Analysis

[1] "労働力調査(主要項目):完全失業者(万人):季節調整値:女:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 119

2000 122 124 123 128 124 125 120 120 122 121 126 126

2001 128 125 126 124 128 130 130 133 141 133 139 139

2002 136 144 143 136 141 145 141 139 136 137 132 141

2003 145 137 135 140 139 136 135 130 130 130 133 127

2004 126 126 123 125 122 119 121 125 117 118 114 114

2005 114 117 116 117 118 108 119 113 112 119 122 115

2006 111 101 106 106 107 116 109 106 107 105 102 103

2007 107 111 108 102 102 95 93 101 106 107 103 102

2008 104 107 108 110 104 108 108 107 107 99 107 117

2009 118 127 135 130 134 133 138 137 142 135 137 139

2010 132 125 127 130 129 130 126 129 126 128 127 122

2011 120 122 120 115 114 121 119 115 106 109 112 111

2012 118 116 117 115 114 110 112 106 108 109 105 109

2013 106 110 101 107 109 99 93 104 100 106 105 100

2014 98 96 99 95 96 98 103 91 96 95 89 93

2015 94 93 89 90 86 87 91 91 90 81 86 83

2016 85 83 85 86 83 85 81 80 76 79 81 76

2017 80 78 78 78 84 78 74 74 78 77 73 77

2018 68 70 70 66 63 67 69 69 67 65 67 67

2019 75 66 68 71 65 61 64 62 67 70

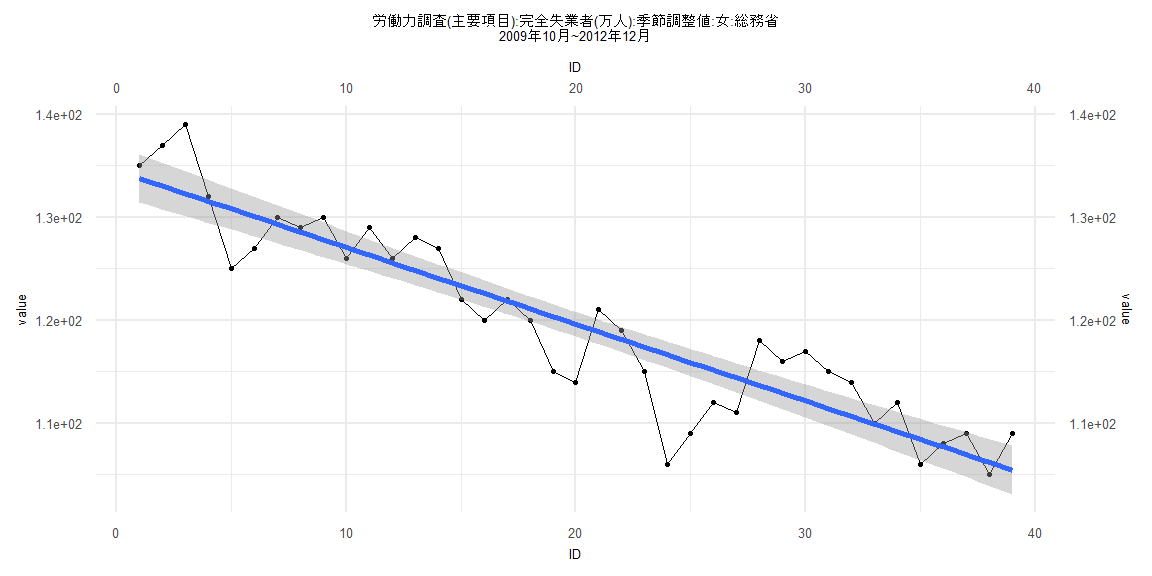

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-10.6340 -2.4073 0.4405 2.8660 6.7138

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 134.52227 1.21090 111.09 <0.0000000000000002 ***

ID -0.74534 0.05276 -14.13 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.709 on 37 degrees of freedom

Multiple R-squared: 0.8436, Adjusted R-squared: 0.8394

F-statistic: 199.5 on 1 and 37 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.0343, p-value = 0.0003034

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.0044327, df = 1, p-value = 0.9469

Box-Ljung test

data: lm_residuals

X-squared = 9.2557, df = 1, p-value = 0.002348

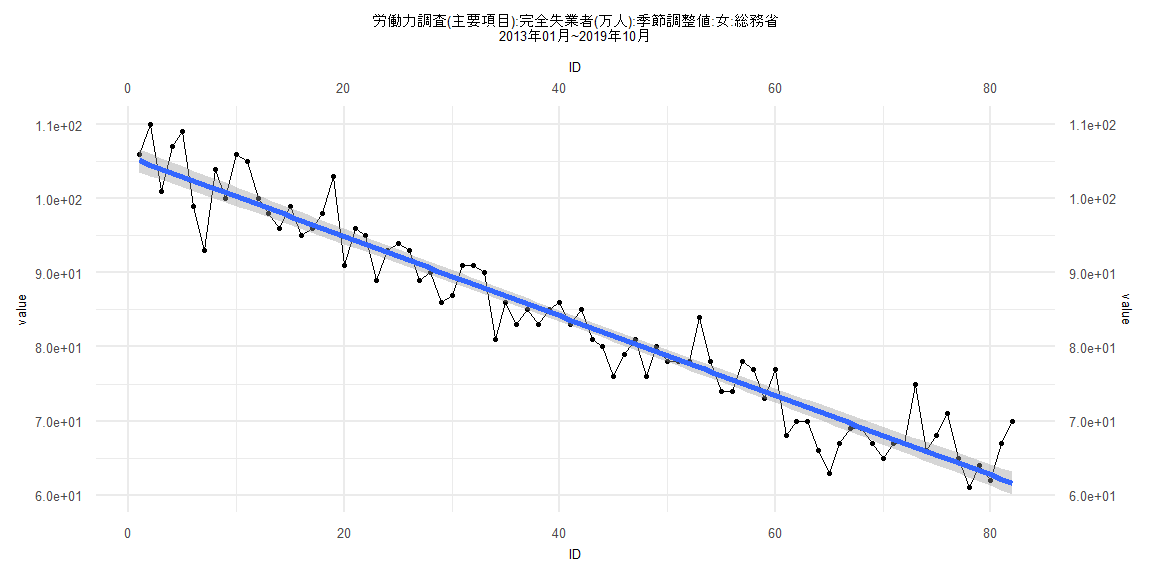

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-8.8773 -2.1220 -0.3901 1.8841 8.5359

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 105.6332 0.7788 135.63 <0.0000000000000002 ***

ID -0.5366 0.0163 -32.91 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.494 on 80 degrees of freedom

Multiple R-squared: 0.9312, Adjusted R-squared: 0.9304

F-statistic: 1083 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.097561, p-value = 0.8332

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5999, p-value = 0.02548

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.022401, df = 1, p-value = 0.881

Box-Ljung test

data: lm_residuals

X-squared = 2.2817, df = 1, p-value = 0.1309

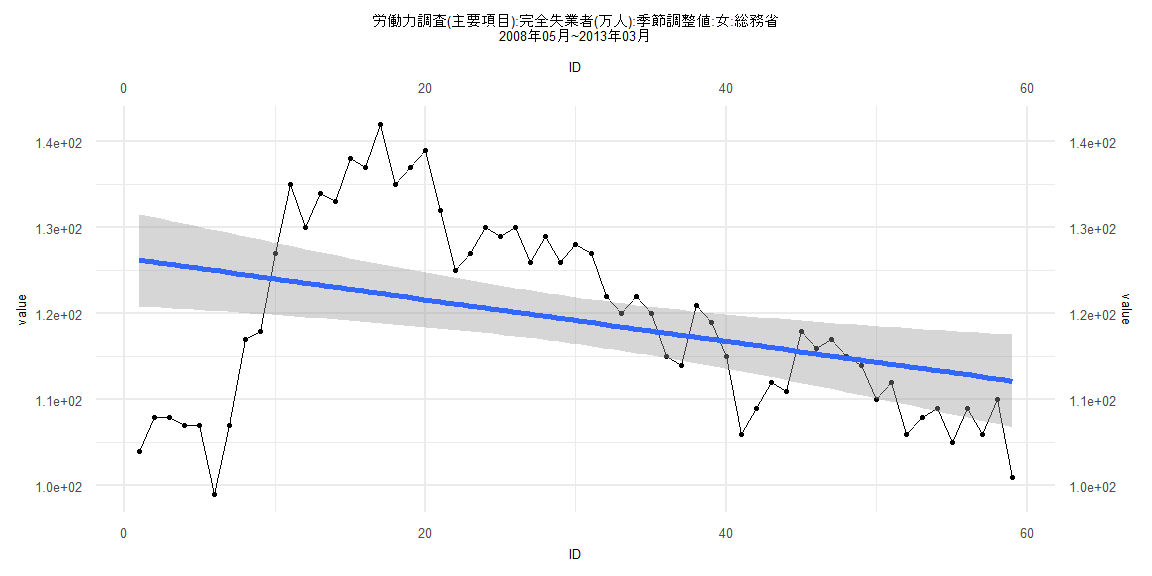

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-26.015 -5.961 1.523 8.312 19.649

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 126.46756 2.75410 45.920 < 0.0000000000000002 ***

ID -0.24214 0.07984 -3.033 0.00364 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 10.44 on 57 degrees of freedom

Multiple R-squared: 0.139, Adjusted R-squared: 0.1238

F-statistic: 9.199 on 1 and 57 DF, p-value: 0.003642

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.19062, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 24.614, df = 1, p-value = 0.0000007005

Box-Ljung test

data: lm_residuals

X-squared = 45.351, df = 1, p-value = 0.00000000001647

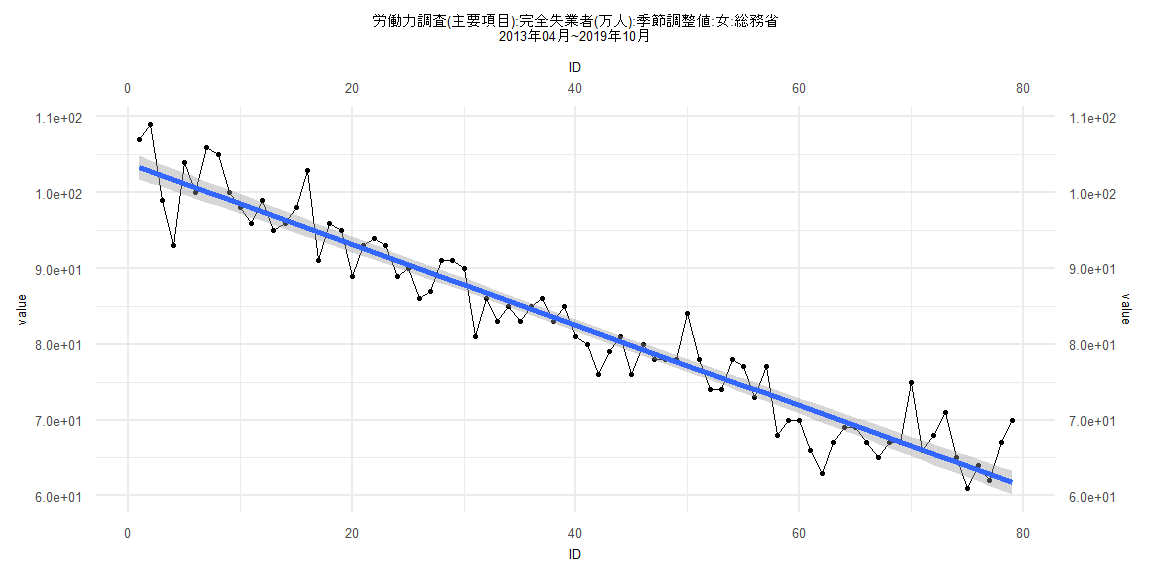

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-8.713 -2.018 -0.381 1.916 8.476

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 103.84518 0.79228 131.07 <0.0000000000000002 ***

ID -0.53315 0.01721 -30.98 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.488 on 77 degrees of freedom

Multiple R-squared: 0.9258, Adjusted R-squared: 0.9248

F-statistic: 960 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.11392, p-value = 0.6878

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5244, p-value = 0.0116

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.01876, df = 1, p-value = 0.8911

Box-Ljung test

data: lm_residuals

X-squared = 3.087, df = 1, p-value = 0.07892