Analysis

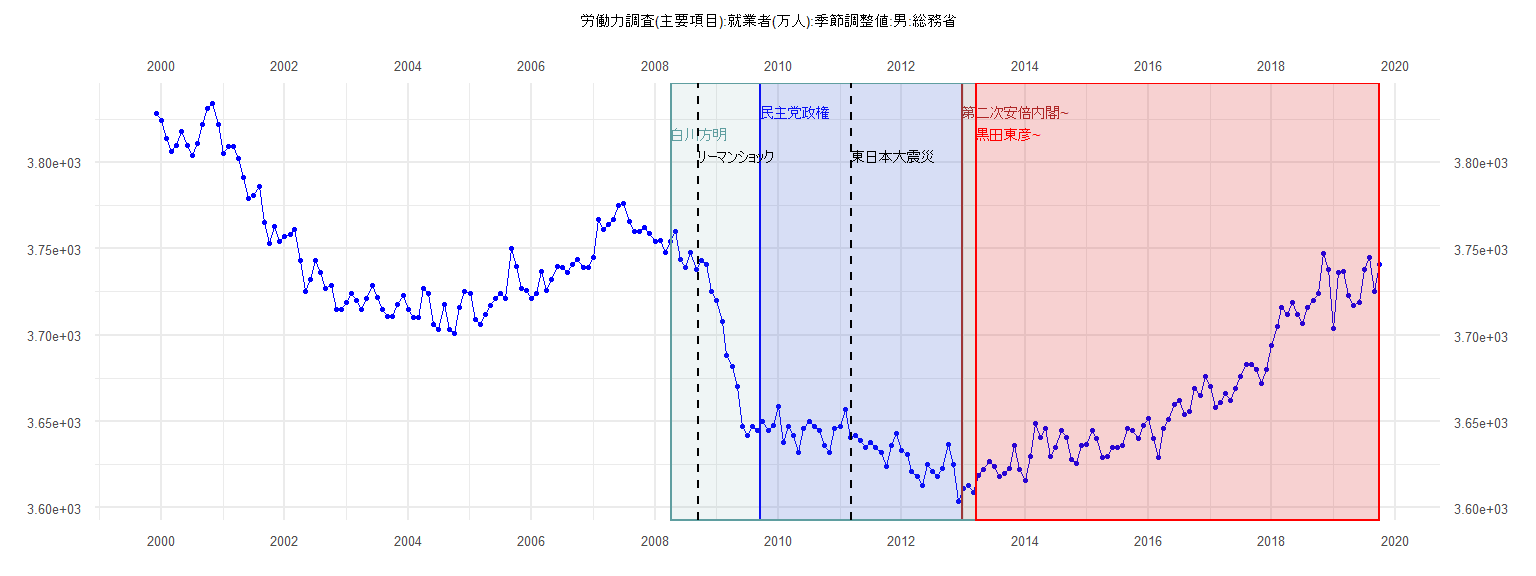

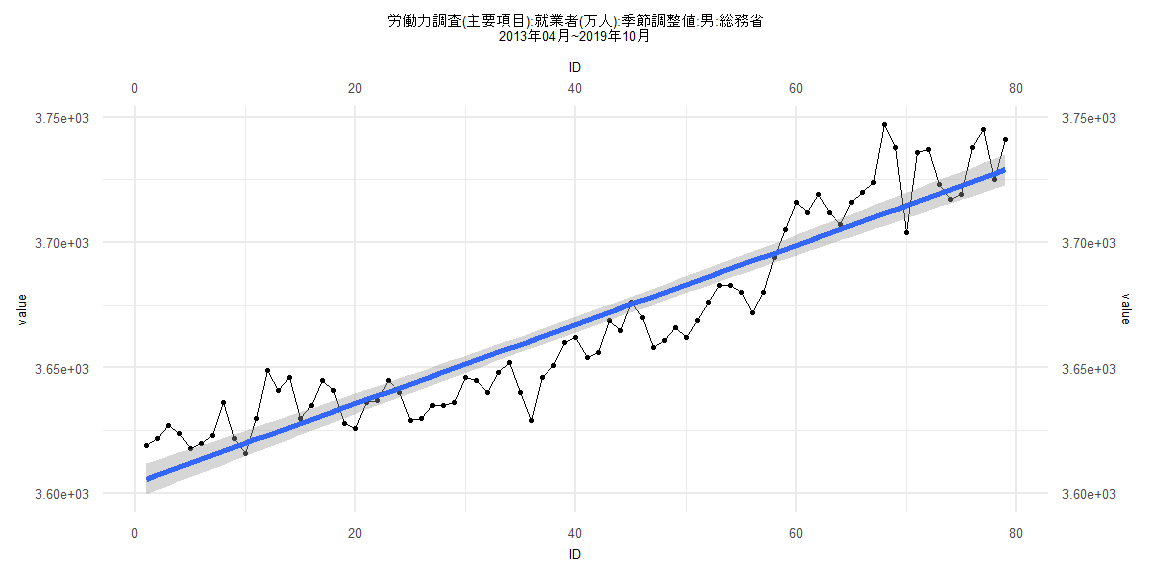

[1] "労働力調査(主要項目):就業者(万人):季節調整値:男:総務省"

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1999 3828

2000 3824 3814 3806 3810 3818 3810 3804 3811 3822 3831 3834 3822

2001 3805 3809 3809 3802 3791 3779 3781 3786 3765 3753 3763 3754

2002 3757 3758 3761 3743 3725 3732 3743 3736 3727 3729 3715 3715

2003 3719 3724 3720 3715 3721 3729 3722 3715 3711 3711 3718 3723

2004 3715 3710 3710 3727 3724 3706 3703 3718 3703 3701 3716 3725

2005 3724 3709 3706 3712 3717 3721 3724 3721 3750 3740 3727 3726

2006 3721 3724 3737 3726 3732 3740 3739 3736 3741 3744 3739 3739

2007 3745 3767 3761 3764 3767 3775 3776 3766 3760 3760 3762 3759

2008 3754 3755 3748 3754 3760 3744 3739 3748 3738 3743 3741 3725

2009 3720 3708 3688 3682 3670 3647 3642 3647 3645 3650 3645 3648

2010 3659 3638 3647 3642 3632 3646 3650 3647 3645 3636 3632 3646

2011 3647 3657 3641 3642 3639 3635 3638 3635 3632 3624 3636 3643

2012 3633 3631 3621 3618 3613 3625 3621 3618 3623 3637 3625 3604

2013 3611 3613 3609 3619 3622 3627 3624 3618 3620 3623 3636 3622

2014 3616 3630 3649 3641 3646 3630 3635 3645 3641 3628 3626 3636

2015 3637 3645 3640 3629 3630 3635 3635 3636 3646 3645 3640 3648

2016 3652 3640 3629 3646 3651 3660 3662 3654 3656 3669 3665 3676

2017 3670 3658 3661 3666 3662 3669 3676 3683 3683 3680 3672 3680

2018 3694 3705 3716 3712 3719 3712 3707 3716 3720 3724 3747 3738

2019 3704 3736 3737 3723 3717 3719 3738 3745 3725 3741

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-16.061 -5.584 0.434 3.930 18.573

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3652.6194 2.5417 1437.093 < 0.0000000000000002 ***

ID -0.8348 0.1108 -7.538 0.00000000551 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.784 on 37 degrees of freedom

Multiple R-squared: 0.6056, Adjusted R-squared: 0.595

F-statistic: 56.82 on 1 and 37 DF, p-value: 0.000000005512

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.17949, p-value = 0.5622

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 1.4049, p-value = 0.01811

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 0.96895, df = 1, p-value = 0.3249

Box-Ljung test

data: lm_residuals

X-squared = 2.4101, df = 1, p-value = 0.1206

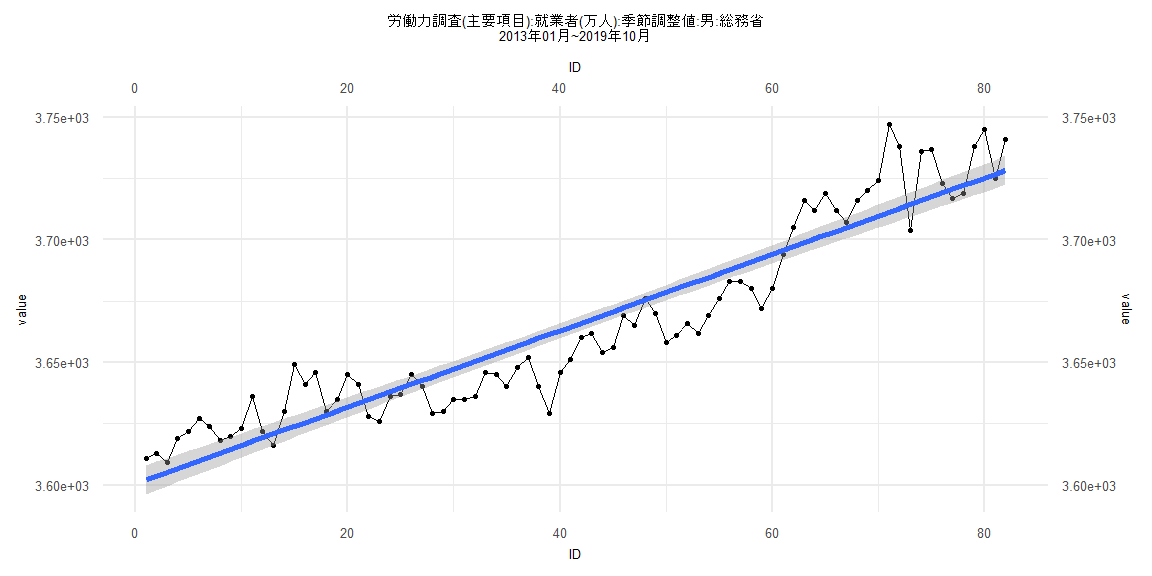

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-32.323 -10.367 -1.866 11.150 35.797

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3600.53117 3.02597 1189.88 <0.0000000000000002 ***

ID 1.55876 0.06334 24.61 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 13.58 on 80 degrees of freedom

Multiple R-squared: 0.8833, Adjusted R-squared: 0.8819

F-statistic: 605.7 on 1 and 80 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.14634, p-value = 0.3453

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.57649, p-value = 0.000000000000004016

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 2.5171, df = 1, p-value = 0.1126

Box-Ljung test

data: lm_residuals

X-squared = 42.102, df = 1, p-value = 0.00000000008663

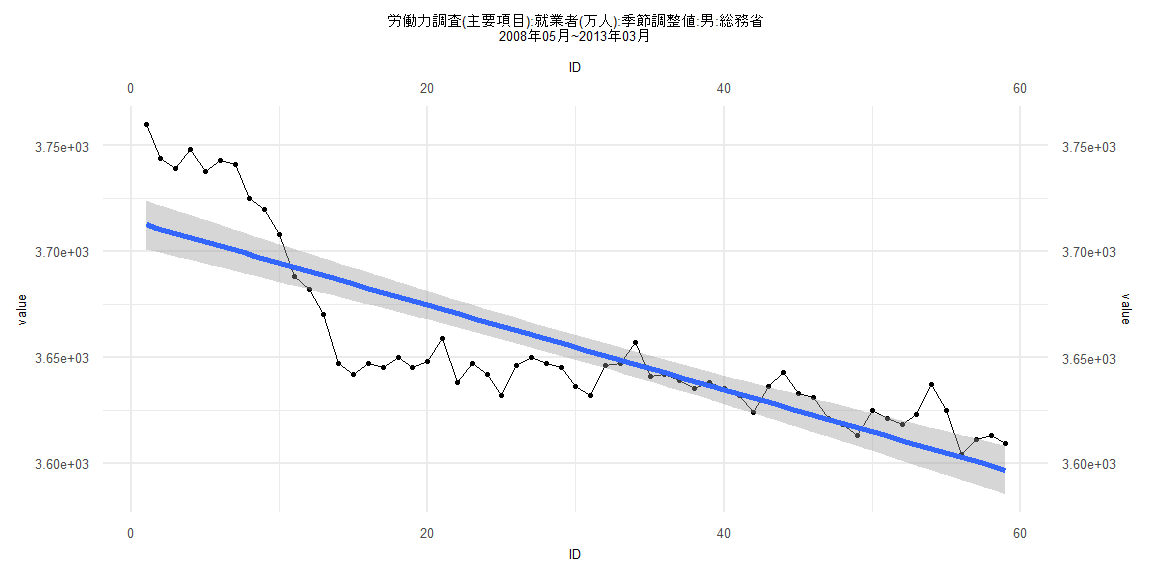

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-42.563 -15.080 -0.615 12.898 47.464

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3714.5336 5.8902 630.6 <0.0000000000000002 ***

ID -1.9980 0.1707 -11.7 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 22.33 on 57 degrees of freedom

Multiple R-squared: 0.7061, Adjusted R-squared: 0.7009

F-statistic: 136.9 on 1 and 57 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.18644, p-value = 0.2582

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.17588, p-value < 0.00000000000000022

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 25.902, df = 1, p-value = 0.0000003593

Box-Ljung test

data: lm_residuals

X-squared = 46.941, df = 1, p-value = 0.000000000007315

Call:

lm(formula = value ~ ID)

Residuals:

Min 1Q Median 3Q Max

-31.955 -10.849 -1.984 11.571 35.457

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3604.04284 3.12127 1154.67 <0.0000000000000002 ***

ID 1.58089 0.06779 23.32 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 13.74 on 77 degrees of freedom

Multiple R-squared: 0.876, Adjusted R-squared: 0.8744

F-statistic: 543.8 on 1 and 77 DF, p-value: < 0.00000000000000022

Two-sample Kolmogorov-Smirnov test

data: lm_residuals and rnorm(n = length(lm_residuals), mean = 0, sd = sd(lm_residuals))

D = 0.12658, p-value = 0.5543

alternative hypothesis: two-sided

Durbin-Watson test

data: value ~ ID

DW = 0.57768, p-value = 0.00000000000001259

alternative hypothesis: true autocorrelation is greater than 0

studentized Breusch-Pagan test

data: value ~ ID

BP = 1.02, df = 1, p-value = 0.3125

Box-Ljung test

data: lm_residuals

X-squared = 40.198, df = 1, p-value = 0.0000000002294