Analysis

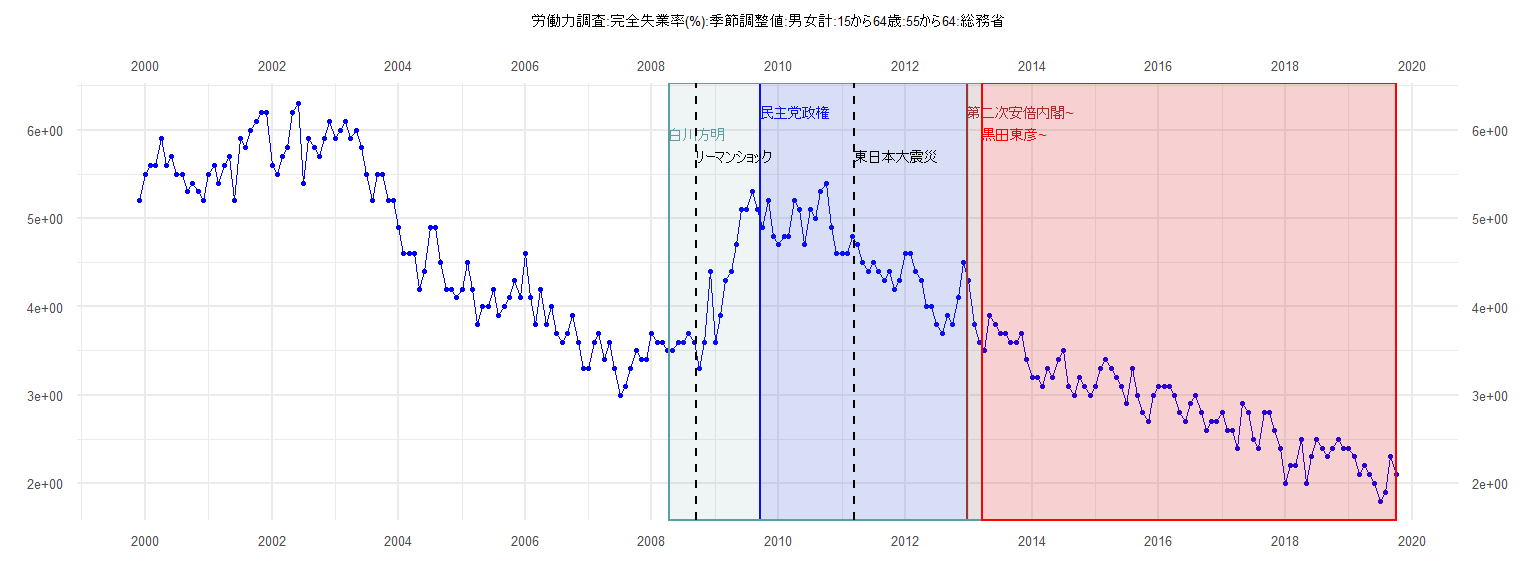

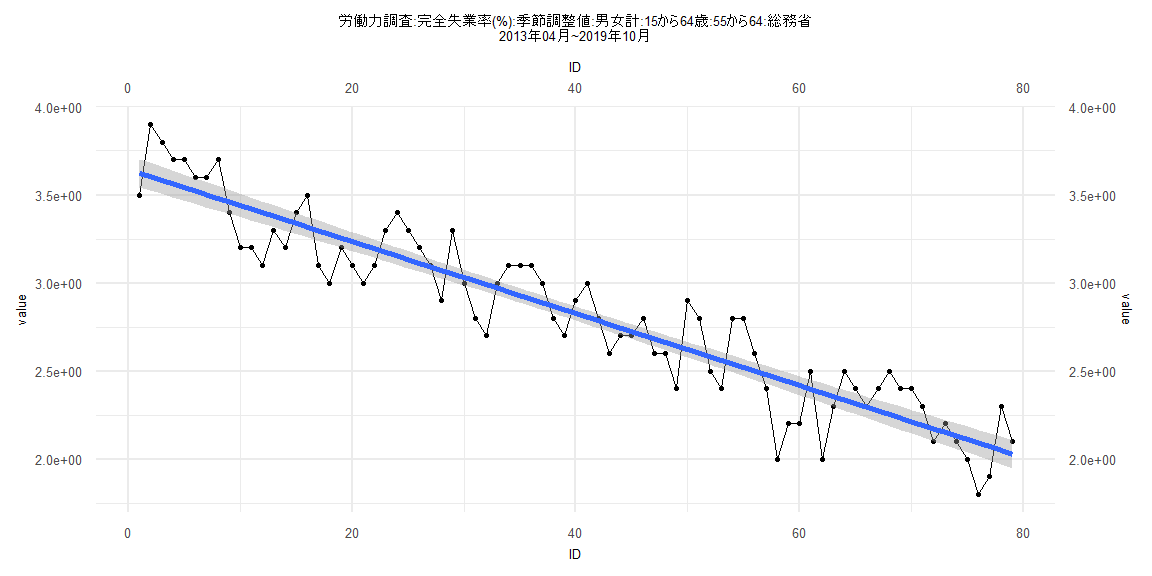

[1] "労働力調査:完全失業率(%):季節調整値:男女計:15から64歳:55から64:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 5.2

2000 5.5 5.6 5.6 5.9 5.6 5.7 5.5 5.5 5.3 5.4 5.3 5.2

2001 5.5 5.6 5.4 5.6 5.7 5.2 5.9 5.8 6.0 6.1 6.2 6.2

2002 5.6 5.5 5.7 5.8 6.2 6.3 5.4 5.9 5.8 5.7 5.9 6.1

2003 5.9 6.0 6.1 5.9 6.0 5.8 5.5 5.2 5.5 5.5 5.2 5.2

2004 4.9 4.6 4.6 4.6 4.2 4.4 4.9 4.9 4.5 4.2 4.2 4.1

2005 4.2 4.5 4.2 3.8 4.0 4.0 4.2 3.9 4.0 4.1 4.3 4.1

2006 4.6 4.1 3.8 4.2 3.8 4.0 3.7 3.6 3.7 3.9 3.6 3.3

2007 3.3 3.6 3.7 3.4 3.6 3.3 3.0 3.1 3.3 3.5 3.4 3.4

2008 3.7 3.6 3.6 3.5 3.5 3.6 3.6 3.7 3.6 3.3 3.6 4.4

2009 3.6 3.9 4.3 4.4 4.7 5.1 5.1 5.3 5.1 4.9 5.2 4.8

2010 4.7 4.8 4.8 5.2 5.1 4.7 5.1 5.0 5.3 5.4 4.9 4.6

2011 4.6 4.6 4.8 4.7 4.5 4.4 4.5 4.4 4.3 4.4 4.2 4.3

2012 4.6 4.6 4.4 4.3 4.0 4.0 3.8 3.7 3.9 3.8 4.1 4.5

2013 4.3 3.8 3.6 3.5 3.9 3.8 3.7 3.7 3.6 3.6 3.7 3.4

2014 3.2 3.2 3.1 3.3 3.2 3.4 3.5 3.1 3.0 3.2 3.1 3.0

2015 3.1 3.3 3.4 3.3 3.2 3.1 2.9 3.3 3.0 2.8 2.7 3.0

2016 3.1 3.1 3.1 3.0 2.8 2.7 2.9 3.0 2.8 2.6 2.7 2.7

2017 2.8 2.6 2.6 2.4 2.9 2.8 2.5 2.4 2.8 2.8 2.6 2.4

2018 2.0 2.2 2.2 2.5 2.0 2.3 2.5 2.4 2.3 2.4 2.5 2.4

2019 2.4 2.3 2.1 2.2 2.1 2.0 1.8 1.9 2.3 2.1

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.39787 -0.18334 -0.05427 0.15663 0.62209

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5.179757 0.080915 64.015 < 0.0000000000000002 ***

ID -0.030911 0.003526 -8.767 0.000000000146 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2478 on 37 degrees of freedom

Multiple R-squared: 0.675, Adjusted R-squared: 0.6663

F-statistic: 76.86 on 1 and 37 DF, p-value: 0.0000000001458

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10256, p-value = 0.9885

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.8765, p-value = 0.0000238

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0041914, df = 1, p-value = 0.9484

Box-Ljung test

data: lm_residuals

X-squared = 9.992, df = 1, p-value = 0.001572

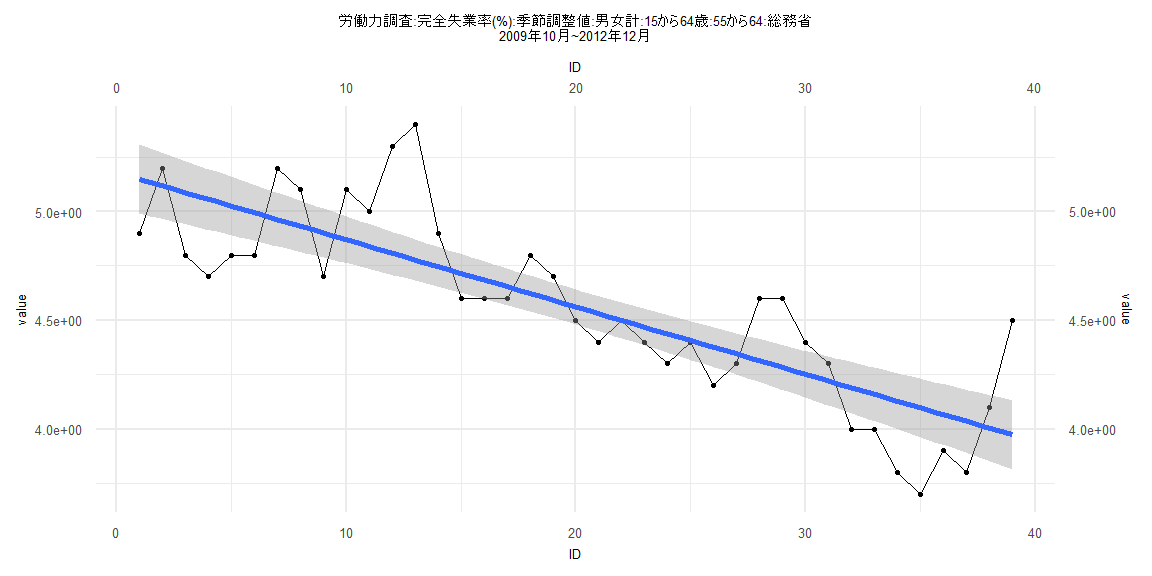

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.45502 -0.15517 0.01071 0.13815 0.58087

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.740199 0.042234 88.56 <0.0000000000000002 ***

ID -0.021069 0.000884 -23.83 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1895 on 80 degrees of freedom

Multiple R-squared: 0.8765, Adjusted R-squared: 0.875

F-statistic: 568 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.097561, p-value = 0.8332

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.178, p-value = 0.00002824

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.75149, df = 1, p-value = 0.386

Box-Ljung test

data: lm_residuals

X-squared = 10.474, df = 1, p-value = 0.001211

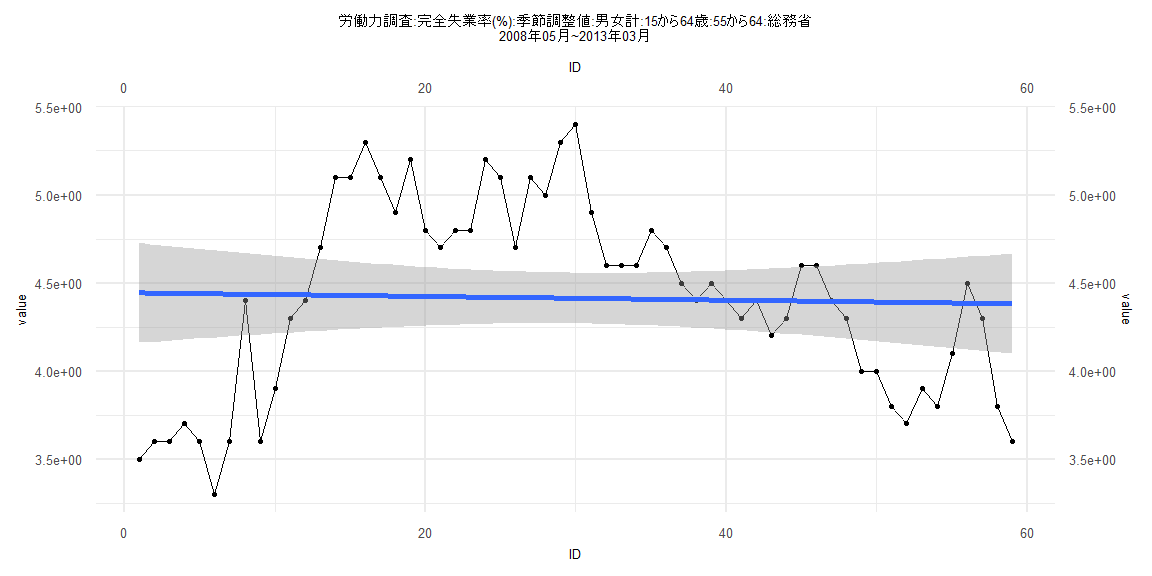

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-1.13881 -0.44147 0.00432 0.37855 0.98644

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.445120 0.145416 30.57 <0.0000000000000002 ***

ID -0.001052 0.004215 -0.25 0.804

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5514 on 57 degrees of freedom

Multiple R-squared: 0.001091, Adjusted R-squared: -0.01643

F-statistic: 0.06228 on 1 and 57 DF, p-value: 0.8038

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15254, p-value = 0.5021

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.25564, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 13.424, df = 1, p-value = 0.0002484

Box-Ljung test

data: lm_residuals

X-squared = 42.621, df = 1, p-value = 0.00000000006643

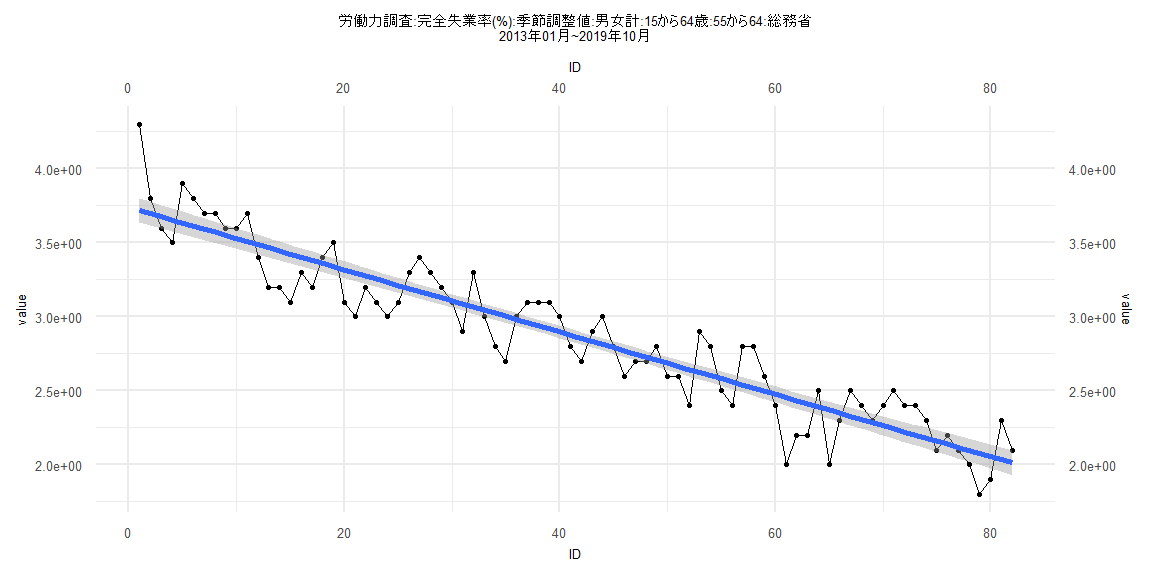

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.45852 -0.14129 0.00759 0.15424 0.29640

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.6444985 0.0409165 89.07 <0.0000000000000002 ***

ID -0.0204479 0.0008886 -23.01 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1801 on 77 degrees of freedom

Multiple R-squared: 0.873, Adjusted R-squared: 0.8714

F-statistic: 529.5 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12658, p-value = 0.5543

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.2472, p-value = 0.000155

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.039121, df = 1, p-value = 0.8432

Box-Ljung test

data: lm_residuals

X-squared = 11.373, df = 1, p-value = 0.0007453