Analysis

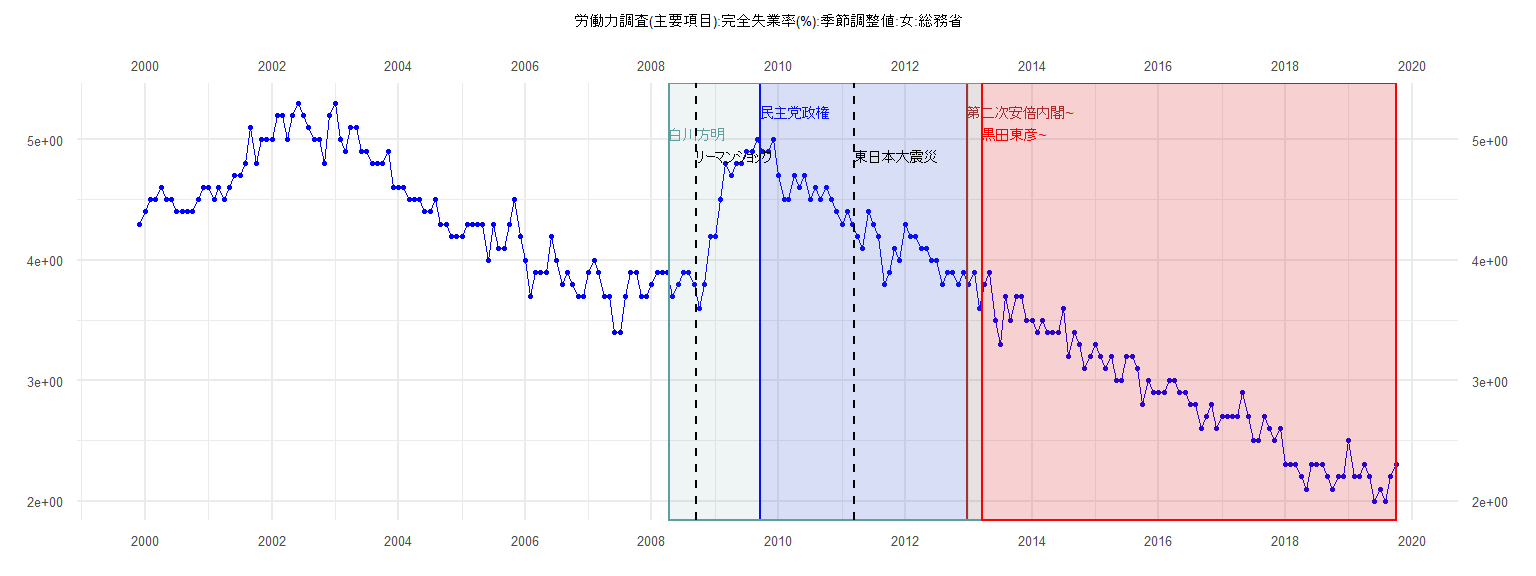

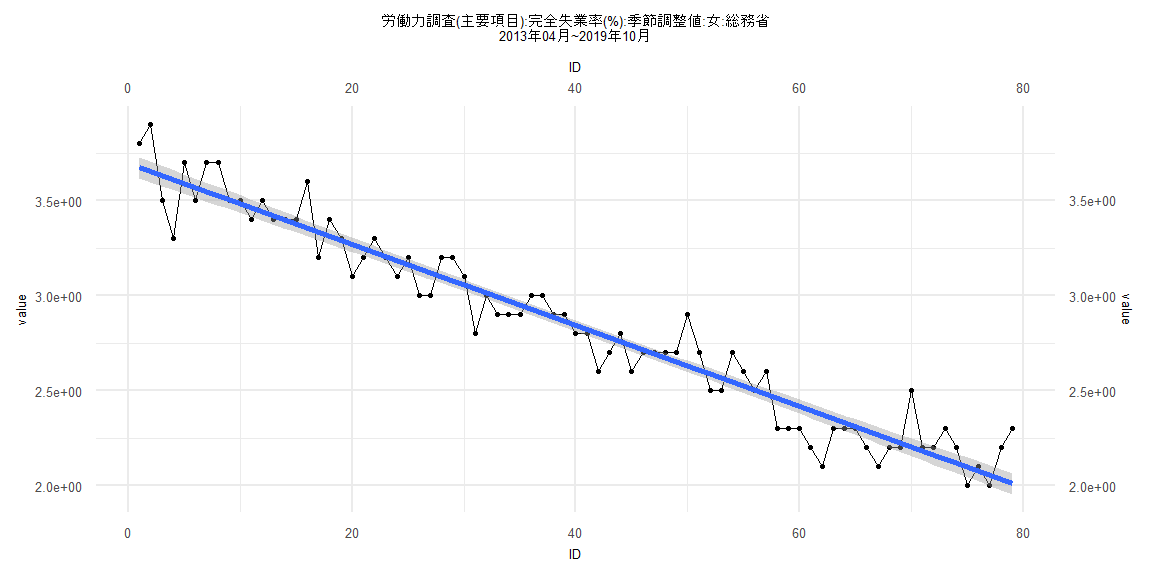

[1] "労働力調査(主要項目):完全失業率(%):季節調整値:女:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 4.3

2000 4.4 4.5 4.5 4.6 4.5 4.5 4.4 4.4 4.4 4.4 4.5 4.6

2001 4.6 4.5 4.6 4.5 4.6 4.7 4.7 4.8 5.1 4.8 5.0 5.0

2002 5.0 5.2 5.2 5.0 5.2 5.3 5.2 5.1 5.0 5.0 4.8 5.2

2003 5.3 5.0 4.9 5.1 5.1 4.9 4.9 4.8 4.8 4.8 4.9 4.6

2004 4.6 4.6 4.5 4.5 4.5 4.4 4.4 4.5 4.3 4.3 4.2 4.2

2005 4.2 4.3 4.3 4.3 4.3 4.0 4.3 4.1 4.1 4.3 4.5 4.2

2006 4.0 3.7 3.9 3.9 3.9 4.2 4.0 3.8 3.9 3.8 3.7 3.7

2007 3.9 4.0 3.9 3.7 3.7 3.4 3.4 3.7 3.9 3.9 3.7 3.7

2008 3.8 3.9 3.9 3.9 3.7 3.8 3.9 3.9 3.8 3.6 3.8 4.2

2009 4.2 4.5 4.8 4.7 4.8 4.8 4.9 4.9 5.0 4.9 4.9 5.0

2010 4.7 4.5 4.5 4.7 4.6 4.7 4.5 4.6 4.5 4.6 4.5 4.4

2011 4.3 4.4 4.3 4.2 4.1 4.4 4.3 4.2 3.8 3.9 4.1 4.0

2012 4.3 4.2 4.2 4.1 4.1 4.0 4.0 3.8 3.9 3.9 3.8 3.9

2013 3.8 3.9 3.6 3.8 3.9 3.5 3.3 3.7 3.5 3.7 3.7 3.5

2014 3.5 3.4 3.5 3.4 3.4 3.4 3.6 3.2 3.4 3.3 3.1 3.2

2015 3.3 3.2 3.1 3.2 3.0 3.0 3.2 3.2 3.1 2.8 3.0 2.9

2016 2.9 2.9 3.0 3.0 2.9 2.9 2.8 2.8 2.6 2.7 2.8 2.6

2017 2.7 2.7 2.7 2.7 2.9 2.7 2.5 2.5 2.7 2.6 2.5 2.6

2018 2.3 2.3 2.3 2.2 2.1 2.3 2.3 2.3 2.2 2.1 2.2 2.2

2019 2.5 2.2 2.2 2.3 2.2 2.0 2.1 2.0 2.2 2.3

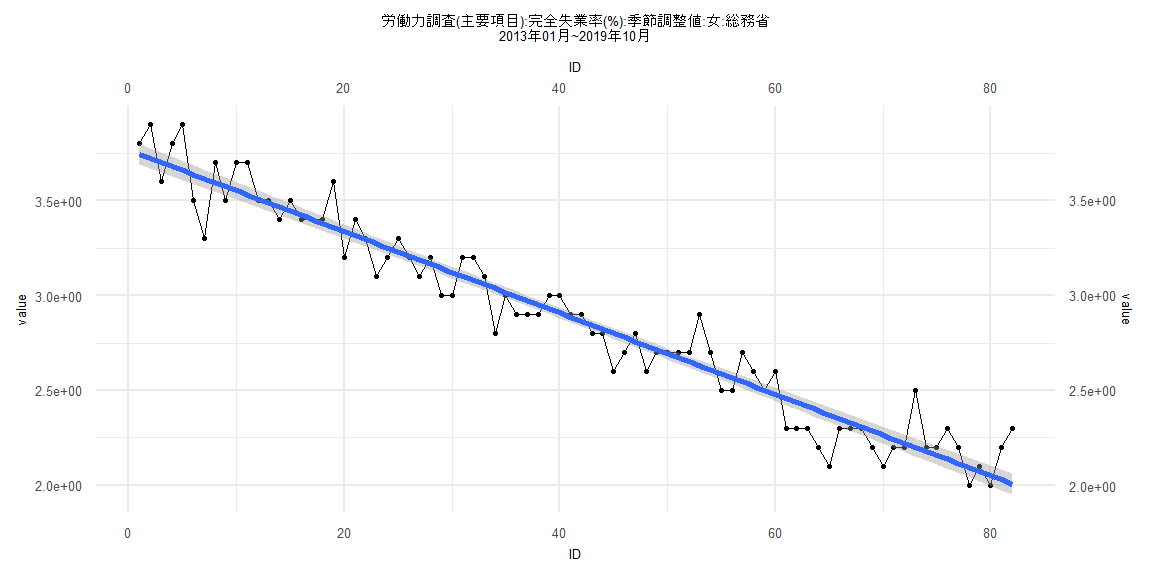

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.39795 -0.05949 0.01897 0.09744 0.25282

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.825641 0.043960 109.77 < 0.0000000000000002 ***

ID -0.026154 0.001916 -13.65 0.000000000000000507 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1346 on 37 degrees of freedom

Multiple R-squared: 0.8344, Adjusted R-squared: 0.8299

F-statistic: 186.4 on 1 and 37 DF, p-value: 0.000000000000000507

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.15385, p-value = 0.7523

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.2431, p-value = 0.00396

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.035284, df = 1, p-value = 0.851

Box-Ljung test

data: lm_residuals

X-squared = 5.5843, df = 1, p-value = 0.01812

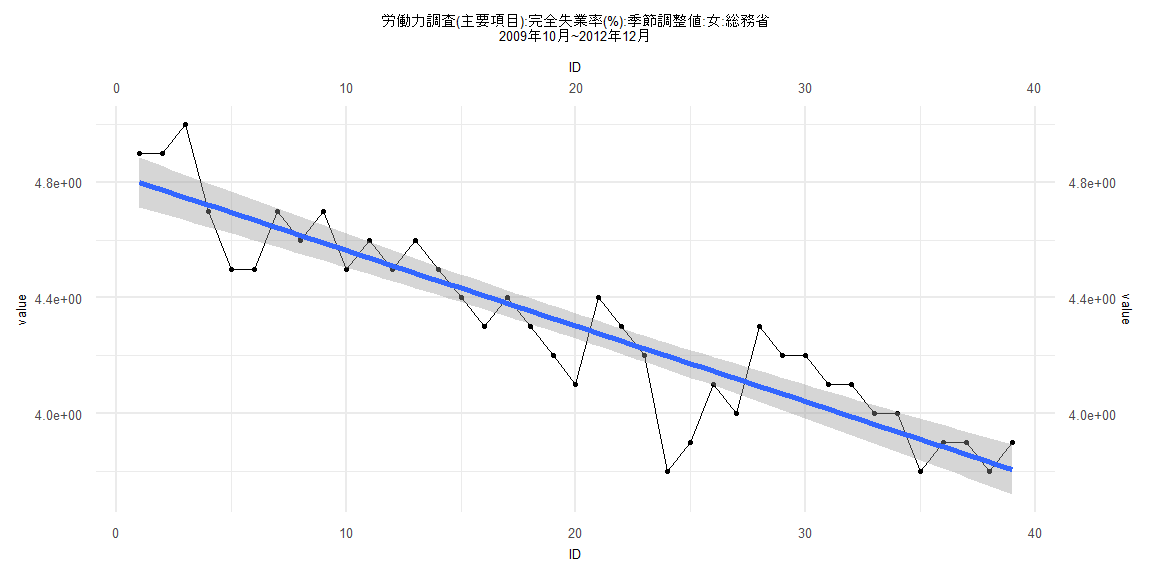

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.315091 -0.084415 -0.004176 0.076243 0.299569

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.7651310 0.0280281 134.33 <0.0000000000000002 ***

ID -0.0214342 0.0005867 -36.54 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1257 on 80 degrees of freedom

Multiple R-squared: 0.9435, Adjusted R-squared: 0.9428

F-statistic: 1335 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14634, p-value = 0.3453

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5992, p-value = 0.0253

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.089768, df = 1, p-value = 0.7645

Box-Ljung test

data: lm_residuals

X-squared = 2.3239, df = 1, p-value = 0.1274

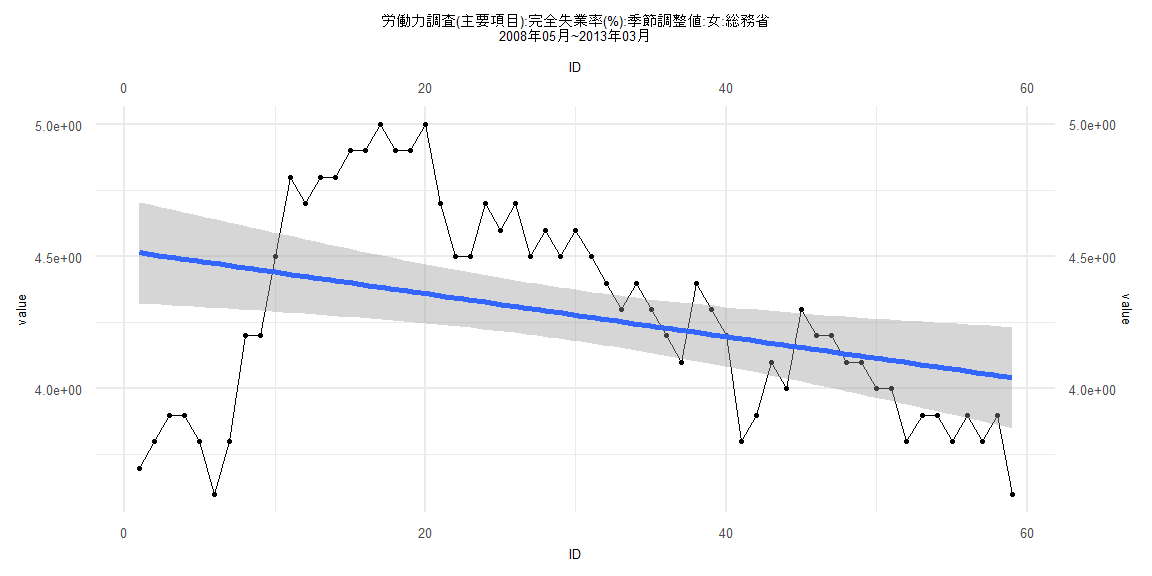

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.87364 -0.21981 0.05248 0.27827 0.64050

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.522560 0.098081 46.111 < 0.0000000000000002 ***

ID -0.008153 0.002843 -2.868 0.00579 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3719 on 57 degrees of freedom

Multiple R-squared: 0.1261, Adjusted R-squared: 0.1107

F-statistic: 8.223 on 1 and 57 DF, p-value: 0.005789

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.10169, p-value = 0.9239

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.18674, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 24.587, df = 1, p-value = 0.0000007103

Box-Ljung test

data: lm_residuals

X-squared = 45.065, df = 1, p-value = 0.00000000001906

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-0.308481 -0.080206 -0.001994 0.076282 0.297152

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.6936709 0.0285831 129.23 <0.0000000000000002 ***

ID -0.0212975 0.0006208 -34.31 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1258 on 77 degrees of freedom

Multiple R-squared: 0.9386, Adjusted R-squared: 0.9378

F-statistic: 1177 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.050633, p-value = 1

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.5435, p-value = 0.01457

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.060691, df = 1, p-value = 0.8054

Box-Ljung test

data: lm_residuals

X-squared = 2.88, df = 1, p-value = 0.08968