Analysis

[1] "労働力調査:完全失業率(%):季節調整値:男女計:65歳以上:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 2.0

2000 2.1 2.5 2.2 2.1 2.2 2.1 2.0 2.2 2.4 2.4 2.3 2.2

2001 2.3 2.5 2.7 2.5 2.8 2.5 2.1 2.2 2.4 2.6 2.1 2.4

2002 2.1 1.7 2.2 2.3 2.2 2.2 2.1 2.1 2.0 2.4 2.4 2.2

2003 2.7 2.5 2.2 2.3 2.3 2.5 2.9 2.6 2.5 2.0 2.5 2.6

2004 2.3 2.3 2.1 2.0 1.6 1.9 2.0 1.8 1.9 2.4 2.3 2.1

2005 1.8 2.1 2.0 1.9 2.5 2.1 1.7 1.7 1.8 1.9 2.0 1.9

2006 2.1 1.9 1.9 1.9 1.9 2.0 2.2 2.4 2.4 2.1 1.7 2.1

2007 2.3 2.3 2.1 2.0 1.8 1.5 1.9 1.9 1.9 1.6 1.7 1.9

2008 1.8 2.0 2.2 2.2 2.5 2.4 2.0 2.2 1.7 2.1 2.5 1.9

2009 1.8 1.9 2.5 2.5 2.3 2.7 2.9 2.5 3.0 2.9 2.6 2.8

2010 2.6 2.3 2.1 2.5 2.5 2.7 2.7 2.6 2.3 2.5 2.4 2.5

2011 2.7 2.7 2.1 2.3 2.0 1.8 2.0 1.9 2.4 2.4 2.0 1.8

2012 2.2 2.3 2.5 2.0 2.7 2.4 2.0 2.0 2.0 1.9 2.2 2.8

2013 2.2 2.2 2.4 2.1 2.0 2.4 2.4 2.5 2.1 2.3 2.6 2.0

2014 2.3 2.0 2.1 2.3 2.1 2.0 2.4 2.4 2.1 2.1 2.0 2.3

2015 2.1 2.1 2.0 2.2 1.9 2.0 1.8 1.9 2.2 1.9 1.8 1.6

2016 1.7 2.0 2.3 1.9 2.1 1.9 1.8 1.9 2.3 2.0 1.9 1.9

2017 2.3 1.8 1.6 1.7 1.9 2.1 1.8 1.6 1.4 1.7 1.8 2.0

2018 1.5 1.7 1.5 1.7 1.7 1.4 1.6 1.7 1.4 1.5 1.4 1.4

2019 1.9 1.5 1.6 1.5 1.1 1.7 2.2 1.7 1.3 1.4

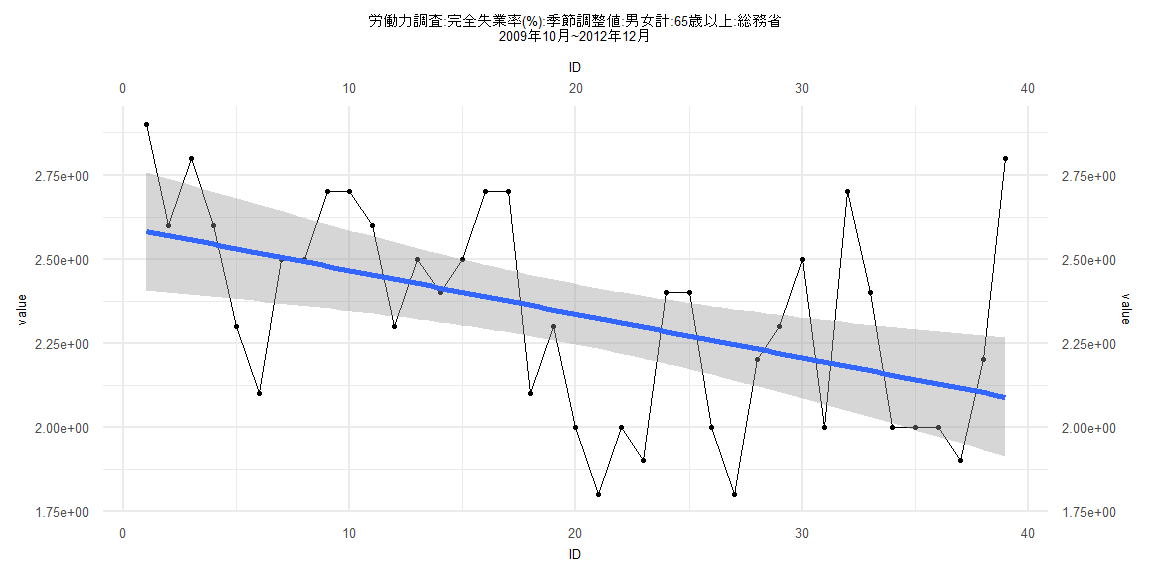

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.52292 -0.20424 0.00839 0.18435 0.71064

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.59541 0.09043 28.701 < 0.0000000000000002 ***

ID -0.01298 0.00394 -3.293 0.00219 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.277 on 37 degrees of freedom

Multiple R-squared: 0.2266, Adjusted R-squared: 0.2057

F-statistic: 10.84 on 1 and 37 DF, p-value: 0.002188

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.20513, p-value = 0.3888

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.1958, p-value = 0.002365

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.5033, df = 1, p-value = 0.1136

Box-Ljung test

data: lm_residuals

X-squared = 3.6703, df = 1, p-value = 0.05539

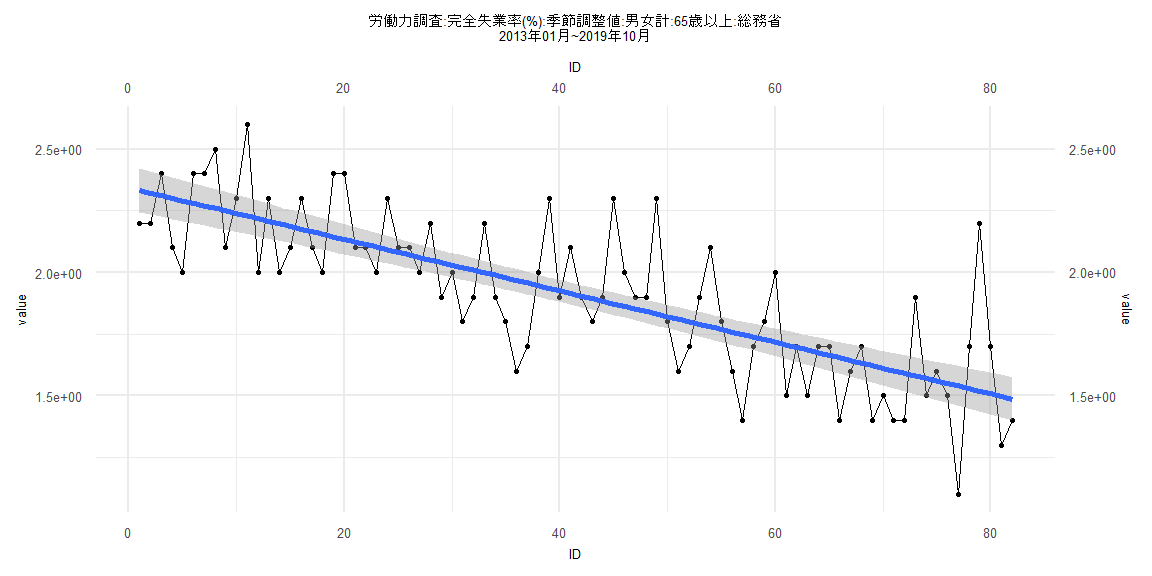

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43907 -0.14690 -0.02241 0.11725 0.68181

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.3430894 0.0454303 51.58 <0.0000000000000002 ***

ID -0.0104418 0.0009509 -10.98 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2038 on 80 degrees of freedom

Multiple R-squared: 0.6012, Adjusted R-squared: 0.5962

F-statistic: 120.6 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.097561, p-value = 0.8332

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.7609, p-value = 0.1141

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.4741, df = 1, p-value = 0.1157

Box-Ljung test

data: lm_residuals

X-squared = 1.1392, df = 1, p-value = 0.2858

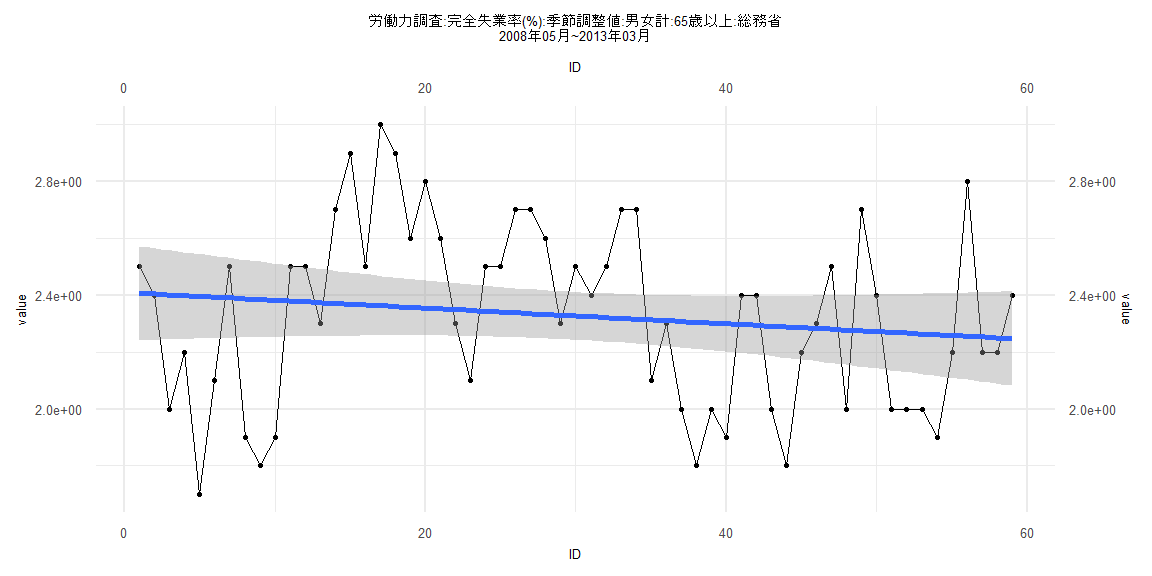

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.69579 -0.26806 0.01683 0.19898 0.63717

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.409527 0.084613 28.48 <0.0000000000000002 ***

ID -0.002747 0.002453 -1.12 0.267

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3208 on 57 degrees of freedom

Multiple R-squared: 0.02153, Adjusted R-squared: 0.004364

F-statistic: 1.254 on 1 and 57 DF, p-value: 0.2674

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11864, p-value = 0.8052

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0174, p-value = 0.00001324

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.7455, df = 1, p-value = 0.09753

Box-Ljung test

data: lm_residuals

X-squared = 14.811, df = 1, p-value = 0.0001189

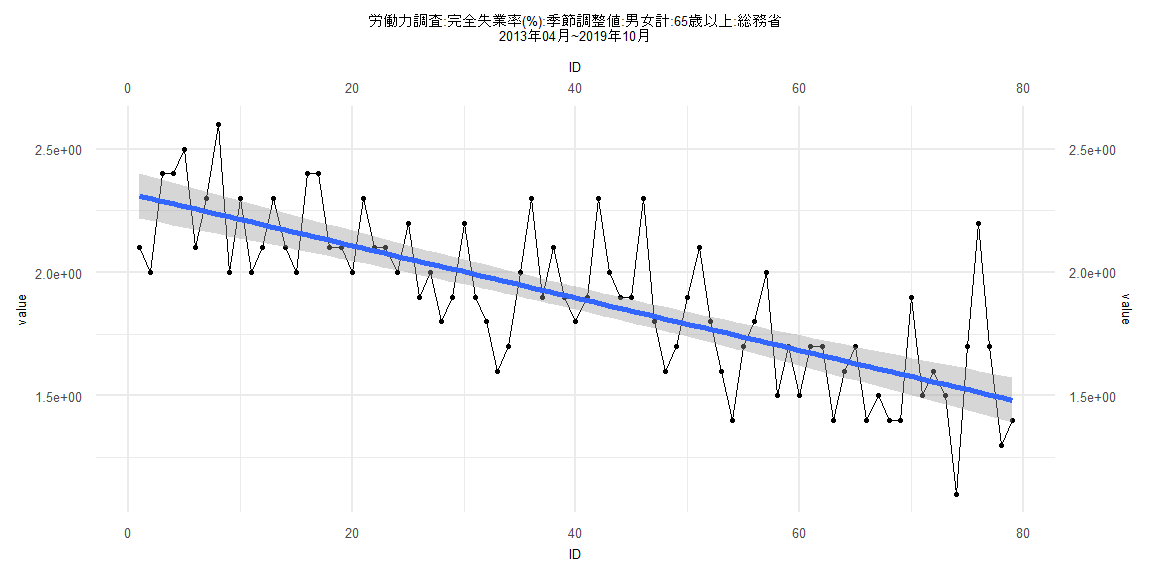

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.43535 -0.15764 -0.02191 0.11417 0.68588

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.320740 0.046896 49.49 < 0.0000000000000002 ***

ID -0.010613 0.001019 -10.42 0.000000000000000229 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2064 on 77 degrees of freedom

Multiple R-squared: 0.5851, Adjusted R-squared: 0.5797

F-statistic: 108.6 on 1 and 77 DF, p-value: 0.0000000000000002295

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10127, p-value = 0.8161

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.7444, p-value = 0.1034

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.9236, df = 1, p-value = 0.1655

Box-Ljung test

data: lm_residuals

X-squared = 1.1826, df = 1, p-value = 0.2768