, df = 1, p-value = 0.0005388

Box-Ljung test

data: lm_residuals

X-squared = 43.335, df = 1, p-value = 0.00000000004612