Analysis

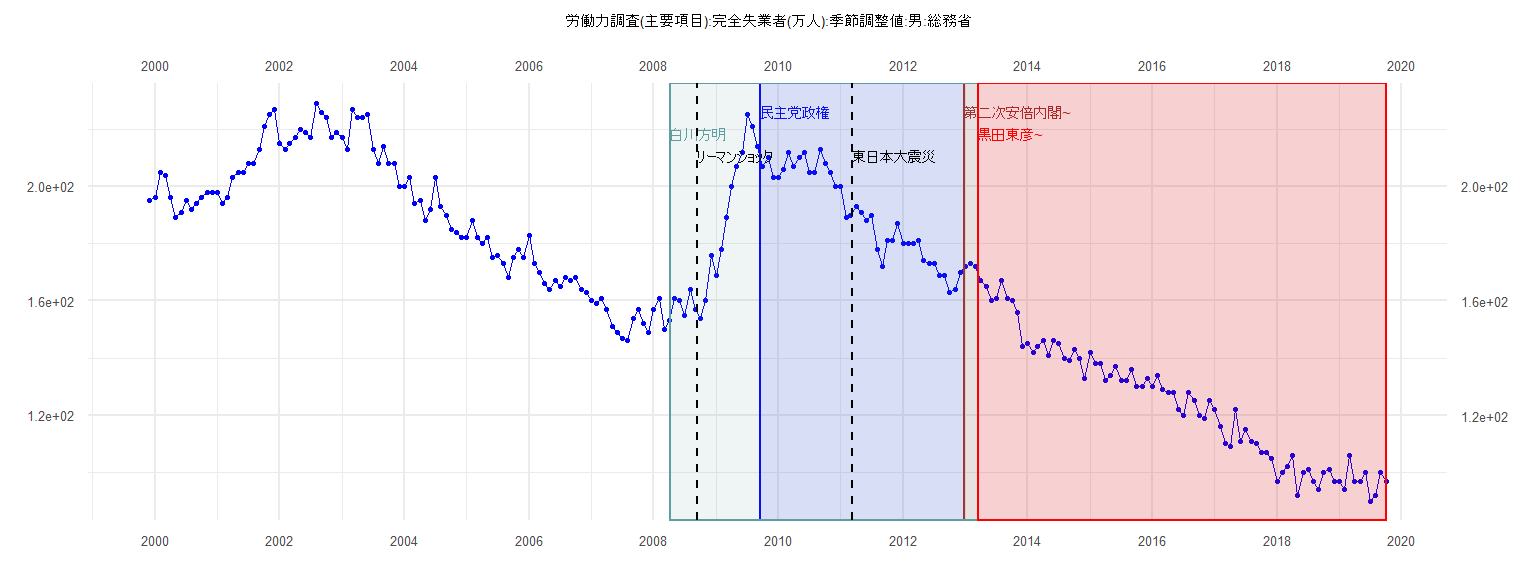

[1] "労働力調査(主要項目):完全失業者(万人):季節調整値:男:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 195

2000 196 205 204 196 189 191 195 192 194 196 198 198

2001 198 194 196 203 205 205 208 208 213 221 225 227

2002 215 213 215 217 220 219 217 229 226 224 217 219

2003 217 213 227 224 224 225 213 208 214 208 208 200

2004 200 203 194 195 188 192 203 193 190 185 184 182

2005 182 188 182 180 182 175 176 173 168 175 178 175

2006 183 173 170 166 164 167 165 168 167 168 164 163

2007 160 159 161 157 151 149 147 146 154 157 152 149

2008 157 161 150 153 161 160 155 164 157 154 160 176

2009 169 178 189 200 207 212 225 221 214 207 210 203

2010 203 206 212 207 210 212 205 205 213 208 205 200

2011 200 189 190 193 191 188 190 178 172 181 181 187

2012 180 180 180 181 174 173 173 169 169 163 164 170

2013 172 173 172 167 165 160 161 167 161 160 156 144

2014 145 142 144 146 141 146 145 140 139 143 140 133

2015 142 138 138 132 134 137 132 132 136 130 130 133

2016 130 134 129 128 128 122 120 128 125 120 119 125

2017 122 116 110 109 122 111 115 111 110 107 107 105

2018 97 100 102 106 92 100 101 97 94 100 101 97

2019 97 94 106 97 97 100 90 92 100 97

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-13.1692 -3.0346 -0.0077 3.4885 12.4154

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 216.00000 1.75435 123.1 <0.0000000000000002 ***

ID -1.28462 0.07645 -16.8 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.373 on 37 degrees of freedom

Multiple R-squared: 0.8842, Adjusted R-squared: 0.881

F-statistic: 282.4 on 1 and 37 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12821, p-value = 0.9114

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.8563, p-value = 0.00001639

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.9456, df = 1, p-value = 0.08611

Box-Ljung test

data: lm_residuals

X-squared = 12.094, df = 1, p-value = 0.0005057

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-11.5874 -3.1368 -0.8248 2.9476 11.7111

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 164.02800 1.18542 138.37 <0.0000000000000002 ***

ID -0.92985 0.02481 -37.48 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.318 on 80 degrees of freedom

Multiple R-squared: 0.9461, Adjusted R-squared: 0.9454

F-statistic: 1404 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10976, p-value = 0.7099

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.93587, p-value = 0.00000004088

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.52856, df = 1, p-value = 0.4672

Box-Ljung test

data: lm_residuals

X-squared = 20.901, df = 1, p-value = 0.000004837

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-37.553 -12.583 -1.632 17.352 35.104

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 192.6569 4.9942 38.576 <0.0000000000000002 ***

ID -0.1840 0.1448 -1.271 0.209

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 18.94 on 57 degrees of freedom

Multiple R-squared: 0.02757, Adjusted R-squared: 0.01051

F-statistic: 1.616 on 1 and 57 DF, p-value: 0.2088

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.16949, p-value = 0.3674

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.10493, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 26.409, df = 1, p-value = 0.0000002763

Box-Ljung test

data: lm_residuals

X-squared = 52.63, df = 1, p-value = 0.0000000000004028

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-11.8700 -3.0684 -0.8539 3.0536 11.8605

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 159.63681 1.12862 141.4 <0.0000000000000002 ***

ID -0.89946 0.02451 -36.7 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.968 on 77 degrees of freedom

Multiple R-squared: 0.9459, Adjusted R-squared: 0.9452

F-statistic: 1347 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.088608, p-value = 0.9184

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.1035, p-value = 0.00000692

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.016694, df = 1, p-value = 0.8972

Box-Ljung test

data: lm_residuals

X-squared = 13.902, df = 1, p-value = 0.0001926