Content

単位根検定・共和分検定

- CADFtest {CADFtest}

- ca.po {urca}

単位根検定

[1] "2019-05-10~2019-09-12"

[1] "n=90"

$DOW30

ADF test

data: x

ADF(0) = -1.7825, p-value = 0.7048

alternative hypothesis: true delta is less than 0

sample estimates:

delta

-0.0736528

$NIKKEI225

ADF test

data: x

ADF(0) = -1.5483, p-value = 0.805

alternative hypothesis: true delta is less than 0

sample estimates:

delta

-0.07242302

$DOW30_Change

ADF test

data: x

ADF(0) = -9.7307, p-value = 0.000000000009647

alternative hypothesis: true delta is less than 0

sample estimates:

delta

-1.055849

$NIKKEI225_Change

ADF test

data: x

ADF(0) = -9.4728, p-value = 0.00000000002239

alternative hypothesis: true delta is less than 0

sample estimates:

delta

-1.033889 共和分検定

[1] "2019-05-10~2019-09-12"

[1] "n=90"

[1] "DOW30 × NIKKEI225"

########################################

# Phillips and Ouliaris Unit Root Test #

########################################

Test of type Pu

detrending of series none

Call:

lm(formula = z[, 1] ~ z[, -1] - 1)

Residuals:

Min 1Q Median 3Q Max

-1148.81 -273.70 73.55 393.96 992.98

Coefficients:

Estimate Std. Error t value Pr(>|t|)

z[, -1] 1.246303 0.002453 508 <0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 491.5 on 89 degrees of freedom

Multiple R-squared: 0.9997, Adjusted R-squared: 0.9997

F-statistic: 2.581e+05 on 1 and 89 DF, p-value: < 0.00000000000000022

Value of test-statistic is: 14.112

Critical values of Pu are:

10pct 5pct 1pct

critical values 20.3933 25.9711 38.3413

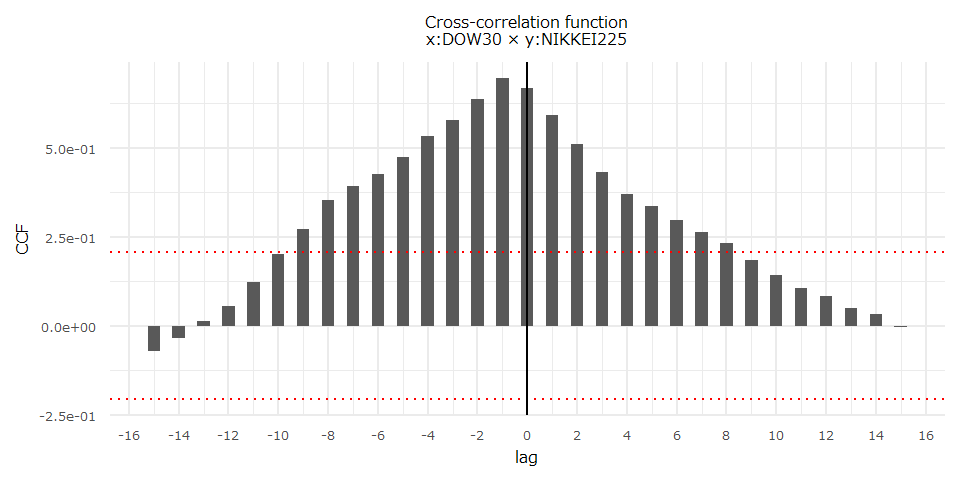

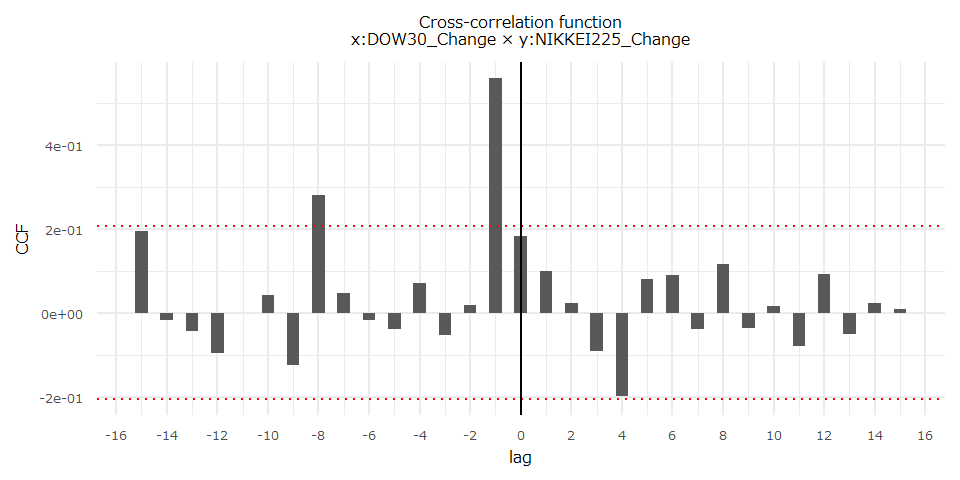

相互相関関数

- ggCcf {forecast}

ベクトル自己回帰モデル

- VARselect {vars}

- VAR {vars}

[1] "2019-05-10~2019-09-12"

[1] "n=90"

VAR Estimation Results:

=========================

Endogenous variables: DOW30, NIKKEI225

Deterministic variables: const

Sample size: 89

Log Likelihood: -1190.034

Roots of the characteristic polynomial:

0.9149 0.8442

Call:

VAR(y = obj, p = selected_lag, type = "const")

Estimation results for equation DOW30:

======================================

DOW30 = DOW30.l1 + NIKKEI225.l1 + const

Estimate Std. Error t value Pr(>|t|)

DOW30.l1 0.95839 0.05215 18.376 <0.0000000000000002 ***

NIKKEI225.l1 -0.04117 0.07948 -0.518 0.606

const 1977.50219 1287.98879 1.535 0.128

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 236.6 on 86 degrees of freedom

Multiple R-Squared: 0.8702, Adjusted R-squared: 0.8672

F-statistic: 288.2 on 2 and 86 DF, p-value: < 0.00000000000000022

Estimation results for equation NIKKEI225:

==========================================

NIKKEI225 = DOW30.l1 + NIKKEI225.l1 + const

Estimate Std. Error t value Pr(>|t|)

DOW30.l1 0.12063 0.03700 3.260 0.0016 **

NIKKEI225.l1 0.80070 0.05638 14.201 <0.0000000000000002 ***

const 1037.83743 913.73636 1.136 0.2592

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 167.9 on 86 degrees of freedom

Multiple R-Squared: 0.8492, Adjusted R-squared: 0.8457

F-statistic: 242.2 on 2 and 86 DF, p-value: < 0.00000000000000022

Covariance matrix of residuals:

DOW30 NIKKEI225

DOW30 55993 8261

NIKKEI225 8261 28181

Correlation matrix of residuals:

DOW30 NIKKEI225

DOW30 1.000 0.208

NIKKEI225 0.208 1.000[1] "2019-05-10~2019-09-12"

[1] "n=90"

VAR Estimation Results:

=========================

Endogenous variables: DOW30_Change, NIKKEI225_Change

Deterministic variables: const

Sample size: 89

Log Likelihood: -205.76

Roots of the characteristic polynomial:

0.3807 0.1457

Call:

VAR(y = obj, p = selected_lag, type = "const")

Estimation results for equation DOW30_Change:

=============================================

DOW30_Change = DOW30_Change.l1 + NIKKEI225_Change.l1 + const

Estimate Std. Error t value Pr(>|t|)

DOW30_Change.l1 -0.11047 0.10838 -1.019 0.311

NIKKEI225_Change.l1 0.12746 0.11644 1.095 0.277

const 0.06143 0.09671 0.635 0.527

Residual standard error: 0.9103 on 86 degrees of freedom

Multiple R-Squared: 0.02154, Adjusted R-squared: -0.001213

F-statistic: 0.9467 on 2 and 86 DF, p-value: 0.392

Estimation results for equation NIKKEI225_Change:

=================================================

NIKKEI225_Change = DOW30_Change.l1 + NIKKEI225_Change.l1 + const

Estimate Std. Error t value Pr(>|t|)

DOW30_Change.l1 0.543214 0.084023 6.465 0.00000000588 ***

NIKKEI225_Change.l1 -0.124549 0.090270 -1.380 0.171

const -0.005501 0.074972 -0.073 0.942

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.7058 on 86 degrees of freedom

Multiple R-Squared: 0.3273, Adjusted R-squared: 0.3116

F-statistic: 20.92 on 2 and 86 DF, p-value: 0.00000003953

Covariance matrix of residuals:

DOW30_Change NIKKEI225_Change

DOW30_Change 0.8287 0.1968

NIKKEI225_Change 0.1968 0.4981

Correlation matrix of residuals:

DOW30_Change NIKKEI225_Change

DOW30_Change 1.0000 0.3063

NIKKEI225_Change 0.3063 1.0000

グレンジャー因果

- causality {vars}

Dow → Nikkei

[1] "2019-05-10~2019-09-12"

[1] "n=90"

Granger causality H0: DOW30_Change do not Granger-cause NIKKEI225_Change

data: VAR object var_result

F-Test = 41.797, df1 = 1, df2 = 172, p-value = 0.000000001008Nikkei → Dow

[1] "2019-05-10~2019-09-12"

[1] "n=90"

Granger causality H0: NIKKEI225_Change do not Granger-cause DOW30_Change

data: VAR object var_result

F-Test = 1.1983, df1 = 1, df2 = 172, p-value = 0.2752

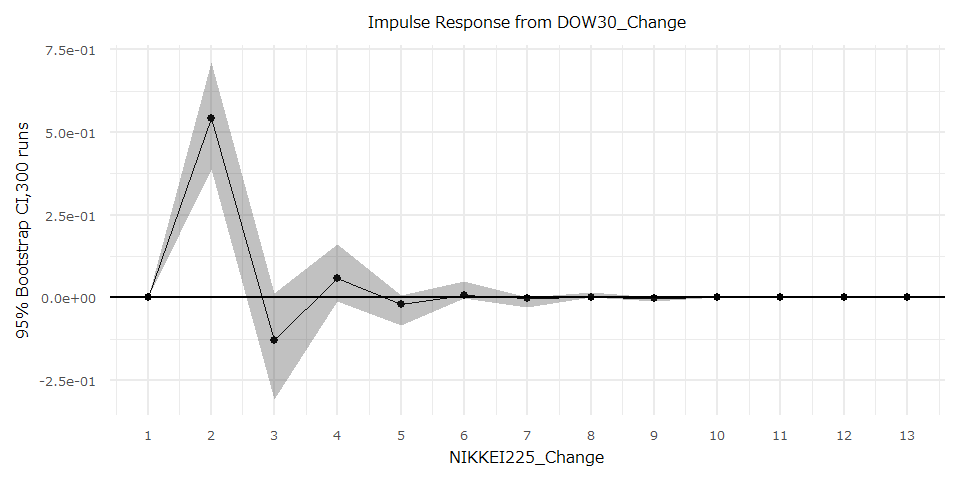

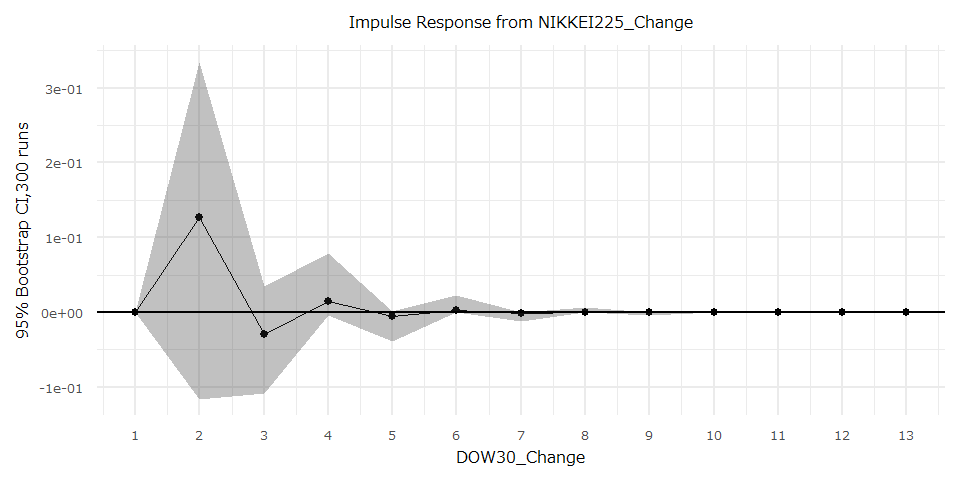

インパルス応答

- irf {vars}

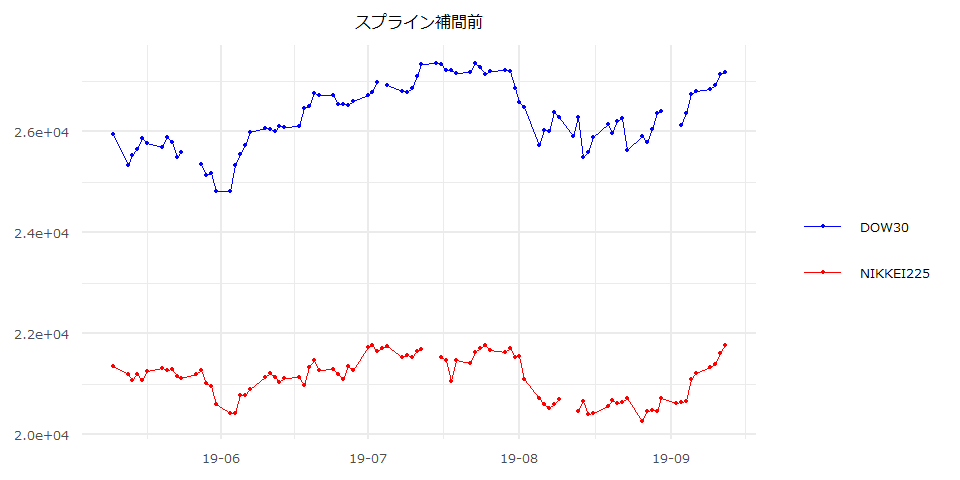

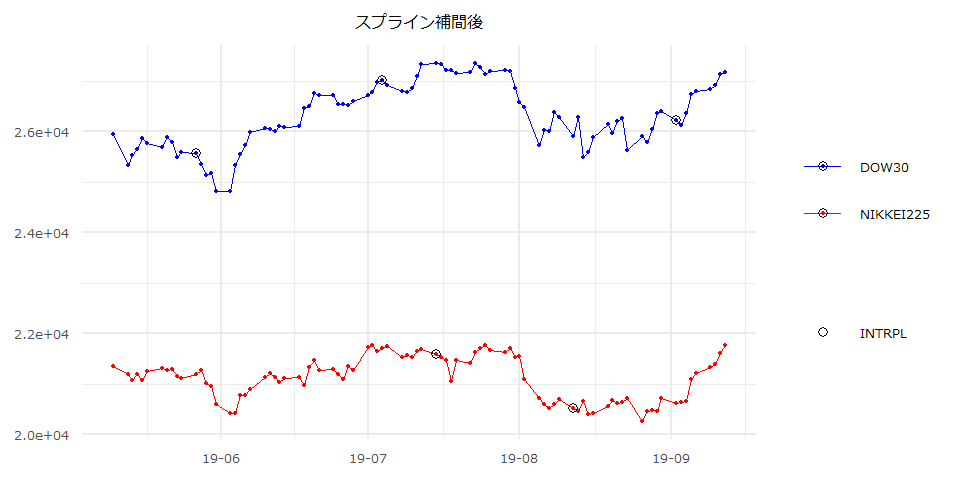

時系列チャート